Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mortgage rates have been moving up and down lately, and that can make buying a home feel harder to plan for. When rates are unpredictable, many buyers wonder whether they should wait, move forward, or try to time the market.

Here’s the good news: while you can’t control where mortgage rates go next, you can control several factors that may help you secure a better rate. The first step is understanding what’s driving today’s market and knowing where to focus your time and effort.

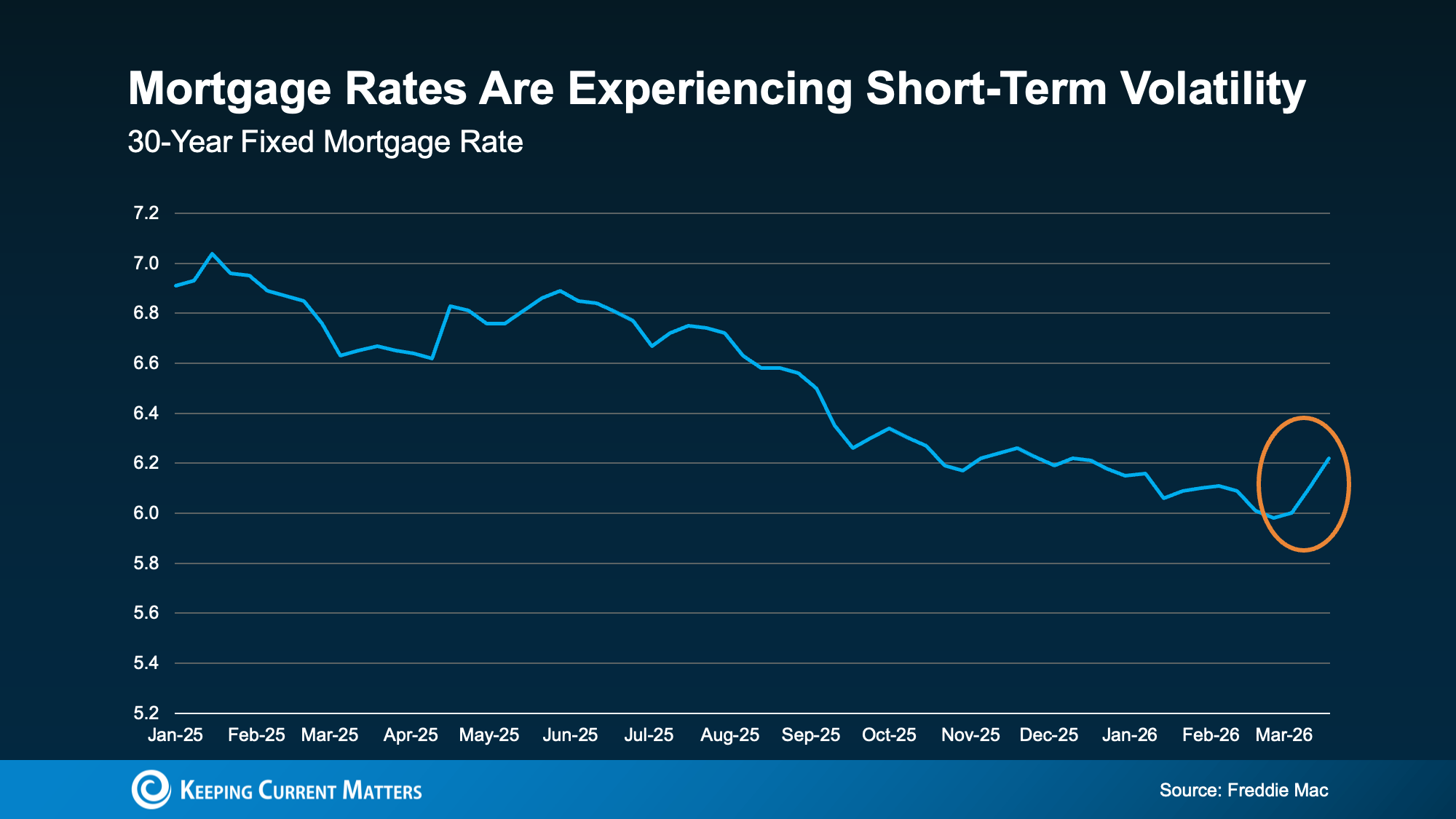

Mortgage Rate Volatility Is Normal

Recent data from Freddie Mac show that mortgage rates have been fluctuating. After trending downward for well over a year, rates ticked up again this month.

That kind of movement can feel frustrating, especially when you’re doing your best to budget for a home purchase. But occasional increases and decreases are a normal part of the mortgage market. Even over the past year, there have been periods when rates jumped before settling back down.

This is another one of those moments, and it helps to keep that in mind.

When there’s economic uncertainty or major global events unfolding, mortgage rates often respond quickly. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

That’s exactly why trying to predict the perfect time to buy usually doesn’t pay off. Rates can change fast, and waiting for the market to cooperate may not give you the outcome you want.

Focus on What You Can Control

You may not be able to influence the market, but you can take steps put yourself in a better position as a buyer. If your goal is to get the best mortgage rate possible, these are the areas that matter most.

Your Credit Score

Your credit score is one of the biggest factors that affects the rate you qualify for. In many cases, even a modest improvement in your score can lead to better loan terms and a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That’s why it’s worth taking steps to strengthen your credit before applying for a mortgage. Paying bills on time, reducing outstanding debt, and avoiding new credit inquiries can all help. If you’re not sure where your score stands or what improvements would make the biggest difference, a trusted loan officer can help you create a plan.

Your Loan Type

The type of mortgage you choose also affects your rate. There are many different types of loans, and each comes with different eligibility requirements, benefits, and pricing.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why exploring your mortgage options is so important. A conventional loan may be the right fit for one buyer, while an FHA, USDA, or VA loan may offer better advantages for another. Comparing programs and speaking with more than one lender can help you understand which path makes the most sense for your financial situation.

Your Loan Term

The length of your loan term matters, too. Most lenders offer 15-year, 20-year, and 30-year mortgage options, and the term you choose can affect both your interest rate and your monthly payment.

Freddie Mac explains it this way:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A shorter loan term may come with a lower interest rate, but the monthly payment is often higher. A longer term may give you more flexibility in your monthly budget, even if you pay more interest over time. The right choice depends on your goals, your budget, and how long you plan to stay in the home.

Conclusion

If you’re in the market for a home right now, the best strategy is not to focus on trying to predict where mortgage rates will go next.

Instead, focus on what you can control. Improve your credit score, explore different loan types, and choose a loan term that fits your needs. Most importantly, work with a trusted lender who can guide you through your options. If you need help connecting with trustworthy lender, reach out to us today.

Mortgage rates may be out of your hands, but the steps you take to prepare are not. And when you focus on what you can change, you give yourself a much better chance to move forward with confidence.