Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

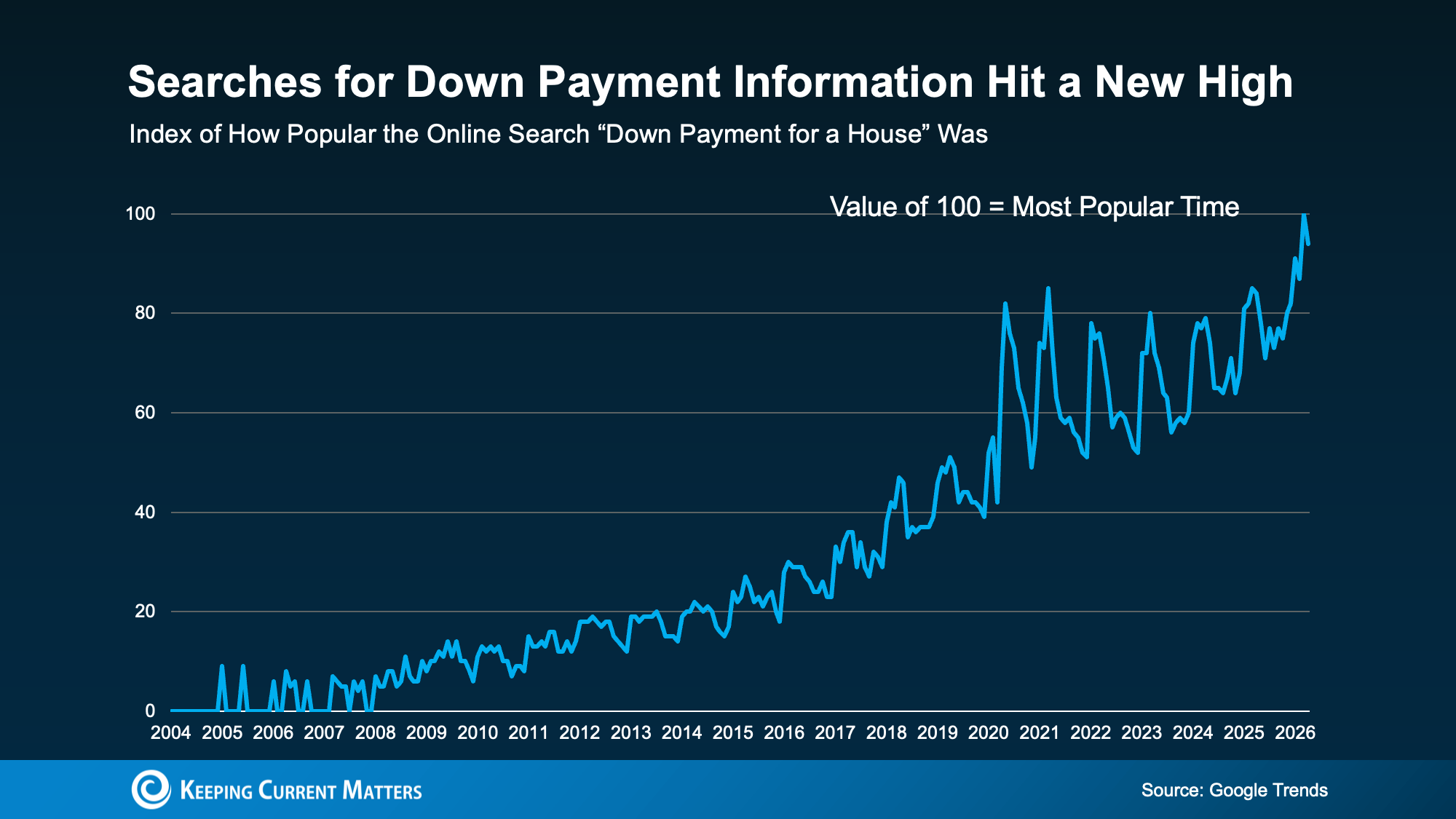

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

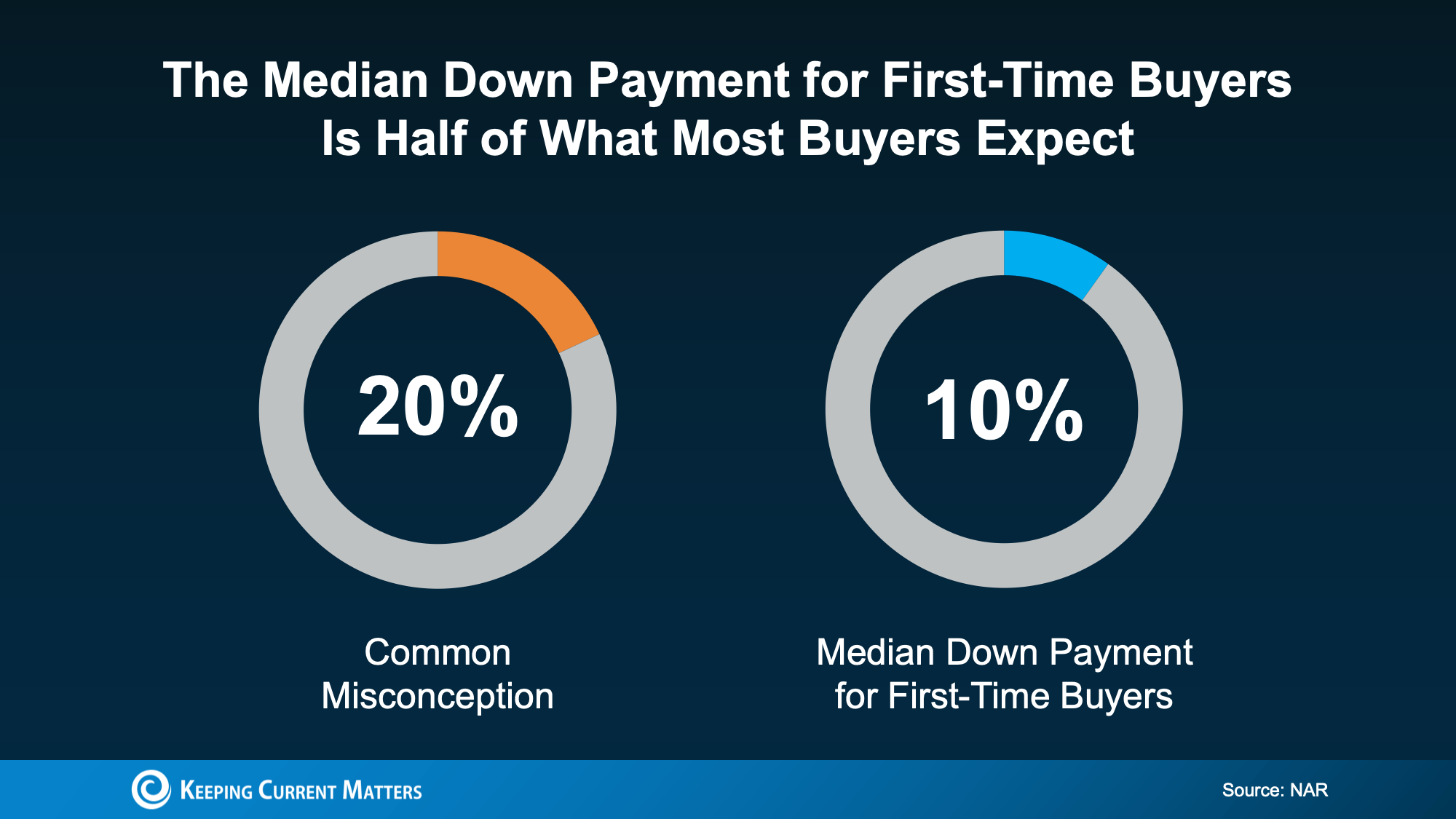

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

3 Things That Aren’t Going To Happen in Today’s Housing Market

There’s no shortage of uncertainty in today’s housing market, and that’s naturally fueling a lot of dramatic headlines. And if you’re trying to buy a home, that kind of noise can make your decision feel a lot more complicated.

In fact, a recent CNBC study asked homebuyers what they’re most concerned about, and the same three topics kept rising to the top:

- Mortgage rates

- The number of homes for sale

- Home prices

The challenge is that much of what people are hearing about these topics is driven by misconceptions, not facts. Let’s separate the headlines from what the data is really showing.

Misconception #1: “I Should Wait Because Mortgage Rates Are Going To Fall Dramatically”

One of the most common ideas circulating on social media is that mortgage rates are about to drop sharply, so waiting to buy is the smarter move.

But is that what experts are expecting?

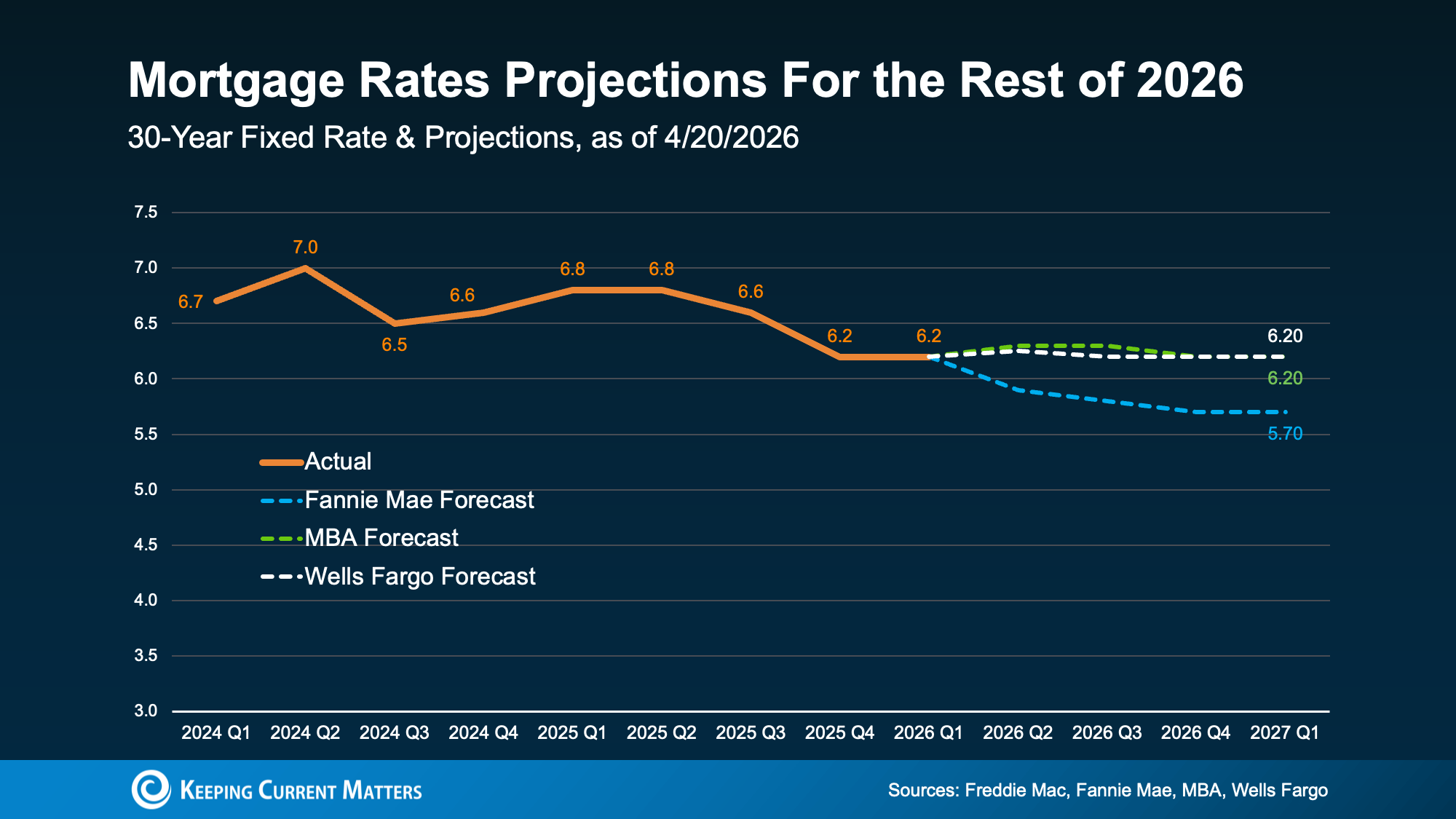

While mortgage rates have eased a little in recent weeks, forecasts still aren’t predicting any major declines. It’s more likely that rates will stay in the low 6% range this year.

And that’s not a remarkable shift from the rates we’re seeing today:

Obviously, a lot depends on inflation and the broader economy. But based on what we know right now, waiting for a big drop in mortgage rates may not play out the way many buyers hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

And even with rates where they are today, buying a home is already more affordable than it was a year ago. Even if rates don’t drop in the near future, home affordability is better now than a year ago.

Misconception #2: “There Are Too Many Homes for Sale”

You may have heard that housing inventory is rising. Nationally, that’s true: the number of homes for sale is 8% higher than it was at this time last year. But that’s not bad news. In lots of markets, it’s easing the pressure on buyers.

The problem is that some headlines make good news sound like bad news. They focus on the fact that inventory is at its highest level since 2019 or highlight how many new homes builders are adding. That can make it sound like supply is growing too much, too fast.

But the bigger picture tells a different story.

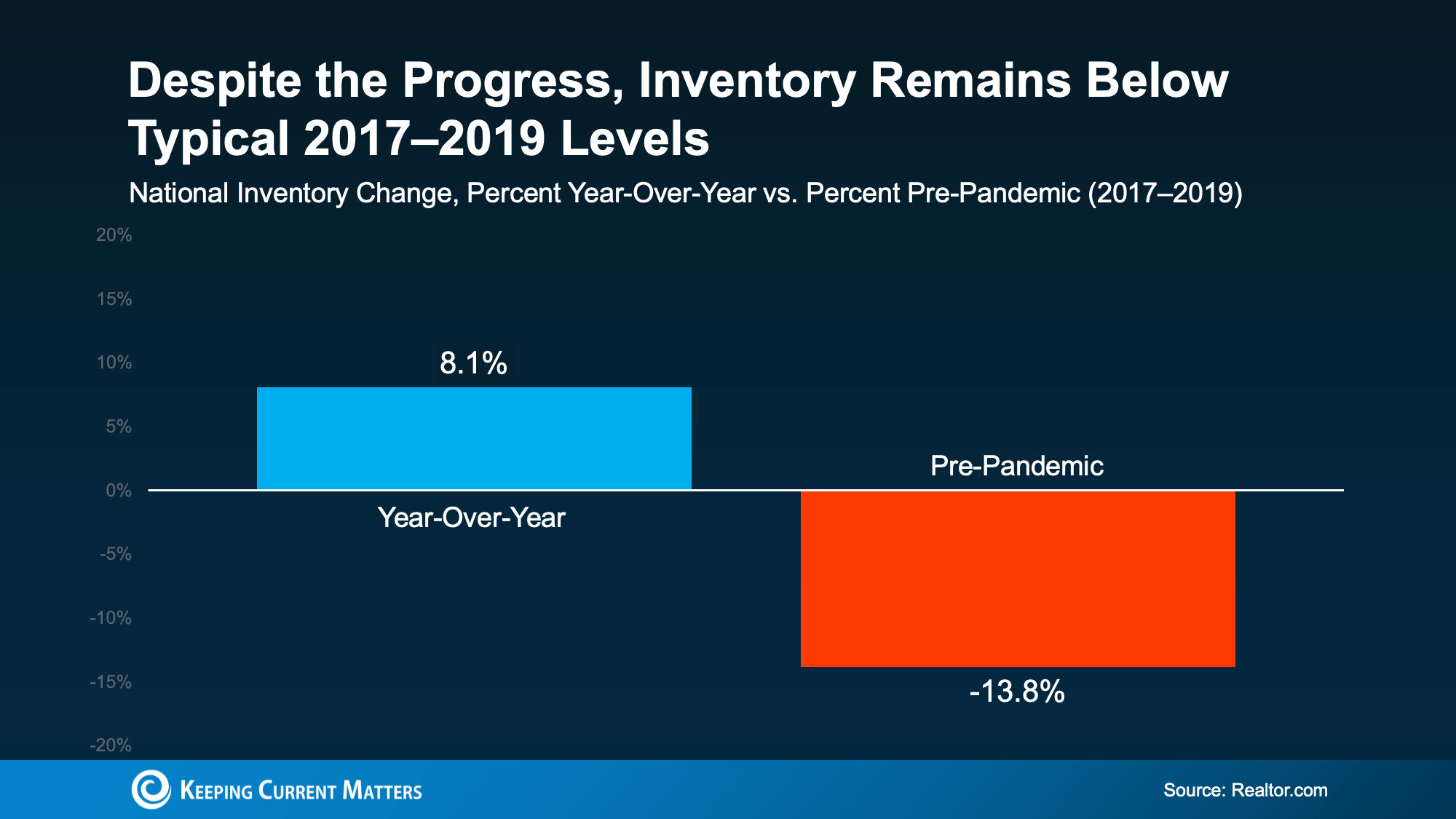

According to new Realtor.com data, even though inventory is up over last year, it’s still nearly 14% lower than it was in the last normal housing market from 2017 to 2019:

And while local conditions vary, only 9 states have more inventory now than they did before the pandemic. That’s a major reason there aren’t enough homes for sale to trigger anything like the 2008 housing crash.

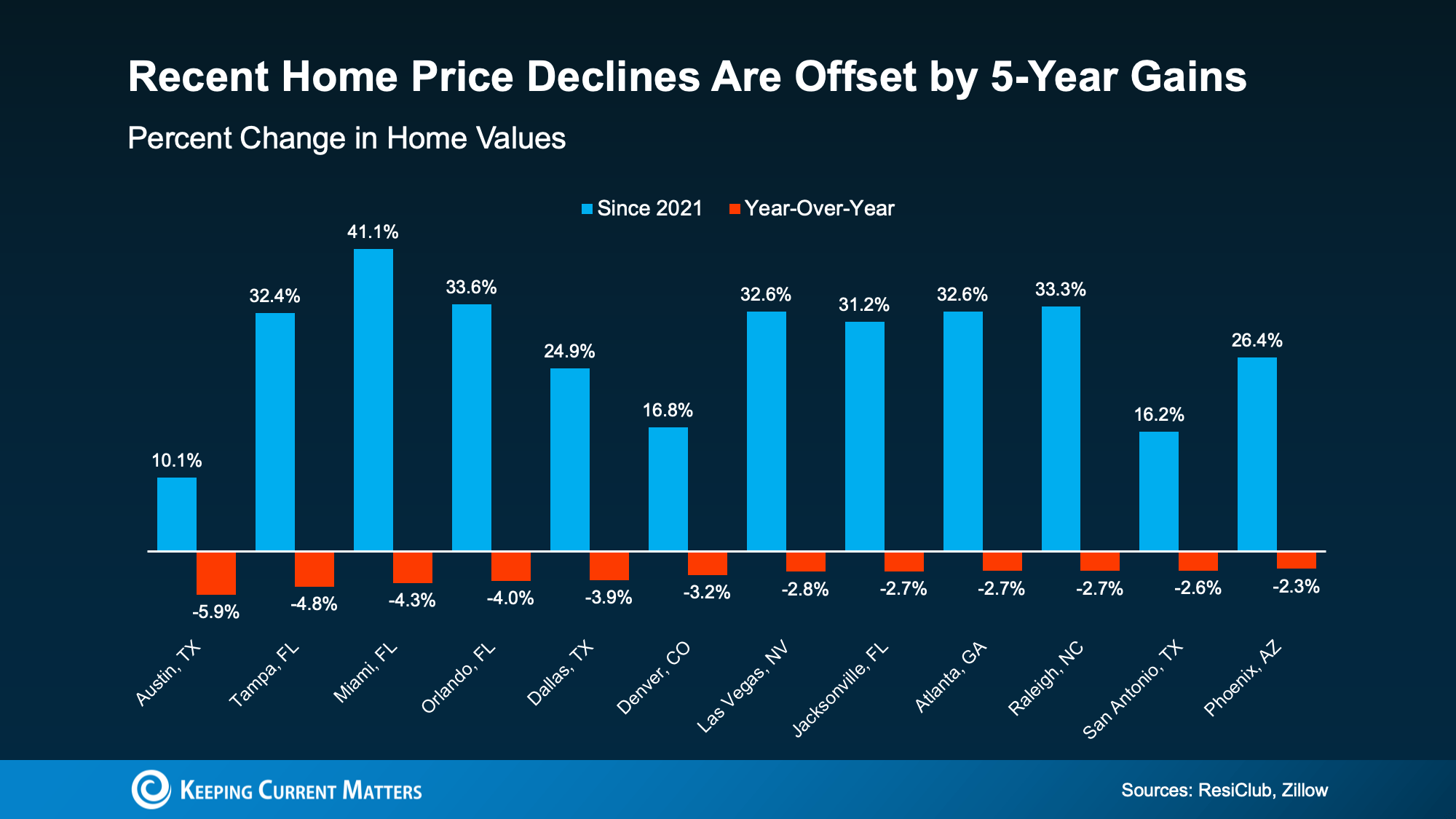

Misconception #3: “Home Prices Are About To Crash”

This is another common headline you’ve probably seen. This misconception comes from the fact that a few metros are actually seeing small price declines. Influencers are pointing to this to claim home prices are crashing. But this is absolutely not true nationally.

In most markets, home prices are still rising, not falling. Here’s why:

- Many homeowners are choosing not to sell to avoid giving up the low mortgage rate they locked in a few years ago. That continues to limit how much inventory can grow.

- Inventory remains below pre-pandemic norms. There still aren’t enough homes for sale to cause a widespread price crash.

- Even in markets with more listings, some sellers are pulling their homes off the market instead of making major price cuts.

Those are three big reasons home prices are not on track for a crash.

And even in the areas seeing small price declines, those drops are nowhere near enough to erase the huge gains most homeowners have built over the past five years:

These drops don’t signal a crash. They show the market settling after a few years of record-breaking spikes in prices.

Bottom Line: Get the Facts on Your Market

The discussions we see online can often exaggerate the negative and ignore the positive, especially in housing. If you want a clearer, truer idea of what’s happening with mortgage rates, housing inventory, and home prices in your market, talk to a trusted real estate professional.

Connect with a local real estate agent so you have an expert who can give you the real story on your local housing market.

Is an Adjustable-Rate Mortgage Right for You? A Homebuyer’s Guide

If you’ve been shopping for a home lately, you’ve likely felt the pressure of today’s affordability challenges. Higher home prices and mortgage rates have made it harder for many buyers to stay within budget. That’s one reason adjustable-rate mortgages, or ARMs, are getting more attention again.

For some homebuyers, an ARM can offer welcome savings upfront. But before you go that route, it’s important to understand how these loans work, why they appeal to certain buyers, and what the long-term risks might be.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage is a home loan that starts with a fixed interest rate for a set number of years. After that initial period ends, the rate can adjust at scheduled intervals based on market conditions.

As Business Insider explains:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

That’s the biggest difference between a fixed-rate mortgage and an ARM. A fixed-rate loan offers predictability, while an ARM may give you a lower payment at first but less certainty later.

It’s true that costs like property taxes and homeowners insurance can still change with a fixed-rate mortgage. But the principal and interest portion of the payment generally stays steady. With an ARM, your monthly payment can rise or fall once the fixed period ends.

Why More Home Buyers Are Considering ARMs

The main reason buyers look at adjustable-rate mortgages is simple: lower initial costs.

Business Insider puts it this way:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

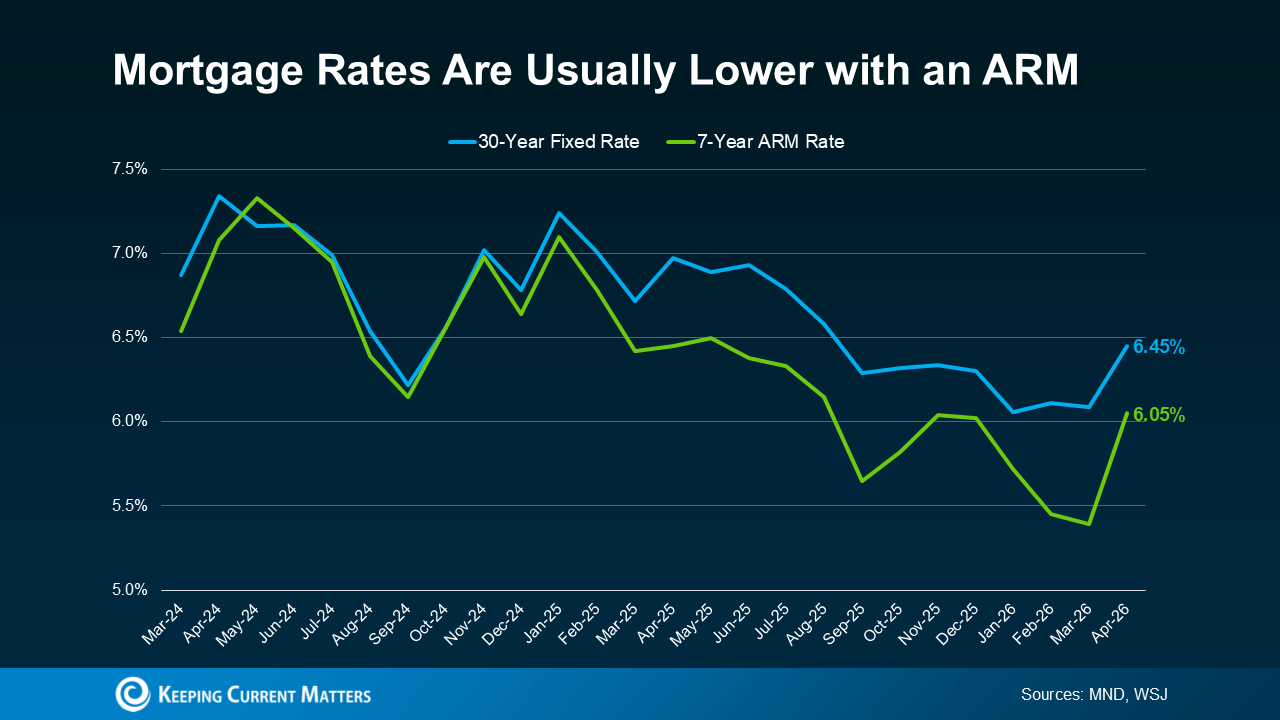

That upfront savings can matter, especially in a market where every dollar counts. Recent reporting from Mortgage News Daily and The Wall Street Journal show that ARM rates have been coming in lower than 30-year fixed mortgage rates.

For many buyers, even modest monthly savings can make a difference. For example, Redfin found that a typical buyer could save about $150 per month by choosing an ARM instead of a 30-year fixed mortgage. Savings like that can help some buyers qualify for a home sooner or make their monthly budget more manageable.

Why Adjustable-Rate Mortgages Are Making a Comeback

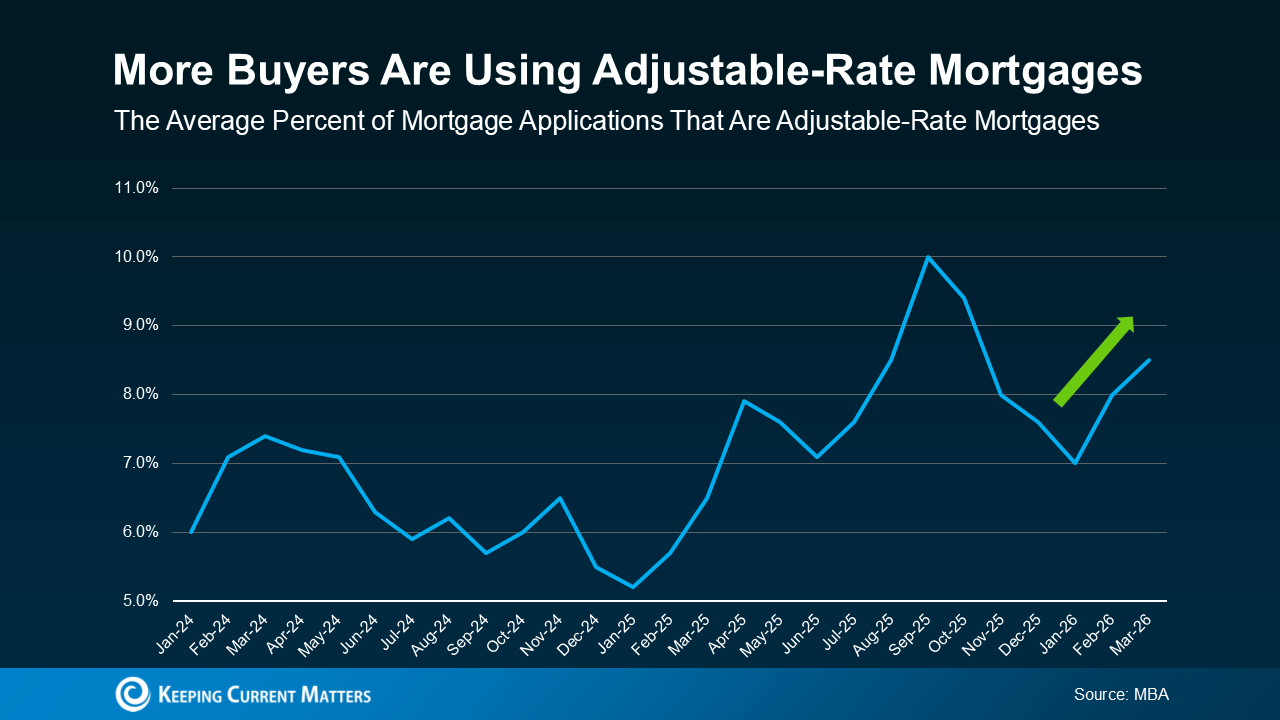

More homebuyers are deciding that a lower payment today is worth considering, even if it means taking on more uncertainty later.

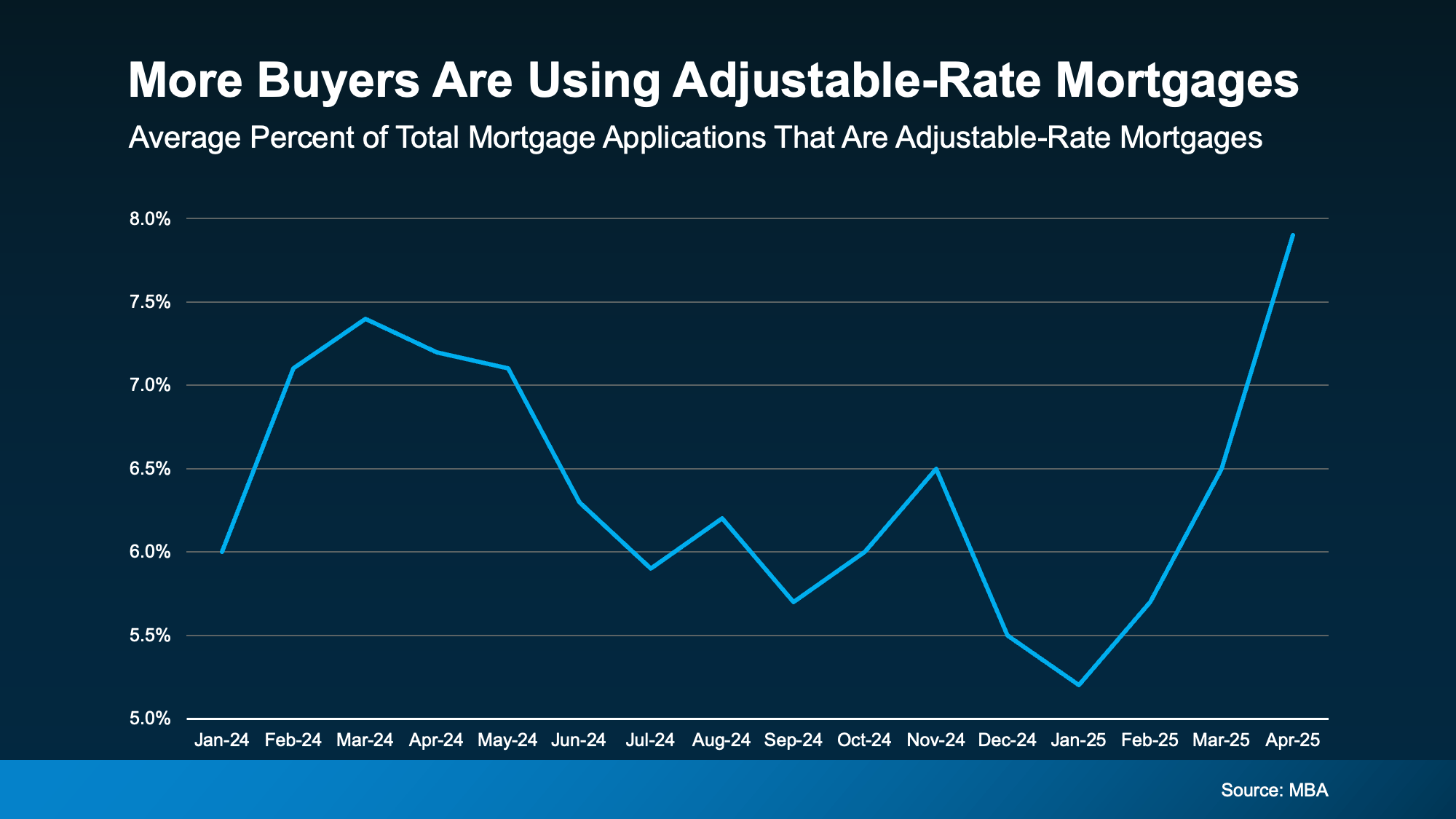

Recent reports from the Mortgage Bankers Association (MBA) show that the share of buyers choosing ARMs has increased in recent years. That doesn’t mean ARMs are becoming the right fit for everyone. But, it shows that some buyers are using them as a strategy to deal with affordability challenges in the current market.

For anyone who remembers the 2008 housing crash, this trend may sound concerning at first. But today’s lending environment is very different.

In the past, some borrowers were approved for loans they couldn’t realistically afford once the interest rate adjusted. Today, lending standards are tighter, and lenders generally evaluate whether borrowers could still manage the payment if rates rise. So while ARMs are becoming more common again, that alone doesn’t point to another housing crisis.

The Pros and Risks of an ARM

An adjustable-rate mortgage can make sense in the right situation, but it depends on your financial plan and your comfort with risk.

An ARM may be worth considering if:

- You expect to move before the rate adjusts.

- You believe your income will increase over time.

- You need a lower initial payment to make homeownership possible now.

Still, there are trade-offs to consider.

Once the fixed-rate period ends, your interest rate can change, and your monthly payment could increase significantly depending on where mortgage rates are at that point. There’s also no guarantee rates will fall in the future, which means refinancing later may not be as easy or as beneficial as some buyers hope.

That’s why it’s important to think beyond the introductory rate. Make sure you understand how long the fixed period lasts, how often the rate can adjust, and how much your payment could increase over time. Most importantly, talk through your options with a trusted lender and financial advisor before making a decision.

Bottom Line: Is an ARM Right for You?

Adjustable-rate mortgages are regaining popularity because they can make buying a home more affordable in the short term. For some buyers, that lower upfront payment can be a helpful tool. But an ARM isn’t necessarily the right move for everyone.

The best decision comes down to understanding how the loan works, weighing the risks, and making sure it fits your long-term goals.

If you’re considering an adjustable-rate mortgage yourself but are still on the fence, reach out to us today. We can connect you with a qualified lender in your area who explore your options with you.

Should You Still Buy a Home Right Now? What Buyers Need To Know

Between nonstop economic headlines, global uncertainty, and ongoing concerns about affordability, it’s understandable to wonder whether now is still a smart time to buy a home.

The good news is this: current events may be influencing the housing market, but they have not taken homeownership off the table. For many buyers, the opportunity is still there. It just may require a more thoughtful strategy than it did a few months ago.

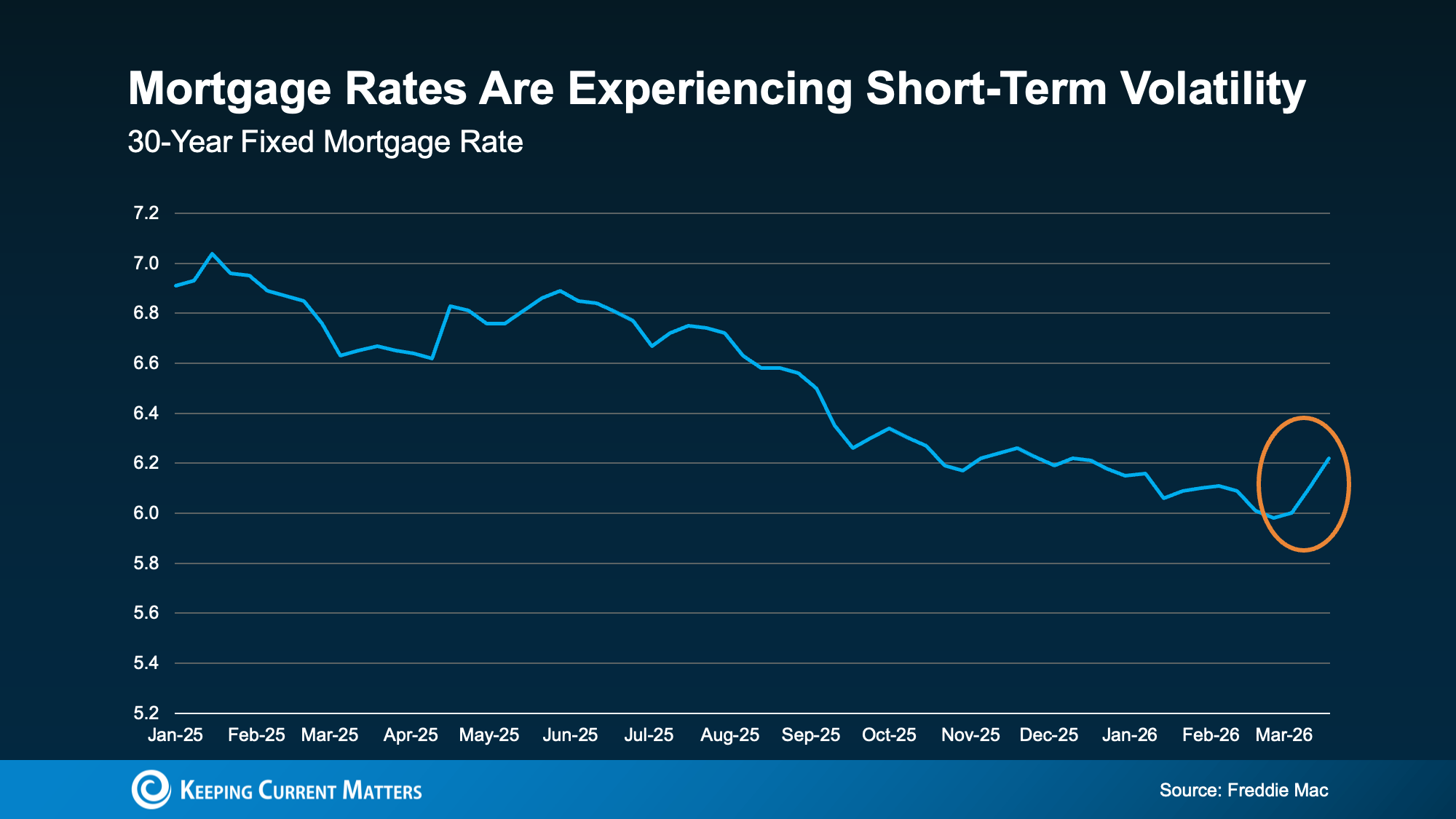

Mortgage Rates Have Risen Slightly. Here’s What’s Behind It

After trending downward for much of 2025, mortgage rates have climbed again over the past month. Experts point to a mix of global events and broader economic pressures as key reasons why.

As Mark Fleming, Chief Economist at First American explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

So what does that mean if you’re thinking about buying a home? Should you wait for conditions to settle before making a move?

Not necessarily.

Your Opportunity To Buy Hasn’t Disappeared

There’s no denying that buying felt a bit more affordable when mortgage rates were closer to 6%. Now that rates are hovering in the mid-6% range, monthly payments are naturally a little higher.

But it helps to take a step back and look at the bigger picture.

For example, if you’re financing a $500,000 home, a rate in the mid-6s could still mean a monthly payment that is roughly $300 lower than what buyers were facing early last year.

That means today’s higher rates have not erased all the progress we’ve seen. In fact, buying a home can still be more affordable than it was just a year ago.

Yes, your payment may have been lower a few weeks ago. But trying to perfectly time the market rarely works in your favor. Conditions can shift quickly, and hindsight always makes past decisions look easier.

Instead of waiting for the “perfect” moment, focus on making the best decision based on your goals, finances, and today’s market conditions.

Expect Mortgage Rate Volatility

One thing buyers should be prepared for is continued movement in mortgage rates.

Rates may keep rising or falling in the weeks and months ahead as new economic reports are released and world events continue to unfold. That kind of uncertainty can feel frustrating, but it’s also part of today’s market.

The truth is, you can’t control what happens with inflation, global events, or mortgage rates next week. What you can control is how prepared you are when the right opportunity comes along.

That preparation can make all the difference.

If You Need To Move, You Still Have Options

For many buyers, the decision to move is not just about market timing. Life keeps moving, even when the market feels unpredictable.

Maybe your family is growing. Maybe you’re relocating for work. Maybe your current home no longer fits your lifestyle or needs. Those reasons still matter, and they may be more important than waiting for rates to change.

Buyers who are moving forward right now are often doing so because their personal situation makes it the right time.

And the good news is there are still strategies that can help make a purchase more manageable.

For example, some buyers are exploring adjustable-rate mortgages (ARMs) to secure a lower initial rate. That approach is not right for everyone, but it’s one example of how flexibility and planning can create opportunities in today’s market.

A Smart Plan Starts With the Right Experts

In a market like this, having a plan matters more than ever.

Working with a trusted real estate agent and lender can help you:

- Understand what you can realistically afford at today’s rates

- Review financing options, including ARMs and buyer assistance programs

- Stay informed as market conditions shift

- Make confident decisions based on your goals, not just the headlines

The right professionals can help you look beyond the noise and focus on what makes sense for your specific situation.

Conclusion

Uncertainty in the market does not mean you’re out of options.

If you need or want to move, buying a home may still be the right decision. The key is to go in with a solid plan, the right support, and a clear understanding of your financing options.

Homeownership is still possible. You just need the right strategy for today’s market.

Mortgage Rate Volatility: What You Can Control as a Buyer

Mortgage rates have been moving up and down lately, and that can make buying a home feel harder to plan for. When rates are unpredictable, many buyers wonder whether they should wait, move forward, or try to time the market.

Here’s the good news: while you can’t control where mortgage rates go next, you can control several factors that may help you secure a better rate. The first step is understanding what’s driving today’s market and knowing where to focus your time and effort.

Mortgage Rate Volatility Is Normal

Recent data from Freddie Mac show that mortgage rates have been fluctuating. After trending downward for well over a year, rates ticked up again this month.

That kind of movement can feel frustrating, especially when you’re doing your best to budget for a home purchase. But occasional increases and decreases are a normal part of the mortgage market. Even over the past year, there have been periods when rates jumped before settling back down.

This is another one of those moments, and it helps to keep that in mind.

When there’s economic uncertainty or major global events unfolding, mortgage rates often respond quickly. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

That’s exactly why trying to predict the perfect time to buy usually doesn’t pay off. Rates can change fast, and waiting for the market to cooperate may not give you the outcome you want.

Focus on What You Can Control

You may not be able to influence the market, but you can take steps put yourself in a better position as a buyer. If your goal is to get the best mortgage rate possible, these are the areas that matter most.

Your Credit Score

Your credit score is one of the biggest factors that affects the rate you qualify for. In many cases, even a modest improvement in your score can lead to better loan terms and a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That’s why it’s worth taking steps to strengthen your credit before applying for a mortgage. Paying bills on time, reducing outstanding debt, and avoiding new credit inquiries can all help. If you’re not sure where your score stands or what improvements would make the biggest difference, a trusted loan officer can help you create a plan.

Your Loan Type

The type of mortgage you choose also affects your rate. There are many different types of loans, and each comes with different eligibility requirements, benefits, and pricing.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why exploring your mortgage options is so important. A conventional loan may be the right fit for one buyer, while an FHA, USDA, or VA loan may offer better advantages for another. Comparing programs and speaking with more than one lender can help you understand which path makes the most sense for your financial situation.

Your Loan Term

The length of your loan term matters, too. Most lenders offer 15-year, 20-year, and 30-year mortgage options, and the term you choose can affect both your interest rate and your monthly payment.

Freddie Mac explains it this way:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A shorter loan term may come with a lower interest rate, but the monthly payment is often higher. A longer term may give you more flexibility in your monthly budget, even if you pay more interest over time. The right choice depends on your goals, your budget, and how long you plan to stay in the home.

Conclusion

If you’re in the market for a home right now, the best strategy is not to focus on trying to predict where mortgage rates will go next.

Instead, focus on what you can control. Improve your credit score, explore different loan types, and choose a loan term that fits your needs. Most importantly, work with a trusted lender who can guide you through your options. If you need help connecting with trustworthy lender, reach out to us today.

Mortgage rates may be out of your hands, but the steps you take to prepare are not. And when you focus on what you can change, you give yourself a much better chance to move forward with confidence.

Mortgage Rates Just Hit a 3-Year Low. Does It Matter in 2026?

If you’ve been watching mortgage rates and waiting for a “better time” to buy, here’s your chance. Rates just dipped below 6% for the first time in more than three years. Even modest rate movement can change what you can afford, how competitive you can be, and whether buying feels realistic again, especially if last year’s higher rates pushed you to the sidelines.

With rates finally easing up into 2026, here’s a fresh take on why lower mortgage rates are still a big deal, plus what to do next if you’re thinking about making a move.

Why Mortgage Rates Impact More Than Just Interest

A mortgage rate isn’t just a number on a lender’s website. It shapes the entire homebuying experience because it affects:

- Your monthly payment

- How much home you can qualify for

- Your comfort level with your budget

- How competitive your offer can be

When rates jump, affordability tightens fast. That’s why many buyers (especially first-time homebuyers) feel the pinch first. When rates ease, the reverse happens: budgets get a little more breathing room, and choices open up.

The “One-Point” Difference That Changes the Math

One of the easiest ways to understand why rate declines matter is to look at a simple example.

When rates are closer to 7%, monthly payments rise sharply. When rates move closer to 6% (or below), payments can drop meaningfully. On a typical loan amount, that can translate into hundreds of dollars per month in savings compared to the higher-rate environment.

That difference can help you:

-

Stretch your budget without stretching your lifestyle

-

Consider more homes in a neighborhood you actually want

-

Keep cash available for repairs, furnishing, or future goals

In practical terms, the change isn’t just “cheaper interest.” It can be the difference between compromising on your wish list and finding a home that fits.

What Lower Rates Can Unlock for Buyers

When borrowing costs come down, three things usually happen for homebuyers:

1) Lower monthly payments

A lower rate can reduce the monthly principal-and-interest payment, which helps many buyers feel more confident about moving forward.

2) More buying power

When the payment drops, you may qualify for more home at the same monthly budget. That can mean a better location, an extra bedroom, or a property that needs fewer updates.

3) Stronger offers without overextending

More budget flexibility can help you compete without taking on a payment that makes you uncomfortable. That matters in markets where inventory is still tight and desirable homes move quickly.

Why This Can Bring More Buyers Off the Sidelines

Rate changes don’t only affect you. They affect everyone who has been waiting, too.

Industry research suggests that when rates sit around certain thresholds, millions more households can afford a median-priced home. In fact, research from the National Association of Realtors (NAR) points to 5.5 million additional households being able to afford the median-priced home when rates are at 6% or below, and it estimates roughly 550,000 of those households could buy within the next 12 to 18 months.

That matters because it signals something important: pent-up demand can return quickly when affordability improves.

If you’re home-searching now (or preparing to), you may be able to act before competition fully ramps back up.

A Quick Reality Check: Rates Aren’t the Only Factor

Lower rates help, but they don’t magically make every home affordable. Your true monthly cost depends on several moving pieces, including:

-

Home price

-

Local inventory and competition

-

Property taxes

-

Homeowners insurance (which can vary widely by state and ZIP code)

-

HOA dues

-

Your down payment and credit profile

That’s why the smartest next step isn’t guessing. It’s running real numbers to figure out what “affordable” looks like for you.

What To Do Next If You’re Considering Buying

If you’ve been waiting for rates to improve, here’s a simple, practical plan:

-

Get pre-approved (not just pre-qualified).

Pre-approval gives you a clearer budget and shows sellers you’re serious. -

Calculate your comfortable payment range.

Decide what fits your life, not just what a lender says you can qualify for. -

Compare scenarios with your lender.

Ask for payment examples at different price points, down payments, and rate options. -

Watch inventory in your target neighborhoods.

The best “deal” is the home that works for your needs and your budget.

Conclusion

Mortgage rates easing from last year’s highs isn’t just an attractive headline. For many buyers, it can be the shift that turns “maybe someday” into “this could actually work.”

If you paused your search when rates were higher, it’s worth revisiting your numbers now. A quick conversation with a trusted lender can show what today’s rate environment means for your payment, your buying power, and your options.

If you’re thinking of buying, or need help finding a lender, reach out to us today. We can connect you with local agents and lenders to make your journey as simple as possible.

CENTURY 21 Affiliated Announces Strategic Partnership with CMG Financial and Welcomes Greg Harkleroad as Joint Venture Division Sales Manager

Madison, WI – June 26, 2025 – CENTURY 21 Affiliated is proud to announce a new strategic partnership with CMG Financial, a top five privately held mortgage lender in the U.S., and the appointment of Greg Harkleroad (NMLS ID# 427611) as the Joint Venture Division Sales Manager to lead this exciting collaboration.

This partnership represents our continued commitment to delivering a seamless and exceptional home-buying experience for our clients across the Midwest and West Coast. With CMG’s innovative lending platform and long-standing reputation for excellence, combined with CENTURY 21 Affiliated’s position as a leading real estate franchise, we are poised to provide unmatched service and support to our buyers and agents.

“We are thrilled to announce our relationship with CMG Financial,” said Dan Kruse, CEO of CENTURY 21 Affiliated. “After extensively researching mortgage partners, we found CMG to be best-in-class when it comes to technology, customer experience, and agent support. By aligning with a lender of their caliber, we are confident this partnership will significantly elevate the home-buying journey for our clients.”

At the helm of this new joint venture is Greg Harkleroad, who brings nearly 40 years of mortgage experience and a proven track record of leadership, team building, and business growth. His passion for helping individuals achieve homeownership and his commitment to Realtor collaboration make him the ideal leader for this initiative.

“Greg brings decades of mortgage expertise to the venture,” said Sam Bell, President of Brokerage, CENTURY 21 Affiliated. “He has built numerous winning teams and is dedicated to supporting our agents and buyers at every step of the home financing process. We are excited to have him onboard.”

Greg’s approach to leadership centers around strategic hiring, coaching, and fostering strong relationships with real estate professionals to ensure a purchase-focused, service-driven mortgage experience.

“A strong Realtor-lender partnership is the foundation for delivering exceptional service,” said Harkleroad. “I’m excited to collaborate with CENTURY 21 Affiliated to bring that vision to life.”

With this partnership, CENTURY 21 Affiliated continues to prioritize innovation, support, and growth across its markets in Wisconsin, Michigan, and Southern California, offering agents and clients access to an experienced lending team, in-house technology, and personalized mortgage solutions.

For more information, please contact Greg Harkleroad at gregh@cmgfi.com or (513) 617-4407.

About CMG Financial

CMG Financial is a well-capitalized mortgage lender founded in 1993 by Christopher M. George, a former Mortgage Bankers Association Chairman. CMG makes its products and services available to the market through three distinct origination channels: retail lending, wholesale lending, and correspondent lending. CMG also operates eight joint venture companies with builder & realtor partners, holds an impressive MSR/servicing portfolio, and serves the capital markets of fixed income trading & sales through CMG Securities. CMG currently operates in all states, including District of Columbia, and holds approvals with FNMA, FHLMC, and GNMA. The company is consistently recognized as a top-producing lender and top mortgage employer, and it prides itself on helping clients achieve the dream of homeownership through product innovation and streamlined servicing.

About CENTURY 21 Affiliated Real Estate LLC

CENTURY 21 Affiliated is a member of multiple listings services in California, Illinois, Michigan, Minnesota, and Wisconsin with over 1,400 sales professionals and 60+ offices. CENTURY 21 Affiliated also specializes in worldwide relocation. At CENTURY 21 Affiliated, the customer comes first. The complete commitment to this philosophy is what has made CENTURY 21 Affiliated such a powerful force in the real estate industry. CENTURY 21 Affiliated has been ranked the number one CENTURY 21® franchise in the world for eleven years in a row. Visit C21Affiliated.com to learn more.

###

Adjustable-Rate Mortgages on the Rise: Should You Jump In?

If you’re in the market for a house, you’re probably not encouraged by today’s mortgage rates. Elevated rates and rising home prices have many homebuyers starting to explore other financing options that make more sense. One type of loan gaining popularity is adjustable-rate mortgages (ARMs).

If you remember the 2008 market crash, you may be wary of new types of loans. It’s wise to be cautious, but there’s no need to worry. Today’s ARMs much safer and stricter than the ones you may remember from 2008.

During that time, some buyers held loans they couldn’t afford once their rate adjusted. Today, lenders are more careful, and determine whether you can afford an increased rate before the loan is ever offered. This time, ARMs are returning thanks to creative buyers looking for affordable ways to buy a home..

According to recent data from the Mortgage Bankers Association (MBA), more buyers are using ARMs to buy this year.

How Does an Adjustable-Rate Mortgage Work?

If you’ve never heard of ARMs before, you may be wondering what they are, and if they’re right for you. Here’s how Business Insider explains the main difference between a traditional fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Taxes or homeowner’s insurance can still influence a fixed-rate loan, but your baseline mortgage payment typically changes very little. Meanwhile, adjustable-rate mortgages can potentially change drastically in either direction after your initial payment period ends. Depending on your situation and anticipated market trends, this could either work for you, or be far too risky.

Pros and Cons of Adjustable-Rate Mortgages

With ARMs on the rise in 2025, it’s clear that more buyers are finding them appealing. Under the right conditions, they may offer attractive upsides, like a lower initial rate. According to Business Insider again:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

Remember that if you have an ARM, your rate will change over time. As Barron’s explains, they can potentially cost you more in the long run:

“Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up.”

While the upfront savings can be helpful now, consider what could happen if your initial rate ends before you move. Even though rates are projected to ease a bit over the next couple years, nothing is ever guaranteed. Before you choose an ARM, talk with your lender and financial advisor about all your options, and the potential risks.

Conclusion

For certain buyers, adjustable-rate mortgages can offer some big advantages, but this won’t be true for everyone. Understand how they work and whether their pros and cons make sense for you financially. Always talk to a trusted lender and a financial advisor before making entering into a new mortgage.

Need help connecting with a trustworthy lender in your area? Reach out to us for help today.

Foreclosures Rose in Q1 2025 – Is It a Warning Sign?

With everyday costs seemingly rising across the board, the state of the housing market is a natural concern. When basic living expenses rise, even critical financial responsibilities like mortgage payments start to slip, leading to increased foreclosures. Unsurprisingly, new data shows filings for foreclosures rose in Q1 2025, stirring worries about another housing crash like in 2008.

But as it turns out, there’s less cause for worry than you might think. When contextualized correctly, it’s clear these new number don’t point to a repeat of the last big housing crash.

The 2008 Market Versus 2025

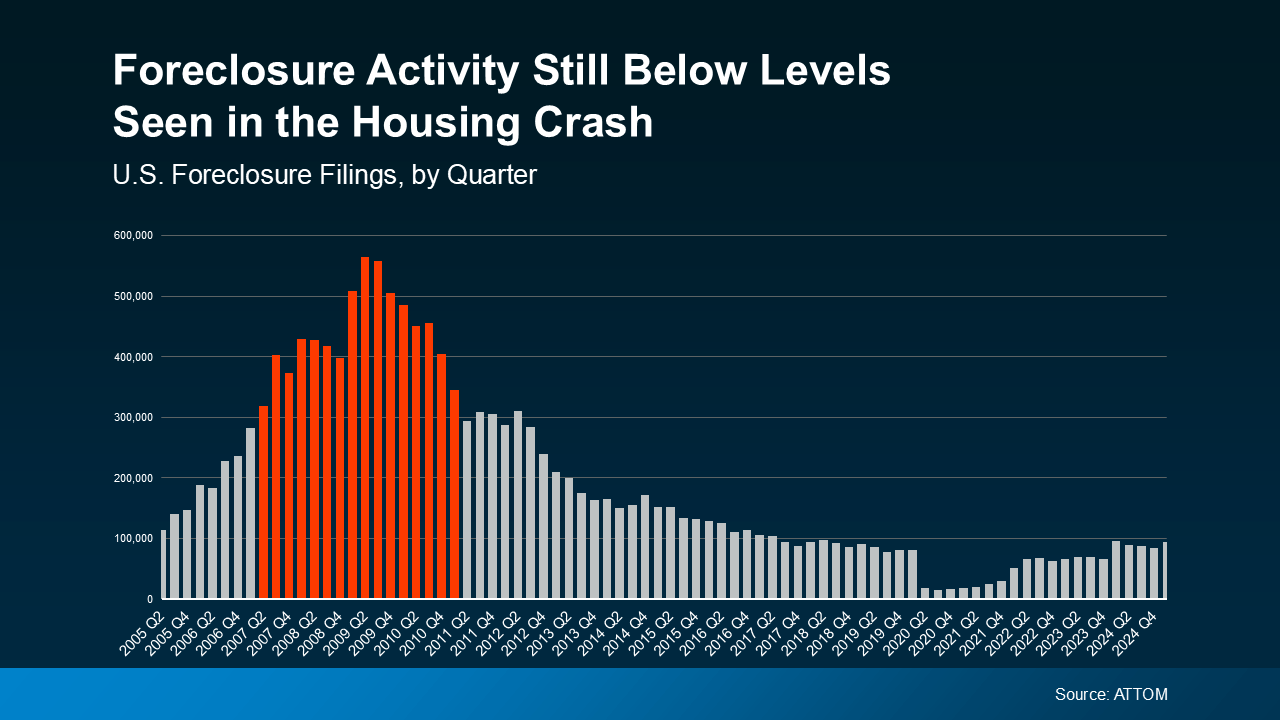

The latest quarterly report from ATTOM shows that foreclosures did rise in Q1 2025, which is concerning at first glance. However, foreclosure filings were still lower than the normal historical average, and far below the levels seen in 2008. When plotted visually, it’s easy to see the huge difference between 2008 and 2025.

Compare the foreclosure filings in Q1 2025 to the years surrounding the 2008 crash on the graph below. Even in the years preceding and following the 2008 crash, foreclosures were dramatically higher than what we’re seeing now.

Back in 2008, lenders were approving loans using much riskier practices, saddling many homeowners with mortgages they couldn’t afford. This flooded the market with distressed properties, surplus housing inventory, and free-falling home prices that collectively caused the crash.

In the years that followed, lending standards became much stricter and stronger to prevent such a crash from happening again. Today, most homeowners are in a much better financial position, and foreclosures have stabilized as a result.

The graph may appear to show foreclosures ramping up since the lows of 2020 and 2021, but this is deceiving. Foreclosures during those years were unusually low thanks to a moratorium designed to help millions of homeowners through the pandemic. That moratorium has since ended, which has caused foreclosure filings to return to the more normal levels we see now.

Compared to pre-pandemic years like 2017-2019, foreclosures overall are actually relatively down from what’s considered normal. So while foreclosures rose in Q1 2025, this doesn’t point to a troubling surge in the market.

Why Foreclosures Haven’t Surged in 2025

Another reassuring difference in today’s real estate market is the power of increased homeowner equity. As home prices have exploded over these past few years, homeowners have enjoyed a welcome boost to their wealth. According to Rob Barber, CEO at ATTOM:

“While levels remain below historical averages, the quarterly growth suggests that some homeowners may be starting to feel the pressure of ongoing economic challenges. However, strong home equity positions in many markets continue to help buffer against a more significant spike . . .”

In short, if a homeowner can’t make their mortgage payments, they may be able to sell their home to avoid foreclosure. During 2008, many people owed more than their homes were worth and had no choice but to foreclose. Today, most homeowners have much stronger equity that protects them from being forced into foreclosing. As Rick Sharga, Founder and CEO of CJ Patrick Company, recently explained in a Forbes article:

“ . . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Conclusion

It’s true that foreclosures rose in Q1 2025, but they’re nowhere near the levels seen during the 2008 crash. Even as home prices continue rising, strong equity is protecting existing homeowners and bolstering their wealth. This doesn’t discount the struggles some homeowners are facing, but it’s a reassuring fact for the market at large.

If you’re a homeowner facing foreclosure, ask your mortgage provider about what options are available to you. Are you a first time buyer eager to build your equity? Contact us today for the info you need to get started.

Should You Buy a Home This Spring or Wait for Lower Prices?

You’re probably familiar with the saying “The best time to plant a tree was yesterday, but the next best time is today.” It’s a valuable lesson about future planning and investment that, surprisingly, applies to the decision to buy a home too.

Even though buying a home is a major financial expense, it’s also a major investment that grows over time. As the price of your home increases over time, the value of the equity you’ve built grows with it. And while waiting for prices to drop may be an attractive option, trying to time the market rarely works.

But here’s something to consider: the longer you wait to buy a home, the more your patience could cost you. Let’s explain why.

Home Prices Are Expected To Continue Climbing

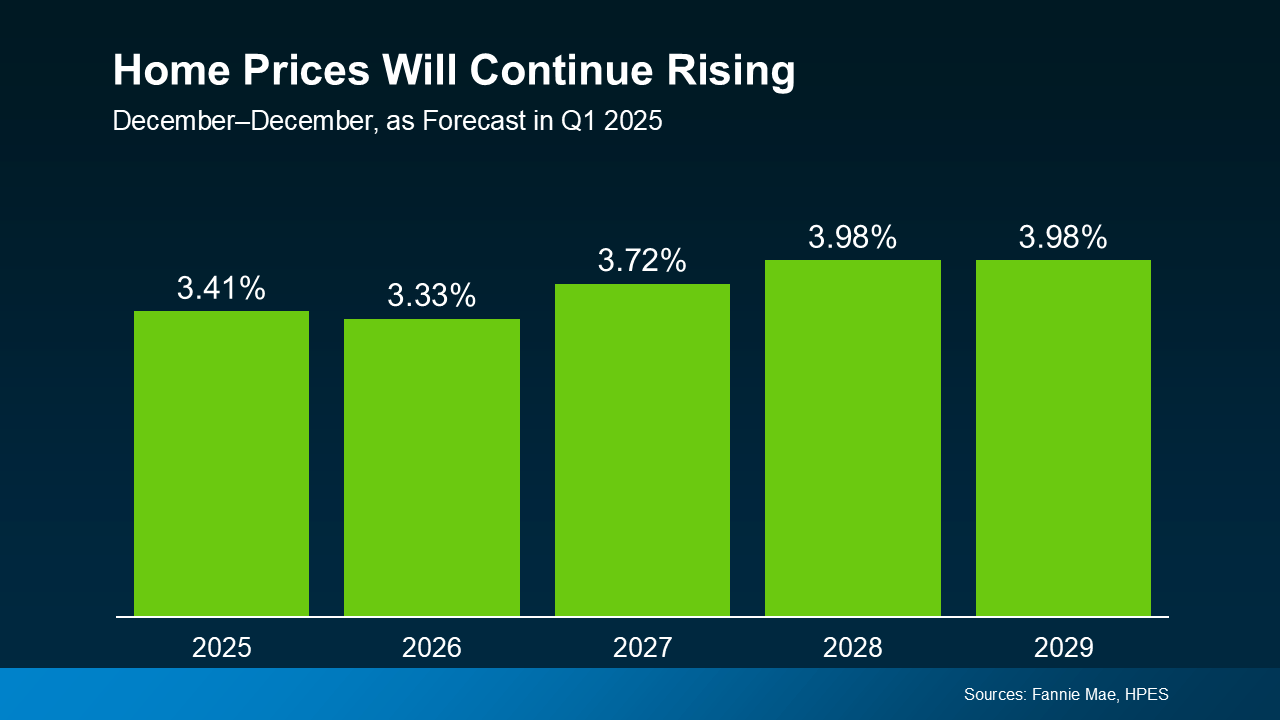

Each quarter, over 100 housing market experts respond to Fannie Mae‘s Home Price Expectations Survey (HPES). Consistently, the survey results show experts agreeing that home prices will continue to rise through 2029 or even longer.

Sharp price increases may be behind us, but experts predict steadier, healthier increases of 3-4% per year moving forward. This rate of increase will vary by market from year to year, but it’s much closer to normal. Reliable growth is a promising sign for hopeful buyers, and the housing market at large, as the graph below demonstrates.

Even in markets experiencing slower price growth or short-term decreases, the steady gains of homeownership eventually win in time. After all, a growing, long-term financial investment will always beat a one-time discount.

Here are the main points to remember:

- Home prices will be higher next year. Experts don’t expect home prices to fall any time soon, at least at the national level.

- Waiting for a perfect mortgage rate or price drops is a gamble. With only slight dips in mortgage rates expected in the near future, price increase could outpace any potential mortgage savings. Unless home price growth is slow or mortgage rates are low in your area, waiting will likely be more expensive.

- Buying early means building more equity. When you invest in homeownership early, your equity and appreciating home value reward you in the long run.

The Costs of Waiting To Buy

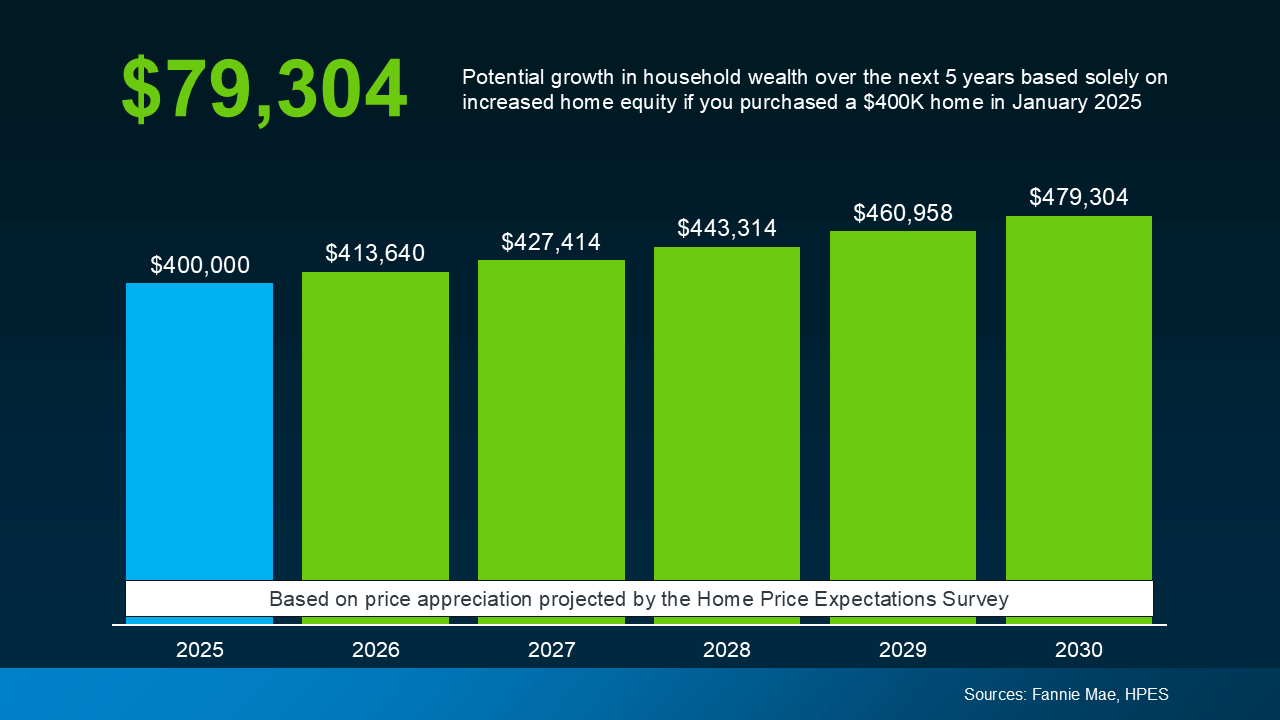

To demonstrate how these theories play out in real-world numbers, here’s a typical example. If you were to buy a $400,000 house in 2025, it could gain almost $80,000 in value by 2030. The graph below demonstrates how this value appreciates year by year based on the expert data we mentioned earlier.

This can be a considerable difference in your future wealth and why buyers who invest early are often glad they did. When it comes to building wealth through long-term investment, time in the market matters.

The question to consider isn’t “Should I wait to buy?” It’s really “Can I afford to buy now?” Just like planting a tree, making short-term sacrifices to buy a home will eventually pay off in the long-term.

Between rising prices and stubborn mortgage rates, today’s housing market is challenging, but achieving homeownership is far from impossible. Exploring different neighborhoods, seeking alternative financing options, or applying for down payment assistance programs can all make a critical difference.

What’s most important is acting decisively when you’re able to, instead of waiting for a perfect opportunity that never comes.

Conclusion

If you’re interested in buying but still undecided, take the time you need to make the right choice. But, remember that realizing an investment takes time, and the sooner you make one, the sooner you’ll be rewarded.

If you’re curious about what’s happening with prices in our local area, then reach out to us. Even if you’re not ready to buy, an expert local agent can fill you in with the info you need.