Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Almost half of Veterans (49%) feel homeownership is beyond their reach, according to a recent NewDay USA survey.

But many Veterans could be closer to buying a home than they think.

VA home loan benefits have been available for more than 80 years, but a lot of confusion remains about what’s actually covered. Some buyers assume they’ll need an impossibly large down payment. Others believe they’ll have high closing costs or monthly private mortgage insurance (PMI).

Misunderstandings like these can make homeownership feel farther away than it may really be.

VA Home Loan Benefits Many Veterans Overlook

A VA loan can offer several advantages for eligible buyers. While every buyer’s situation is different, these benefits may help reduce some of the upfront and monthly costs that often make buying a home feel financially overwhelming.

Let’s walk through a few of the biggest misconceptions.

You May Not Need a Down Payment

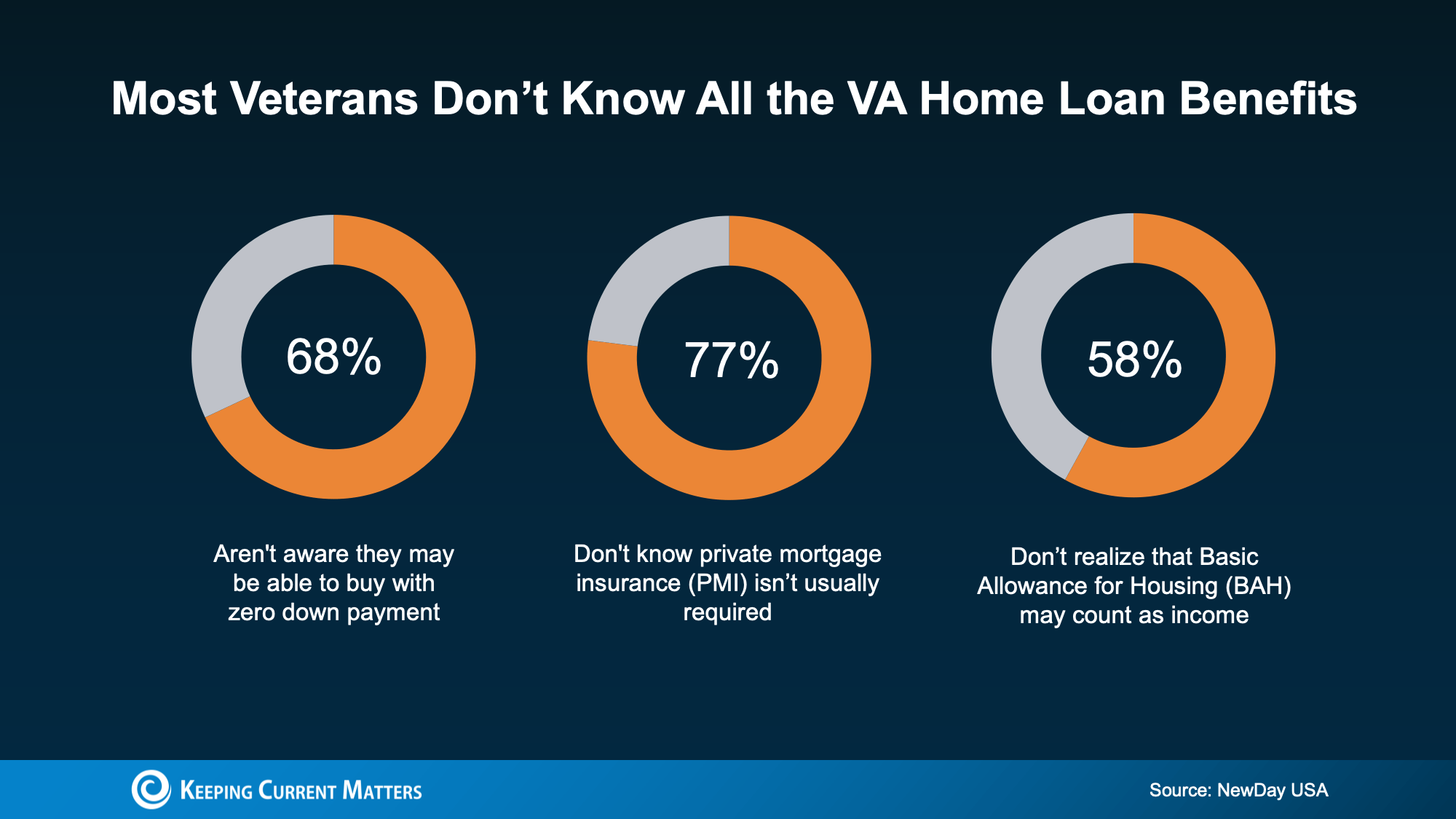

One of the most valuable VA home loan benefits is the potential to buy with zero money down.

That surprises many buyers. According to the NewDay USA survey, many respondents thought they would need to save between $10,000 and $19,900 before purchasing a home.

For some buyers, that kind of savings goal can take years. But with a VA loan, a large down payment isn’t always necessary. That can make the path to homeownership feel much more realistic for eligible Veterans and service members.

You May Have Lower Closing Costs

Closing costs are another area where VA loans can make a big difference.

According to the Department of Veterans Affairs, VA loans can include limits on the types of closing costs buyers are required to pay. That may help eligible buyers keep more money in their pocket on closing day.

When combined with the potential for no down payment, this benefit can lower the amount you need to save up before buying a home.

Your Monthly PMI Cost Could Be $0

Many loan programs require private mortgage insurance, commonly called PMI, when a buyer puts less than 20% down.

VA loans typically do not require monthly PMI, even when buyers use low or no money down.

That can make a meaningful difference in your monthly housing costs. If you use a conventional loan instead, you could pay $100 to $300 per month in PMI until you reach 20% equity, according to NewDay USA.

Over time, avoiding that monthly cost could add up to thousands of dollars.

Your BAH and BAS May Help You Qualify

For active-duty service members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan.

Since both BAH and BAS are non-taxable, they can help increase the amount you can qualify for. A trusted lender can help review your full financial picture and explain how these allowances might apply to your situation.

Why This Matters for Veterans and Service Members

If you have been assuming homeownership is out of reach, it may be worth taking a closer look at your VA home loan benefit.

A VA loan may help eligible buyers by offering:

- The potential for no down payment

- Limits on certain closing costs

- No monthly PMI in many cases

- The ability to include qualifying BAH and BAS income

These benefits don’t guarantee approval, and every buyer’s situation is different. But they may help remove some of the common barriers that keep Veterans and service members from exploring homeownership.

Bottom Line

VA home loan benefits can be a powerful tool for eligible Veterans, active-duty service members, and qualifying reservists.

If you’ve served, are currently serving, or know someone who has, connect with a trusted lender who understands VA loans. They can help you review your options, understand what you may qualify for, and decide whether buying a home makes sense for your goals.