Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Renting vs. Buying: Which Home Option Is Right for You?

Between stubborn mortgage rates and rising home prices, you’ve probably mulled over renting vs. buying a home. In market conditions like these, renting and waiting to buy can feel like your only realistic option. This can be the truth in many cases, and buying before you’re ready can be a costly mistake.

But the short-term savings of renting can sometimes trap you in a cycle, preventing you from making wealth-building investments. Over time, this can actually end up costing you more than buying a home early and slowly building equity. Unsurprisingly, a recent survey from Bank of America found that 70% of prospective homebuyers feel renting could hinder their financial future.

Ultimately, the pros and cons of renting and buying come down to your own short-term and long-term financial goals. If you’re feeling torn over whether you should nest or invest, take these major differences into account to decide.

Homeownership Builds Your Wealth Over Time

Apart from giving you your own place to live, homeownership grants the important bonus of building your wealth over time. This is because home prices usually rise as time goes on, meaning waiting longer to buy costs you more. This isn’t always true of every housing market, but the general national trend tends to speak for itself.

The average home sale price has more than tripled in the past 30 years.

Even better, your home equity also grows over time when you’re a homeowner. Equity is the difference between what your home is worth and what you still owe on your mortgage. Your equity grows with each mortgage payment you make, and this builds your net worth over time.

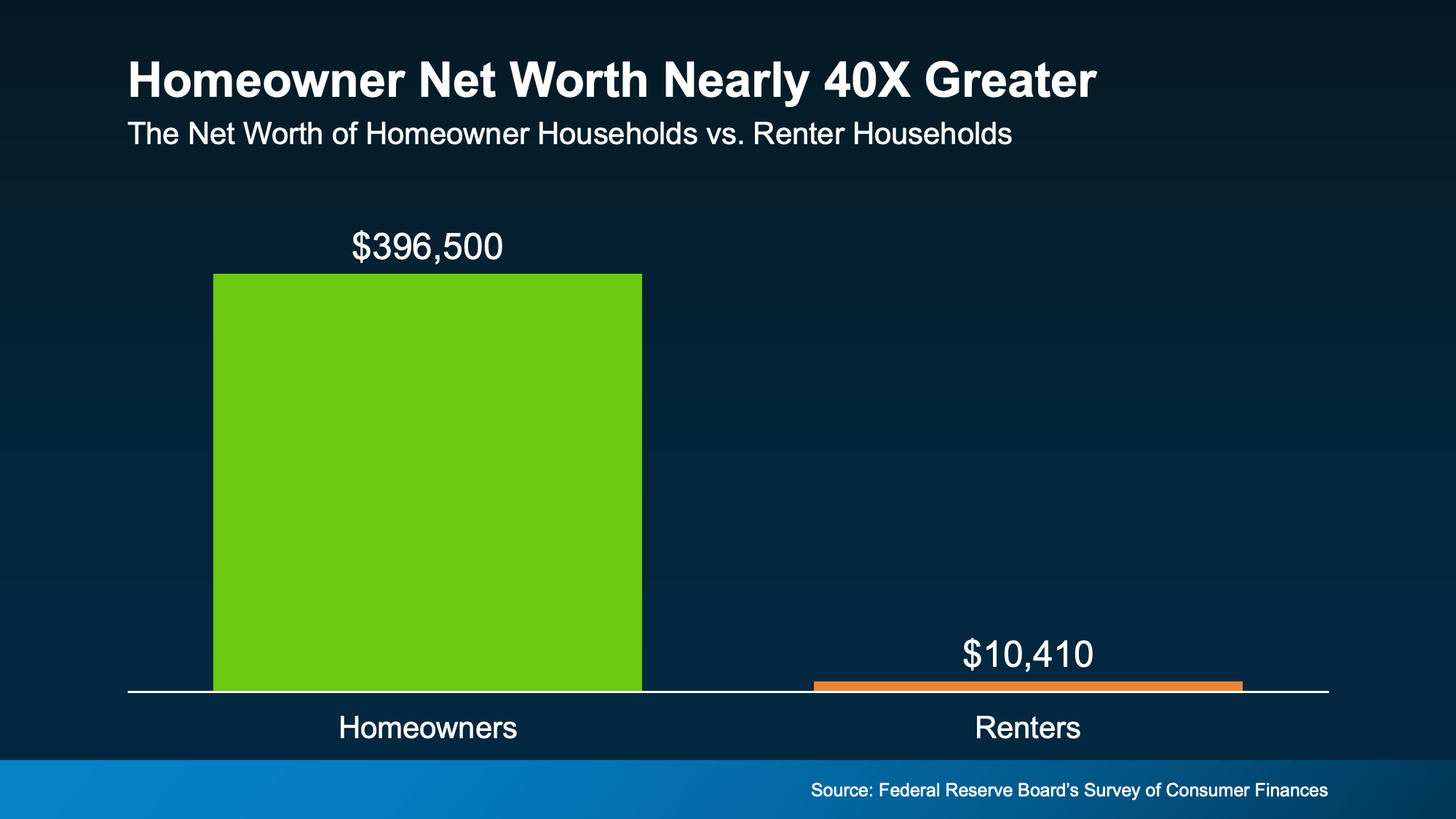

According to the Federal Reserve, the average homeowner’s net worth is nearly 40 times greater than that of a renter. That’s a life-changing difference, and seeing it represented visually really drives the point home.

The average net worth of a homeowner household is almost 40X greater than that of a renter household.

This massive difference in personal wealth is just one of the reasons that Forbes says:

“While renting might seem like [the] less stressful option . . . owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

Renting Helps You Save in the Short Term

Compared to homeownership, renting offers lower monthly payments and the freedoms of relatively negligible commitment and responsibility. This often makes renting feel like the safer option, and it usually is, at least in the short term. But in the long term, renting can land you in a trap that prevents you from building real wealth.

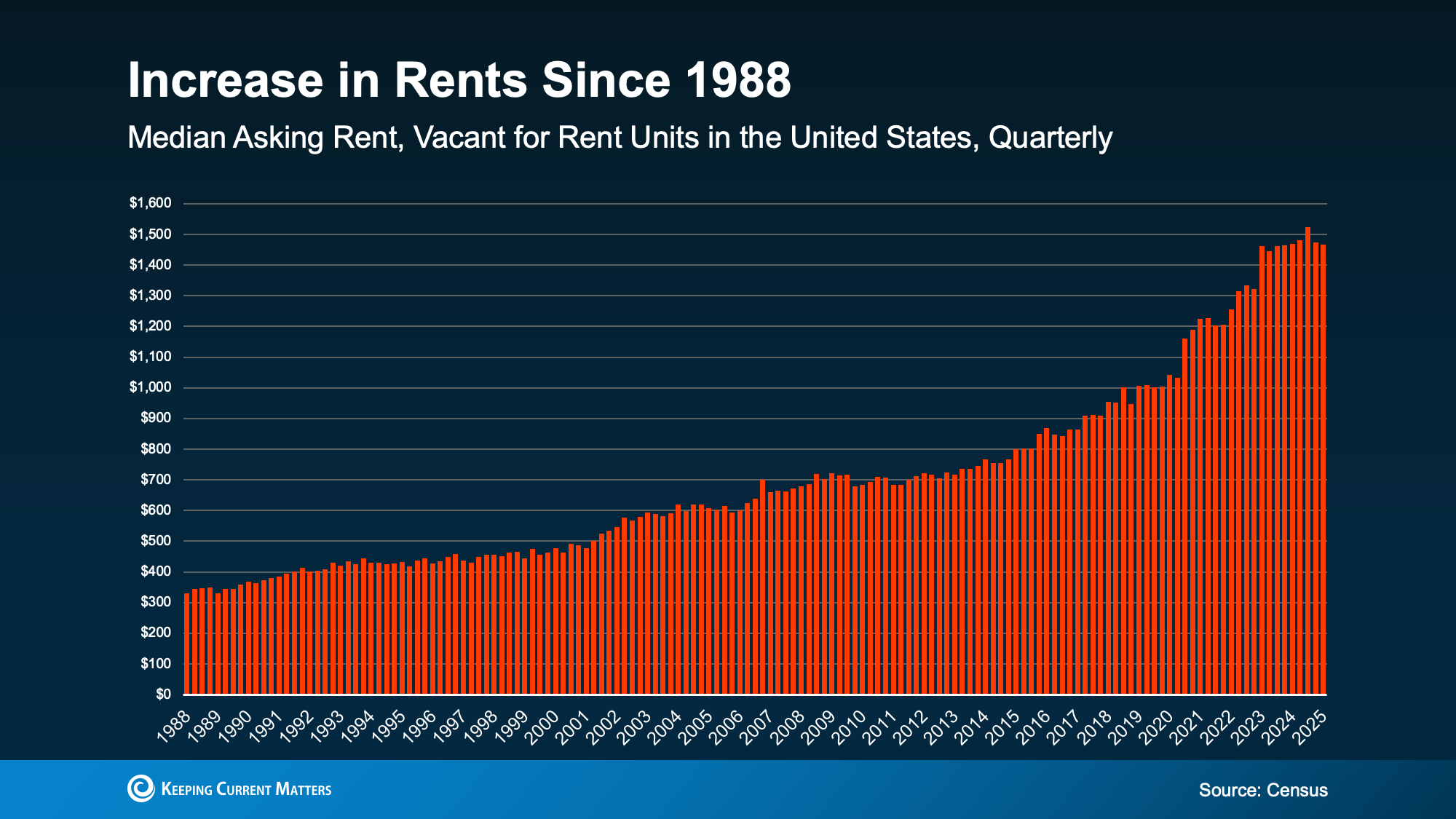

Rent tends to rise along with home prices, and this has been true for decades. Rental costs have been somewhat stable recently, but they almost never trend downward. This trap of paying increasing rent without building wealth can make buying a home feel impossible.

Like home prices, rental costs have risen dramatically in the past several years.

Financial uncertainty like this can have a real, lasting impact on any of your financial decisions. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

Rent money doesn’t come back to you, and that means it doesn’t grow your wealth. The only mortgage it’s paying is your landlord’s.

So, whether you’re renting or owning, you’re paying off a mortgage. The question is: whose mortgage do you want to pay?

Renting vs. Buying: What Really Matters

Here’s another way to look at renting vs. buying. Rent money is gone once you pay it. Payments toward your own house build equity, like a savings account you can live in. Obviously, buying comes with higher upfront costs and more long-term responsibility. But the reward is a stable investment that grows over time. And while buying a home often feels out of reach, a solid plan can get you there.

As Realtor.com Senior Economist Joel Berner explains:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

Conclusion

Renting may be cheaper in the short term, but it can cost you more over time without building your wealth. If you’re weighing the pros and cons of renting vs. buying, consider your long-term financial goals. Short-term saving can trap you in an endless cycle of renting, but buying without planning can be financially overwhelming.

If you’re ready to make the leap from renting into buying a home, contact us today. We’d be happy to connect you with a local agent who can make your dreams a reality.

How Could a Recession in 2025 Affect the Housing Market?

As talk about economic slowdowns runs wild, worries about a potential recession in 2025 are on the rise. Naturally, many homeowners are wondering what a recession could do to the value of their home, and their buying power.

Using historical data from recessions of decades past, let’s see how a recession might affect the housing market in 2025.

A Recession Won’t Lower Home Prices

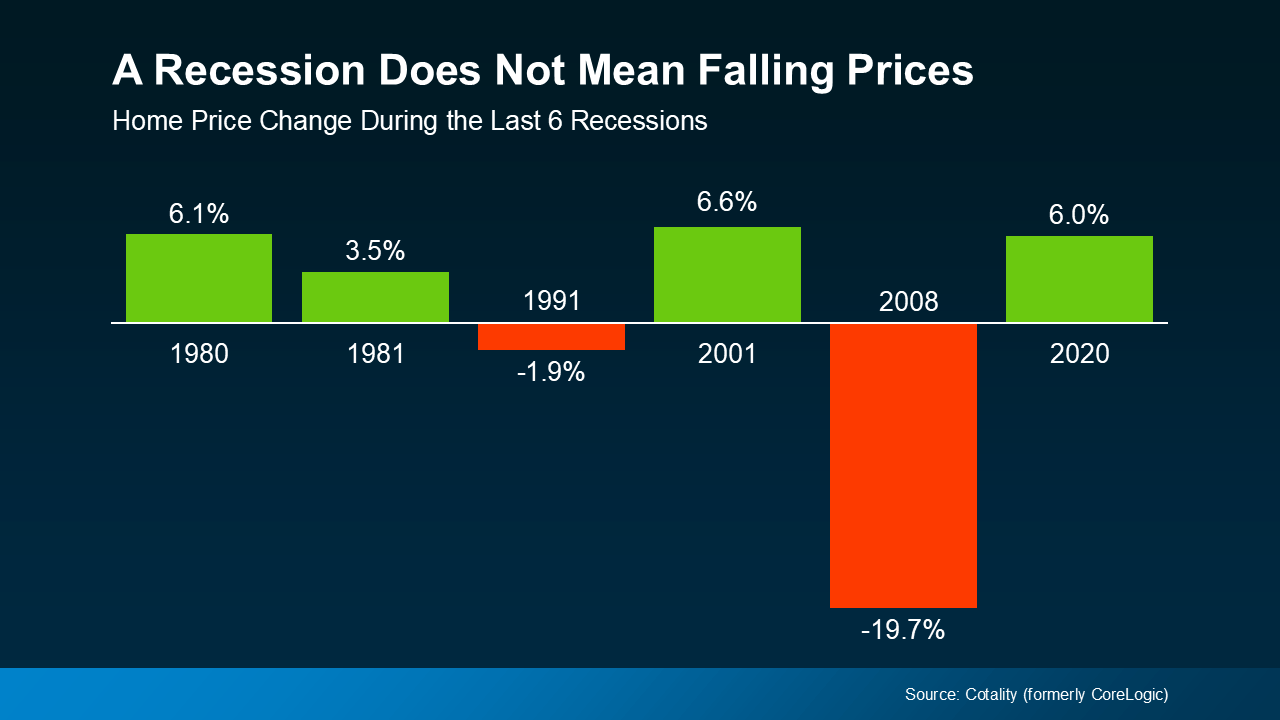

It’s a common misconception that a recession will cause home prices to crash, like they did in 2008. In reality, 2008 was the only time the housing market saw such an extreme, dramatic drop in prices. Overflowing home inventory caused that price crash, and conversely, low inventory has prevented a similar crash in the years since.

Even in markets where housing inventory is up, it’s still far below the listing oversupply that caused the 2008 crash. Indeed, according to data from Cotality, home prices actually increased during four of the last six major recessions.

As the graph shows, a recession doesn’t necessarily mean that home prices will crash, or even drop. In reality, historical data shows that home prices usually continue along their current trajectory when a recession hits. And at the moment, home prices are still rising nationally, but at a more normalized rate. So, as the market stands now, a recession in 2025 would most likely drive prices even higher.

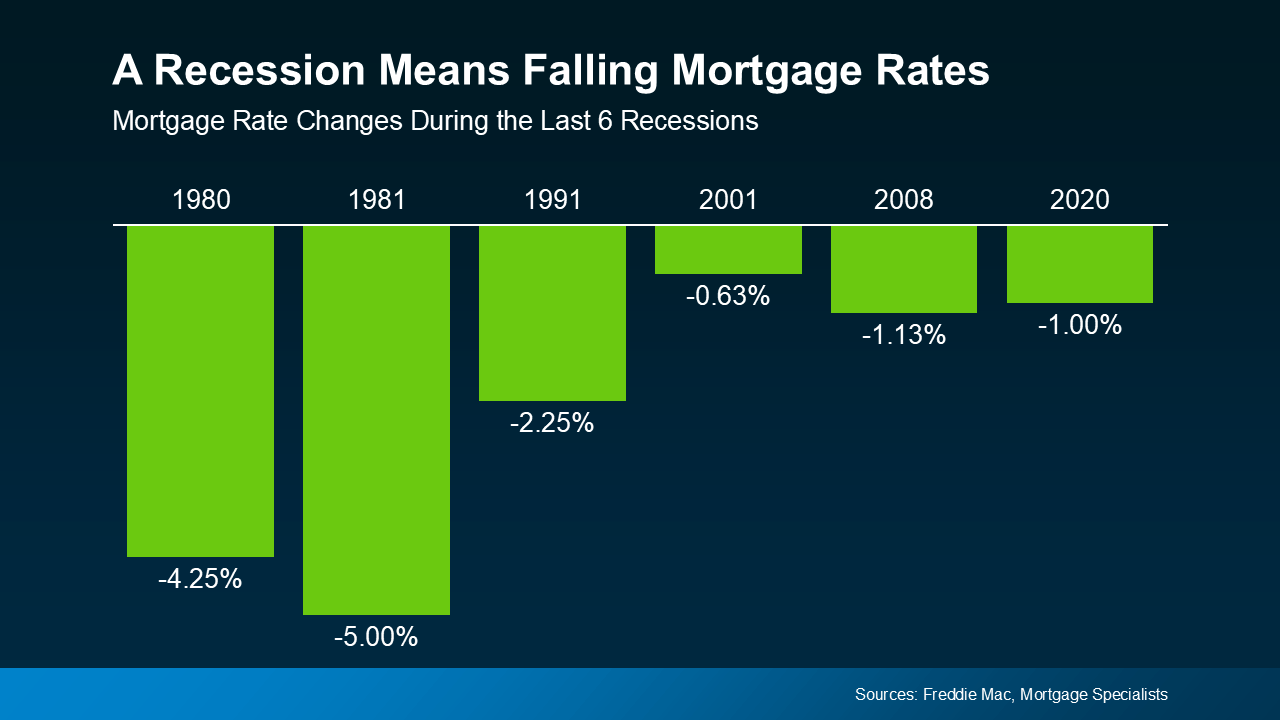

Mortgage Rates Typically Decline During Recessions

Home prices may stay their path during economic slowdowns, but mortgage rates actually tend to drop. Looking again at historical data from the last six recessions, this time from Freddie Mac, mortgage rates fell each time.

Historically speaking, a recession could mean that mortgage rates may even decline this year. However, the last time a recession dramatically lowered mortgage rates was over three decades ago in 1991. So with that said, even if a recession does happen, don’t expect a game-changing drop in mortgage rates.

Conclusion

Nobody ever truly knows what the economy will do, but the odds of a recession in 2025 have increased. Still, a recession doesn’t mean you need to worry about the housing market or the value of your home. The historical data tells us that a recession may even drive home prices higher and mortgage rates lower.

Wondering how an economic slowdown could impact your local market? Connect with us to get the info you need to plan ahead.

Should You Buy a Home This Spring or Wait for Lower Prices?

You’re probably familiar with the saying “The best time to plant a tree was yesterday, but the next best time is today.” It’s a valuable lesson about future planning and investment that, surprisingly, applies to the decision to buy a home too.

Even though buying a home is a major financial expense, it’s also a major investment that grows over time. As the price of your home increases over time, the value of the equity you’ve built grows with it. And while waiting for prices to drop may be an attractive option, trying to time the market rarely works.

But here’s something to consider: the longer you wait to buy a home, the more your patience could cost you. Let’s explain why.

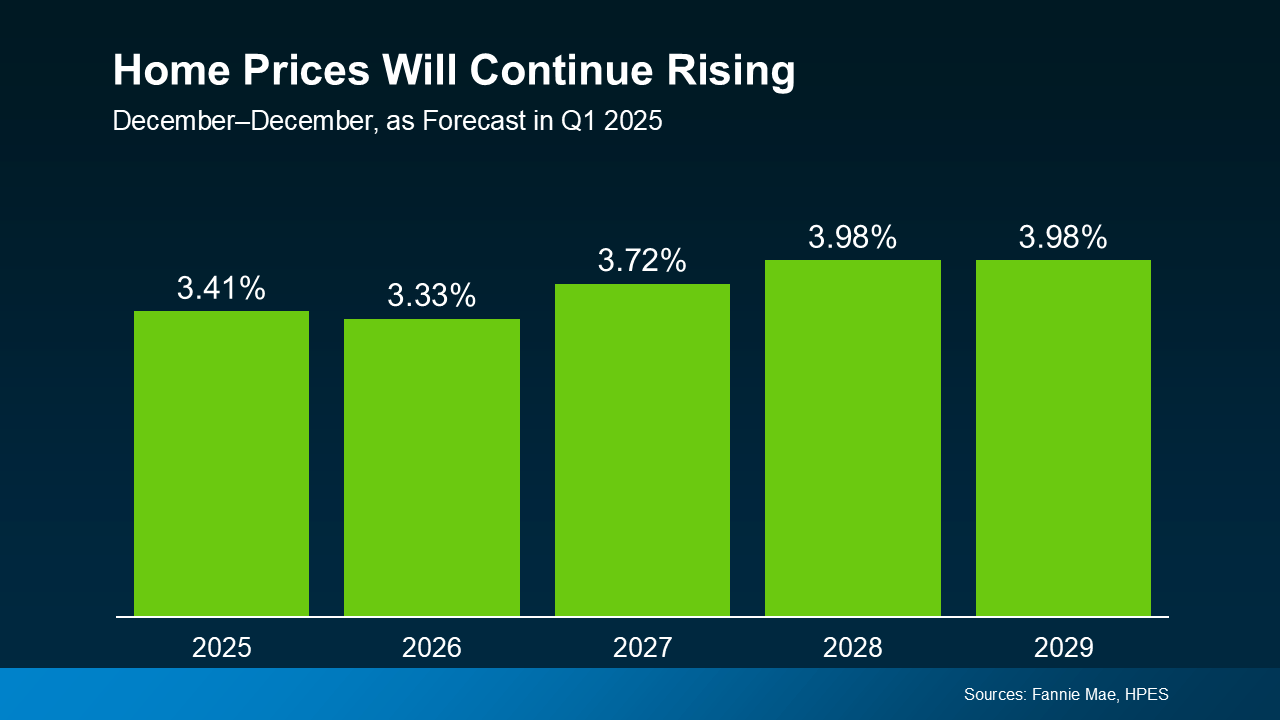

Home Prices Are Expected To Continue Climbing

Each quarter, over 100 housing market experts respond to Fannie Mae‘s Home Price Expectations Survey (HPES). Consistently, the survey results show experts agreeing that home prices will continue to rise through 2029 or even longer.

Sharp price increases may be behind us, but experts predict steadier, healthier increases of 3-4% per year moving forward. This rate of increase will vary by market from year to year, but it’s much closer to normal. Reliable growth is a promising sign for hopeful buyers, and the housing market at large, as the graph below demonstrates.

Even in markets experiencing slower price growth or short-term decreases, the steady gains of homeownership eventually win in time. After all, a growing, long-term financial investment will always beat a one-time discount.

Here are the main points to remember:

- Home prices will be higher next year. Experts don’t expect home prices to fall any time soon, at least at the national level.

- Waiting for a perfect mortgage rate or price drops is a gamble. With only slight dips in mortgage rates expected in the near future, price increase could outpace any potential mortgage savings. Unless home price growth is slow or mortgage rates are low in your area, waiting will likely be more expensive.

- Buying early means building more equity. When you invest in homeownership early, your equity and appreciating home value reward you in the long run.

The Costs of Waiting To Buy

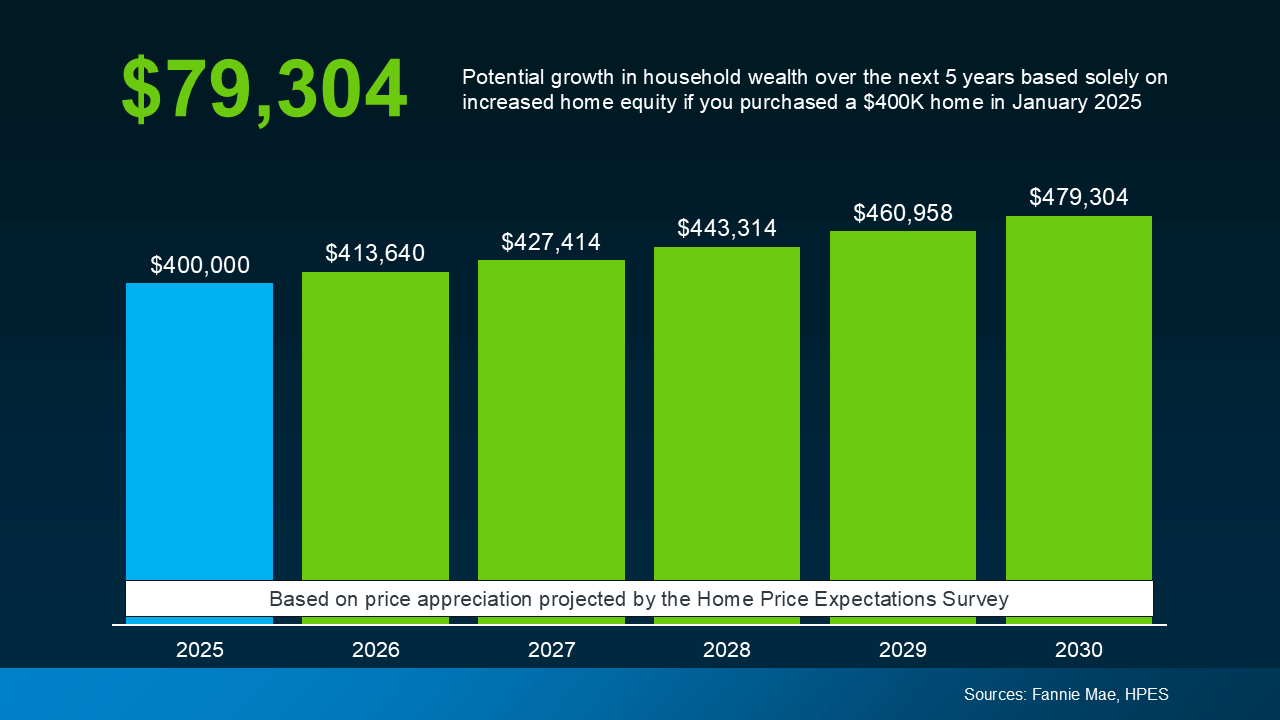

To demonstrate how these theories play out in real-world numbers, here’s a typical example. If you were to buy a $400,000 house in 2025, it could gain almost $80,000 in value by 2030. The graph below demonstrates how this value appreciates year by year based on the expert data we mentioned earlier.

This can be a considerable difference in your future wealth and why buyers who invest early are often glad they did. When it comes to building wealth through long-term investment, time in the market matters.

The question to consider isn’t “Should I wait to buy?” It’s really “Can I afford to buy now?” Just like planting a tree, making short-term sacrifices to buy a home will eventually pay off in the long-term.

Between rising prices and stubborn mortgage rates, today’s housing market is challenging, but achieving homeownership is far from impossible. Exploring different neighborhoods, seeking alternative financing options, or applying for down payment assistance programs can all make a critical difference.

What’s most important is acting decisively when you’re able to, instead of waiting for a perfect opportunity that never comes.

Conclusion

If you’re interested in buying but still undecided, take the time you need to make the right choice. But, remember that realizing an investment takes time, and the sooner you make one, the sooner you’ll be rewarded.

If you’re curious about what’s happening with prices in our local area, then reach out to us. Even if you’re not ready to buy, an expert local agent can fill you in with the info you need.

It’s Tax Day – Here’s How a Refund Can Help You Save For a Home

If you’ve been planning to buy a house, you know how hard it can be to save for a home. What you might not know is that your tax return can be a helpful boost to your savings and budget. According to a recent post by Freddie Mac:

“ . . . your tax refund from the IRS can be a useful supplement to your homebuying budget.”

So if you’re planning to get a tax refund this year, consider the difference that extra funding can make. A refund can help you pay for the upfront costs of homebuying, like a down payment or closing costs. And, according to the IRS, your tax refund may even help you out this year more than ever.

How a Tax Return Can Help You Buy a Home in 2025

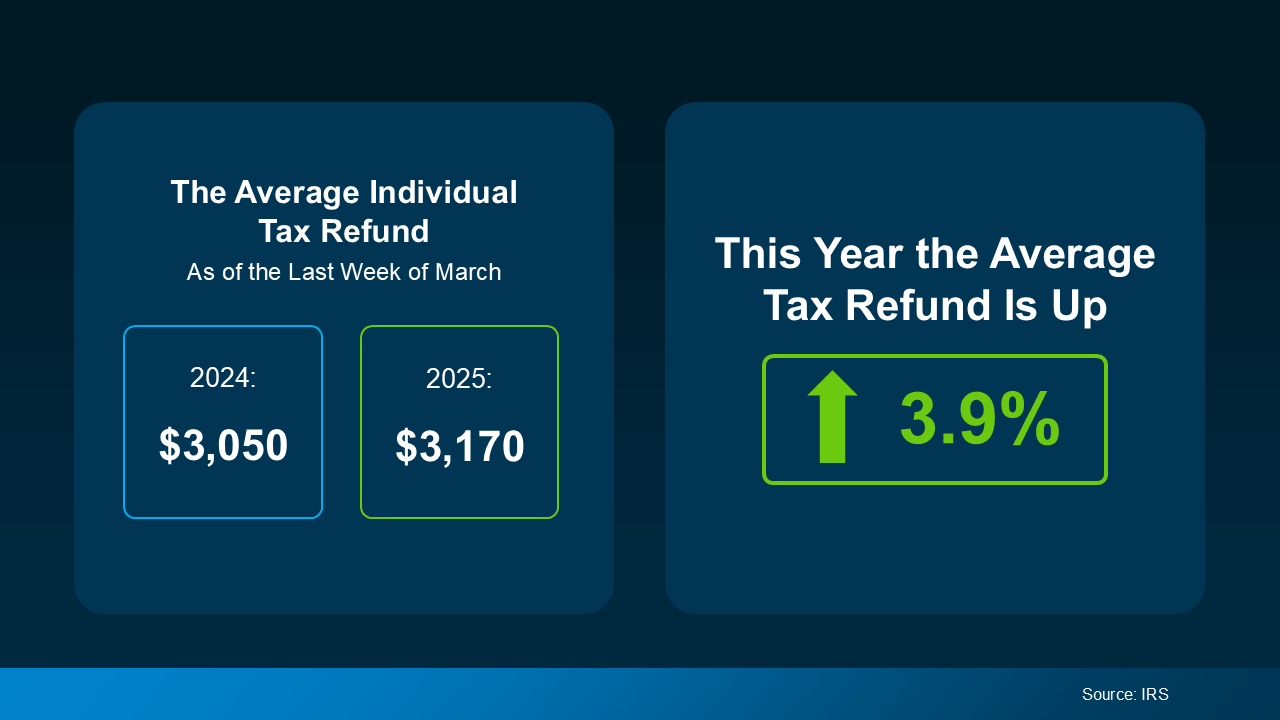

Recent data from the Internal Revenue Service (IRS) has found that the average individual’s refund is 3.9% higher this year. And while that’s not a huge increase, it can make a big difference if you’ve been struggling to save. The graphic below visualizes the new IRS data, comparing the average tax return in March 2024 to March 2025.

Your own personal tax refund will likely vary, but any financial boost helps when you’re saving for a home. According to Freddie Mac, the following are several ways you can put your tax return to good use when homebuying:

- Saving for a down payment – A down payment on a home is often one of the biggest obstacles to homeownership that buyers face. Saving your tax refund for a down payment can be a smart way to make this major step easier. Keep in mind while a 20% down payment may be common, it’s not typically a hard requirement to buy.

- Paying for closing costs – Usually due at closing, closing costs include fees for services like the appraisal, title insurance, and underwriting of your loan. While these vary by state, they’re often between 2% and 6% of your home’s total final purchase price. As a much lower percentage of your home’s price, closing costs can be a great use of your yearly refund..

- Lowering your mortgage rate – Lenders sometimes give buyers the option to buy down their mortgage rate if they qualify. This allows buyers to pay an upfront fee to lower their initial mortgage rate, reducing monthly payments in the short-term. This option can be particularly helpful if interest rates and mortgage payments are a major homebuying hurdle you’re facing..

Financially speaking, this may be more complicated in practice, but there’s no need to do it all on your own. Working with an experienced, trustworthy real estate professional can simplify your financial planning, helping you reach the best decision possible. An agent who understands the homebuying process, your unique financial needs, and your personal goals can make all the difference.

Conclusion

If you’ve been saving for a home, you already know well that every penny counts. Your tax return probably won’t be the final financial boost you need, but there are ways to use it effectively. Planning and identifying how to best spend that money can give you a real, meaningful step toward buying your home.

Are you eager to buy a home but having trouble making things work? Contact us today. We can connect you with local lenders and agents to help make your dream of homeownership a reality.

What’s Your Real Home Value in the 2025 Market?

If you’ve checked home prices in the past few years, you know too well that they’re always rising. But if you’re a current homeowner, have you considered what this might mean for your own home value? It may be that your home is worth far more than you think in 2025.

While rising prices are expected, the home value increases of the post-Pandemic housing market have been dramatic. And if you’re a seller waiting to list, this could mean a huge payoff when you finally close. If you’re eager to know much your own house could sell for, finding out is easier than you think.

The Post-Pandemic Home Value Launch

Home prices typically rise around 2-5% per year, but in 2021-2022 that number rose to double-digit levels. In the spring of 2022, year-over-year percentage growth finally peaked at over 20% nationally. The sheer number of buyers in the market during this time sent home prices soaring as housing supply lagged. And though price growth has settled since then, the home value accrued by homeowners in that time remains.

The lingering effects of that volatile period have caused difficulties for buyers, but they’ve also produced great opportunities for sellers. There’s a good chance your house has gained tremendous value since then, and that means more wealth for you.

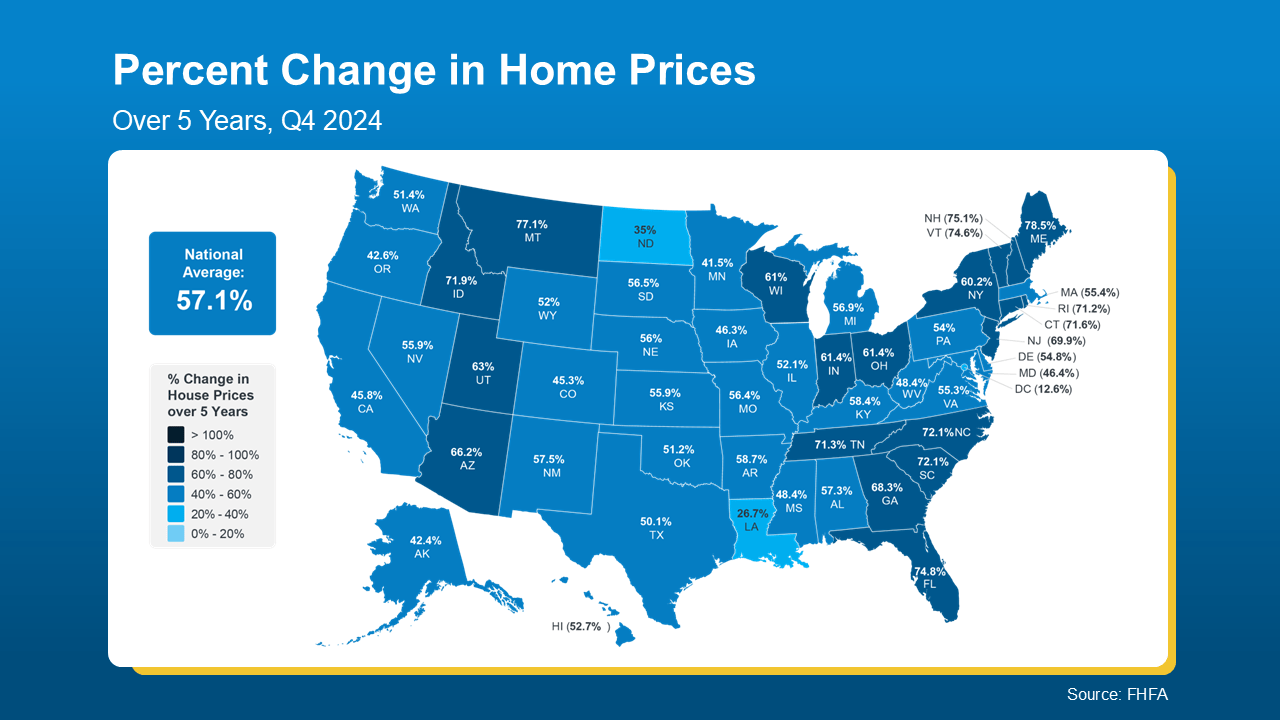

The map below references data from the Federal Housing Finance Agency (FHFA) to illustrate that home prices have risen by nearly 60% in just the past 5 years alone nationally. The most extreme increases have taken place in states marked with a darker blue, like Maine, New Hampshire, and Florida.

If worries about today’s rates and prices have stopped you from selling your home, let these numbers reassure you. Your home’s risen value may be exactly what you need to close the affordability gap and purchase your next house.

Even better, if you’ve owned your home for 10 years or more, your value is likely even higher. You can stack the incredible gains of the past five years on top of five years of healthy appreciation too. And an agent can help you figure out what that really looks like.

How To Find Out What Your House Is Really Worth

Percentages will help you ballpark an estimate, but you need specific numbers to make real, actionable decisions. To help, you can get a free home valuation estimate from us right now using the tool below. You can even sign up for a full valuation report.

Home valuations can be great tools, but only a local real estate agent can give you the best, most accurate look at your house’s real market value. An agent will know the state of your local housing market and the factors driving it. They can provide insights about current housing inventory, pricing of comparable homes, and unique contributors to value like renovations.

By knowing what’s happening where you live, an agent can stack their market knowledge against the unique condition and features of your home and give you an accurate estimate of your home’s current value in your area.

Conclusion

Home values have taken off in just the past few years, and that’s great news for current homeowners. Knowing what your house is worth in today’s real estate market will help you plan your next move. A local agent can give you a great idea of how much your home might realistically sell for.

If you’re a homeowner considering a move, get your free home valuation from us at Century 21 Affiliated now. Ready to sell? Reach out now and we’ll connect you with a local expert real estate agent who can get your house sold.

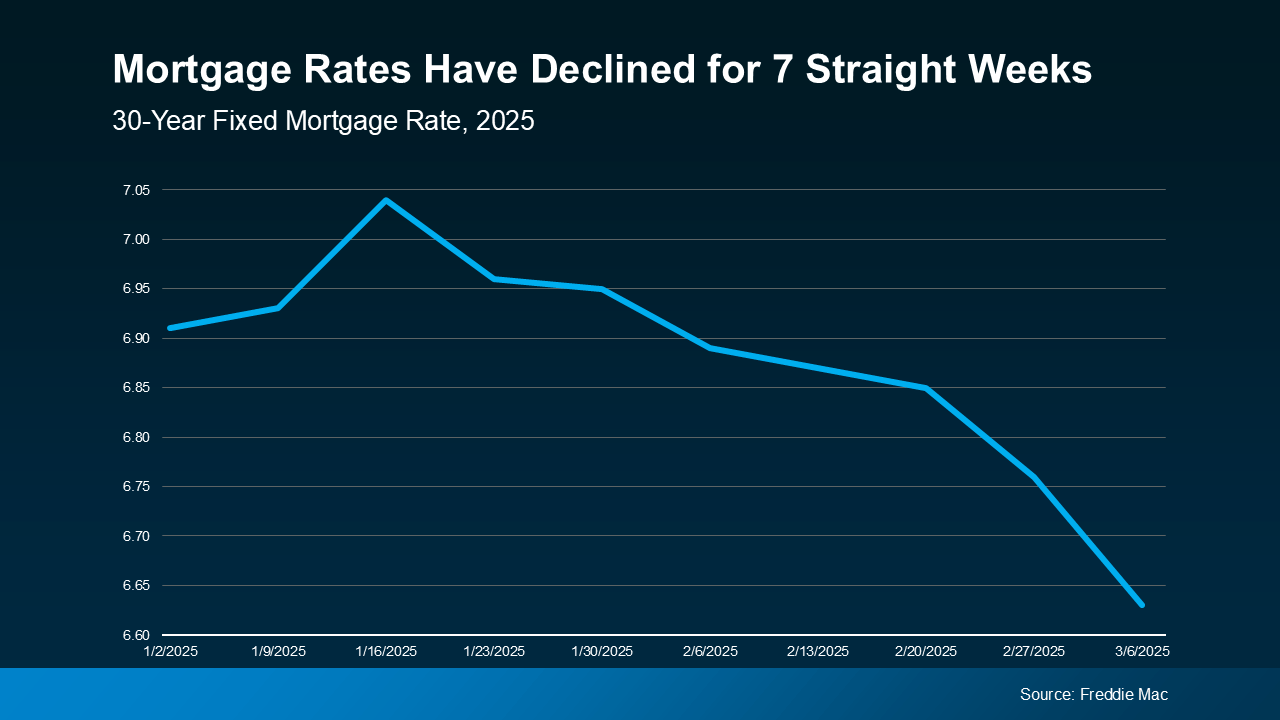

Mortgage Rates Drop to the Lowest Point in 2025 So Far

If you’ve been holding off on buying a home for a lower mortgage rate, take another look at the market. Mortgage rates are trending downward, and they just hit their lowest point of the year so far.

According to a report from Freddie Mac, mortgage rates have been falling for seven straight weeks. The average weekly rate for a 30-year-fixed mortgage is now at the lowest level its been in 2025.

This may not sound significant on its own, but it outlines a remarkable trend. A drop in rates from over 7% to the mid-6’s can make all the difference when buying a home. What’s most significant is that experts previously predicted that rates wouldn’t fall this low until Q3 of this year.

Why Are Mortgage Rates Dropping?

According to Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), ongoing economic uncertainty is a driving force in pushing rates lower:

“Mortgage rates declined last week on souring consumer sentiment regarding the economy and increasing uncertainty over the impact of new tariffs levied on imported goods into the U.S. Those factors resulted in the largest weekly decline in the 30-year fixed rate since November 2024.”

The timing of this rate drop is great for buyers moving into the Spring 2025 market. But remember that mortgage rates can change quickly, and always expect some volatility in markets driven by uncertainty. With that said, this small window of rates dropping into prime buying season might be exactly wait you’ve waited for.

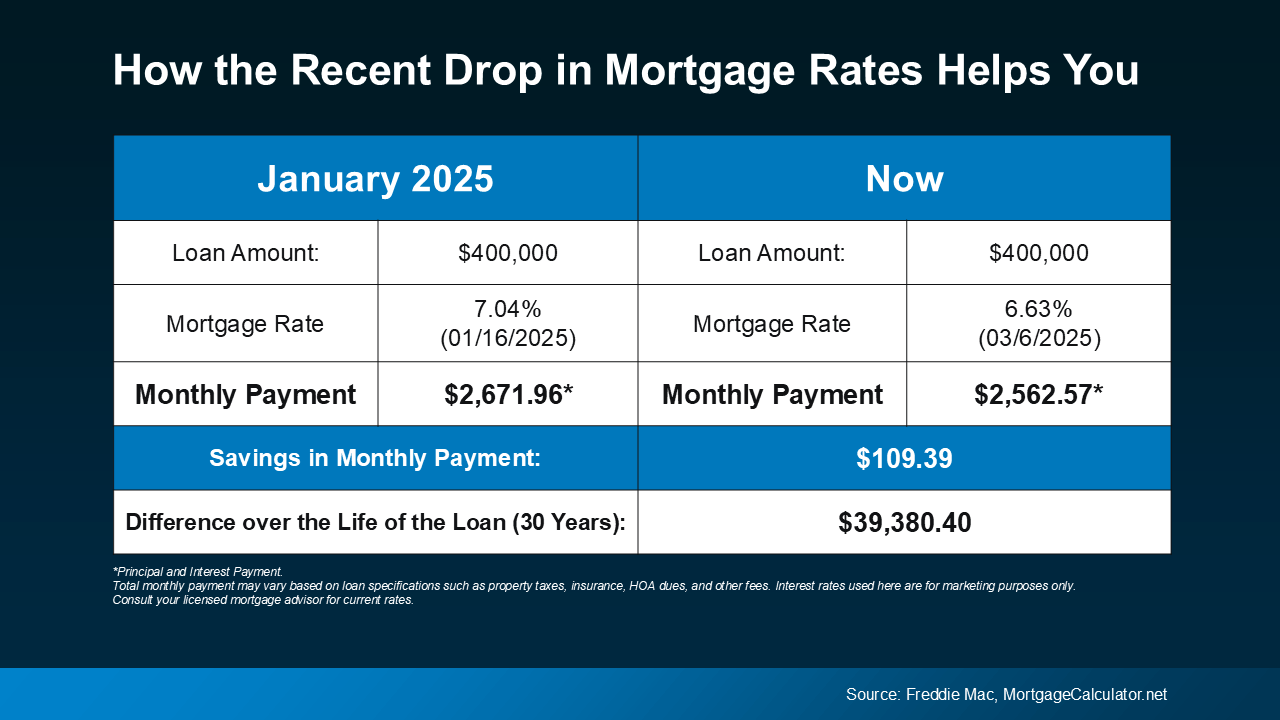

What Falling Mortgage Rates Mean for Your Buying Power

Even a small reduction in your mortgage rate can make a huge difference in your monthly housing payment. The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house when rates were 7.04% back in mid-January (this year’s mortgage rate high). The right side shows what it could look like if you buy a home now at current rates.

In just the past few weeks, the expected payment on a $400K loan has come down by over $100 per month. That’s a significant savings that can make a world of difference when deciding to buy a house.

Recent economic shifts have driven rates down faster than expected, and that’s great news. But remember that this could change at any time in the coming days and months for better or worse. So if you’re waiting for rates to fall further before you buy, think hard about the current window of opportunity before making a decision.

Conclusion

Mortgage rates have dipped to their lowest point in 2025 so far. This grants buyers a great position moving into the spring buying season, especially for those who have been waiting. The unpredictability of the market and larger economy mean volatility, so get expert advice and consider before making a decision.

Can You Buy a Home in 2025 Without Waiting for Lower Rates?

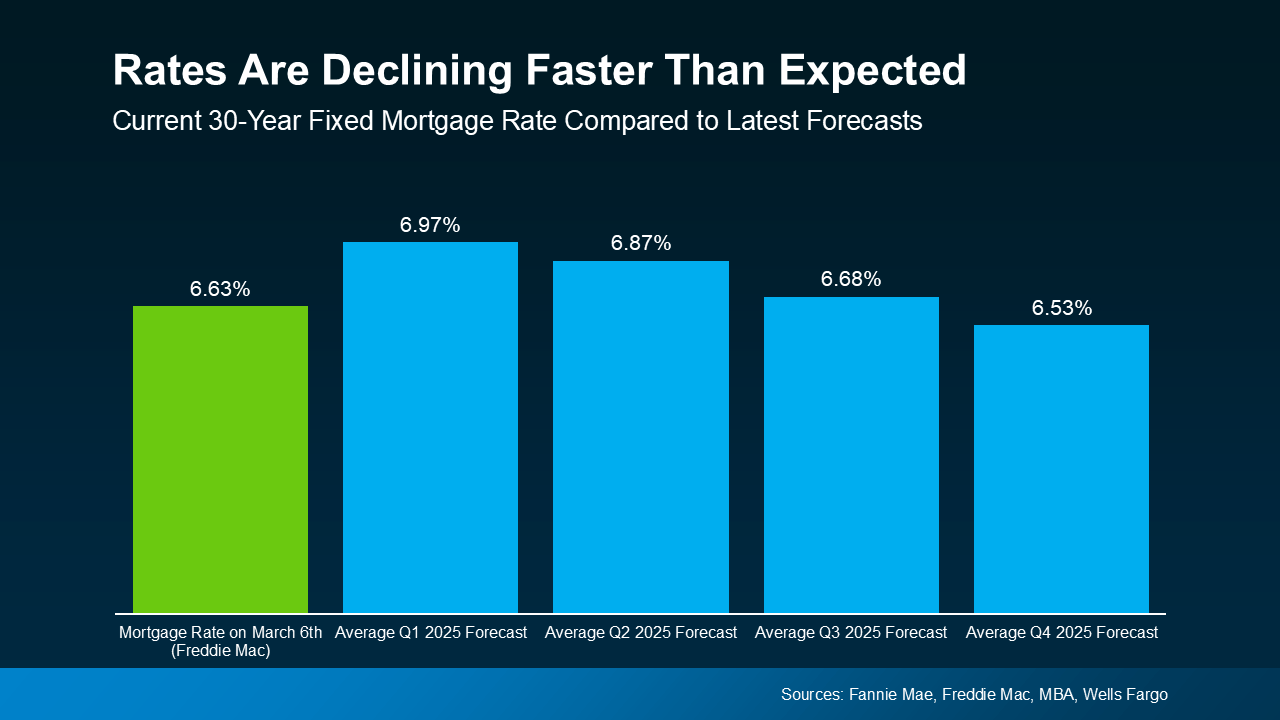

Like many homebuyers, you may be waiting for rates to drop before you finally buy a home this year. The latest expert reports predict that rates will continue to fall, but not as low as many hope. While this may be discouraging, the good news is that there are still ways you can buy a home in 2025 without waiting for lower rates.

Will Rates Keep Dropping?

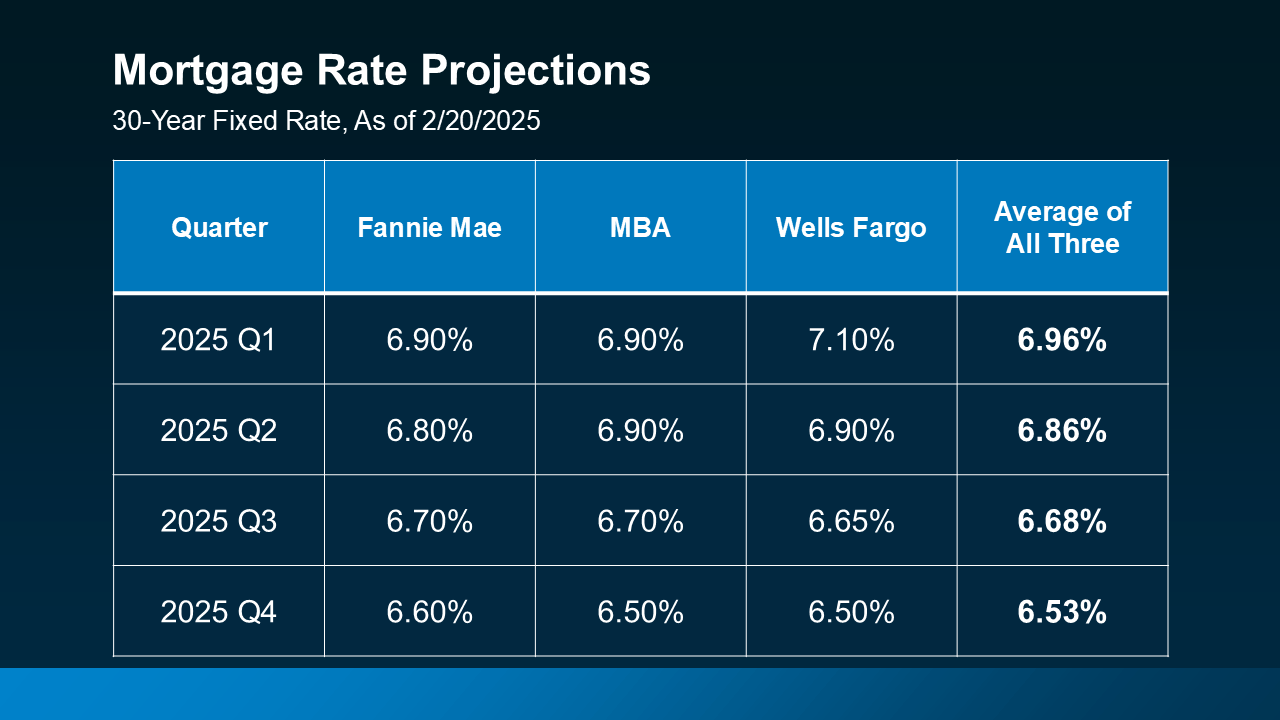

Near the end of 2024, experts were predicting that mortgage rates could dip below 6% by the end of 2025. More recent projections are suggesting that rates will continue to fall but hover somewhere above 6%.

Recent projections from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo now predict that mortgage rates will stabilize around 6.5% by the end of the year.

If you’re holding out for mortgage rates to drop below 6% before buying, you may need to keep waiting into next year at least. But what if you’re a buyer who can’t wait to move because of a major life event, like a new job, a new baby, or a marriage? Don’t panic—you’ll still be able to move this year, but you may need to take advantage of some alternative financing options.

How to Finance a Home in Today’s Market

With rates predicted to hold more stubbornly than expected this year, it’s worth researching different financing options, especially if your move is a non-negotiable one. Here are three unique financing strategies that may be helpful to you depending on your situation. If you’ve already chosen a lender, discuss each of these options with them to decide if any are a good fit. It may make all the difference you need to buy a house in 2025.

1. Mortgage Buydowns

A mortgage buydown allows you to pay an upfront fee—sometimes called “discount points”— to lower your mortgage rate temporarily or sometimes permanently. This can be an especially helpful option if you want or need a lower monthly mortgage payment early on. Of course, the obvious downside is a higher upfront cost.

A recent survey by HomeLight found that 27% of real estate agents day first-time homebuyers are increasingly requesting mortgage buydowns from sellers. This is a new program called RateReduce Sell that allows sellers to pay an upfront cost to lock in a lower mortgage rate for buyers. However, a real estate agent can help negotiate this with a seller, so be sure to mention it if you’re actively looking to buy a house.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) are loans that combine a fixed-rate period with an adjustable-rate period. ARMs typically start with a lower rate than a traditional 30-year fixed mortgage then fluctuate with the market once the fixed-rate period ends. This can make them an attractive option if you expect rates to drop in the future, or plan to refinance your home later.

If you remember the 2008 housing crash, it may be reassuring to know that today’s ARMs aren’t like the volatile loans from back then. Lance Lambert, Co-Founder of ResiClub, describes modern ARMs this way:

“. . . ARM products today are different from many of the products issued in the mid-2000s. Before 2008, lenders often approved ARMs based on borrowers ability to pay the initial lower interest rates. And sometimes they didn’t even check that (remember Ninja loans). Today, adjustable-rate borrowers qualify based on their ability to cover a higher monthly payment, not just the initial lower payment.”

Before 2008, banks used to give loans without checking to see if buyers could realistically afford them. These days, lenders verify income, assets, and employment, reducing the risks previously associated with loans like ARMs.

3. Assumable Mortgages

An assumable mortgage allows you to take over a seller’s existing loan, usually including its lower mortgage rate, repayment period, and remaining balance. This can be a great option if the seller was locked into a low mortgage rate, but few are willing to offer it by default. According to U.S. News, more than 11 million homes qualify for an assumable mortgage, so it’s always worth bringing up with your agent or seller.

Conclusion

With mortgage rates looking unlikely to fall below 6% in this year, waiting for a drop may not work out if you’re eager to buy a house in 2025. Consider options like mortgage buydowns, ARMs, or assumable mortgages depending on what makes the most sense for you. Connect with a local lender or expert agent today to explore your options and get the help you need.

3 Questions About Selling Your House You May Be Asking

Selling a house is one of the most significant financial and emotional decisions a homeowner can make, and unanswered questions about the market make this decision even harder. Sometimes, sellers’ concerns are based on misconceptions or outdated info, but can be quickly alleviated with a trustworthy agent’s help.

If your own uncertainty about the market is keeping you from selling your house, don’t wait to get the answers you need. Despite rising home prices and stiff demand, the 2025 real estate market is active, and recent reports prove it. If you’re uncertain about selling your house, here are the answers to three you may be asking.

1. Is It a Good Idea To Move Right Now?

If you’re a homeowner itching to make a move, you might be waiting to sell because you don’t to take on a higher mortgage rate on your next house. Between interest rates, inflation, and the job market, it’s both wise and responsible to consider your own finances and the greater state of the economy. The good news is that moving may be a lot more feasible than you think, mainly thanks to how much your house has likely grown in value.

Consider if there’s anyone in your neighborhood who sold their house recently. If so, do you know what it sold for? Considering how much home values have increased since 2021, the final closing price may surprise you. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), the typical homeowner has gained almost $150,000 in housing wealth in the last five years alone.

That’s a significant gain depending on your house’s initial value when you bought. When you decide to sell, the increased value of your home along with the equity you’ve built can make all the difference you need to lock down your new home.

2. Will I Be Able To Find a Home I Like?

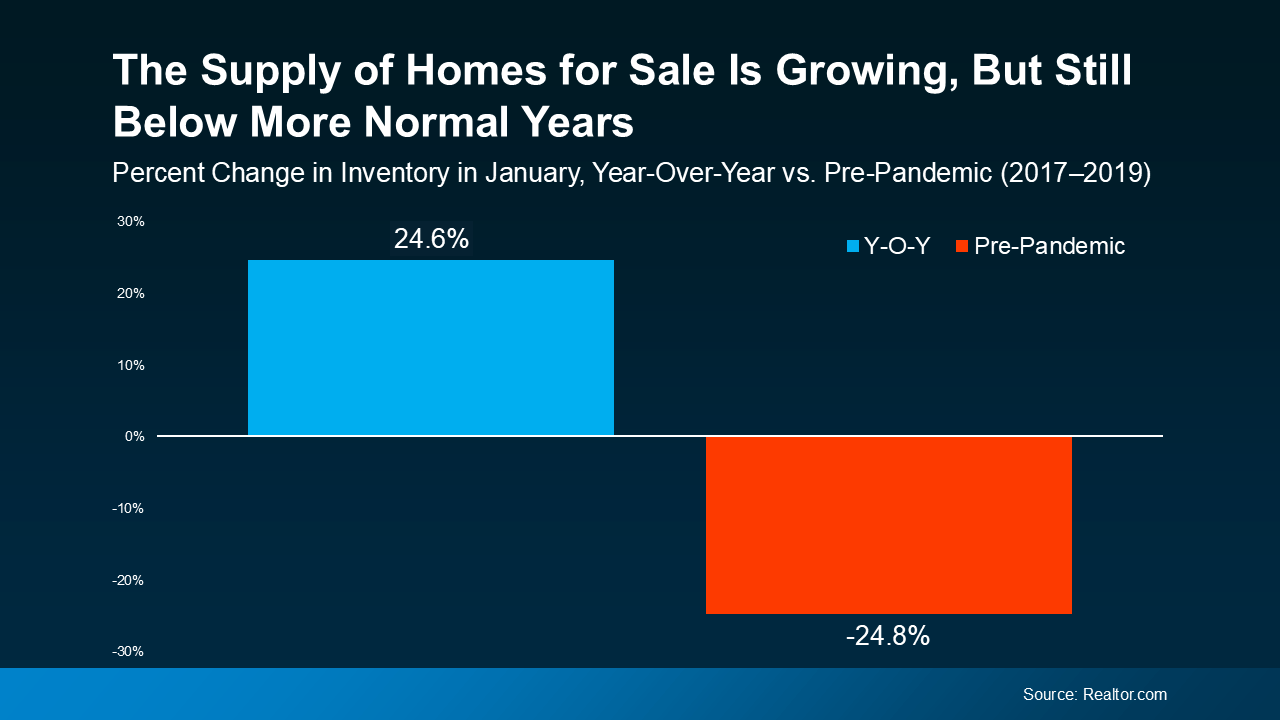

If finding the right house is stopping you from selling your house, it’s probably because you remember how hard it’s been to find a home these past few years due to low housing inventory. But thanks to positive inventory trends in today’s market, finding a good home is becoming easier.

According to a January 2025 report from from Realtor.com, home supply has increased nearly 25% since this time last year.

Housing inventory still hasn’t risen to pre-pandemic levels, but it’s improved significantly in the past year since January 2024. Even better, real estate experts say the supply of homes will continue to grow another 10 to 15% in 2025. More houses on the market means more options for you as a buyer, and a better chance of finding the perfect home.

3. Will My House Sell?

Lastly, if you’re worried that buyers aren’t buying thanks to home prices and mortgage rates, here’s some encouraging info. While last year’s home sales were still below normal, about 4.24 million homes sold according to data from the National Association of Realtors (NAR). Experts expect that number to rise in 2025, but here’s how 2024’s break down over time:

- 4.24 million homes ÷ 365 days in a year = 11,616 homes sold each day.

- 11,616 homes ÷ 24 hours in a day = 484 homes sold per hour.

- 484 homes ÷ 60 minutes = 8 homes sold every minute.

To apply some perspective: in the minute it took you to read this paragraph, 8 homes sold last year. And homes are expected to sell even faster in 2025, so rest assured that buyers are still buying. The market may not be back to pre-pandemic levels, but there are thousands of active buyers looking for homes like yours.

Conclusion

Selling your house is a major decision just like buying, but there are plenty of reasons for optimism in 2025. Home inventory is increasing, buyers are becoming more active, and your current home is likely worth more than you think.

Are you thinking of selling but have unanswered questions holding you back? Reach out today and we’ll connect you with an expert local real estate agent who can help.

Top 10 Best Real Estate Markets for First-Time Buyers in 2025

If you’re like many aspiring homebuyers, the rising cost of living might feel like a major roadblock. From groceries to gas, and yes, especially home prices, everything seems to be getting more expensive.

But even in today’s market, there are still ways to make your homeownership dreams a reality. The key is knowing the current best real estate markets and how to approach your first home purchase strategically.

Think of Your First Home as a Stepping Stone

One of the biggest misconceptions among buyers is that their first home has to be their dream home. The truth is, your very first home doesn’t need to check every box on your wish list. Instead, think of your first home as a stepping stone to your final destination.

Owning a home allows you to start building equity, which grows over time as home prices increase. That equity can be a powerful tool when you’re ready to upgrade to a bigger home or move to a more desirable location in the future.

Rather than waiting until you can afford your dream home in your ideal neighborhood, consider starting with something that fits your current needs and budget. This approach gets you into the market sooner and may cost you in the short-term, but it sets you up for long-term financial growth. Best of all, it’s a real start to eventually buying your dream home at some point in the future.

Explore the Best Real Estate Markets in 2025

If the price of homes in your preferred area are holding you back, it might be worth broadening your search. With some flexibility in location, you can find more affordable options without sacrificing the amenities most important to you. Many first-time buyers find homebuying success by exploring surrounding areas or even considering a move to a different state.

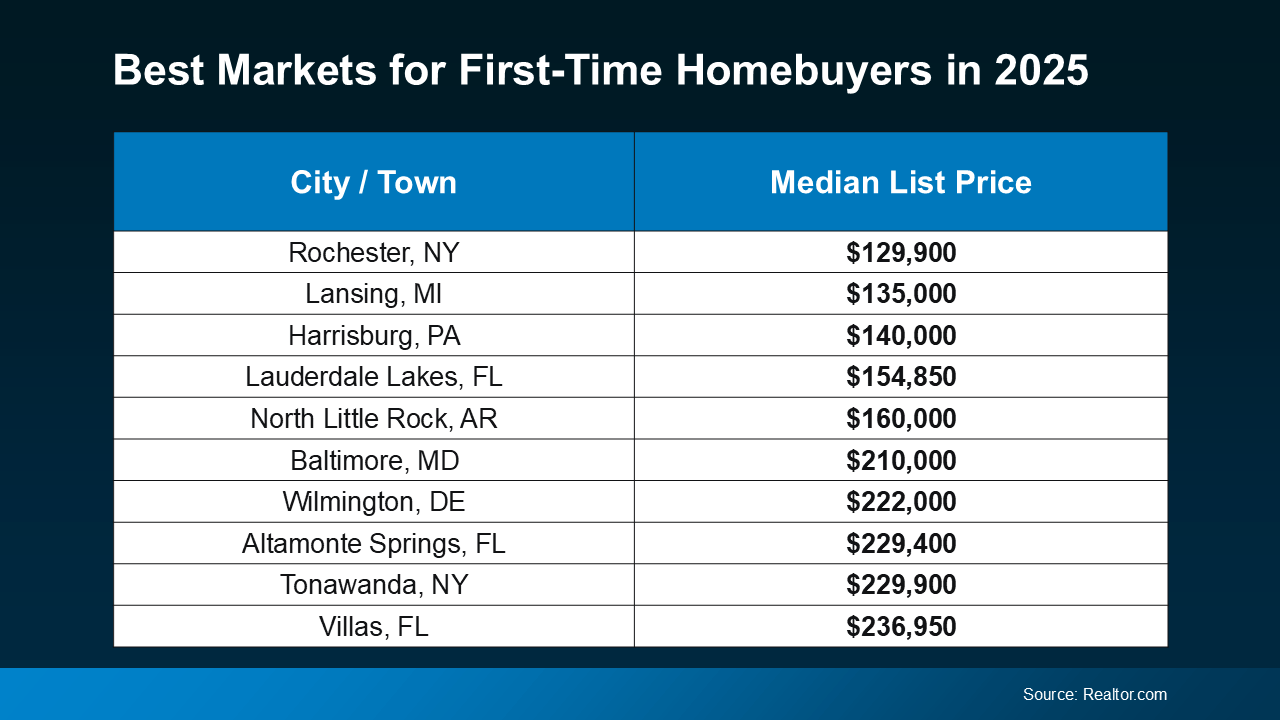

According to a report from Realtor.com, these are the 10 best real estate markets for first-time homebuyers in 2025:

- Rochester, NY with a Median List Price of $129,900.

- Lansing, MI with a Median List Price of $135,000.

- Harrisburg, PA with a Median List Price of $140,000.

- Lauderdale Lakes, FL with a Median List Price of $154,850.

- North Little Rock, AR with a Median List Price of $160,000.

- Baltimore, MD with a Median List Price of $210,000.

- Wilmington, DE with a Median List Price of $222,000.

- Altamonte Springs, FL with a Median List Price of $229,400.

- Tonawanda, NY with a Median List Price of $229,000.

- Villas, FL with a Median List Price of $236.950.

Realtor weighted their market rankings by several factors including median price, location score, number of home listings, average commute time, and others specified in the full report. If one of these cities is in or near your target home location, it’s worth looking to see what properties are available. Even if you don’t find your dream home, you might find the perfect starter home on the path to it.

Stay Local and Look Just Outside Your Preferred Area

If moving to a different state isn’t an option, you can still find affordable homes by expanding your search locally. Sometimes, looking even just 10 to 20 minutes outside your ideal neighborhood can make a significant difference in price. Nearby areas can often offer similar amenities, like access to restaurants, shops, and activities, but at a lower cost.

And the best way to see what’s available is to work with a real estate agent who understands the local market and can help you identify hidden gems nearby. An agent can point you to communities you may not have considered that have lower price tags now and are steadily gaining value and appeal. That way you can buy your first home and be set up to gain equity through the years.

Conclusion

Today’s cost of living is a challenge for many homebuyers, but by exploring 2025’s best real estate markets and working with a knowledgeable agent, you can take that first step toward owning a home this year, and building equity for your future.

How far outside your area would you be willing to look to make your homeownership dreams a reality? Connect with us to discuss your options and find the perfect market for your first home.

Home Price Growth Is Slowing in 2025 – What Does That Mean for You?

Over the past few years, home prices have skyrocketed as demand has increased and supply has stiffened. It’s been a frustrating market for buyers, leaving many to doubt their chances of ever owning their own home. But the early weeks of 2025 have brought welcome news: the pace of home price growth is finally slowing down, and that’s a positive shift for anyone looking to buy a home.

Home Price Growth Drops to a Healthy Pace

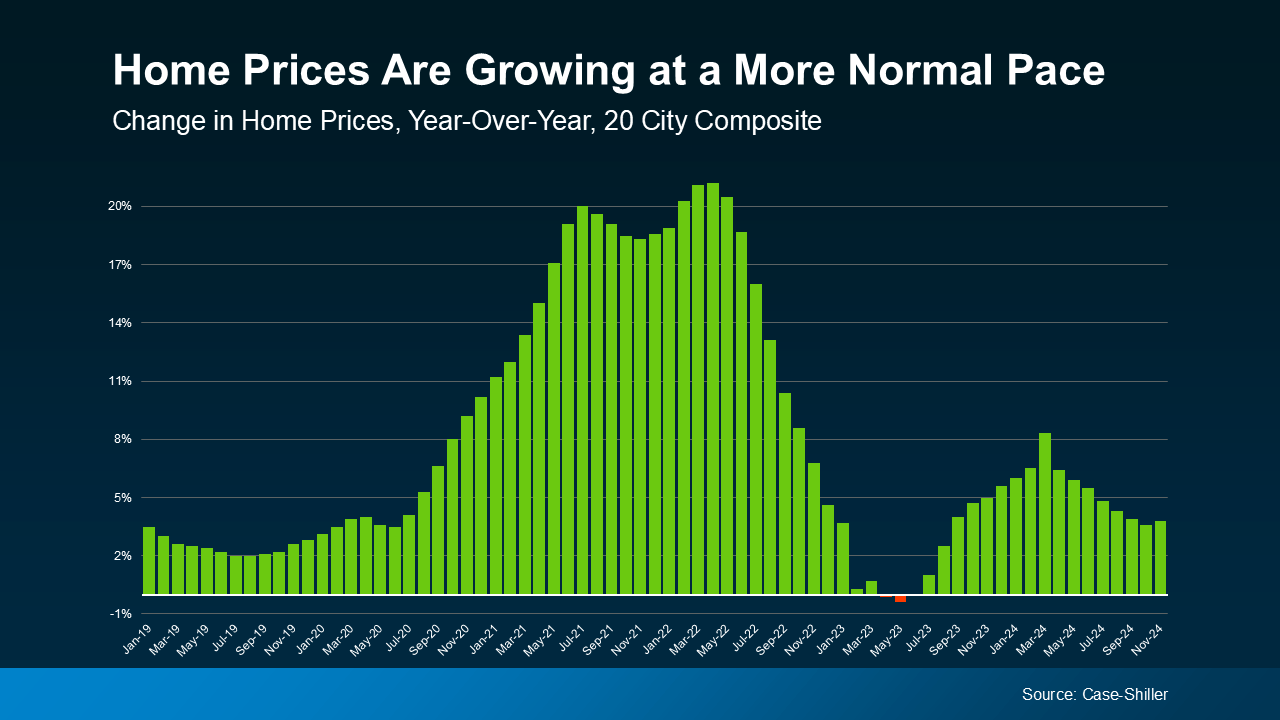

At the national level, home prices are still rising, but at a much more normal, manageable rate compared to the double-digit spikes we saw in 2021 and 2022. Recent data from Case-Shiller show that in November 2024, the year-over-year increase in home prices was just 3.8% nationally, a clear drop from Pandemic rates:

What does this mean for you? For one thing, you’re less likely to experience the sticker shock that was common just a few years ago. The days of rapid price jumps that made it difficult to plan or pursue your purchase are behind us, and projected drops in mortgage rates this year paint an even more positive picture. More stable price growth also means that the home you buy today is still likely to appreciate in value over time, helping you build equity and secure your financial future.

Real Estate Is Local: Prices Vary by Market

While the national trend is pointing to more moderate price growth, keep in mind that all real estate is local. Some markets are still experiencing strong demand and upward price pressures, while others are cooling off or even seeing declines. For example, smaller, more affordable metro areas are still seeing significant demand and price increases. As CoreLogic Chief Economist Selma Hepp explains:

“Regionally, variations persist, as some affordable areas – including smaller metros in the Midwest — remain in high demand and continue to see upward home price pressures.”

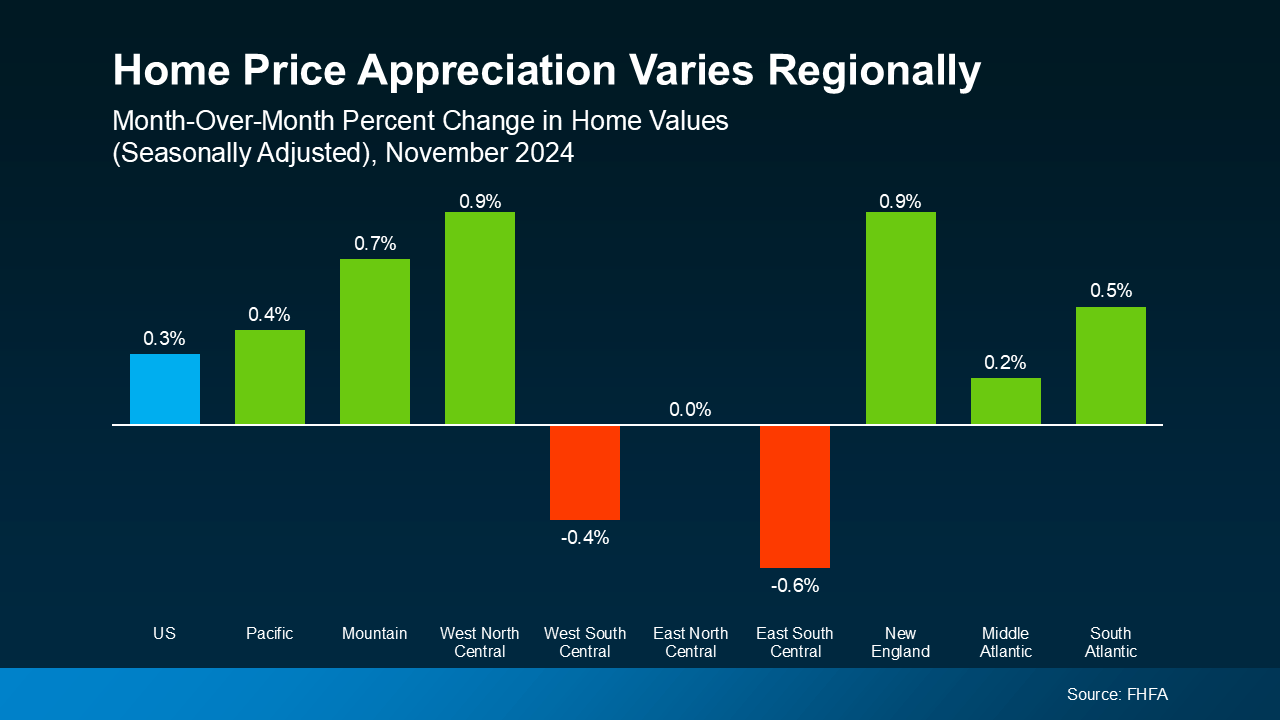

Meanwhile, other regions, particularly those in southern markets, experienced slight month-over-month declines in November, according to Federal Housing Finance Agency (FHFA) data:

Differences like these highlight the importance of understanding what’s happening in your specific market. National averages can provide a general idea, but they rarely give you the whole picture. That’s where the knowledge and expertise of a local real estate agent can really help. They can help you understand local trends, identify opportunities, and create a buying strategy tailored to your needs and budget. Whether you’re buying in a high-demand market or one that’s cooling off, having a local expert on your side ensures you’re making more informed and confident decisions.

Conclusion

Home prices in early 2025 are growing at a more manageable pace, giving you the opportunity to plan your purchase without fearing the rapid price hikes of recent years. Connecting with a local real estate agent can help you navigate your area’s local home market, and make the best decision possible.

If you’re thinking about buying a home, 2025 is shaping up to be a great time to explore your options. Reach out to us today to connect with a local expert who can help you buy with confidence and find the perfect home for you.