Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

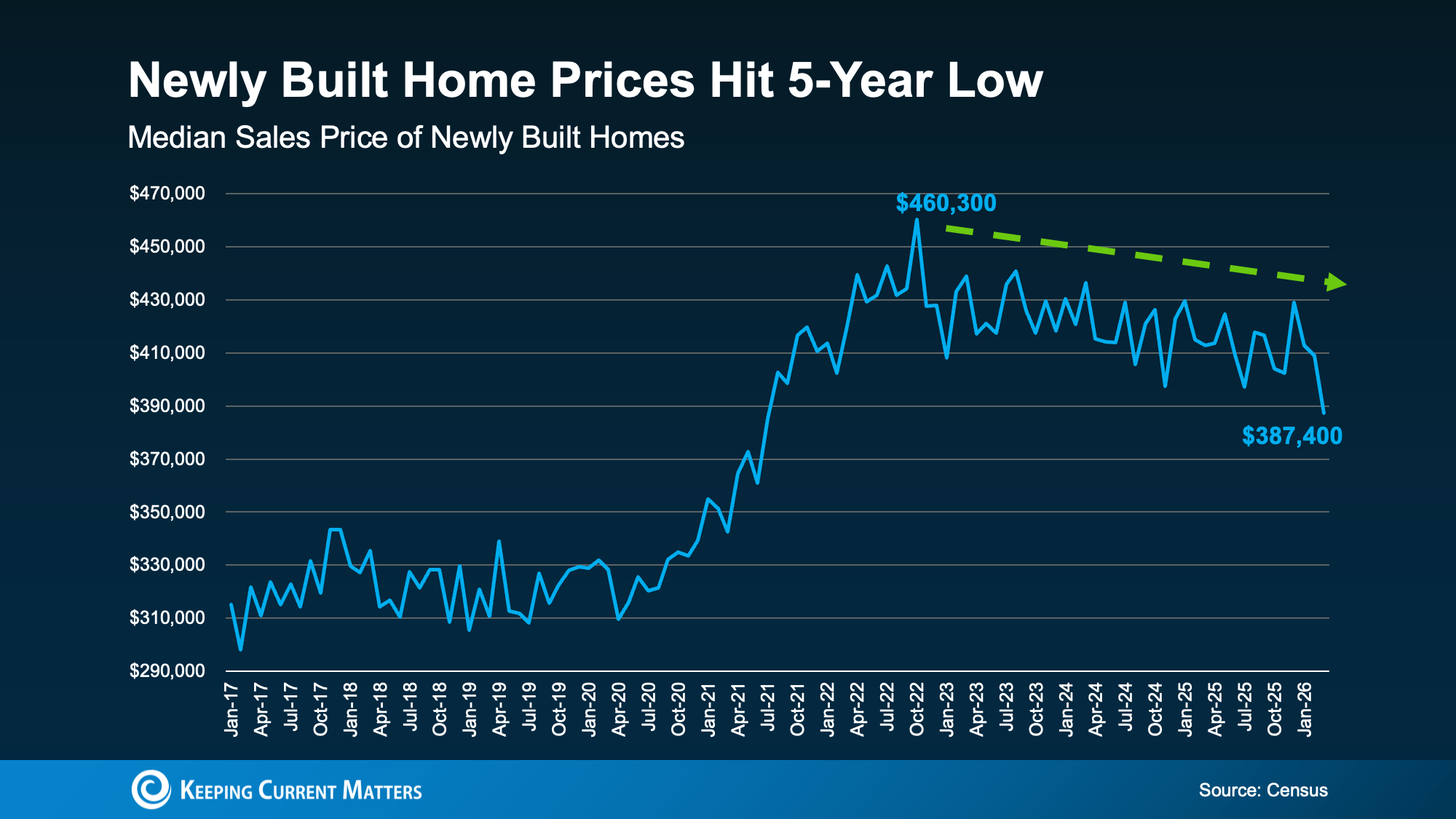

New Home Prices Hit a 5-Year Low

If you’ve assumed a newly built home is out of reach, it may be time to take another look.

The median sale price of a newly built home has dropped to its lowest level since 2021, according to the latest United States Census Bureau data. At the same time, many builders are still offering incentives to help attract buyers.

New Home Prices Have Come Down

After climbing sharply during the pandemic years, new home prices have eased. The median sale price of a newly built home is now around $390,000, which is the lowest level in nearly five years.

Local markets can vary, but the national trend may work in buyers’ favor, especially in the entry-level price range. According to Zonda, prices in the entry-level new construction segment have dropped about 2.7% over the past 12 months, which is more than any other price tier.

This doesn’t mean every newly built home is suddenly affordable now. But, it does mean that buyers may be seeing some of the best new construction pricing since 2021.

Why Lower New Home Prices Do Not Mean a 2008 Repeat

Lower prices can make some buyers wonder whether the new home market is in trouble. But today’s conditions are very different from 2008.

Builders are being more intentional about how much inventory they bring to market. Instead of letting homes pile up, many are using pricing adjustments and incentives to keep inventory moving.

It’s also important to keep perspective. Even with recent price improvements, new home prices are still higher than pre-pandemic norms. This isn’t a market crash. It’s a builder strategy designed to match today’s buyer demand.

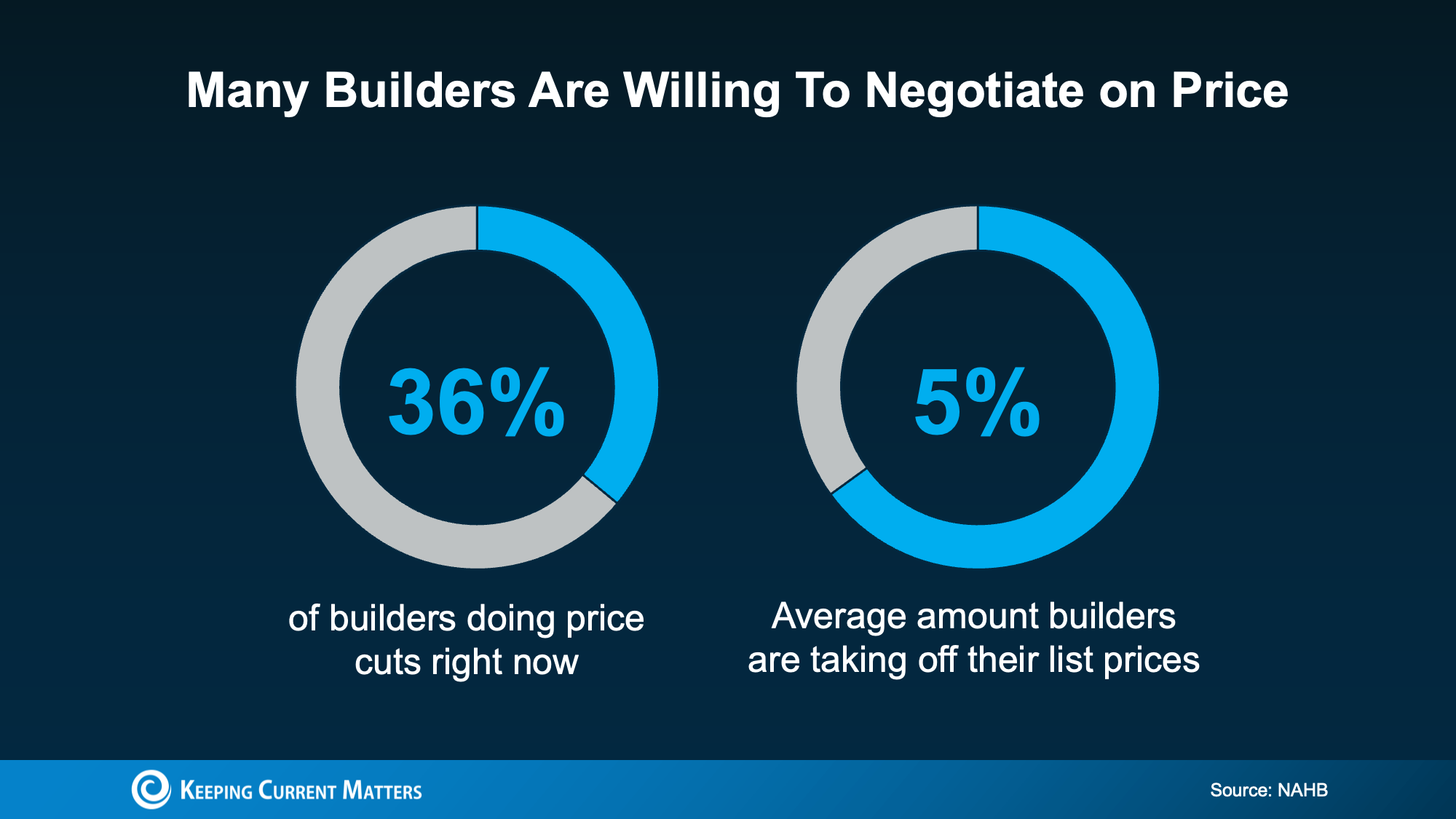

Builders Are Still Offering Buyer Incentives

Lower prices aren’t the only potential advantage for buyers. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers.

Common builder incentives include:

- Closing cost assistance: Some builders may help cover upfront costs, which can reduce the cash buyers need at closing.

- Upgrade packages: Builders might include premium finishes, appliance packages, or design features at no additional cost.

- Mortgage rate buydowns: Some builders might pay to reduce a buyer’s mortgage rate, which can lower the monthly payment.

- Price cuts: More than one in three builders, or 36%, are cutting prices right now, with reductions averaging around 5% off list price.

Why Builders May Be More Flexible Than Sellers

Many buyers assume builders won’t negotiate on price. But builders often have different motivations than individual homeowners.

A homeowner may decide to take a listing off the market rather than accept a lower price. Meanwhile, builders usually need to sell the homes they’ve already built so they can keep projects moving.

As Joel Berner, Senior Economist at Realtor.com, explains:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

That doesn’t mean every builder will negotiate the same way. But it does mean buyers should ask about current pricing, incentives, rate buydowns, and available inventory before assuming a new build is outside their budget.

What This Means for Home Buyers

If you’re shopping for a home, newly built homes may deserve a closer look. Between lower new home prices and ongoing builder incentives, some buyers may find opportunities they did not expect.

Before you make a decision, look at the whole picture:

- The purchase price

- Builder incentives

- Closing cost assistance

- Mortgage rate buydown options

- Included upgrades

- Monthly payment estimates

- Location, commute, and long-term housing needs

A local real estate agent can help you compare new construction homes with existing homes in your market, review builder incentives, and understand what questions to ask before you make a move.

Bottom Line

New home prices have eased, and many builders are still offering incentives to attract buyers. That could give today’s home shoppers more room to explore newly built homes than they’ve had in recent years.

If you’re curious about new construction homes in your area, connect with a local real estate professional to see what’s available and what builder incentives might be offered in your market.

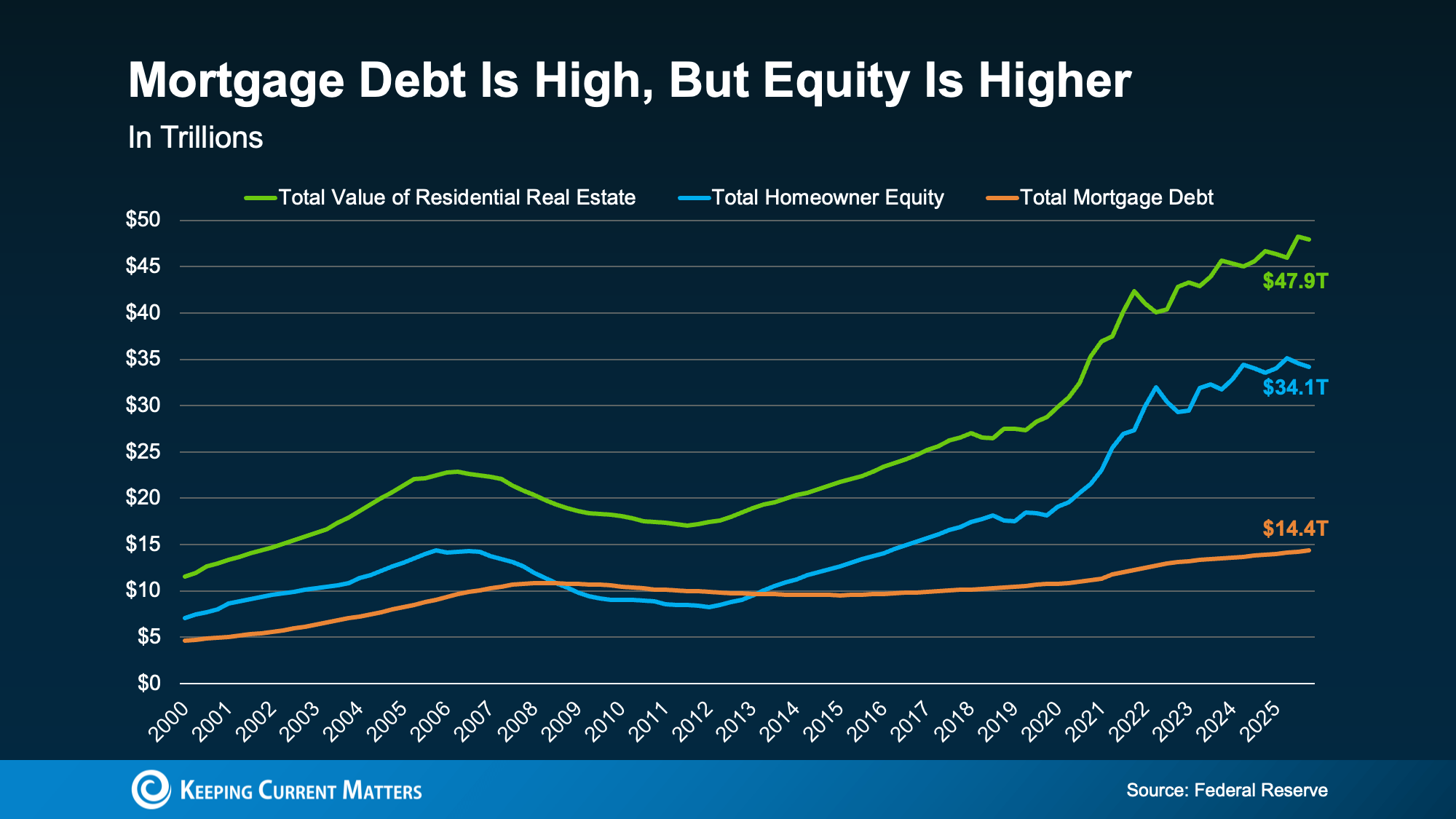

Record High Mortgage Debt: What Do Buyers Need To Know?

Mortgage debt in the United States has hit a record high, and at first glance, that looks like a warning sign for the housing market.

It’s an attention-grabbing headline for sure. After all, when people hear “record debt,” most think back to the 2008 housing crash and wonder if today’s market is heading in the same direction.

But headlines leave out the real story.

It’s true that mortgage debt is higher than ever. But, so are home values and homeowner equity. When you add in those missing pieces, the real picture becomes much less alarming than you might think.

Mortgage Debt Is High, But So Is Homeowner Wealth

New data from the Federal Reserve says total U.S. mortgage debt is now around $14.4 trillion, and the Federal Reserve Bank of New York found it was $13.19 trillion at the end of March 2026. Both numbers are record highs, but they’re missing some critical perspective.

Meanwhile, the total value of U.S. homes is about $47.9 trillion, while homeowners collectively hold roughly $34.1 trillion in equity. In other words, homeowners owe a lot, but they also own a great deal more.

Mortgage debt has peaked, but that alone doesn’t determine the health of the housing market. What matters more is how much equity homeowners have compared to what they owe.

Right now, homeowner equity is more than double the amount of mortgage debt, and near its own historical peak. That’s a very different situation from the years surrounding the 2008 housing crisis.

Why Today’s Housing Market Is Not Like 2008

During the housing crash, many homeowners owed more on their mortgages than their homes were worth. When home prices fell, they had little to no financial cushion. That caused a wave of serious distress, including short sales and foreclosures.

Today’s market looks very different.

Homeowners have significantly more equity than debt, which gives them options. Even if home prices soften in some areas, many owners still have a substantial financial buffer. They can sell, refinance when conditions improve, or use their equity strategically if needed.

That equity cushion is one of the biggest reasons today’s housing market is on much stronger footing than it was during the last crash.

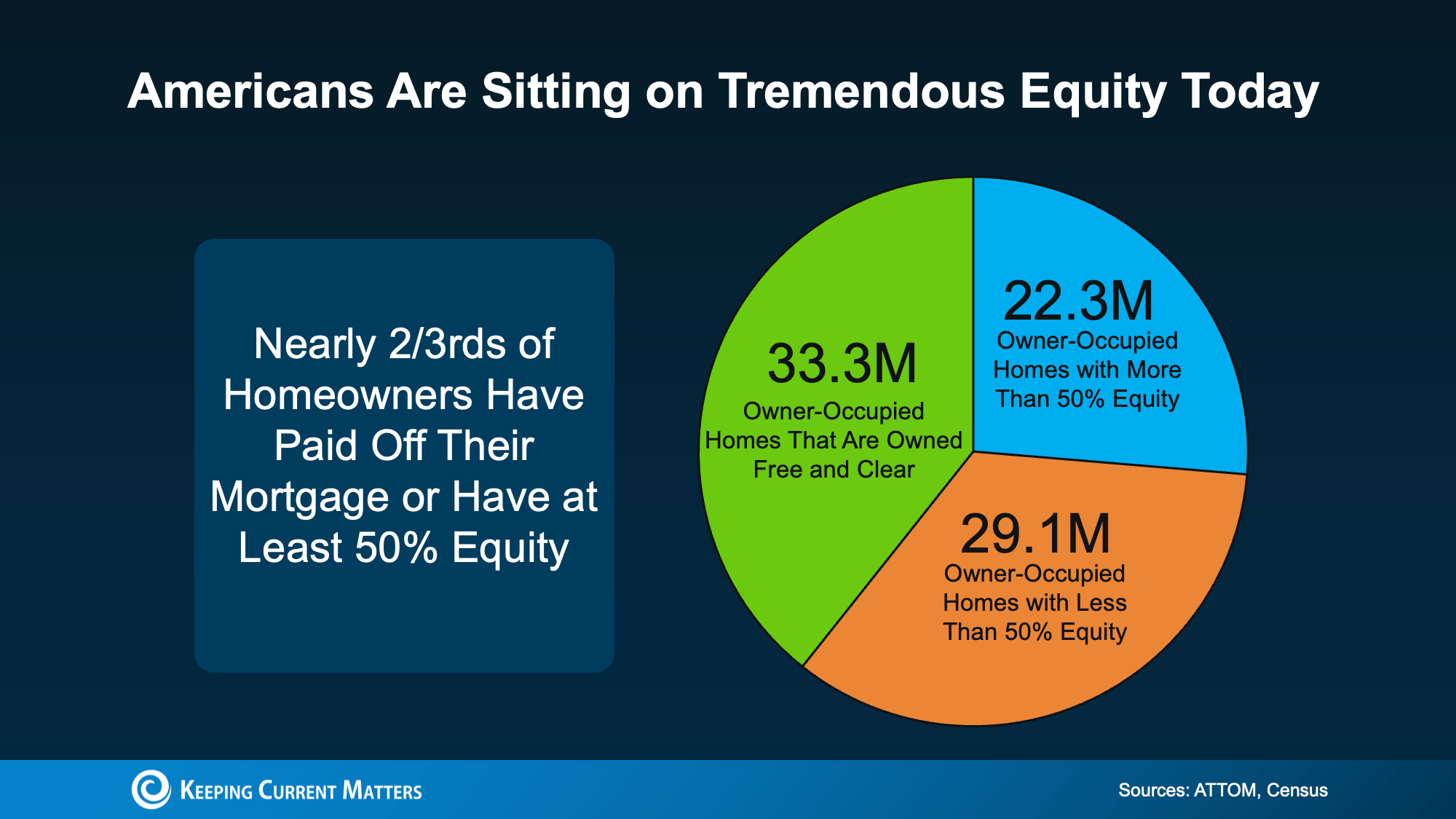

Many Homeowners Have Little or No Mortgage Debt

The strength of today’s market is even clearer when you look at homeowners individually. Recent data from ATTOM and Census illustrate this point.

Of all owner-occupied homes in the United States, 33.3 million are owned free and clear, meaning there’s no mortgage on the property at all. On top of that, 22.3 million homeowners have more than 50% equity in their homes.

Put those groups together, and nearly two-thirds of homeowners are in an exceptionally strong financial position. Some owe no mortgage debt, and others owe far less than their homes are worth.

Those are the signs of a strong market, not a fragile one.

What About Homeowners With Less Than 50% Equity?

The remaining group includes homeowners with less than 50% equity. But these homeowners aren’t necessarily in trouble.

Many of these homeowners are simply recent buyers. Since equity builds over time through mortgage payments and home price appreciation, newer buyers naturally tend to have less equity than people who have owned their homes for years.

Low equity doesn’t always signal financial stress or threat of foreclosure. Often, it just means someone is a first-time buyer in early homeownership.

The Real Story Behind Record Mortgage Debt

Mortgage debt is a critical piece of the housing market’s health, but it’s only one piece it.

When you also consider record or near-record home values, strong homeowner equity, and the number of people who own their homes outright, there’s far less cause for alarm.

Homeowners today aren’t severely overleveraged the way they were before the 2008 crash. Many have meaningful equity, and most have no mortgage debt at all.

Bottom Line: Strong Equity Balances High Debt

Dramatic headlines about record mortgage debt can make it seem like the housing market is in trouble, but the actual data tell a more reassuring story.

Home values are high. Homeowner equity is strong. And a large share of homeowners are in a stable financial position.

So while mortgage debt has reached a record level, today’s market has a much stronger foundation than recent headlines would suggest.

No matter if you’re thinking about buying, selling, or simply trying to understand what these numbers mean for your local market, talking with a trusted real estate professional can help you learn the real story.

Are Home Prices Going To Fall? Here’s What Buyers Should Know

One of the biggest questions buyers are asking right now is: Will home prices fall after I buy?

It’s a common concern. Buying a home is a major financial decision, and no one wants to feel like they bought too early, or too late. With headlines pointing to changing prices in some markets, it’s easy to want to play it safe by waiting.

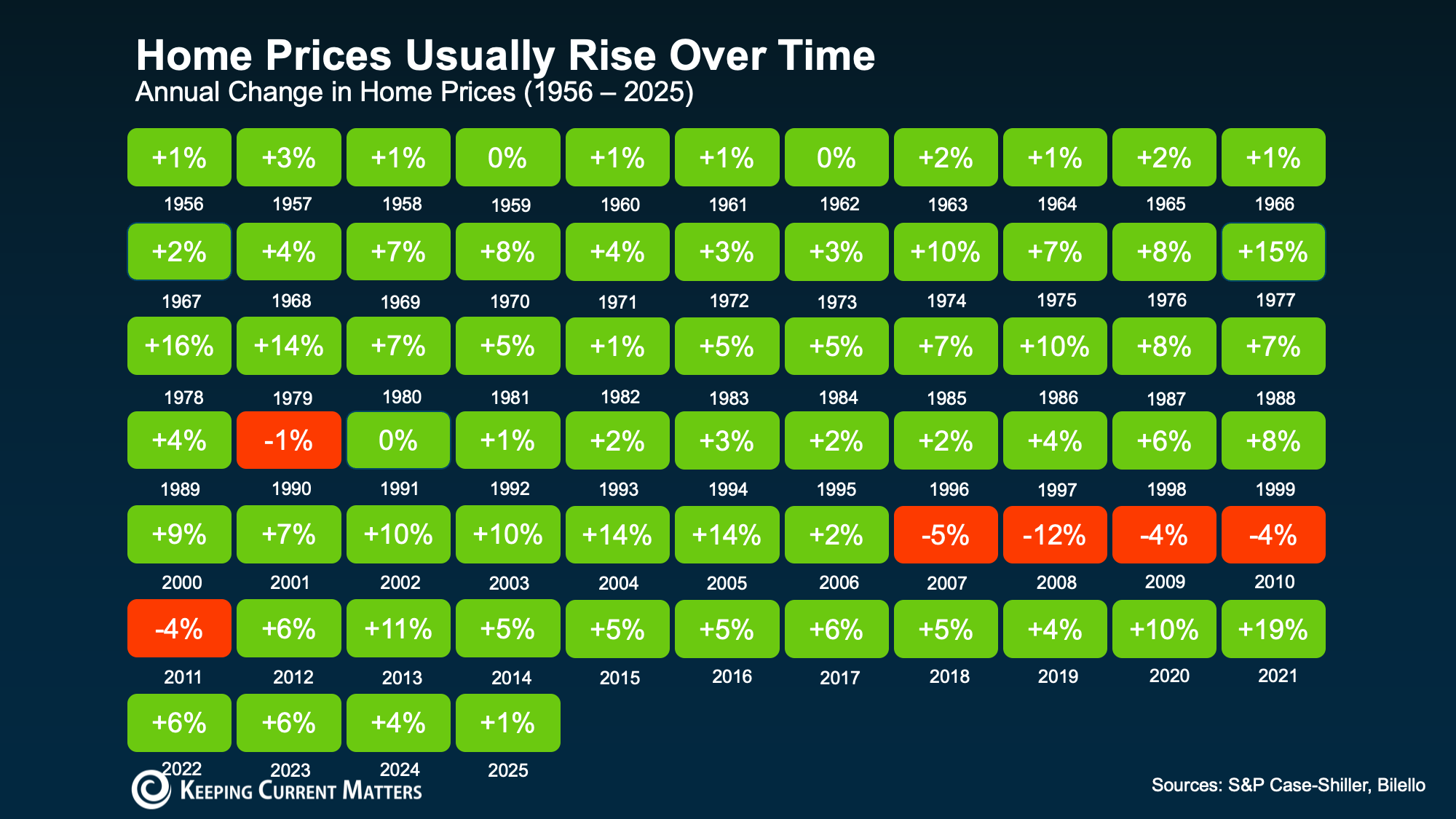

But the short-term noise isn’t the whole story. While some local markets may see temporary dips, the bigger, long-term picture is much different: home prices historically rise over time.

What Housing Market Data Shows

When you look at long-term housing data, one trend becomes clear. Home values have generally moved upward for decades.

Yes, there have been exceptions. The housing crash of 2008 is the most dramatic example. And in some years, certain markets have seen slight declines. But outside of major disruptions, home prices have typically either held steady or increased, and data from Case-Shiller and Biello shows this.

That long-term track record is important for buyers to understand. Real estate is not usually about what happens over the next few weeks or months. It’s about what happens over several years.

Short-term price drops can happen, especially in markets where inventory is rising or buyer demand has cooled. But historically, those dips have proven to be temporary.

Why Home Prices Tend To Rise Over Time

There are several consistent reasons home prices tend to increase in the long run.

People Always Need Homes

Life changes keep the housing market moving. People get married, have children, change jobs, retire, downsize, or relocate to be closer to family. No matter what the market is doing, people always need places to live.

Steady demand like this helps support home values over time.

Housing Supply Is Still Limited

Even though more homes may be available for sale than there were during the tightest years of the market, many areas are still dealing with housing shortages.

When there aren’t enough homes to meet buyer demand, prices tend to stay elevated. Even when demand slows, limited inventory helps prevent dramatic price drops in most markets.

Inflation Plays a Role

Over time, the cost of goods and services tends to rise, and housing is no exception. Land, labor, materials, and construction costs all influence home values.

As the everyday cost of living inflates, home prices naturally move higher too.

What This Means If You’re Thinking About Buying

It’s natural to worry about whether home prices will drop after you buy a home. That concern is especially common among first-time buyers trying to make a smart financial decision.

But what matters most is your own expected timeline.

If you’re planning to buy a home and stay there for several years, short-term market movements matter less. That’s because time gives your home more opportunity to appreciate in value, helping you ride out the kind of ups and downs we’re seeing in some markets.

That’s why many real estate professionals recommend buying only when you expect to stay in the home for at least five years. While there’s no guaranteed timeline, a longer-term approach often gives homeowners a better chance to benefit from rising values.

Real Estate Is Local

Another critical point to remember is that not all housing markets are the same.

Some areas may see home prices soften. Others may continue to rise because demand is strong and inventory remains low. National headlines can give you a general idea of what’s happening, but they don’t always reflect conditions in your specific city, neighborhood, or price range.

That’s why local market insight matters. A trusted real estate agent can help you understand whether prices are rising, flattening, or adjusting in your area.

Don’t Try To Time the Market Perfectly

Trying to buy at the exact bottom of the market is extremely difficult. By the time it’s clear prices have bottomed out, competition may already be increasing again.

Instead of focusing only on timing, focus on whether buying makes sense for your life, your finances, and your long-term goals.

Ask yourself:

- Can I comfortably afford the monthly mortgage payment?

- Do I plan to stay in the home for several years?

- Does buying now support my lifestyle and financial goals?

- Am I prepared for the responsibilities of homeownership?

If the answer is yes, buying may still make sense, even if prices fluctuate in the short term.

Bottom Line: Most Price Drops Are Temporary

So, are home prices going to fall? In some markets, small short-term declines are possible. Historically though, data shows home prices strongly tend to rise over time.

That’s why buying a home is often considered a long-term investment, not a short-term gamble.

You don’t have to buy before you’re ready. But if homeownership fits your goals and you plan to stay put for a while, today’s market headlines shouldn’t scare you away.

For the most reliable picture, talk with a local real estate agent who can explain what home prices are doing in your area and help you decide whether now is the right time to make a move.

What Foreclosure Headlines Are Missing About Today’s Housing Market

You’ve probably seen the headlines: foreclosures are on the rise. And if that immediately makes you think of the 2008 housing crash, you’re not alone.

For many homeowners and buyers, the word “foreclosure” brings back memories of the Great Recession, when distressed properties flooded the market and home values fell sharply. But today’s housing market is very different.

Yes, foreclosure activity has increased, but the bigger picture doesn’t point to a crash. Rather, it shows a market slowly shifting back to normal after several unusual years.

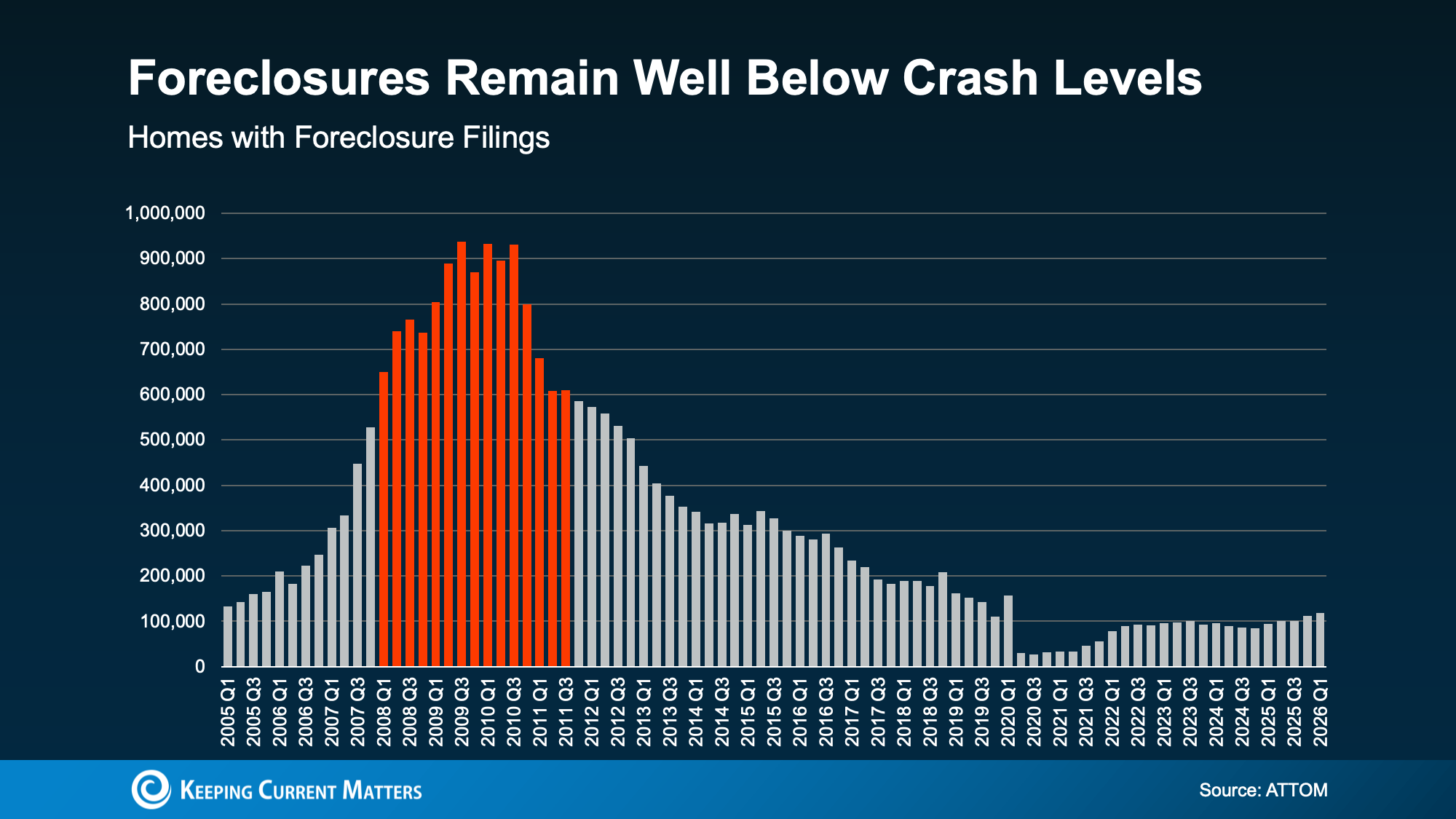

Foreclosures Are Rising, But Still Down Historically

According to data from ATTOM, foreclosure filings are up 26% compared to a year ago and have now increased for five straight quarters. That’s definitely worthy of attention, but it doesn’t mean the housing market is in trouble.

A clear perspective requires a bit of context.

Foreclosure numbers were unusually low in 2020 and 2021 because of pandemic-era protections, including the government’s foreclosure moratorium. Those were exceptional years with totally abnormal market conditions.

A better comparison is 2017, 2018, and 2019, which were the last few years before the pandemic disrupted the housing market. When you compare today’s foreclosure activity to those years, filings are still lower than pre-pandemic levels.

This shows the current increase in foreclosures is more about normalization than distress. The market isn’t returning to 2008 conditions: it’s slowly moving back toward a more typical level of activity.

And compared to the foreclosure wave during 2008 the housing crash, today’s numbers remain far, far lower.

Why Today Is Not Like 2008

One of the biggest differences between now and 2008 is homeowner equity.

During the last housing crash, many homeowners owed more on their mortgages than their homes were worth. That left them with few to no options. Selling often wasn’t possible because selling wouldn’t cover their remaining mortgage balance. For many people, foreclosure became the only path forward.

Today, most homeowners are in a much stronger position.

According to Cotality, the average homeowner has roughly $295,000 in home equity. Home equity like that creates options, even for someone who is struggling financially.

If a homeowner has enough equity to cover their mortgage balance and selling costs, they may be able to sell their home, pay off what they owe, protect their credit, and potentially walk away with money.

That’s a very different picture from 2008, and one that doesn’t point to foreclosures rising out of control.

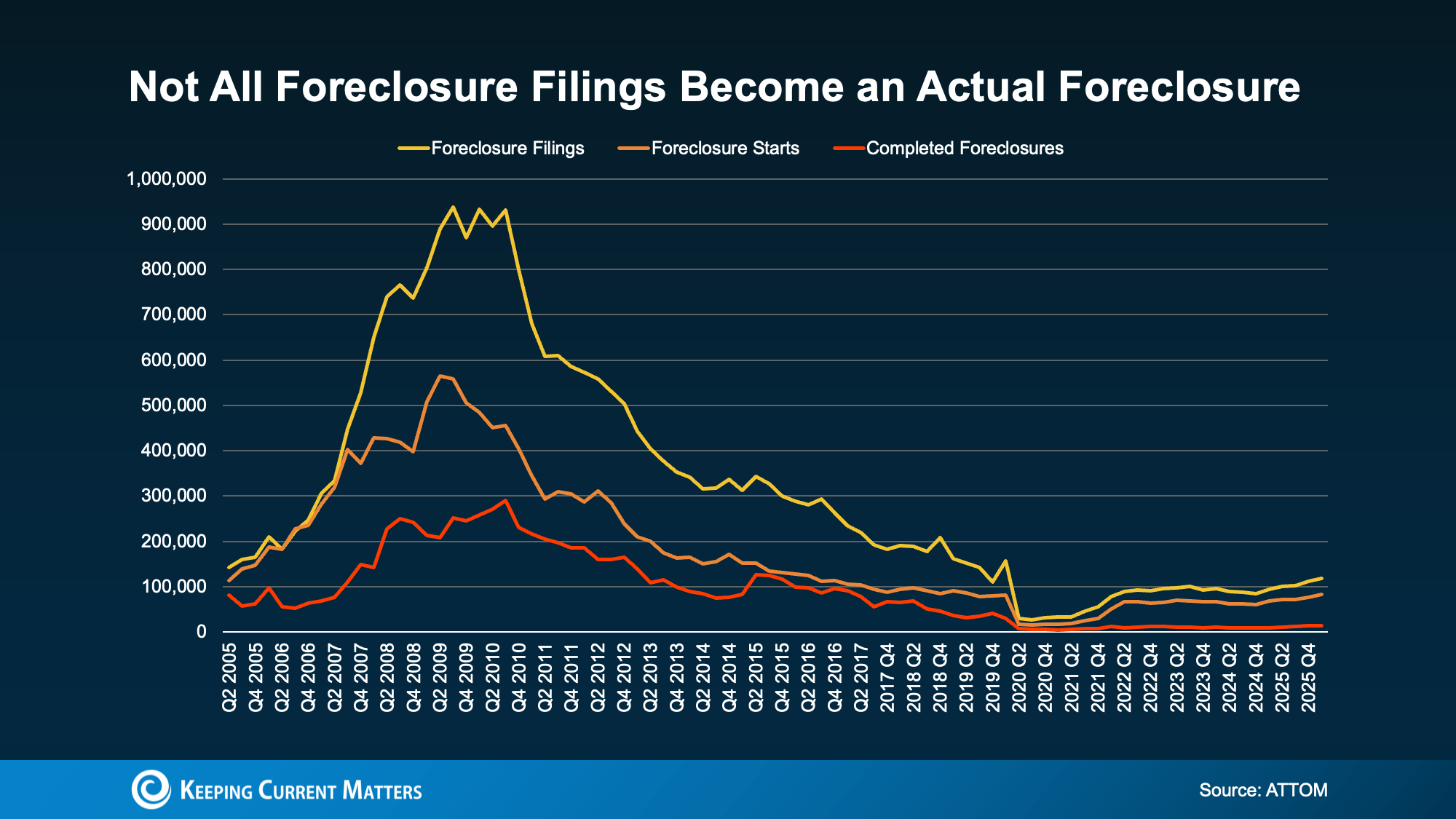

Foreclosure Filings Don’t Always Lead to Foreclosure

Another important point that often gets lost in the headlines is this: a foreclosure filing does not always mean someone loses their home.

Foreclosure filings only show that the process has started, but many homeowners find a solution before the process is completed. Some work out an agreement with their lender. Others sell their home before foreclosure is finalized. Some may qualify for loan modifications or other assistance.

That’s why completed foreclosures are typically much lower than total foreclosure filings.

According to ATTOM’s data, completed foreclosures have barely risen despite the jump in filings. The home equity that many homeowner’s have now is a huge reason for this. Strong homeowner equity gives many people a path forward that doesn’t end in losing their home.

Struggling Homeowners Still Have Options

If you’re behind on mortgage payments or worried you may fall behind soon, the most important thing to know is that you may have more options than you think.

Missing a payment does not automatically mean you’ll lose your home.

Most lenders would rather work with you than go through foreclosure; the process is costly and time-consuming for them too. Depending on your situation, they may be able to discuss options such as:

- A repayment plan

- Temporary forbearance

- Loan modification

- Other hardship assistance programs

The sooner you contact your lender, the sooner you’ll be able to explore your options. Waiting too long can make the situation more difficult, especially in states where the foreclosure process moves quickly.

And if selling your home becomes your best option, talking with a real estate professional can help you understand your home’s current value, your equity position, and whether selling could help you avoid foreclosure.

Bottom Line: Don’t Panic

Foreclosure filings are rising, but that doesn’t mean the housing market is headed for another crash. Today’s numbers are still low compared to historical levels, and the equity homeowners have built gives many people options they didn’t have in 2008.

Online headlines and discussion may sound alarming, but the full story is much more reassuring. This is not a repeat of the last housing crisis. It’s a normalizing housing market, and one supported by much stronger homeowner equity.

Why Staging Your House Could Help It Sell Faster This Spring

Selling your house this spring? Before your listing goes live, there’s one step that could make a meaningful difference in how buyers see your home: staging.

Home staging is more than making a house look pretty for photos. It helps buyers picture themselves living in the space, which can lead to more interest, stronger offers, and a faster sale. And in a market where buyers have more options to choose from, first impressions matter more than ever.

As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), explains:

“Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.”

Here’s why staging your house could pay off this spring, plus a few options to fit different budgets.

What Is Home Staging?

Home staging is the process of preparing your home so it appeals to the widest pool of potential buyers. The idea is to make each space feel clean, open, functional, and inviting.

That may include:

- Decluttering countertops, closets, and storage areas

- Deep cleaning every room

- Rearranging furniture to improve flow

- Removing overly personal items

- Adding simple décor, lighting, or fresh linens

- Highlighting key features like natural light, fireplaces, or outdoor spaces

Staging helps buyers focus on the home itself instead of distractions. When a home feels spacious and well cared for, buyers are more likely to connect emotionally with the property, and more likely to make an offer.

Why Staging Your House Is Worth It

A well-staged home can help your listing stand out both online and in person. And since most buyers start their search by scrolling through photos, your home needs to make a strong first impression.

Staging can help:

1. Your Home Look Better in Listing Photos

Professional photos are one of the most important tools in your marketing plan. Staged rooms tend to look brighter, cleaner, and more balanced, which can encourage more buyers to schedule a showing.

2. Buyers Understand the Space

Empty rooms can sometimes feel smaller than they really are. On the other hand, crowded or poorly arranged rooms can make a home feel cramped. Staging shows buyers how each area can be used, from a cozy living room to a flexible home office.

3. Your House Sell Faster

Staged homes have been shown to sell significantly faster than unstaged homes. Redfin reports that staged homes sell up to 73% faster and often close in under a month. Meanwhile, vacant homes might sit on the market from two to three months, and that’s if they sell.

4. You See a Stronger Return

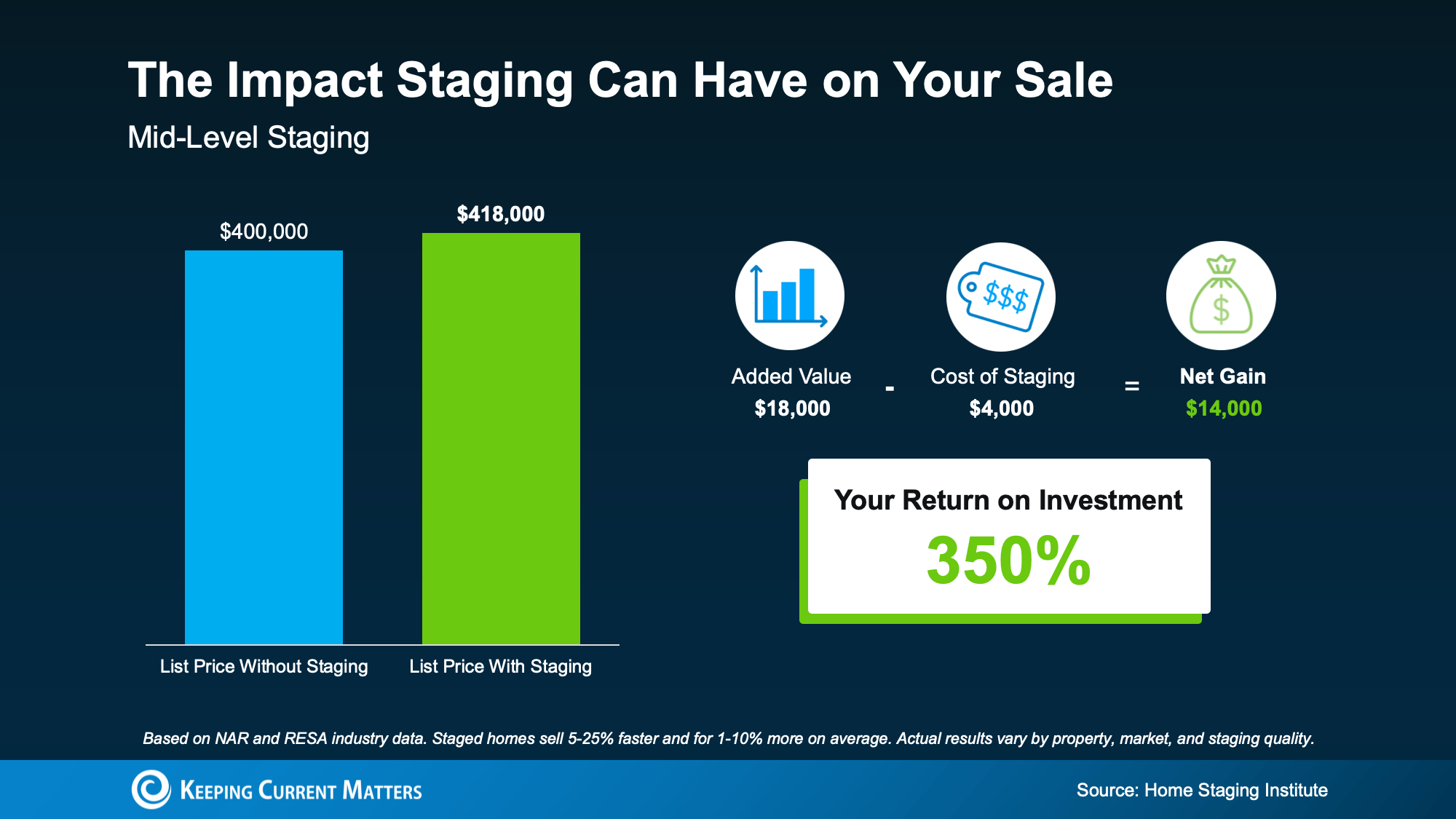

Staging does require an investment, but it may pay off. The Home Staging Institute claims mid-level staging can deliver roughly a 350% return on investment, especially when it helps a home sell for more or reduces time on market.

Home Staging Options for Different Budgets

Staging your house doesn’t need to mean hiring a full-service staging company or renting furniture for every room. There are several ways to approach it based on your timeline, budget, and the condition of your home.

Most Expensive: Professional Staging

A professional stager can handle the full process, including furniture layout, décor, and design details. This option can be especially helpful if your home is vacant, outdated, or otherwise difficult for buyers to visualize.

Professional staging often costs more, but it can create a polished look that photographs well and attracts more buyers.

Less Expensive: Virtual Staging

Virtual staging uses digital furniture and décor in listing photos. This can be a cost-effective option for vacant homes, especially when you want buyers to see the potential of each room.

Keep in mind that buyers should still understand what the home looks like in person, so your agent can help you decide when virtual staging makes sense.

Least Expensive: DIY Staging

If your home is already in good condition, DIY staging may be enough. Simple updates like decluttering, cleaning, rearranging furniture, and adding fresh towels or neutral bedding can make a noticeable difference.

This is often the most budget-friendly option and will still help your home feel more move-in ready.

Ask Your Real Estate Agent What Buyers Expect

Before you spend money on staging, talk with your real estate agent. Agents see how buyers respond during showings and open houses, so they can recommend which updates are worth your time and which ones may not be necessary.

For example, your agent may suggest focusing on the living room, kitchen, primary bedroom, and entryway first. These are often the spaces that create the strongest first impression. An expert agent will know how to best use staging to leverage your home’s own unique strengths and personality.

Bottom Line: Consider Staging For Your Selling Strategy

Staging your house can help it look its best, attract more buyers, and potentially sell faster this spring. Whether you choose professional staging, virtual staging, or a simple DIY approach, the right preparation can make your home more appealing in a competitive market.

Before you list, connect with a local real estate agent to decide which level of staging makes the most sense for your home, budget, and local market.

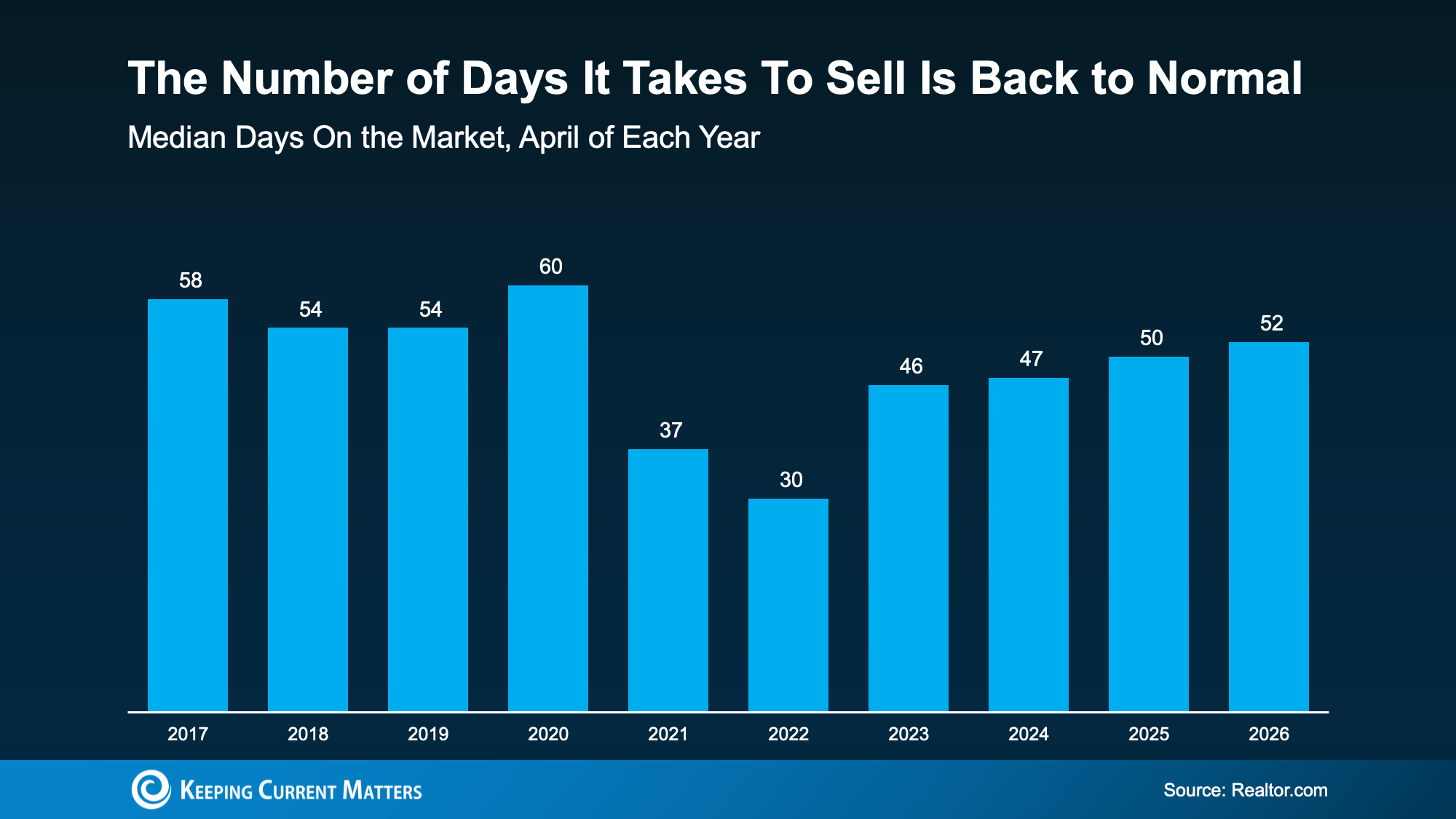

How To Sell Your Home Fast in Any Market

When you list your house, you probably have two goals: sell for a strong price and sell your home fast. But in today’s housing market, homes are taking a little longer to move than they did during the ultra-competitive years.

But in every market, there’s one clear trend standing out:

Well-priced, well-presented homes are still attracting attention and going under contract quickly. The key is making sure your home stands out for the right reasons from the moment it hits the market.

How Long Does It Take To Sell a Home Today?

According to Realtor.com data, homes are selling in about 52 days from listing to closing. That may feel slow if you remember the days when homes seemed to sell almost overnight, but historically, that timeline is much closer to a normal market.

The important thing to understand is this: the market is normalizing, not stopping.

You may still receive an accepted offer much sooner than the full 52-day timeline. In fact, Zillow data says the typical home goes pending or under contract in about 19 days, and some homes move in as little as 7 days.

Why Some Homes Still Sell Quickly

If you want to sell your home fast, location can help, but it’s not the only factor. Even in slower-moving markets, some homes continue to get strong buyer interest because they are positioned correctly.

As Orphe Divounguy, Senior Economist at Zillow, says:

“The cream of the crop is still selling fast, even in markets that have slowed considerably. . .”

That’s the real takeaway. Buyers are still out there, but they’re more selective than ever. Buyers today are comparing homes carefully, looking at price, condition, photos, updates, layout, location, and overall value.

Homes that feel move-in ready and priced appropriately are the ones that tend to rise to the top, and sell the quickest.

The Biggest Reasons Some Homes Sit on the Market

In any market, homes are more likely to sit when they miss the mark on critical buyer expectations. Here are some of the most common issues buyers find:

- The home is priced too high for current market conditions.

- The property needs more work than buyers are willing to take on.

- Listing photos do not make the home look appealing.

- The home is not staged or prepared well.

- The marketing does not highlight the home’s best features.

The Wall Street Journal (WSJ) explains it this way:

“. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready.”

Move-in-ready homes often have an advantage because many buyers are already dealing with higher costs and tighter budgets. A home that feels clean, functional, and well cared is much more attractive.

How To Sell Your Home Fast

The best way to improve your odds of selling quickly is to focus on the things you can control before your home goes live.

1. Price It Strategically

Pricing too high can cause your home to sit, which can lead buyers to wonder what’s wrong with it. A local real estate agent can help you compare your home to similar listings and recent sales so you list at a price that attracts serious buyers.

2. Make a Strong First Impression

Buyers often decide whether they are interested before they ever schedule a showing. Professional photos, curb appeal, decluttering, and simple updates can make a big difference.

3. Highlight What Buyers Care About Most

Your listing should clearly show what makes your home valuable, whether it’s an updated kitchen, a flexible floor plan, a great location, outdoor space, or recent renovations made.

4. Work With a Local Market Expert

A local agent can help you understand what buyers in your area expect, how quickly homes are moving, and what changes might be needed if the market shifts after listing.

Bottom Line: Stand Out Strategically

Today’s real estate market still rewards sellers who use the right strategy. If your goal is to sell your home fast, focus on pricing realistically, preparing your home well, and working with an expert agent who understands your local market.

The homes that stand out are still selling, and sometimes even faster than sellers expect.

4 Ways To Make Your Home Offer Stand Out This Spring

If you’re planning to buy a home this spring, you may have more options than buyers have had in recent years. Home inventory has improved in many markets, and some sellers are more willing to negotiate than they were during the peak of the market.

But that doesn’t mean every homebuyer has an easy path forward.

In popular neighborhoods or areas where there still aren’t enough homes for sale, competition can pick up quickly. And spring is traditionally one of the busiest seasons for real estate, as many buyers hope to move before summer or get settled before the next school year begins.

That’s why making a strong, thoughtful offer still matters. Even in a more balanced market, the right strategy can help your offer stand out when you find a home you love.

Why Strong Offers Still Matter This Spring

Spring often brings more buyers into the market. Experts at Zillow and Realtor.com often say it’s one of the busiest times of year to purchase a home.

More activity can mean more competition, especially for homes that are priced well, located in desirable areas, or move-in ready. So while buyers may have more leverage than they did a few years ago, local market conditions still play a major role.

Here are four ways to give your offer an edge this spring.

1. Start with a Strong and Realistic Offer

It’s always tempting to make a low offer and hope the seller negotiates. In some markets, that approach may work. But if a home is getting a lot of attention, starting too low could cause the seller to move on to another buyer.

Instead, focus on making an offer that is competitive, realistic, and aligned with your local market.

As Bankrate explains:

“There is no magic formula for an optimal home offer. Any offer will be heavily dependent on asking price and local market conditions . . . Your real estate agent will know the local market well and can advise what a competitive — but fair — offer will look like in your area.”

A strong offer doesn’t always mean offering far above asking price. Most times, it means understanding the home’s value, the seller’s position, and how quickly similar homes are selling nearby.

2. Strategize for Multiple Competing Offers

If you find a home that checks all the boxes, another buyer likely feels the same way. That’s why it helps to talk with your agent ahead of time about what you’re willing to do if multiple offers come in.

One option your agent may discuss is an escalation clause. Investopedia defines it this way:

“An escalation clause is a way to automatically escalate your bid by a certain dollar amount, up to a certain ceiling, to compete with other bids.”

This strategy can help you stay competitive without going beyond your comfort zone. The key is setting a clear maximum price before emotions take over.

Still, there are potential risks to understand and keep in mind. If the home appraises for less than your offer price, you may need to cover the difference out of pocket. Your agent can help you decide whether an escalation clause makes sense for your budget and your market.

3. Keep Your Offer as Clean as Possible

Price is important, but it isn’t the only thing sellers consider. The terms of your offer can also make a big difference.

A clean offer is one that feels simple, straightforward, and easy for the seller to accept. That may mean limiting unnecessary requests, being thoughtful about contingencies, or avoiding terms that could make the transaction feel complicated.

As Redfin says:

“Sellers tend to want clean, straightforward offers with minimal strings attached. Keep your requests simple and focus on the essentials.”

This means working with your agent to decide which terms matter most and where you may have flexibility. The trick is to strike a balance, making an attractive offer without giving up important protections.

4. Be Flexible When It Helps the Seller

Sometimes the strongest offer is about more than price. In some cases, there are things that matter to the seller beyond simple dollar amount.

As NerdWallet explains:

“As you prepare an offer, you tend to focus on what the seller has (a house) and what you want (their house). But you’ll gain a competitive edge by viewing the transaction from the seller’s eyes: What does the seller want?”

For example, does the seller need extra time to move? Are they hoping for a quick closing? Would a flexible possession date make the offer more appealing?

Your agent can communicate with the seller’s agent to better understand what matters most. When you can align your offer with the seller’s priorities, you may have a big advantage over buyers who only focus on price.

Bottom Line: The Right Offer Strategy Can Help You Win

Today’s housing market may offer buyers more breathing room, but strong offers still matter, especially during the busy spring season.

If you’re getting ready to buy, work with a trusted local real estate agent who understands your market. The right strategy can help you move quickly, make a competitive offer, and feel confident when the right home comes along.

Is Late May a Good Time To Sell Your House?

If you heard that April 12-18 was the “best week” to list your house, you may be wondering whether you missed your chance to take advantage of the spring market.

Simply put, you didn’t.

While one report from Realtor.com pointed to that specific April week as a strong time for sellers, the truth is there’s rarely just one perfect week to sell your home. Rather, there’s usually a prime selling season, and right now, that window is still very much open.

The Spring Selling Window Is Still Going Strong

Every year, different real estate organizations study the best time to list your house. These reports don’t always point to the exact same week. And that’s not a bad thing.

Why the disconnect? Each study may use different data, market factors, and definitions of what “best” means. Some focus on sale price. Others look at how quickly homes sell, how much buyer demand exists, or how many sellers receive offers above asking.

But even when the exact dates vary, the bigger trend is clear: spring remains one of the strongest seasons for home sellers.

That means if you weren’t quite ready to list earlier in April, you still have time to make a smart move.

Why Late May Can Be a Smart Time To List

According to Zillow, the best time to list your house this year is during the last two weeks of May. That timing matters, especially if your goal is to sell for the strongest possible price.

Zillow’s research shows that homes listed during this late-May window can sell for more. Depending on your local market, price point, and buyer demand, that could mean a noticeably higher sale price.

As Zillow explains:

“Why late spring? Buyer demand typically peaks before Memorial Day. Families want to move during the summer and settle in before the new school year. More buyers shopping at once can spark competition and lift prices.”

That timing makes sense. Many buyers want to be under contract before summer gets too far along, especially if they are trying to move before a new school year starts. When more buyers are actively looking, sellers may benefit from stronger competition.

ATTOM Data found a similar pattern after analyzing nearly 52 million home sales over the past 10 years. Their research shows that May has historically been one of the months when sellers achieve some of the highest returns.

So, while the “best week” may have passed according to one report, the spring window is still open.

What This Means if You’re Thinking About Selling

If you want to sell your house this spring, now is the best time to get serious about preparation.

That doesn’t not mean you need to tackle every home project on your list. When the listing window is short, the goal is to do the right things, not everything at once.

A local real estate agent can help you focus on updates that are most likely to matter to buyers in your area. They can also tell you whether the best time to list your house is slightly different in your specific market.

Here are some quick examples of things you might want to do before you sell, according to Redfin.

Likewise, your own local real estate agent may recommend:

- Improving curb appeal with fresh landscaping or exterior touch-ups.

- Decluttering and deep cleaning key living areas.

- Making small repairs buyers are likely to notice.

- Refreshing paint in high-impact rooms.

- Staging your home to highlight space and flow.

- Pricing strategically based on current local demand.

These steps can help your home make a stronger first impression without wasting time or money on projects that may not deliver a meaningful return.

The Right Strategy Matters More Than Perfect Timing

Timing can absolutely help when you are selling a home. But it’s only one piece of the equation.

To make the most of a late-May listing, your home still needs to be priced well, marketed effectively, and positioned to stand out from other homes on the market. That’s where local real estate expertise becomes especially valuable.

An experienced agent can help you understand what buyers are looking for right now, how much competition you may face, and what steps will help your home attract serious attention quickly.

Bottom Line: Preparation Is Key

Late May could be one of the best times to list your house, especially if you want to take advantage of strong spring buyer demand.

If you’re still thinking about selling, it’s not too late. The key is to act strategically, prepare your home the right way, and work with a local agent who understands your market.

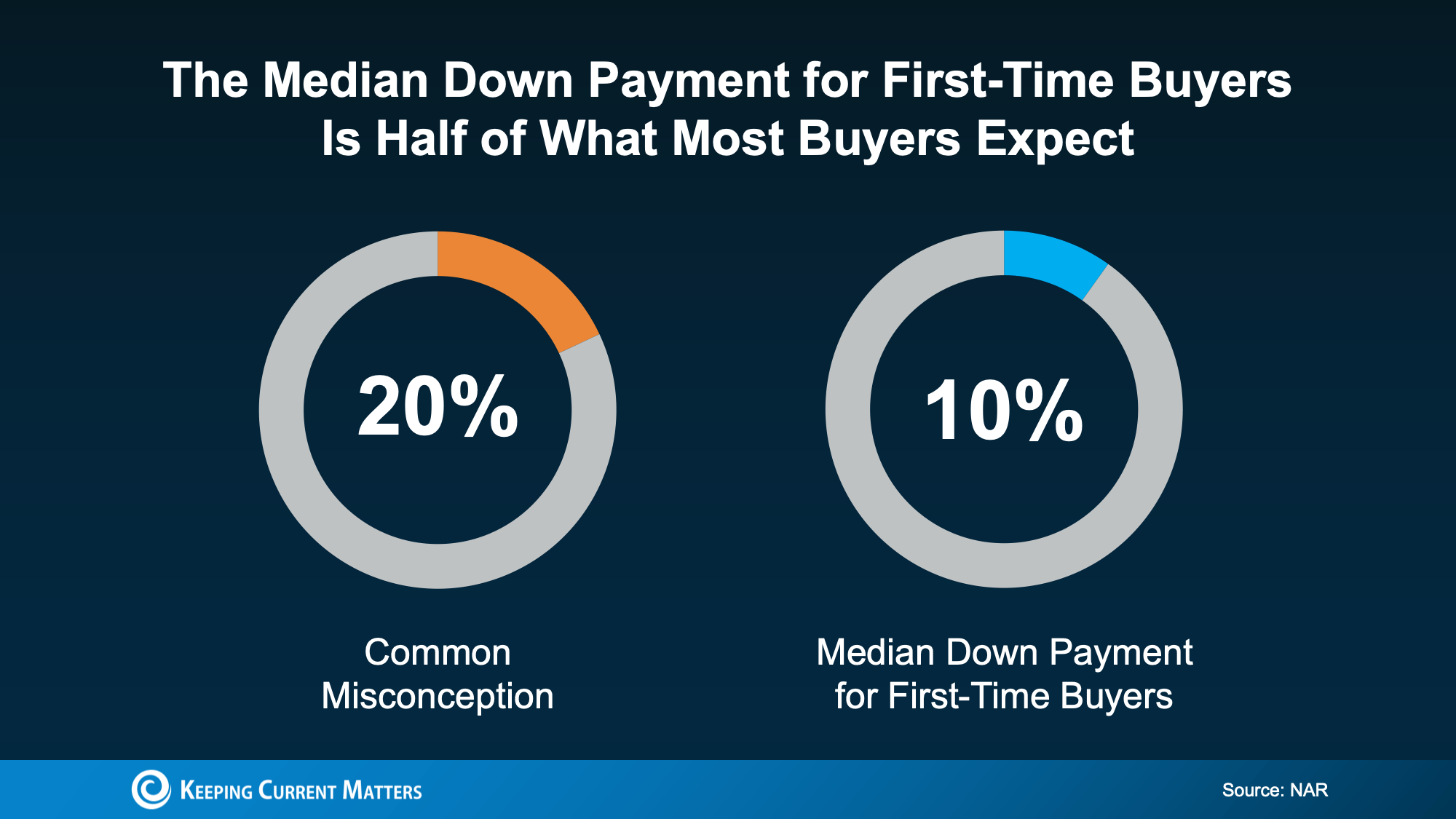

Do You Need 20% Down? Most First-Time Buyers Pay Less

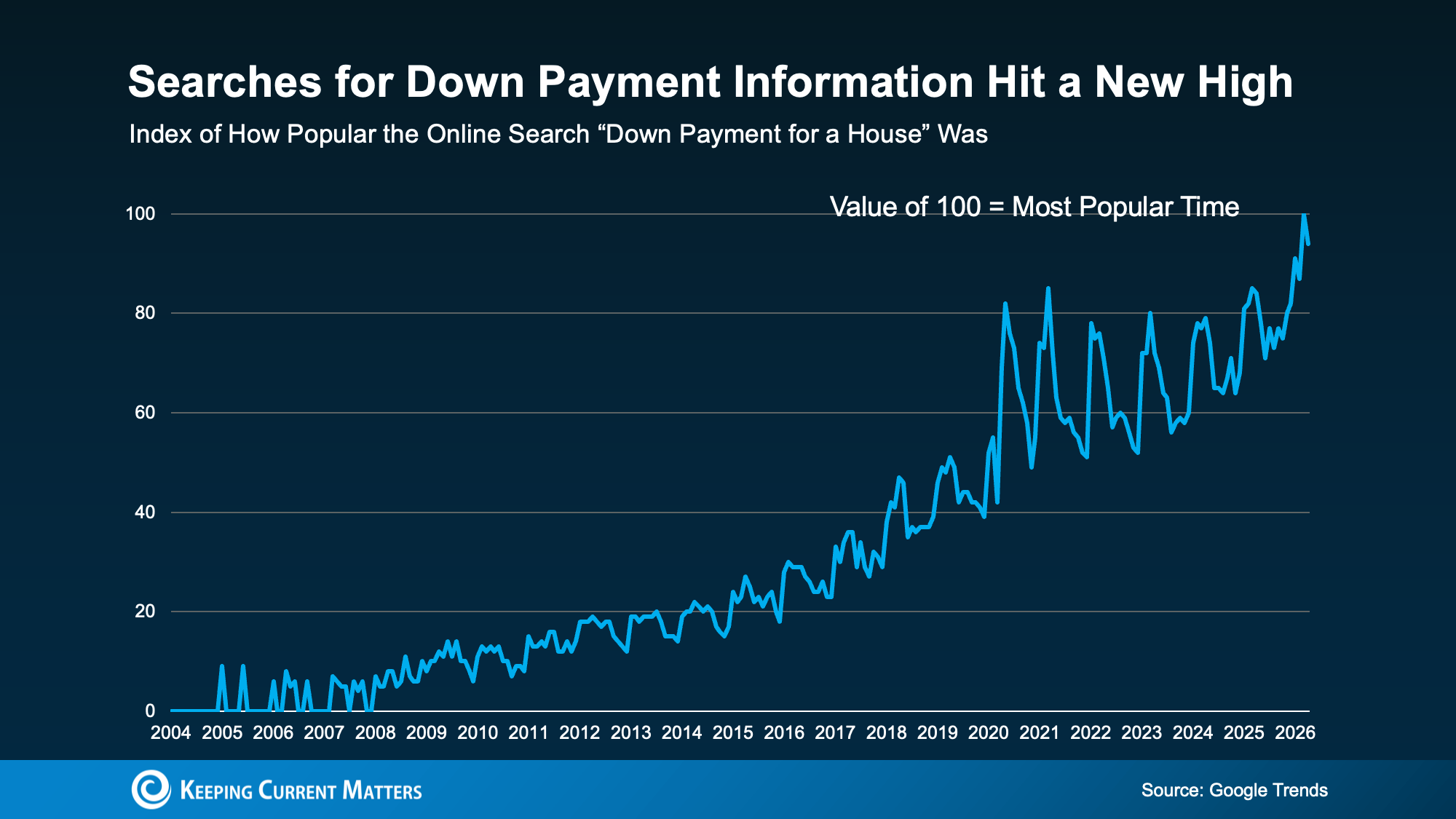

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

CENTURY 21 Affiliated Named Chairman’s Club and President’s Club Awards Winner by CIH | Leads Network

We’re excited to share that CENTURY 21 Affiliated has been named a Chairman’s Club and President’s Club Winner by CIH | Leads Network for its outstanding performance during the past year.

The Chairman’s Club is the highest honor within the CIH | Leads Network, recognizing the top 5 performing brokerages, and placing winners among the top 1% of brokers nationwide. This award is reserved for those who consistently meet rigorous performance standards while delivering unparalleled service to clients and customers. The President’s Club, awarded to the top 25 performers in the network, celebrates the top 5% of brokers who consistently demonstrate excellence and leadership in the real estate industry.

Together, these honors affirm CENTURY 21 Affiliated’s position as a leader within the CIH | Leads Network. Their dedication to delivering exceptional results and fostering collaboration reflects the core values that continue to elevate the Network.

“It is a privilege to celebrate CENTURY 21 Affiliated’s achievements as a Chairman’s Club and President’s Club winner,” said Ashton Alexander, Chief Strategy Officer, CIH | Leads Network. “These awards represent the pinnacle of success within the CIH | Leads Network and are a testament to CENTURY 21 Affiliated’s dedication, leadership and ability to consistently deliver exceptional results. Their accomplishments continue to raise the bar, both within our network and across the industry.”

“Being recognized with both the Chairman’s Club and President’s Club Awards is an incredible honor for our team,” said Kim Yeoman, Vice President of Relocation & Corporate Services at CENTURY 21 Affiliated. “These accolades reflect the hard work, collaboration and commitment we bring to serving our clients every day. It’s a privilege to be counted among the best in the CIH | Leads Network and the real estate industry.”

About Compass International Holdings

Compass, Inc. (“Compass International Holdings”, “CIH” or the “Company”) (NYSE: COMP) is a global real estate services company with a presence in every major U.S. city and approximately 120 countries and territories. Compass International Holdings serves millions of buyers and sellers through a portfolio of some of the most recognized and iconic brands: @properties, Better Homes and Gardens® Real Estate, CENTURY 21®, Christie’s International Real Estate, Coldwell Banker®, Compass, Corcoran®, ERA®, and Sotheby’s International Realty®. Every day, we empower a global network of 300,000 real estate professionals and affiliate broker-owners to grow their businesses and deliver exceptional service to consumers

The Company empowers real estate professionals to streamline operations and seamlessly guide clients through every phase of residential and commercial transactions, leveraging powerful tools, including its modern technology platform. Compass International Holdings brings together integrated services, including brokerage, franchise, mortgage, title, insurance, escrow, and relocation.

CIH | Leads is provided through Anywhere Leads, Inc., which is a business unit within Compass International Holdings. References to “CIH | Leads,” “CIH | Leads Network,” or “Anywhere Leads Network” are intended to describe programs available through Anywhere Leads, Inc.