Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

It’s Tax Day – Here’s How a Refund Can Help You Save For a Home

If you’ve been planning to buy a house, you know how hard it can be to save for a home. What you might not know is that your tax return can be a helpful boost to your savings and budget. According to a recent post by Freddie Mac:

“ . . . your tax refund from the IRS can be a useful supplement to your homebuying budget.”

So if you’re planning to get a tax refund this year, consider the difference that extra funding can make. A refund can help you pay for the upfront costs of homebuying, like a down payment or closing costs. And, according to the IRS, your tax refund may even help you out this year more than ever.

How a Tax Return Can Help You Buy a Home in 2025

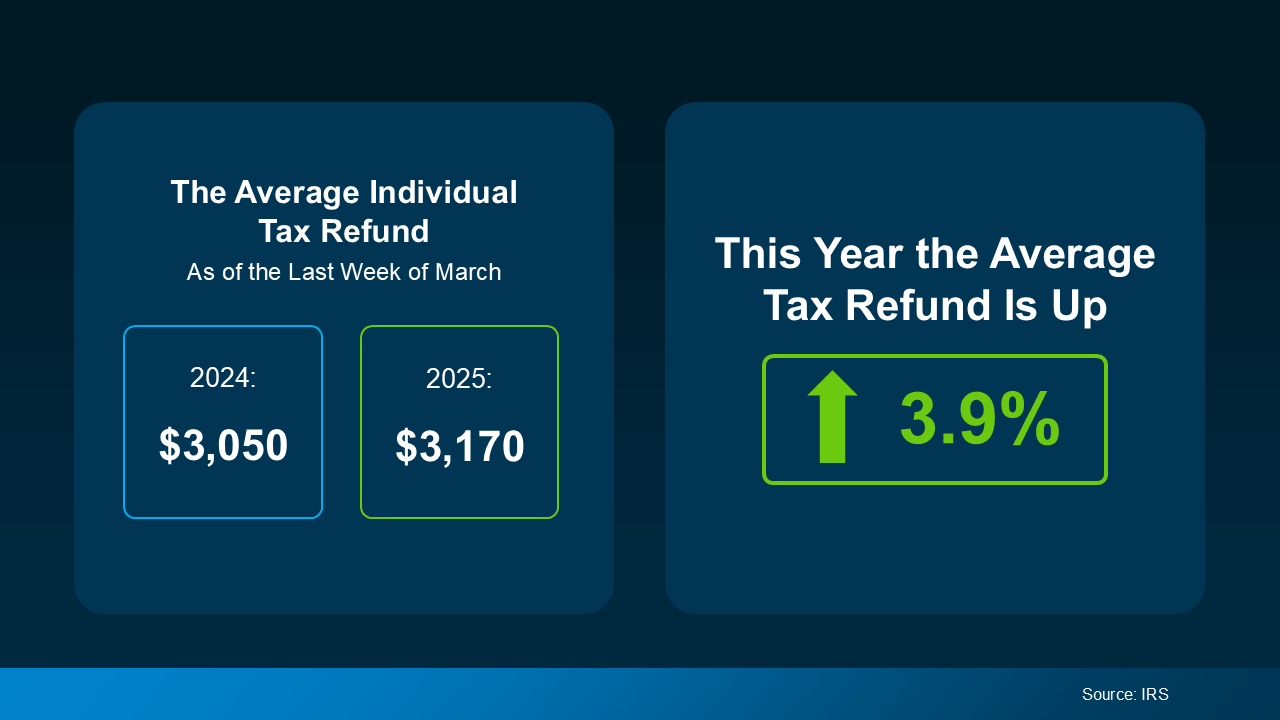

Recent data from the Internal Revenue Service (IRS) has found that the average individual’s refund is 3.9% higher this year. And while that’s not a huge increase, it can make a big difference if you’ve been struggling to save. The graphic below visualizes the new IRS data, comparing the average tax return in March 2024 to March 2025.

Your own personal tax refund will likely vary, but any financial boost helps when you’re saving for a home. According to Freddie Mac, the following are several ways you can put your tax return to good use when homebuying:

- Saving for a down payment – A down payment on a home is often one of the biggest obstacles to homeownership that buyers face. Saving your tax refund for a down payment can be a smart way to make this major step easier. Keep in mind while a 20% down payment may be common, it’s not typically a hard requirement to buy.

- Paying for closing costs – Usually due at closing, closing costs include fees for services like the appraisal, title insurance, and underwriting of your loan. While these vary by state, they’re often between 2% and 6% of your home’s total final purchase price. As a much lower percentage of your home’s price, closing costs can be a great use of your yearly refund..

- Lowering your mortgage rate – Lenders sometimes give buyers the option to buy down their mortgage rate if they qualify. This allows buyers to pay an upfront fee to lower their initial mortgage rate, reducing monthly payments in the short-term. This option can be particularly helpful if interest rates and mortgage payments are a major homebuying hurdle you’re facing..

Financially speaking, this may be more complicated in practice, but there’s no need to do it all on your own. Working with an experienced, trustworthy real estate professional can simplify your financial planning, helping you reach the best decision possible. An agent who understands the homebuying process, your unique financial needs, and your personal goals can make all the difference.

Conclusion

If you’ve been saving for a home, you already know well that every penny counts. Your tax return probably won’t be the final financial boost you need, but there are ways to use it effectively. Planning and identifying how to best spend that money can give you a real, meaningful step toward buying your home.

Are you eager to buy a home but having trouble making things work? Contact us today. We can connect you with local lenders and agents to help make your dream of homeownership a reality.

Mortgage Rates Drop to the Lowest Point in 2025 So Far

If you’ve been holding off on buying a home for a lower mortgage rate, take another look at the market. Mortgage rates are trending downward, and they just hit their lowest point of the year so far.

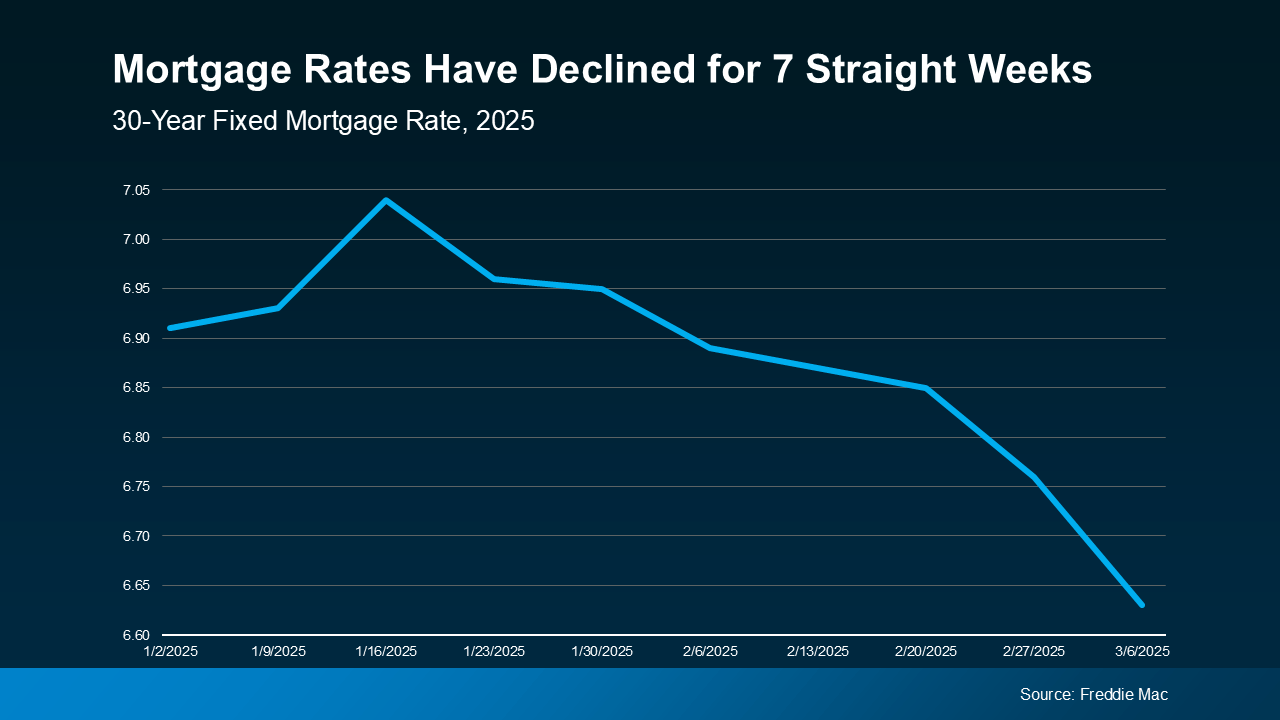

According to a report from Freddie Mac, mortgage rates have been falling for seven straight weeks. The average weekly rate for a 30-year-fixed mortgage is now at the lowest level its been in 2025.

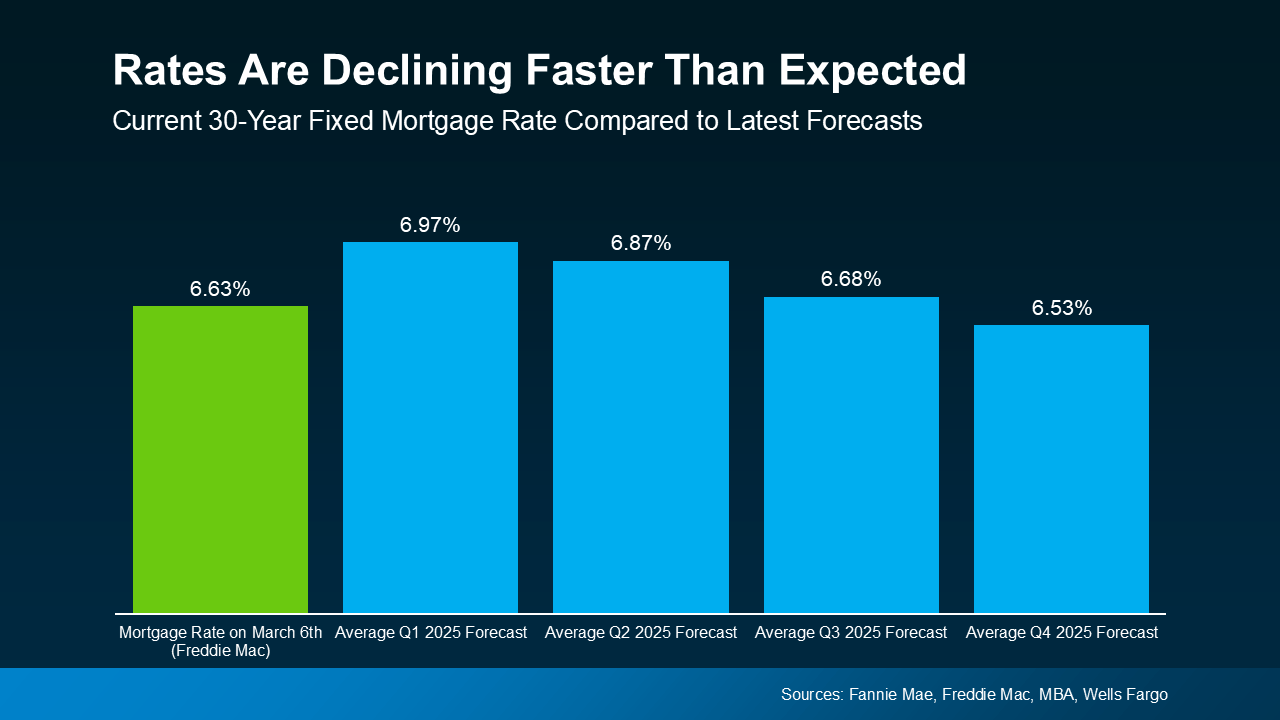

This may not sound significant on its own, but it outlines a remarkable trend. A drop in rates from over 7% to the mid-6’s can make all the difference when buying a home. What’s most significant is that experts previously predicted that rates wouldn’t fall this low until Q3 of this year.

Why Are Mortgage Rates Dropping?

According to Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), ongoing economic uncertainty is a driving force in pushing rates lower:

“Mortgage rates declined last week on souring consumer sentiment regarding the economy and increasing uncertainty over the impact of new tariffs levied on imported goods into the U.S. Those factors resulted in the largest weekly decline in the 30-year fixed rate since November 2024.”

The timing of this rate drop is great for buyers moving into the Spring 2025 market. But remember that mortgage rates can change quickly, and always expect some volatility in markets driven by uncertainty. With that said, this small window of rates dropping into prime buying season might be exactly wait you’ve waited for.

What Falling Mortgage Rates Mean for Your Buying Power

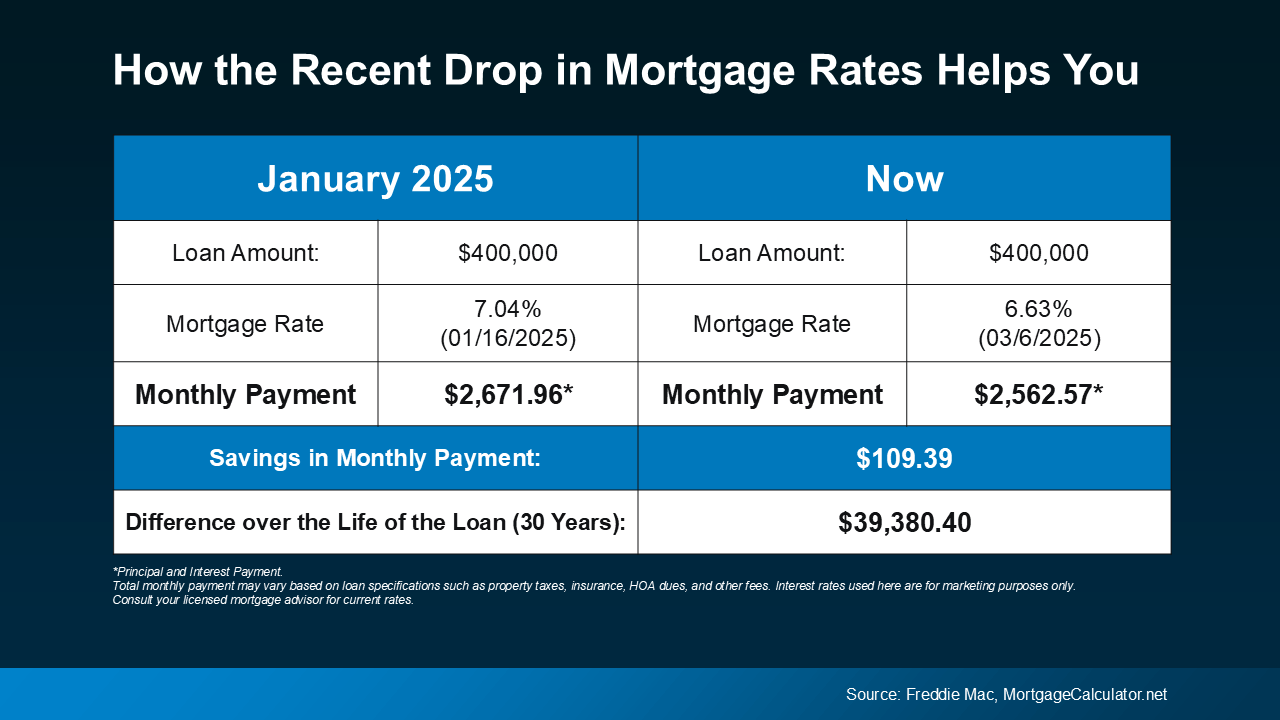

Even a small reduction in your mortgage rate can make a huge difference in your monthly housing payment. The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house when rates were 7.04% back in mid-January (this year’s mortgage rate high). The right side shows what it could look like if you buy a home now at current rates.

In just the past few weeks, the expected payment on a $400K loan has come down by over $100 per month. That’s a significant savings that can make a world of difference when deciding to buy a house.

Recent economic shifts have driven rates down faster than expected, and that’s great news. But remember that this could change at any time in the coming days and months for better or worse. So if you’re waiting for rates to fall further before you buy, think hard about the current window of opportunity before making a decision.

Conclusion

Mortgage rates have dipped to their lowest point in 2025 so far. This grants buyers a great position moving into the spring buying season, especially for those who have been waiting. The unpredictability of the market and larger economy mean volatility, so get expert advice and consider before making a decision.

FHA Home Loans in Wisconsin

If you’re in the market for a home in Wisconsin, you may have heard of FHA loans, or Federal Housing Administration loans, as a financing option. These government-backed loans are a popular choice for first-time homebuyers and those with less-than-perfect credit. In this guide, we’ll break down everything you need to know about FHA loans in Wisconsin, along with benefits and requirements of state-specific programs that can help you achieve your dream of homeownership.

What are FHA Home Loans?

FHA loans are mortgages insured by the Federal Housing Administration (FHA) and are designed to make homeownership more accessible, especially for Americans who may not qualify for a traditional mortgage or other loans. This reduces the risk for lenders and allows them to offer lower down payments and more lenient credit requirements. This also makes FHA loans particularly appealing to first-time buyers or those with limited savings.

Here are a few ways that FHA loans stand out from other options:

- Low Down Payment: You can qualify with as little as 3.5% down if your credit score is 580 or higher, meaning that up to 96.5% of a home’s value can be borrowed through an FHA loan.

- Flexible Credit Requirements: FHA loans are more forgiving of lower credit scores compared to conventional loans. Borrowers with scores as low as 500 may still qualify with a 10% down payment.

- Competitive Interest Rates: Being backed by the federal government, FHA loans often have lower interest rates than conventional loans, making monthly payments more affordable.

- Mandatory Mortgage Insurance: FHA loans require both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP), which is paid monthly.

These are just a few ways FHA loans can help homebuyers overcome financial barriers and make homeownership a reality for more Americans. With lower credit score requirements and lower down payments, it’s an easier pathway to securing a loan and finally owning a house.

Current FHA Loan Interest Rates in Wisconsin

As of February 2025, the average interest rate for a 30-year fixed FHA loan in Wisconsin is 6.24%, with an APR of 6.92%. These rates are slightly lower than conventional loan rates, making FHA loans a more cost-effective option. However, rates vary depending on your credit score, the lender, and the loan type and length, so always explore your options and compare offers when possible.

FHA Loan Requirements in Wisconsin

To qualify for a FHA home loans in Wisconsin, several key criteria must be met to ensure that potential borrowers are financially stable and capable of repaying their loan. Most notably, applicants need to demonstrate a reliable employment history and income.

Here’s a summary of the main eligibility criteria:

- Credit Score: As of 2023, a minimum score of 580 is required for a 3.5% down payment. Scores between 500 and 579 require a 10% down payment.

- Debt-to-Income Ratio (DTI): Your total monthly debt, including the mortgage, should not exceed 43% of your income, though some lenders may allow up to 57% in certain cases.

- Employment and Income: You’ll need a steady employment history of at least two years and verifiable income.

- Primary Residence: The home must be your primary residence.

- Property Standards: The property must meet FHA’s minimum standards for safety and livability, as determined by an FHA-approved appraiser.

- Loan Limits: For 2025, the FHA loan limit for a single-family home in most Wisconsin counties is $524,225. In higher-cost areas like Pierce and St. Croix counties, the limit is $529,000.

By meeting these requirements, you better position yourself for loan approval. It can also simplify the loan process, making it smoother and preventing potential setbacks or delays.

Applying for an FHA Loan in Wisconsin

Applying for FHA home loans in Wisconsin is straightforward but involves several basic steps. Borrowers should start by researching and comparing various FHA-approved lenders to find the best loan terms and secure the best deal.

After selecting a lender, borrowers complete the FHA loan application process. This process may vary between lenders, but should follow the same general steps. Here’s an overview of the major stages involved:

- Find an FHA-Approved Lender: Choose a lender approved by the FHA. Most banks, credit unions, and mortgage companies offer FHA loans.

- Pre-Approval: Get pre-approved to determine your budget and show sellers you’re a serious buyer.

- Submit Your Application: Provide details about your income, employment, and the property you want to buy .

- Provide Documentation: Submit tax returns, pay stubs, bank statements, and other financial documents.

- Property Appraisal: The lender will order an appraisal to ensure the home meets FHA standards and is worth the loan amount.

- Underwriting: The lender reviews your application to ensure you meet all FHA requirements.

- Closing: Sign the final paperwork, pay closing costs, and officially become a homeowner.

Wisconsin-Specific Programs to Pair with FHA Loans

Certain areas in Wisconsin may offer programs that can make FHA loans even more affordable. These programs are most common in larger metropolitan areas like Madison and Milwaukee, but some are available statewide through the Wisconsin Housing and Economic Development Authority (WHEDA). Here are a few options to explore if you’re planning to buy a home in Wisconsin:

- WHEDA Down Payment Assistance: The Wisconsin Housing and Economic Development Authority (WHEDA) offers programs like the Easy Close DPA, which provides up to 6% of the home’s purchase price as a second mortgage. Another option is the Capital Access DPA, offering $7,500 with no interest or monthly payments

- City of Madison’s Home-Buy the American Dream Program: Provides up to $35,000 in down payment and closing cost assistance, deferred until the home is sold or refinanced.

- Milwaukee Down Payment Assistance: Offers forgivable grants of up to $7,000 for homes in designated areas, provided the buyer contributes at least $1,000 and lives in the home for five years.

- Local Assistance Programs: Many cities and counties in Wisconsin offer grants or zero-interest loans for first-time buyers. Check with your local housing authority for details.

Conclusion

FHA loans are an excellent choice for hopeful homebuyers, especially first-time buyers or those with limited savings. By combining the benefits of FHA loans with Wisconsin-specific programs like WHEDA’s down payment assistance, you can make your dream of homeownership a reality. Whether you’re buying in Milwaukee, Madison, or a smaller town, understanding the FHA loan process and available resources will help you make informed decisions and secure the best deal for your new home.

If you’re ready to take the next step, start by finding an FHA-approved lender and exploring the down payment assistance programs available in your area. With the right preparation, you’ll be well on your way to owning a home in the beautiful state of Wisconsin!

Ready to buy but not sure how to secure a loan? Reach out to us today for help finding a qualified lender that works for you.

2025 Housing Market Predictions: What Do the Experts Say?

Wondering how the housing market is expected to change in 2025? And more specifically, what it all means for you if you plan to buy or sell a home? As always, the best way to get that information is to consult the pros.

Experts are constantly refining their predictions in response to changes in the market and overall economy. Here’s the latest information on two key factors sure to influence the housing market in 2025: mortgage rates and home prices.

Will Mortgage Rates Come Down?

Mortgage rates remain one of the strongest factors influencing the market, and everyone is waiting for them to come down. The real question is: will they drop, and how quickly?

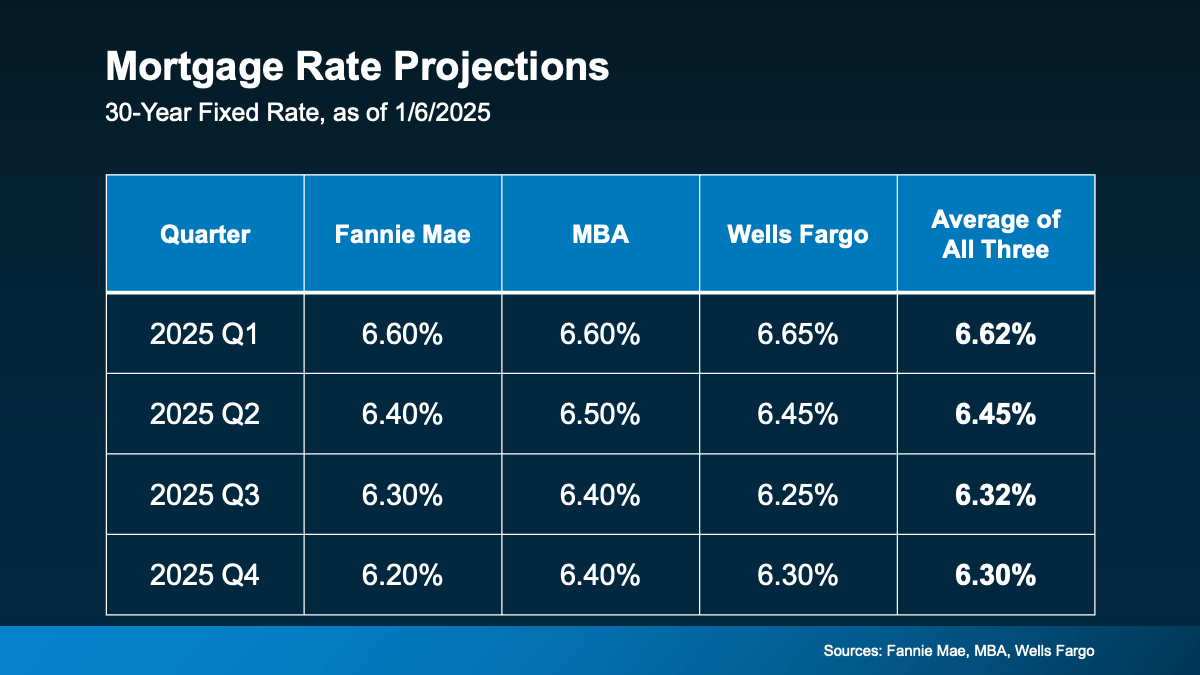

The good news is that mortgage rates are indeed projected to ease a bit in 2025, falling into the mid-6% range on average. But experts say not to expect a return to 3-4% mortgage rates, at least not this year. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Are we going to go back to 4%? Per my forecast, unfortunately, we will not. It’s more likely that we’ll go back to 6%.”

Other experts agree with Yun’s 6% prediction. They’re forecasting rates could settle in the mid-to-low 6% range by the end of 2025 (see chart below):

But remember that the market can change quickly, and experts will revise their predictions as the new year continues. Market forecasts are based on what experts know right now. And since everything from inflation to economic drivers have an impact on where rates go from here, some ups and downs are still very likely. So, don’t get caught up in the most exact numbers and try to time the market. Instead, focus on the overall industry trend and on what you can actually control.

A trusted lender and a local agent partner will make sure you’ve always got the latest data and the context on what it really means for you and your financial goals. With their help, you’ll see that even a small decline in mortgage rates can help bring down your future mortgage payment when you decide to buy.

Will Home Prices Fall?

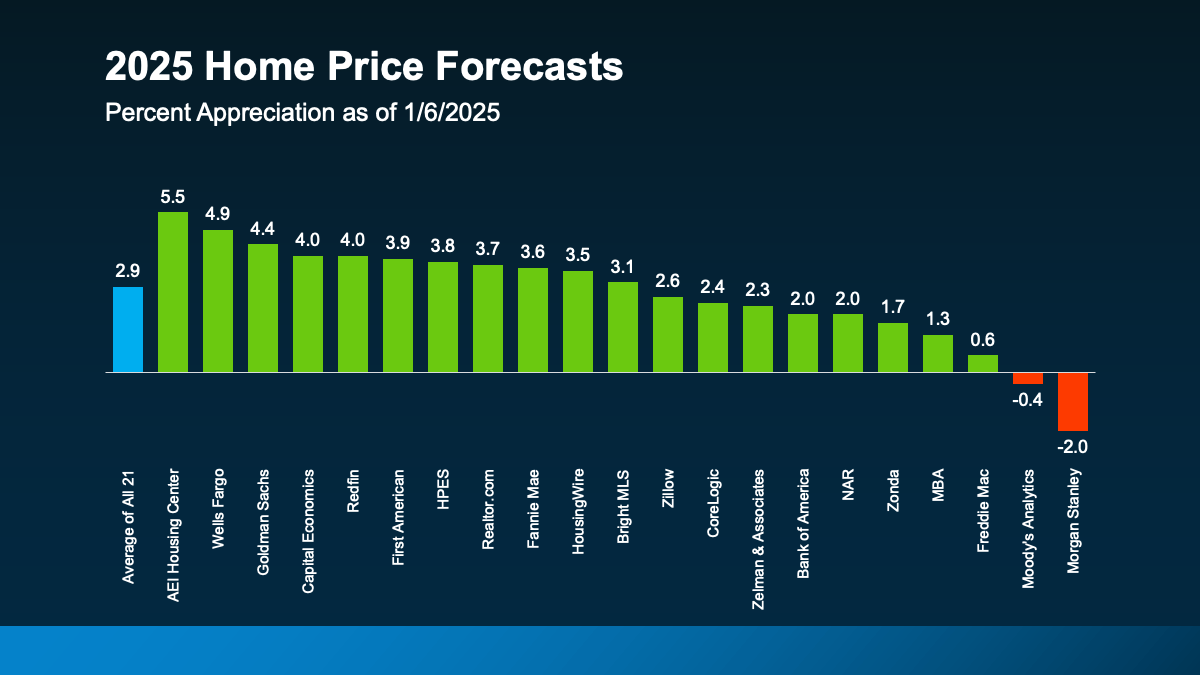

The short answer? Not likely. While mortgage rates are expected to ease, home prices are projected to keep climbing in most areas – but at a slower, more normal pace. If you average the expert forecasts together, you’ll see prices are expected to go up roughly 3% next year, with most of them hitting somewhere in the 3 to 4% range. But this is a much more typical and sustainable rise in prices compared to (see graph below):

If you’re thinking of buying in 2025, don’t expect a sudden drop to score you a big deal. That may sound disappointing if you’re hoping for home prices to come down, but this means you won’t have to deal with the steep increases we saw in recent years. You’ll also likely see any home you do buy go up in value after you get the keys in hand, and this can turn into a great investment over time.

Like many buyers, you might be wondering how it’s even possible that home prices are still rising. The answer all comes down to supply and demand. Even though there are more homes for sale now than there were in 2024, it’s still not enough to keep up with all the active home buyers on the market. As Redfin explains:

“Prices will rise at a pace similar to that of the second half of 2024 because we don’t expect there to be enough new inventory to meet demand.”

Keep in mind that the housing market is hyper-local, so this will vary by area. Some markets will see even higher prices, and some may see prices level off or even dip if inventory is up in that area. In most places though, prices will continue to rise as they usually do.

If you want to find out what’s happening in your local housing market, it always helps to lean on an agent who can explain the latest trends and what they mean for your homeownership plans.

Conclusion

The housing market is always changing, and 2025 will be no different. With mortgage rates likely to ease down to the 6% range and prices rising at a slower, more sustainable pace, it could be a great time to finally buy or sell. As always, it’s all about staying informed and making a plan that works for you.

If you’re in the market to buy or sell a home in 2025, let’s connect you with a local agent who can give expert advice on what’s happening in your area and make sure your next move is a smart one.

What Credit Score Do You Need To Buy a House?

Buying a house is a major milestone for many people, but it can also be a daunting process. One of the biggest concerns for potential homebuyers is their credit score. So what credit score do you need to buy a house in Wisconsin? Let’s explore this question and how it relates to the housing market.

Understanding Credit Scores

Before we dive into the specific credit score needed to buy a house, it’s important to understand what a credit score is and how it is calculated. A credit score is a three-digit number that represents your creditworthiness and is used by lenders to determine your risk as a borrower. The most commonly used credit score is the FICO (Fair Isaac Corporation) model, which ranges from 300 to 850 and prioritizes payment history. The other credit score type is the VantageScore model, which prioritizes total credit usage and is typically referred to less often.

Your FICO score is calculated based on several factors, including your payment history, amounts owed, length of credit history, new credit, and types of credit used. Credit payment history and amounts owed are typically the most significant factors in determining your FICO score. Keeping your credit balances low and making regular on-time payments are the best ways to maintain a good FICO score. The higher your credit score, the better your chances of getting approved for a loan and receiving favorable mortgage rates.

The Housing Market and Credit Scores

The housing market is constantly changing, and this can have an impact on the credit score needed to buy a house. In a strong housing market, lenders may be more lenient with credit score requirements as they are more confident in the market’s stability. On the other hand, in a weaker housing market, lenders may tighten their requirements and look for higher credit scores to mitigate their risk.

Credit Score Requirements for Different Types of Loans

Different types of loans have different credit score requirements. For example, a conventional loan typically requires a credit score of at least 620, while an FHA loan may accept a credit score as low as 500 with a 10% down payment. While a higher credit score will usually result in better mortgage rates and loan terms, it’s always advisable to compare the repayment terms of different loan offers before accepting one. While a loan with a lower down payment may be enticing in the short term, a lower interest rate will results in a lower monthly payment, saving you more in the long term.

Good Credit Score for Buying a House

While the minimum credit score required for a mortgage loan may vary, a good credit score for buying a house is generally considered to be 700 or above. In particular, Wisconsin has one of the highest average credit scores in the country at 732, which falls in the upper end of the “Good” score range. Having an average credit score or better shows lenders that you are a responsible borrower and can handle the financial responsibility of a mortgage. With a good credit score, you are more likely to be approved for a loan and receive favorable mortgage rates.

Improving Your Credit Score

If your credit score isn’t where you want it to be, don’t worry. There are steps you can take to improve your credit score before applying for a mortgage. These include paying off outstanding debts, making all payments on time, and keeping credit card balances low. It’s also a great practice to regularly check your credit report for any errors and dispute them if necessary. Generally, the best way to build your credit score over time is to make regular monthly payments that slowly lower your total credit usage.

Final Thoughts

The credit score needed to buy a house can vary depending on the local housing market and the type of loan you are applying for. With that said, a good credit score for buying a house is generally considered to be 700 or above. If your credit score is not where you want it to be, take steps to improve it before applying for a mortgage. Keep in mind that the average credit score in Wisconsin is relatively high at 732, and that meeting or exceeding this score will grant you a valuable advantage. With a good credit score, you can increase your chances of loan approval and receive better mortgage rates that will save you a considerable amount of money in the long run.