Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

4 Ways To Make Your Home Offer Stand Out This Spring

If you’re planning to buy a home this spring, you may have more options than buyers have had in recent years. Home inventory has improved in many markets, and some sellers are more willing to negotiate than they were during the peak of the market.

But that doesn’t mean every homebuyer has an easy path forward.

In popular neighborhoods or areas where there still aren’t enough homes for sale, competition can pick up quickly. And spring is traditionally one of the busiest seasons for real estate, as many buyers hope to move before summer or get settled before the next school year begins.

That’s why making a strong, thoughtful offer still matters. Even in a more balanced market, the right strategy can help your offer stand out when you find a home you love.

Why Strong Offers Still Matter This Spring

Spring often brings more buyers into the market. Experts at Zillow and Realtor.com often say it’s one of the busiest times of year to purchase a home.

More activity can mean more competition, especially for homes that are priced well, located in desirable areas, or move-in ready. So while buyers may have more leverage than they did a few years ago, local market conditions still play a major role.

Here are four ways to give your offer an edge this spring.

1. Start with a Strong and Realistic Offer

It’s always tempting to make a low offer and hope the seller negotiates. In some markets, that approach may work. But if a home is getting a lot of attention, starting too low could cause the seller to move on to another buyer.

Instead, focus on making an offer that is competitive, realistic, and aligned with your local market.

As Bankrate explains:

“There is no magic formula for an optimal home offer. Any offer will be heavily dependent on asking price and local market conditions . . . Your real estate agent will know the local market well and can advise what a competitive — but fair — offer will look like in your area.”

A strong offer doesn’t always mean offering far above asking price. Most times, it means understanding the home’s value, the seller’s position, and how quickly similar homes are selling nearby.

2. Strategize for Multiple Competing Offers

If you find a home that checks all the boxes, another buyer likely feels the same way. That’s why it helps to talk with your agent ahead of time about what you’re willing to do if multiple offers come in.

One option your agent may discuss is an escalation clause. Investopedia defines it this way:

“An escalation clause is a way to automatically escalate your bid by a certain dollar amount, up to a certain ceiling, to compete with other bids.”

This strategy can help you stay competitive without going beyond your comfort zone. The key is setting a clear maximum price before emotions take over.

Still, there are potential risks to understand and keep in mind. If the home appraises for less than your offer price, you may need to cover the difference out of pocket. Your agent can help you decide whether an escalation clause makes sense for your budget and your market.

3. Keep Your Offer as Clean as Possible

Price is important, but it isn’t the only thing sellers consider. The terms of your offer can also make a big difference.

A clean offer is one that feels simple, straightforward, and easy for the seller to accept. That may mean limiting unnecessary requests, being thoughtful about contingencies, or avoiding terms that could make the transaction feel complicated.

As Redfin says:

“Sellers tend to want clean, straightforward offers with minimal strings attached. Keep your requests simple and focus on the essentials.”

This means working with your agent to decide which terms matter most and where you may have flexibility. The trick is to strike a balance, making an attractive offer without giving up important protections.

4. Be Flexible When It Helps the Seller

Sometimes the strongest offer is about more than price. In some cases, there are things that matter to the seller beyond simple dollar amount.

As NerdWallet explains:

“As you prepare an offer, you tend to focus on what the seller has (a house) and what you want (their house). But you’ll gain a competitive edge by viewing the transaction from the seller’s eyes: What does the seller want?”

For example, does the seller need extra time to move? Are they hoping for a quick closing? Would a flexible possession date make the offer more appealing?

Your agent can communicate with the seller’s agent to better understand what matters most. When you can align your offer with the seller’s priorities, you may have a big advantage over buyers who only focus on price.

Bottom Line: The Right Offer Strategy Can Help You Win

Today’s housing market may offer buyers more breathing room, but strong offers still matter, especially during the busy spring season.

If you’re getting ready to buy, work with a trusted local real estate agent who understands your market. The right strategy can help you move quickly, make a competitive offer, and feel confident when the right home comes along.

Is Late May a Good Time To Sell Your House?

If you heard that April 12-18 was the “best week” to list your house, you may be wondering whether you missed your chance to take advantage of the spring market.

Simply put, you didn’t.

While one report from Realtor.com pointed to that specific April week as a strong time for sellers, the truth is there’s rarely just one perfect week to sell your home. Rather, there’s usually a prime selling season, and right now, that window is still very much open.

The Spring Selling Window Is Still Going Strong

Every year, different real estate organizations study the best time to list your house. These reports don’t always point to the exact same week. And that’s not a bad thing.

Why the disconnect? Each study may use different data, market factors, and definitions of what “best” means. Some focus on sale price. Others look at how quickly homes sell, how much buyer demand exists, or how many sellers receive offers above asking.

But even when the exact dates vary, the bigger trend is clear: spring remains one of the strongest seasons for home sellers.

That means if you weren’t quite ready to list earlier in April, you still have time to make a smart move.

Why Late May Can Be a Smart Time To List

According to Zillow, the best time to list your house this year is during the last two weeks of May. That timing matters, especially if your goal is to sell for the strongest possible price.

Zillow’s research shows that homes listed during this late-May window can sell for more. Depending on your local market, price point, and buyer demand, that could mean a noticeably higher sale price.

As Zillow explains:

“Why late spring? Buyer demand typically peaks before Memorial Day. Families want to move during the summer and settle in before the new school year. More buyers shopping at once can spark competition and lift prices.”

That timing makes sense. Many buyers want to be under contract before summer gets too far along, especially if they are trying to move before a new school year starts. When more buyers are actively looking, sellers may benefit from stronger competition.

ATTOM Data found a similar pattern after analyzing nearly 52 million home sales over the past 10 years. Their research shows that May has historically been one of the months when sellers achieve some of the highest returns.

So, while the “best week” may have passed according to one report, the spring window is still open.

What This Means if You’re Thinking About Selling

If you want to sell your house this spring, now is the best time to get serious about preparation.

That doesn’t not mean you need to tackle every home project on your list. When the listing window is short, the goal is to do the right things, not everything at once.

A local real estate agent can help you focus on updates that are most likely to matter to buyers in your area. They can also tell you whether the best time to list your house is slightly different in your specific market.

Here are some quick examples of things you might want to do before you sell, according to Redfin.

Likewise, your own local real estate agent may recommend:

- Improving curb appeal with fresh landscaping or exterior touch-ups.

- Decluttering and deep cleaning key living areas.

- Making small repairs buyers are likely to notice.

- Refreshing paint in high-impact rooms.

- Staging your home to highlight space and flow.

- Pricing strategically based on current local demand.

These steps can help your home make a stronger first impression without wasting time or money on projects that may not deliver a meaningful return.

The Right Strategy Matters More Than Perfect Timing

Timing can absolutely help when you are selling a home. But it’s only one piece of the equation.

To make the most of a late-May listing, your home still needs to be priced well, marketed effectively, and positioned to stand out from other homes on the market. That’s where local real estate expertise becomes especially valuable.

An experienced agent can help you understand what buyers are looking for right now, how much competition you may face, and what steps will help your home attract serious attention quickly.

Bottom Line: Preparation Is Key

Late May could be one of the best times to list your house, especially if you want to take advantage of strong spring buyer demand.

If you’re still thinking about selling, it’s not too late. The key is to act strategically, prepare your home the right way, and work with a local agent who understands your market.

Do You Need 20% Down? Most First-Time Buyers Pay Less

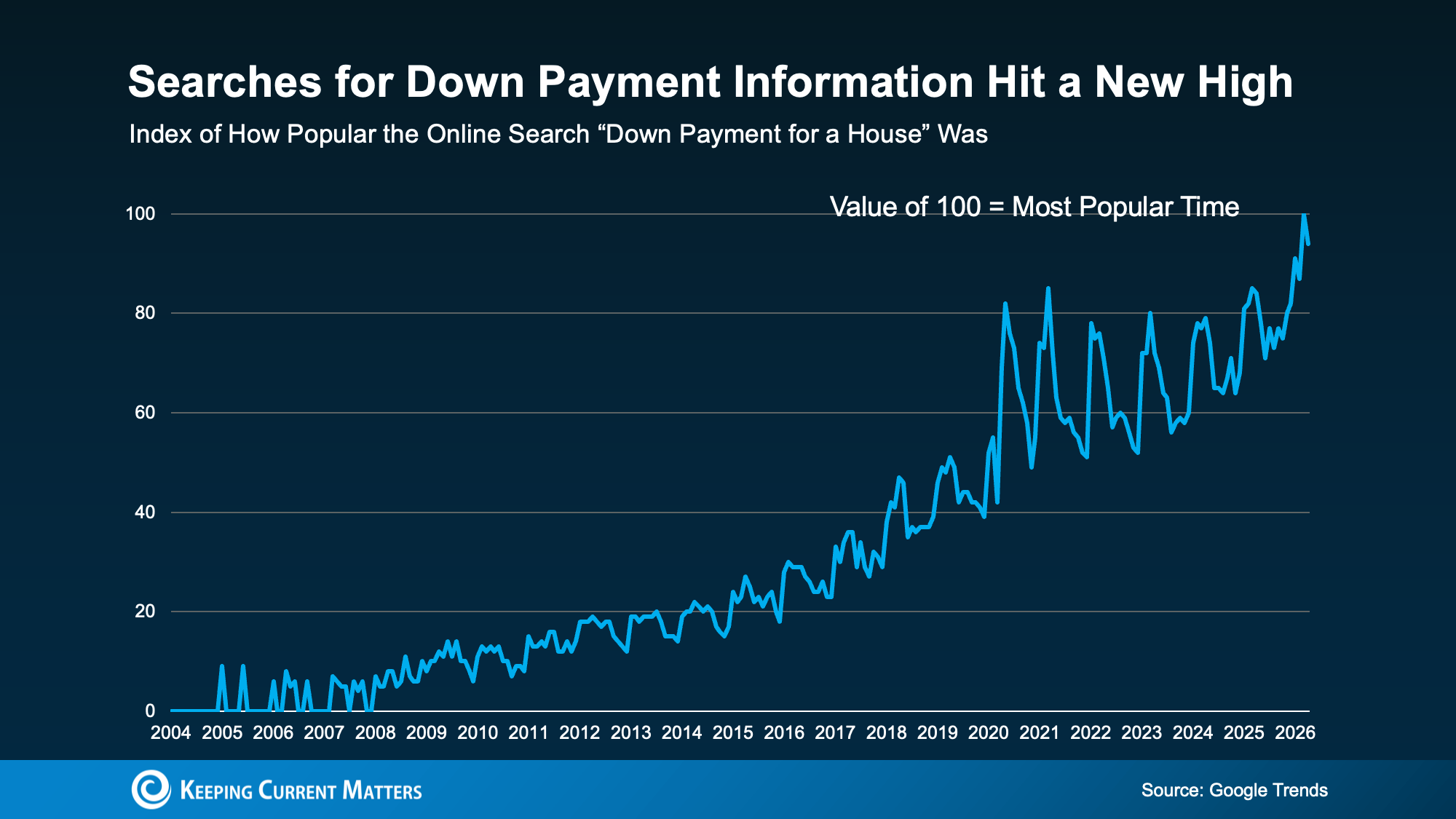

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

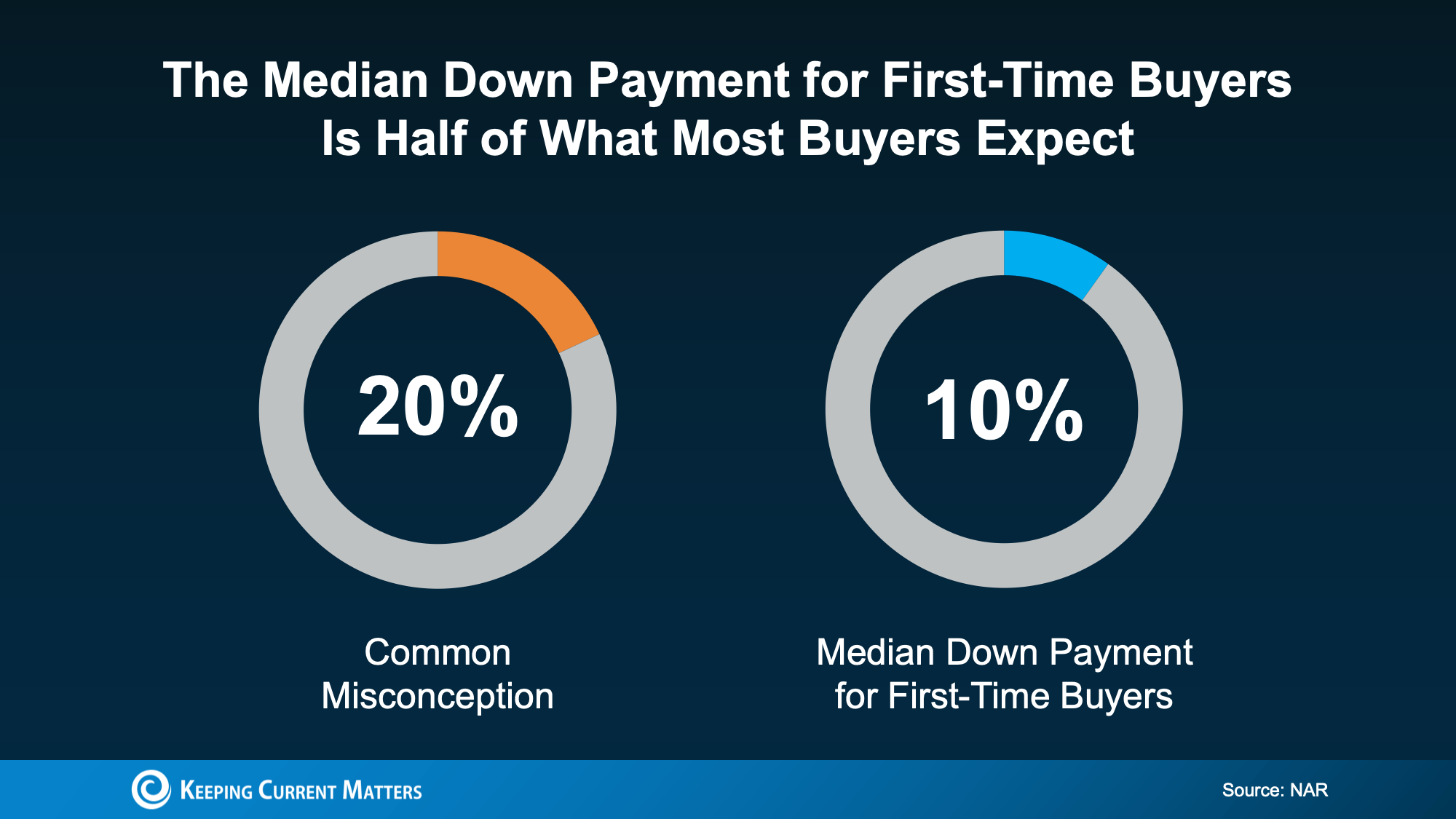

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

3 Things That Aren’t Going To Happen in Today’s Housing Market

There’s no shortage of uncertainty in today’s housing market, and that’s naturally fueling a lot of dramatic headlines. And if you’re trying to buy a home, that kind of noise can make your decision feel a lot more complicated.

In fact, a recent CNBC study asked homebuyers what they’re most concerned about, and the same three topics kept rising to the top:

- Mortgage rates

- The number of homes for sale

- Home prices

The challenge is that much of what people are hearing about these topics is driven by misconceptions, not facts. Let’s separate the headlines from what the data is really showing.

Misconception #1: “I Should Wait Because Mortgage Rates Are Going To Fall Dramatically”

One of the most common ideas circulating on social media is that mortgage rates are about to drop sharply, so waiting to buy is the smarter move.

But is that what experts are expecting?

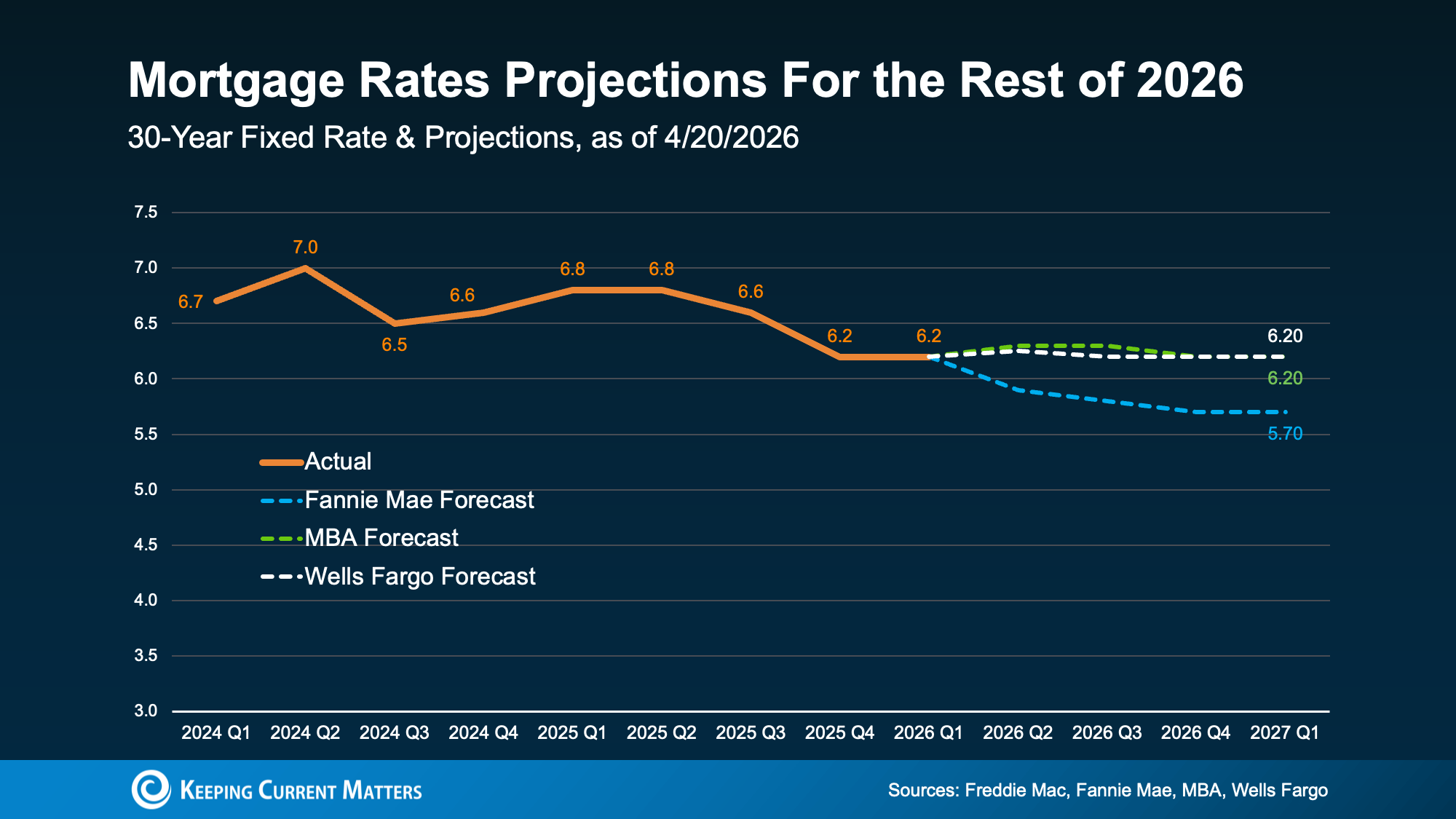

While mortgage rates have eased a little in recent weeks, forecasts still aren’t predicting any major declines. It’s more likely that rates will stay in the low 6% range this year.

And that’s not a remarkable shift from the rates we’re seeing today:

Obviously, a lot depends on inflation and the broader economy. But based on what we know right now, waiting for a big drop in mortgage rates may not play out the way many buyers hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

And even with rates where they are today, buying a home is already more affordable than it was a year ago. Even if rates don’t drop in the near future, home affordability is better now than a year ago.

Misconception #2: “There Are Too Many Homes for Sale”

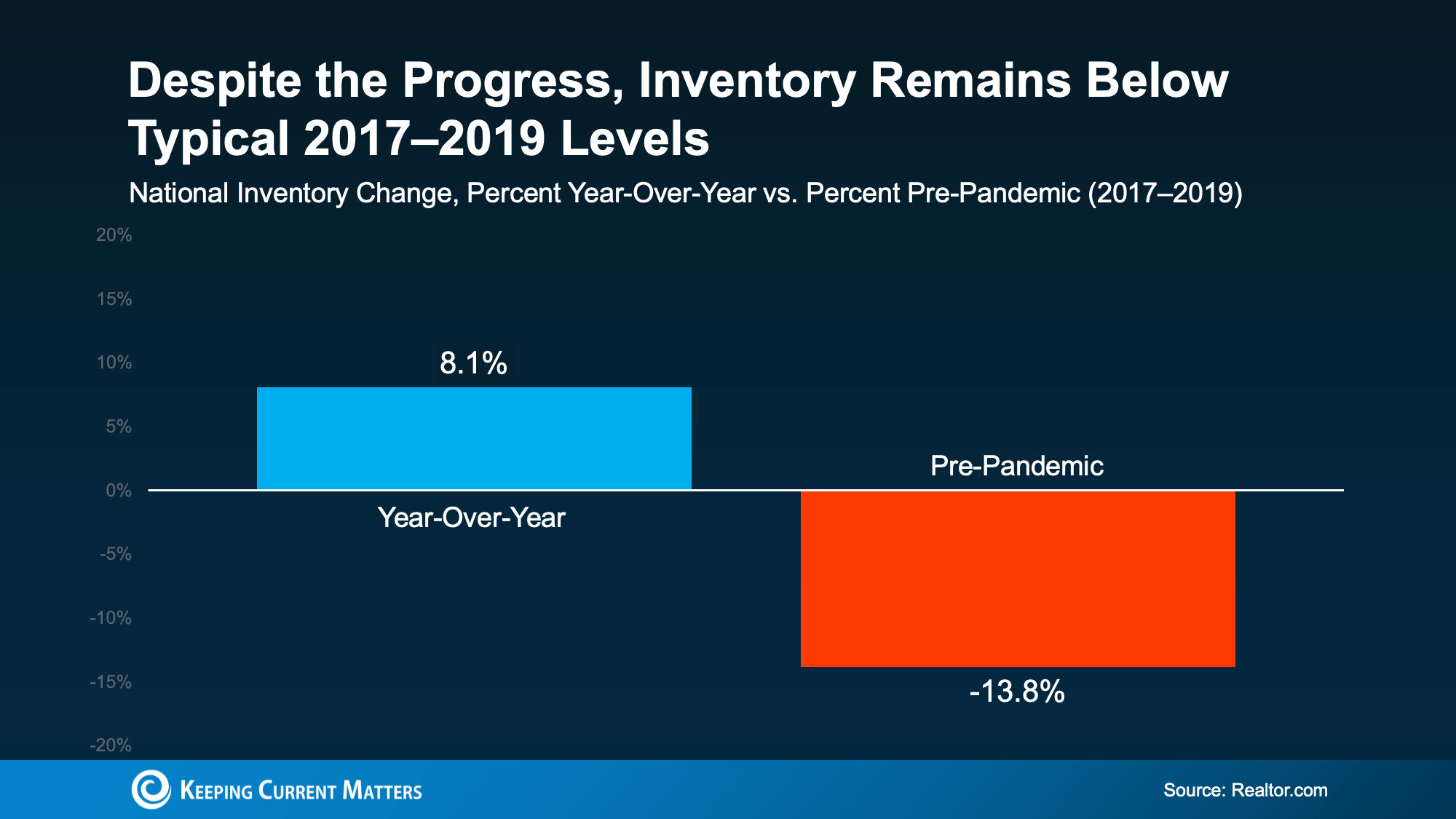

You may have heard that housing inventory is rising. Nationally, that’s true: the number of homes for sale is 8% higher than it was at this time last year. But that’s not bad news. In lots of markets, it’s easing the pressure on buyers.

The problem is that some headlines make good news sound like bad news. They focus on the fact that inventory is at its highest level since 2019 or highlight how many new homes builders are adding. That can make it sound like supply is growing too much, too fast.

But the bigger picture tells a different story.

According to new Realtor.com data, even though inventory is up over last year, it’s still nearly 14% lower than it was in the last normal housing market from 2017 to 2019:

And while local conditions vary, only 9 states have more inventory now than they did before the pandemic. That’s a major reason there aren’t enough homes for sale to trigger anything like the 2008 housing crash.

Misconception #3: “Home Prices Are About To Crash”

This is another common headline you’ve probably seen. This misconception comes from the fact that a few metros are actually seeing small price declines. Influencers are pointing to this to claim home prices are crashing. But this is absolutely not true nationally.

In most markets, home prices are still rising, not falling. Here’s why:

- Many homeowners are choosing not to sell to avoid giving up the low mortgage rate they locked in a few years ago. That continues to limit how much inventory can grow.

- Inventory remains below pre-pandemic norms. There still aren’t enough homes for sale to cause a widespread price crash.

- Even in markets with more listings, some sellers are pulling their homes off the market instead of making major price cuts.

Those are three big reasons home prices are not on track for a crash.

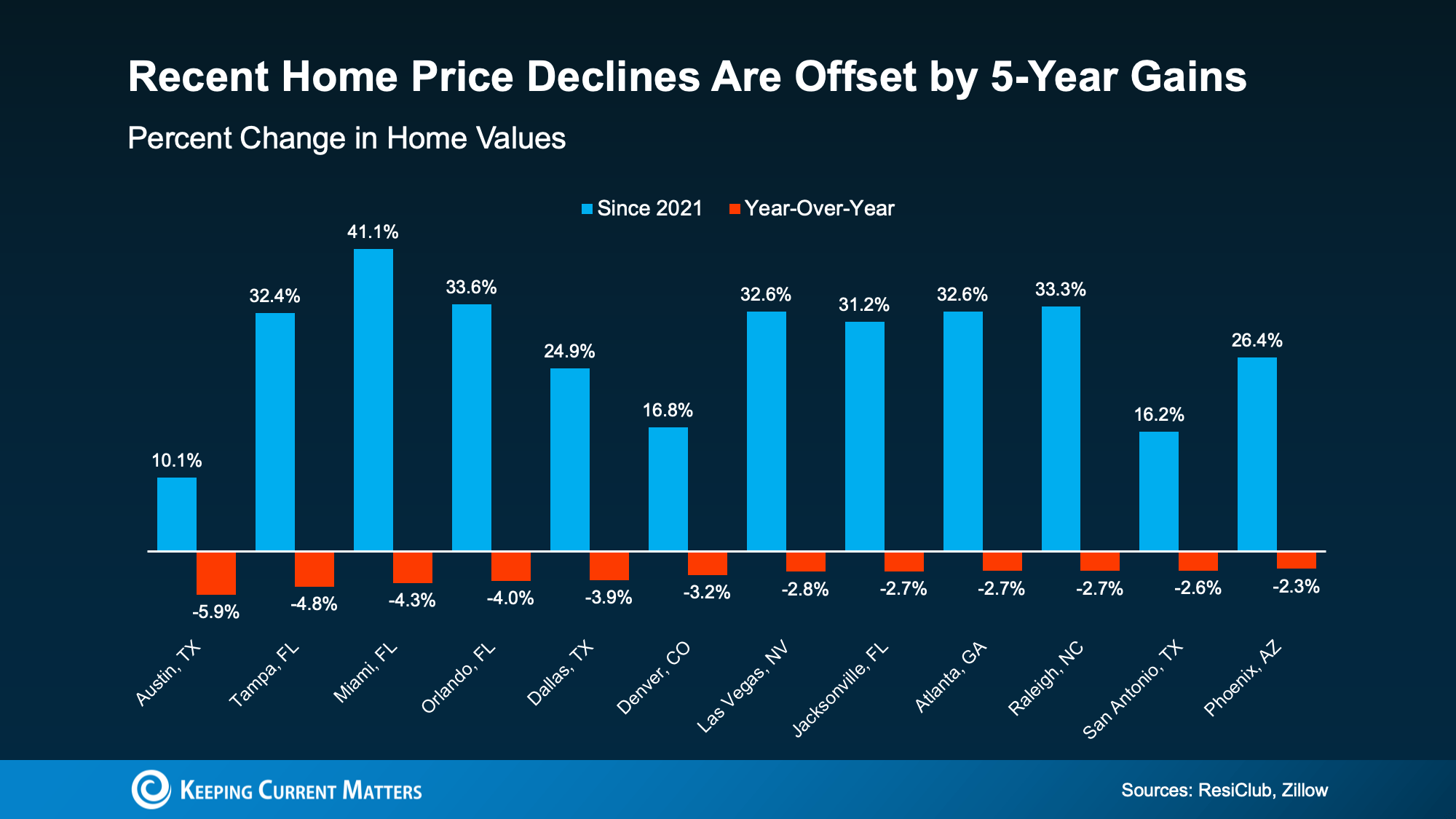

And even in the areas seeing small price declines, those drops are nowhere near enough to erase the huge gains most homeowners have built over the past five years:

These drops don’t signal a crash. They show the market settling after a few years of record-breaking spikes in prices.

Bottom Line: Get the Facts on Your Market

The discussions we see online can often exaggerate the negative and ignore the positive, especially in housing. If you want a clearer, truer idea of what’s happening with mortgage rates, housing inventory, and home prices in your market, talk to a trusted real estate professional.

Connect with a local real estate agent so you have an expert who can give you the real story on your local housing market.

Top 10 Best Housing Markets for First-Time Home Buyers This Spring

For many hopeful buyers, purchasing a first home has lately felt less like a goal and more like a long shot.

Not because you weren’t financially responsible. Not because you weren’t ready to make a move. But because, every time you checked the numbers, homeownership still didn’t feel realistic.

That’s why so many first-time buyers have put their plans on hold.

Now, after years of watching from the sidelines, this spring may finally bring new opportunities. Especially in certain housing markets where affordability and inventory are starting to improve.

The 10 Best Markets for First-Time Buyers

Zillow recently released its list of the top 50 metro areas for first-time home buyers this spring, and the top 10 housing markets stand out for good reason.

Here are Zillow’s top 10 best markets for new buyers in 2026:

- Jacksonville, FL

- Birmingham, AL

- San Antonio, TX

- Atlanta, GA

- Houston, TX

- St. Louis, MO

- Detroit, MI

- Raleigh, NC

- Baltimore, MD

- Louisville, KY

In these higher-ranked metros, Zillow says median-income households can afford 68% of all homes currently for sale.

This is a major shift, and one that could give buyers real options in some areas.

Not long ago, many buyers felt lucky to find even a few homes within reach. Today, in some markets, there are finally more realistic options for first-time buyers trying to break into the market.

What Makes These Housing Markets Stand Out?

These markets aren’t becoming more favorable for any single reason. Rather, several smaller trends are beginning to work together.

As Orphe Divounguy, Senior Economist at Zillow, explains:

“First-time buyers are finally seeing some light at the end of the tunnel. Affordability is still a challenge, but rising incomes, stabilizing prices and improving inventory are creating real opportunities in parts of the country. In the strongest markets for first-time buyers, they’ll find more choices, less competition and a clearer path to homeownership than they’ve had in years.”

That shift comes down to three key factors:

1. More Homes Are Coming to Market

According to Realtor.com, housing inventory is up 8.1% compared to last year.

More homes for sale means buyers have more choices. It can also reduce the pressure that comes with low-inventory markets, where bidding wars and quick decisions often make it harder for new buyers to compete.

2. Home Price Growth Is Slowing

While affordability is still a challenge in many areas, home prices aren’t rising as quickly as they were in recent years.

Slower price growth can help keep more homes within reach, and in some markets, prices may even be easing enough to bring new neighborhoods back into play.

3. Incomes Are Rising

Wage growth is also helping improve the picture for buyers.

When household income increases, it can offset part of the affordability challenge, even when mortgage rates remain elevated. As Mark Fleming, Chief Economist at First American, explains:

“Income growth has outpaced house price growth for 19 straight months, boosting house-buying power even as mortgage rates remain elevated.”

Taken together, these trends are creating better conditions for new buyers in select markets across the country.

What If Your Market Didn’t Make the List?

If your city did not make Zillow’s top 10, or even the top 50, there’s no reason to worry. You’re not out of options.

Opportunities exist in any market. The key is knowing where to look and having the right guidance along the way.

Even within the same metro area, one buyer’s experience can be very different from another’s. A lot depends on local knowledge and strategy. The right real estate agent can help you identify overlooked opportunities, such as:

- Neighborhoods where prices have not climbed as fast.

- Areas with more available inventory.

- New construction communities offering builder incentives.

These kinds of opportunities may not make national headlines, but they can make a meaningful difference when trying to buy your first home.

Bottom Line: More Options for First-Time Home Buyers

For a long time, first-time home buyers have felt stuck, waiting for the market to shift in their favor.

This spring, that may finally be happening in certain markets.

With more inventory, slower price growth, and rising incomes, buying a first home may feel more realistic than it has in years. And even if your market isn’t on Zillow’s list, there may still be neighborhoods or communities nearby offering a better chance to get started.

If you want to find out where those opportunities exist in your local market, connect with a trusted real estate agent who knows where to look.

Is an Adjustable-Rate Mortgage Right for You? A Homebuyer’s Guide

If you’ve been shopping for a home lately, you’ve likely felt the pressure of today’s affordability challenges. Higher home prices and mortgage rates have made it harder for many buyers to stay within budget. That’s one reason adjustable-rate mortgages, or ARMs, are getting more attention again.

For some homebuyers, an ARM can offer welcome savings upfront. But before you go that route, it’s important to understand how these loans work, why they appeal to certain buyers, and what the long-term risks might be.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage is a home loan that starts with a fixed interest rate for a set number of years. After that initial period ends, the rate can adjust at scheduled intervals based on market conditions.

As Business Insider explains:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

That’s the biggest difference between a fixed-rate mortgage and an ARM. A fixed-rate loan offers predictability, while an ARM may give you a lower payment at first but less certainty later.

It’s true that costs like property taxes and homeowners insurance can still change with a fixed-rate mortgage. But the principal and interest portion of the payment generally stays steady. With an ARM, your monthly payment can rise or fall once the fixed period ends.

Why More Home Buyers Are Considering ARMs

The main reason buyers look at adjustable-rate mortgages is simple: lower initial costs.

Business Insider puts it this way:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

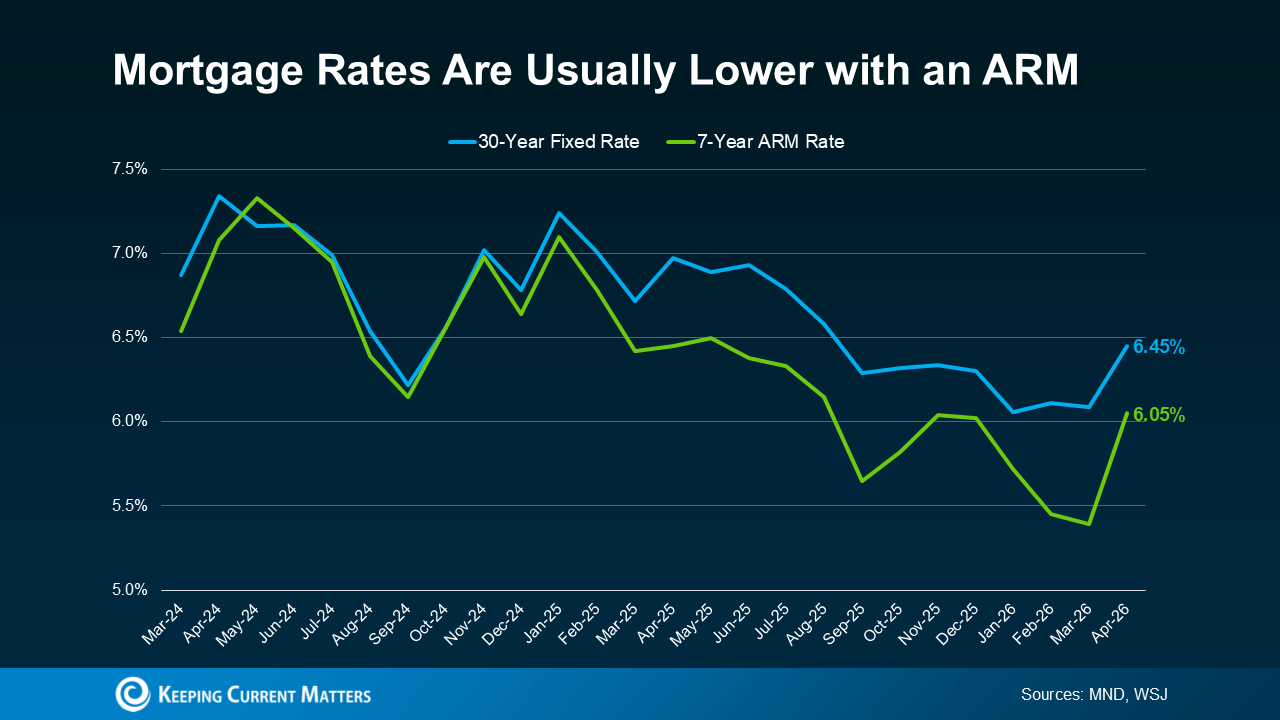

That upfront savings can matter, especially in a market where every dollar counts. Recent reporting from Mortgage News Daily and The Wall Street Journal show that ARM rates have been coming in lower than 30-year fixed mortgage rates.

For many buyers, even modest monthly savings can make a difference. For example, Redfin found that a typical buyer could save about $150 per month by choosing an ARM instead of a 30-year fixed mortgage. Savings like that can help some buyers qualify for a home sooner or make their monthly budget more manageable.

Why Adjustable-Rate Mortgages Are Making a Comeback

More homebuyers are deciding that a lower payment today is worth considering, even if it means taking on more uncertainty later.

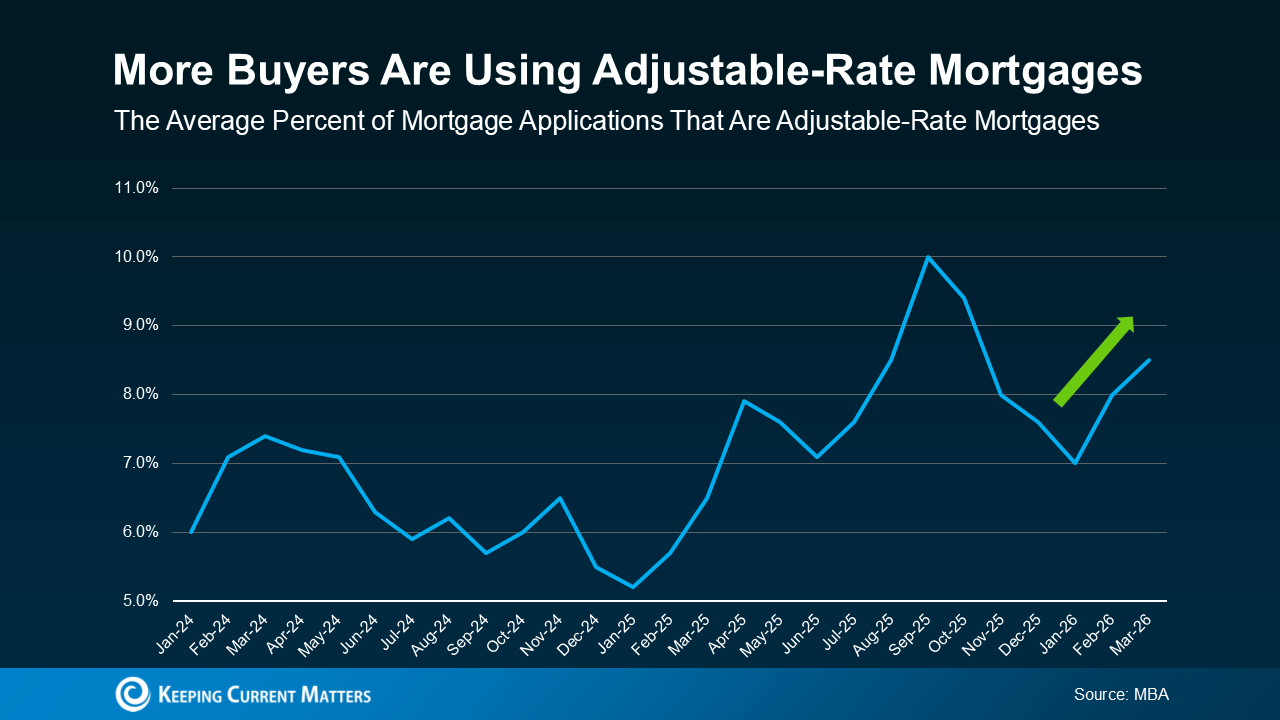

Recent reports from the Mortgage Bankers Association (MBA) show that the share of buyers choosing ARMs has increased in recent years. That doesn’t mean ARMs are becoming the right fit for everyone. But, it shows that some buyers are using them as a strategy to deal with affordability challenges in the current market.

For anyone who remembers the 2008 housing crash, this trend may sound concerning at first. But today’s lending environment is very different.

In the past, some borrowers were approved for loans they couldn’t realistically afford once the interest rate adjusted. Today, lending standards are tighter, and lenders generally evaluate whether borrowers could still manage the payment if rates rise. So while ARMs are becoming more common again, that alone doesn’t point to another housing crisis.

The Pros and Risks of an ARM

An adjustable-rate mortgage can make sense in the right situation, but it depends on your financial plan and your comfort with risk.

An ARM may be worth considering if:

- You expect to move before the rate adjusts.

- You believe your income will increase over time.

- You need a lower initial payment to make homeownership possible now.

Still, there are trade-offs to consider.

Once the fixed-rate period ends, your interest rate can change, and your monthly payment could increase significantly depending on where mortgage rates are at that point. There’s also no guarantee rates will fall in the future, which means refinancing later may not be as easy or as beneficial as some buyers hope.

That’s why it’s important to think beyond the introductory rate. Make sure you understand how long the fixed period lasts, how often the rate can adjust, and how much your payment could increase over time. Most importantly, talk through your options with a trusted lender and financial advisor before making a decision.

Bottom Line: Is an ARM Right for You?

Adjustable-rate mortgages are regaining popularity because they can make buying a home more affordable in the short term. For some buyers, that lower upfront payment can be a helpful tool. But an ARM isn’t necessarily the right move for everyone.

The best decision comes down to understanding how the loan works, weighing the risks, and making sure it fits your long-term goals.

If you’re considering an adjustable-rate mortgage yourself but are still on the fence, reach out to us today. We can connect you with a qualified lender in your area who explore your options with you.

Should You Still Buy a Home Right Now? What Buyers Need To Know

Between nonstop economic headlines, global uncertainty, and ongoing concerns about affordability, it’s understandable to wonder whether now is still a smart time to buy a home.

The good news is this: current events may be influencing the housing market, but they have not taken homeownership off the table. For many buyers, the opportunity is still there. It just may require a more thoughtful strategy than it did a few months ago.

Mortgage Rates Have Risen Slightly. Here’s What’s Behind It

After trending downward for much of 2025, mortgage rates have climbed again over the past month. Experts point to a mix of global events and broader economic pressures as key reasons why.

As Mark Fleming, Chief Economist at First American explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

So what does that mean if you’re thinking about buying a home? Should you wait for conditions to settle before making a move?

Not necessarily.

Your Opportunity To Buy Hasn’t Disappeared

There’s no denying that buying felt a bit more affordable when mortgage rates were closer to 6%. Now that rates are hovering in the mid-6% range, monthly payments are naturally a little higher.

But it helps to take a step back and look at the bigger picture.

For example, if you’re financing a $500,000 home, a rate in the mid-6s could still mean a monthly payment that is roughly $300 lower than what buyers were facing early last year.

That means today’s higher rates have not erased all the progress we’ve seen. In fact, buying a home can still be more affordable than it was just a year ago.

Yes, your payment may have been lower a few weeks ago. But trying to perfectly time the market rarely works in your favor. Conditions can shift quickly, and hindsight always makes past decisions look easier.

Instead of waiting for the “perfect” moment, focus on making the best decision based on your goals, finances, and today’s market conditions.

Expect Mortgage Rate Volatility

One thing buyers should be prepared for is continued movement in mortgage rates.

Rates may keep rising or falling in the weeks and months ahead as new economic reports are released and world events continue to unfold. That kind of uncertainty can feel frustrating, but it’s also part of today’s market.

The truth is, you can’t control what happens with inflation, global events, or mortgage rates next week. What you can control is how prepared you are when the right opportunity comes along.

That preparation can make all the difference.

If You Need To Move, You Still Have Options

For many buyers, the decision to move is not just about market timing. Life keeps moving, even when the market feels unpredictable.

Maybe your family is growing. Maybe you’re relocating for work. Maybe your current home no longer fits your lifestyle or needs. Those reasons still matter, and they may be more important than waiting for rates to change.

Buyers who are moving forward right now are often doing so because their personal situation makes it the right time.

And the good news is there are still strategies that can help make a purchase more manageable.

For example, some buyers are exploring adjustable-rate mortgages (ARMs) to secure a lower initial rate. That approach is not right for everyone, but it’s one example of how flexibility and planning can create opportunities in today’s market.

A Smart Plan Starts With the Right Experts

In a market like this, having a plan matters more than ever.

Working with a trusted real estate agent and lender can help you:

- Understand what you can realistically afford at today’s rates

- Review financing options, including ARMs and buyer assistance programs

- Stay informed as market conditions shift

- Make confident decisions based on your goals, not just the headlines

The right professionals can help you look beyond the noise and focus on what makes sense for your specific situation.

Conclusion

Uncertainty in the market does not mean you’re out of options.

If you need or want to move, buying a home may still be the right decision. The key is to go in with a solid plan, the right support, and a clear understanding of your financing options.

Homeownership is still possible. You just need the right strategy for today’s market.

The Best Time To List Your House Is Almost Here

Spring is usually one of the strongest seasons to sell a home, but according to research from Realtor.com, one specific week tends to stand out year after year. And it’s almost here.

Based on historical housing market trends, the best week to list your house this year is April 12–18.

Here’s why that window can be especially favorable for sellers.

Buyers Are More Active

Realtor.com reports that homes listed during this week typically receive 16.7% more views than the average week. In a market where buyers have more choices, extra visibility can make a real difference.

More attention early on can help generate stronger interest, more showings, and a better overall start to your sale.

Homes Sell Faster

More buyer activity can also lead to a quicker sale. Realtor.com found that homes listed during this week spend 17% less time on the market than usual.

That matters, especially in a market where some homes are taking longer to sell than they did a year ago. A faster sale can mean less stress, fewer disruptions, and more momentum from the start.

Sellers May Get a Better Price

As inventory grows, buyers often feel more comfortable asking for repairs, concessions, or price reductions. But during this early spring window, Realtor.com says about 18.9% fewer homes need a price cut.

That gives sellers a stronger chance of listing confidently and holding closer to their asking price.

More Money in Your Pocket

According to the same study, a well-prepared home listed during this week can sell for about $5,300 more than the average week and about $26,000 more than homes listed at the beginning of the year.

For sellers, that’s a meaningful difference.

More views, less time on the market, and a better shot at top dollar all make this one of the most appealing times to list.

What You Should Do Now To Prepare

If you’re thinking about selling and want to take advantage of this timing, the next step is simple: connect with a local real estate agent.

A trusted local agent can help you decide how to prepare based on what is happening in your market. Real estate trends can vary by city, neighborhood, and even price point, so local insight matters.

Your agent can help you figure out:

- What updates are worth making before you list

- Which repairs should come first

- What buyers in your area care about most

- Which small improvements can have the biggest impact

For some sellers, getting ready may only take a couple of weekends. Fresh paint, basic landscaping, or a deep clean can go a long way.

For others, taking a few extra weeks to make light updates may be the smarter move. And that’s completely fine. While mid-April may offer an advantage, it is not the only good time to sell.

Spring Still Offers a Strong Opportunity

Zillow says May is also one of the best times to list a home. That means sellers still have a strong window of opportunity throughout the spring season.

So while April 12–18 may be a standout week, it’s not your only shot at a successful sale.

Conclusion

Listing your house in mid-April could help you attract more buyers, sell faster, and maximize your sale price. But the bigger opportunity is the spring market as a whole.

The real question is: what do you need to do now to get your home ready to list?

For anyone planning a spring move, now is the time to start preparing. The sooner you connect with a local agent, the sooner you can make a plan that fits your goals and your timeline.

3 Key Steps for First-Time Home Buyers

Buying your first home is exciting, but it can feel a bit overwhelming. When you’ve never gone through the buying process before, it’s easy to wonder where to start and what to do first.

The good news is that you don’t need to figure out everything out on your own, or all at once. The best approach is to take it all step by step.

If you’re getting ready to buy your first home, here are the three most important steps to focus on first.

1. Build Your Team: Don’t Do It Alone

Buying a home is not a solo project. Having the right professionals on your side can make the entire experience smoother, less stressful, and more successful.

Here are two key people every first-time home buyer should have in place early:

A local real estate agent

A knowledgeable local agent will guide you from your first showing all the way to closing day. They can help you understand the market, explain each step of the process, and make sure you feel confident in the decisions you make.

A trusted lender

A lender will help you explore your mortgage options, estimate your monthly payment, and understand what price range makes sense for your budget. Having that info early helps you shop smarter and avoid unwanted surprises later.

When you have the right team in place, you can find your new home with more clarity and confidence.

2. Prep Your Finances: Build a Strong Foundation

It goes without saying that your finances play a major role in the homebuying process. They affect what you can afford, how competitive your offer may be, and how comfortable you’ll feel once you own the home.

Here are the main financial steps first-time home buyers should take:

Check your credit score

Your credit score can affect the loan programs available to you and the mortgage rate you receive. Checking it early gives you time to improve it if needed.

Save for your down payment and closing costs

Many buyers focus only on the down payment, but closing costs are also an important part of the equation. Saving for both can help reduce last-minute stress.

Research first-time buyer assistance programs

There are programs designed to help first-time home buyers with upfront costs. Depending on where you live and your financial situation, you may qualify for assistance that helps you buy sooner than expected.

Talk to a lender about your mortgage options

Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all work differently. Understanding the pros and cons of each option can help you choose the loan that best fits your needs.

Get pre-approved

A mortgage pre-approval gives you a clearer picture of how much a lender may be willing to lend you. It also helps you set a realistic price range and shows sellers you’re serious when it’s time to make an offer.

Set a realistic monthly budget

Your mortgage payment is only part of the cost of homeownership. You also need to account for utilities, home insurance, maintenance, and everyday living expenses. Setting a realistic budget helps ensure your home feels affordable, not overwhelming.

Being confident in your finances before you start house hunting can help you feel more prepared and better positioned in a competitive market.

3. Gather Your Documents: Save Time and Reduce Stress

Once you’re ready to move forward, your lender will need to verify your income, assets, and financial history. Gathering your documents ahead of time can help speed up the loan process and avoid unnecessary back-and-forth.

Here are some of the most common documents lenders may ask for:

W-2s and tax returns from the past two years

These help verify your income history and show consistency over time.

Recent pay stubs, usually from the last one to two months

These confirm your current income and employment.

Bank statements from the past two to three months

These show your available funds, spending patterns, and where your down payment money is coming from.

Investment account statements from the past two to three months

If investments are part of your financial picture, your lender may want to review them as well.

A copy of your driver’s license

This is used to verify your identity during the loan process.

Your residential history for the past two years

Lenders may request this to confirm your housing background and stability.

Statements for outstanding debts from the past two months

This may include student loans, car loans, and credit cards. These debts help lenders calculate your debt-to-income ratio.

Proof of supplemental income

If you receive bonuses, commissions, freelance income, or child support, you may need documentation to show that income can be counted.

Keep in mind that document requirements and timelines can vary by lender. Still, having these items ready is a smart way to stay organized and avoid potential hiccups.

Conclusion

Buying your first home doesn’t mean you need to have every detail figured out from day one. It just means starting your journey with a plan.

When you gather the right people, prepare your finances, and organize your documentation early, you give yourself a much better chance to buy with confidence.

If you want help understanding any part of the process or are ready to take the first step to homeownership, connect with a trusted real estate agent.

Home Affordability Improved in All 50 States: What Buyers Need To Know

For the past few years, affordability has been one of the biggest reasons buyers have put their home search on hold. Maybe you did the same.

At some point, you may have looked at the numbers, saw what a monthly mortgage payment would be, and decided to wait for the market to become more manageable. But there’s encouraging news you may have missed.

Over the past year, housing affordability has improved in all 50 states. Yes, every single one.

That’s according to new research from First American. And while buying a home is still more expensive than what’s historically normal, the affordability pressure many buyers have felt over the last several years is finally starting to ease.

Some Markets Are Seeing Bigger Improvements

One of the most important things to understand is this isn’t limited to one part of the country or just a few select markets. Affordability is improving almost all over the country.

Of course, real estate is always local. Conditions can vary a lot from one state, city, or neighborhood to the next. But overall, the market is becoming more favorable for buyers. In fact, affordability has improved in 48 of the top 50 metros over the past year.

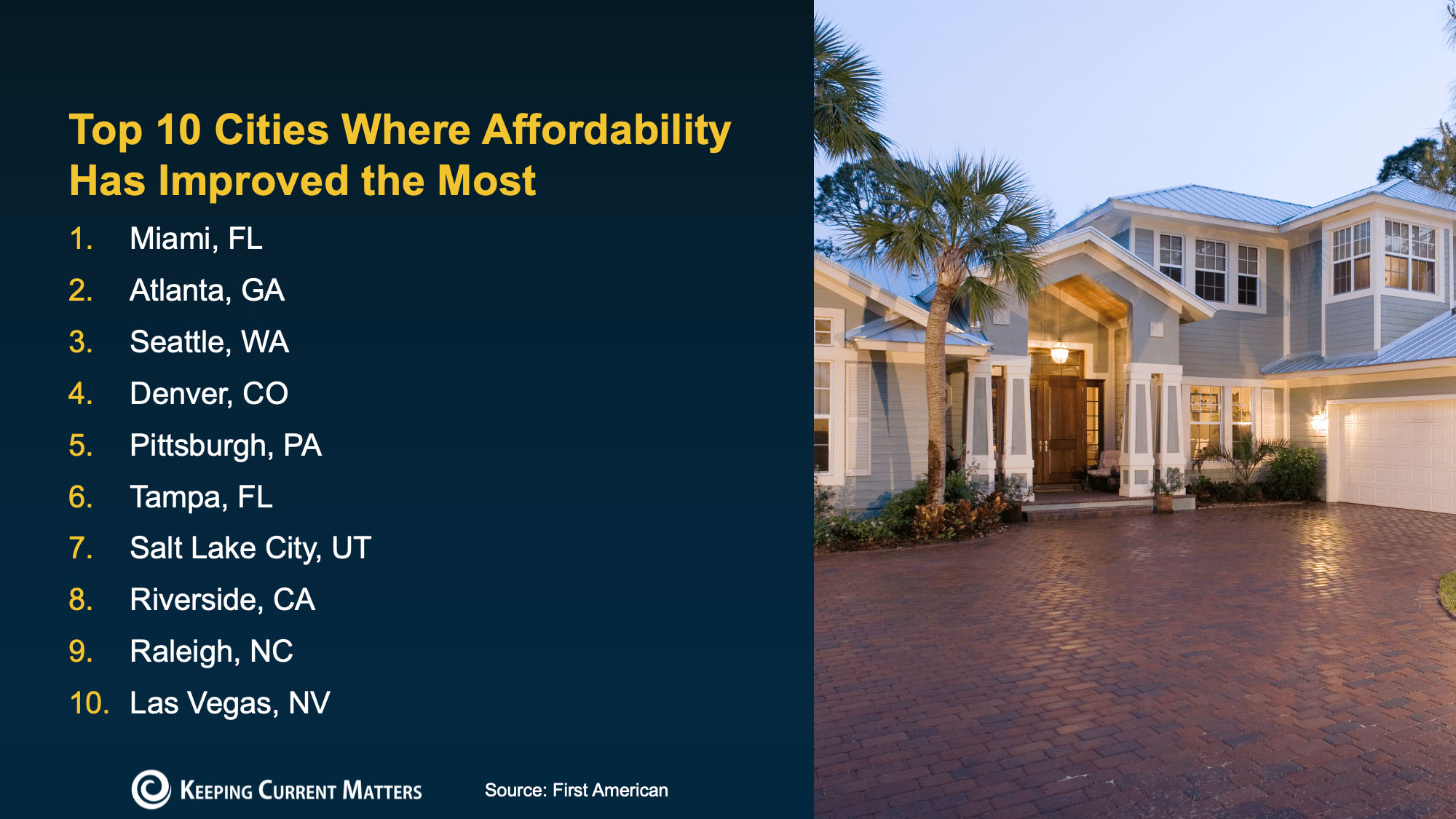

That same research also highlights the top 10 cities seeing the biggest gains in affordability:

Top 10 Cities Where Home Affordability Has Improved the Most

- Miami, FL

- Atlanta, GA

- Seattle, WA

- Denver, CO

- Pittsburgh, PA

- Tampa, FL

- Salt Lake City, UT

- Riverside, CA

- Raleigh, NC

- Las Vegas, NV

If you’re wondering why some markets are improving faster than others, a lot of it comes down to home inventory.

When there are more homes for sale, the market becomes more balanced. This can help improve affordability by giving buyers more negotiating power. With more options available, buyers may have a better chance of finding a home that fits their budget, and they may also be in a stronger position to ask for seller concessions, price reductions, or closing cost assistance.

That can make a bigger difference than many people expect.

What Does This Mean for Buyers?

Home affordability challenges haven’t disappeared altogether, obviously. Buying a home is still a major financial decision, and housing prices remain high in many markets. But the overall nationwide trend is moving in a direction that gives buyers more opportunity than they’ve had in recent years.

As Chen Zhao, Head of Economic Research at Redfin, explains:

“The housing affordability crisis is showing signs of easing. . . opening the door for more Americans to make the jump to homeownership.”

Conclusion

If you’ve been waiting on the sidelines for affordability to improve, this may be the sign you’ve been hoping for. To find out what’s happening in your local market and how much buying power you may have today, connect with a trusted local real estate agent.