Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mid-Year Housing Market Update 2026

If you’re feeling confused by the housing market right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up as quickly as many experts expected. And buyers and sellers are still waiting for affordability to improve and market activity to turn up.

The short answer? A lot changed during the first half of 2026.

At the end of 2025, economists were forecasting a stronger housing market for the year ahead. Many expected mortgage rates to come down, affordability to improve more noticeably, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. With rates staying elevated for longer, many buyers have continued to wait on the sidelines.

Unexpected factors like these have forced experts to revise their housing forecasts for the rest of the year.

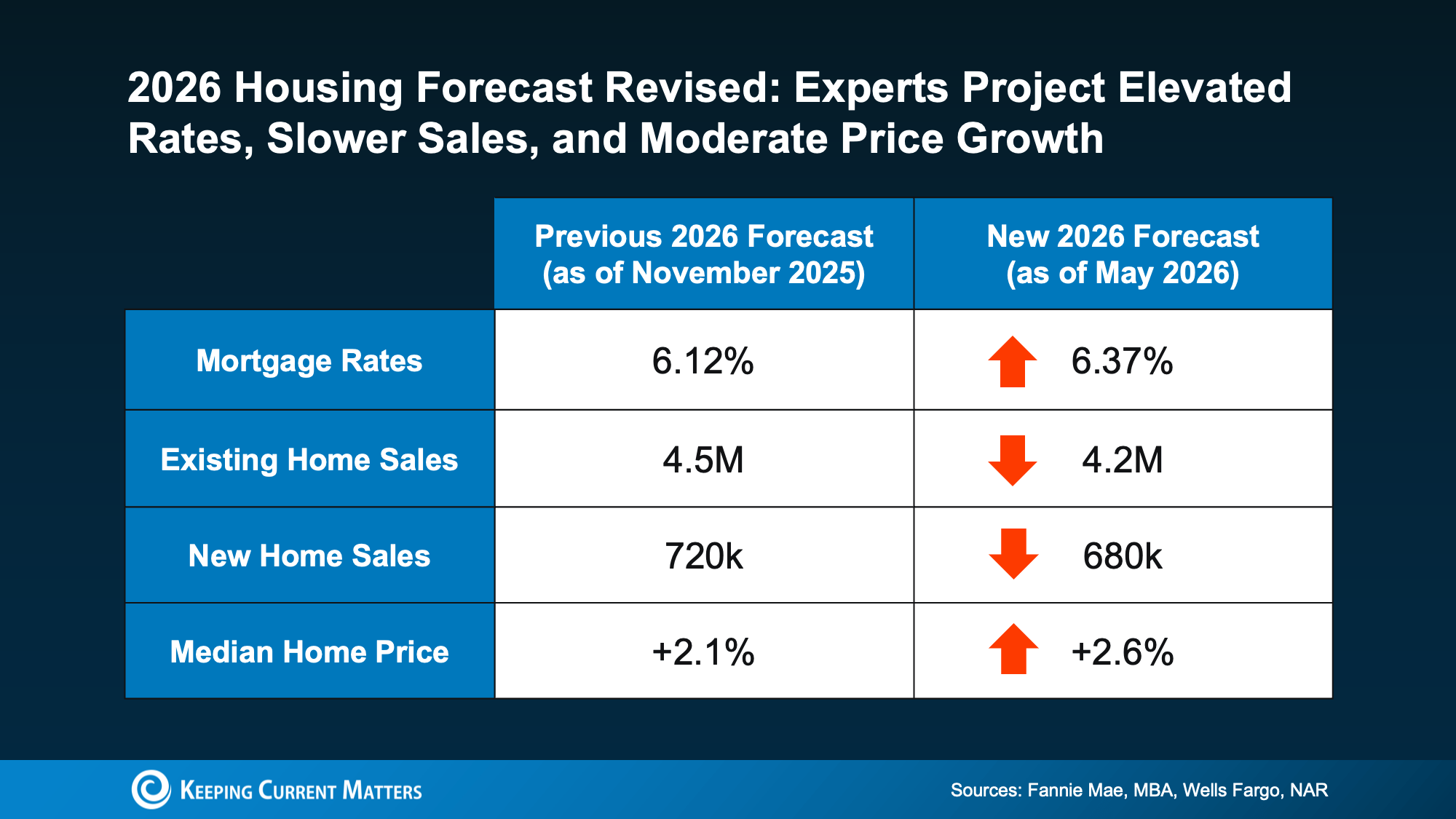

Experts are now projecting elevated mortgage rates (6.37%) and a dip in total home sales. However, home values remain resilient with a projected 2.6% growth in median prices.

So, what does this mid-year housing market update actually mean for you? Let’s break it down.

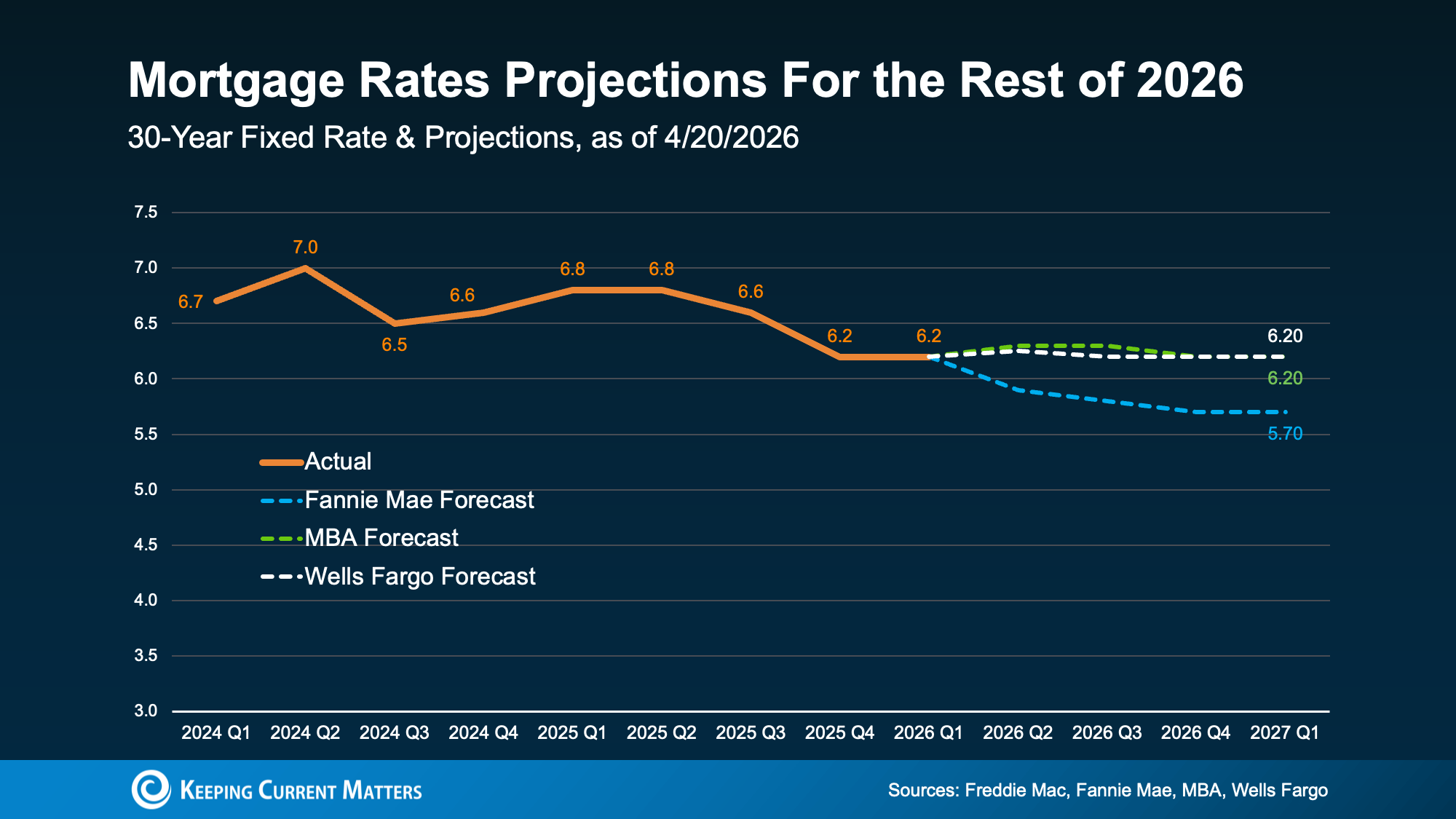

Mortgage Rates May Stay Elevated Longer Than Expected

Just about everyone would like to see mortgage rates return to the upper 5s or low 6s we saw earlier in the year. But based on current forecasts, experts don’t expect that to happen this year.

Instead, many industry organizations now expect mortgage rates to stay closer to the mid-6% range in 2026. The good news is that this is still lower than rates were a year ago.

Of course, forecasts can change. If inflation cools or overseas conflicts ease, mortgage rates could shift again. But for buyers waiting for a major rate drop, the payoff may not be as big or as immediate as hoped.

For many buyers, the better question may be: Can you comfortably afford a home at today’s rate? If the answer is yes, waiting may not automatically put you in a stronger position.

Existing Home Sales Were Revised Lower

At the end of 2025, experts expected existing home sales to average around 4.5 million in 2026. That forecast has now been revised down to about 4.2 million.

That change tells us something important: affordability is still a challenge, and many buyers remain hesitant.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. As a result, the market has moved more slowly than originally expected.

But there is still some positive news. Even with the revised forecast, experts still expect more homes to sell this year than last year.

There’s also a pool of buyers who may re-enter the market once rates settle and uncertainty eases. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

Recent improvements in pending home sales also suggest some buyers are starting to move forward again, even with rates still elevated.

For today’s buyers, that’s a big deal. If you can afford a home now, buying before more buyers return could mean less competition than you might face later.

New Home Sales Also Slowed

Builders also expected a stronger year.

Earlier forecasts projected new home sales would top 700,000 in 2026. Now, economists expect new home sales to come in just under that number.

Once again, mortgage rates are a major reason why.

But for buyers, there may be an upside. When new home sales slow, builders may become more motivated to sell available inventory. Depending on the market, that could create opportunities for:

- Builder incentives

- Closing cost assistance

- Price flexibility

- Negotiation on upgrades or finishes

This doesn’t mean every builder will negotiate, and incentives vary by location. But in areas with more new construction, buyers may have more leverage than they would in a a more active market.

Home Prices Are Still Expected To Rise

Here’s one of the biggest takeaways from this mid-year housing market update: even though sales activity has slowed, experts did not revise national home price forecasts downward.

They still expect home prices to rise nationally this year.

Why? Because buyer demand has softened, but the overall number of homes for sale remains relatively limited. That imbalance continues to support prices, even in a slower market.

Local conditions can vary; some markets are cooling more than others, and pricing trends depend heavily on inventory, buyer demand, property condition, and location.

Still, experts are projecting steady price growth rather than a major decline, at least at the national level.

That can be reassuring whether you’re buying or selling. Sellers generally don’t want to see a sharp drop in values. And buyers may feel more confident about a major purchase when prices aren’t expected to fall significantly right away.

What This Means for Buyers

For buyers, the updated 2026 housing market forecast is a reminder to focus on what you can control.

Mortgage rates may not fall as quickly as hoped, but that doesn’t mean buying is off the table. A local real estate agent can help you understand what’s happening in your specific market, including inventory levels, price trends, and negotiation opportunities.

Before making a move, think about reviewing:

- Your current budget

- Estimated monthly payment at today’s rates

- Available homes in your preferred price range

- Local competition from other buyers

- New construction options and possible builder incentives

You should also speak with a trusted mortgage professional to understand loan options, rate scenarios, and affordability based on your situation.

What This Means for Sellers

For sellers, slower sales activity doesn’t point to a stalled market.

Buyers are still active, but many are more selective thanks to tighter affordability. That makes pricing, preparation, and marketing even more important.

A strong selling strategy should include:

- A realistic pricing plan based on current local data

- Thoughtful preparation before listing

- Professional marketing that highlights the home clearly

- Flexibility around buyer questions, timelines, and negotiations

With home prices still expected to rise nationally, many sellers may still be in a strong position. A successful sale will depend on understanding your local market, not relying on broader national headlines.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. Still, the market hasn’t totally stalled.

Higher inflation, economic uncertainty, and global tensions caused economists to revise their 2026 housing market forecasts. Mortgage rates are expected to remain higher than originally projected, and home sales forecasts have been adjusted lower.

Even so, more homes are still expected to sell this year than last year, and national home prices are still projected to rise.

The key is to make decisions based on your own local market, budget, and goals.

If you want to understand what this mid-year housing market update means for your next move, connect with our team. We can help you review local trends, explore your options, and decide what makes sense for the rest of 2026.

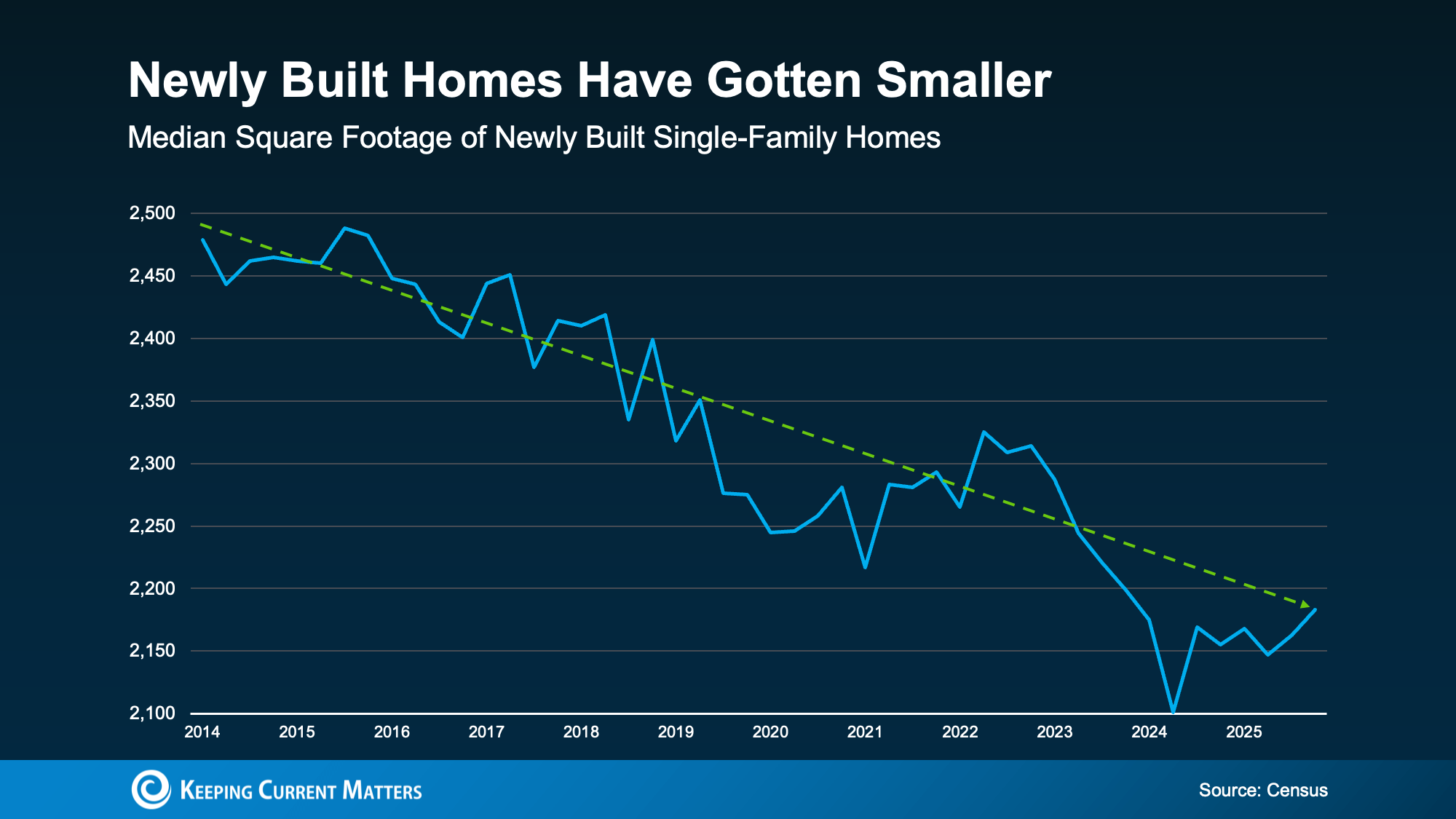

Smaller Homes, Bigger Value for Today’s Buyers

You might have started your home search with a simple picture in mind: a certain number of bedrooms, a spacious layout, maybe even a home office or dedicated workout room.

Then reality sets in. The homes that fit your budget may be smaller than what you originally imagined.

That’s a common experience for many buyers right now. Affordability is tight, and buyers are taking a closer look at what they truly need in a home. But going smaller doesn’t need to feel like a compromise.

In fact, smaller homes for buyers can offer real advantages in today’s market, especially when considering newer construction, condos, and communities designed with shared amenities.

Why Smaller Homes Are Getting More Attention

Smaller homes are not just a backup plan. They have become a more practical path for many buyers who want to balance comfort, location, and budget.

In fact, newly built homes have been getting smaller for years, and the median square footage of new single-family homes has generally declined since 2014, based on US Census data.

This shift makes sense. Builders pay close attention to what buyers are not only willing, but able to purchase. When affordability becomes a bigger concern, smaller floor plans can help bring new homes within reach for more shoppers.

Smaller New Construction Homes May Be Worth a Look

If the existing homes in your price range aren’t checking enough boxes, it may be time to explore new construction.

Many builders are focusing on smaller homes with modern layouts, updated finishes, and move-in-ready features. Smarter designs can make a smaller footprint feel more functional than an older home with a less efficient floor plan.

A smaller, newer home may offer:

- Modern appliances and finishes

- Open, practical layouts

- Less unused space

- Move-in-ready convenience

- A price point that may better fit your budget

Shifting buyer preferences are a big reason that new home prices have hit a five-year low. If you’ve ruled out new construction in the past, you want to take another look at what builders are offering in your area.

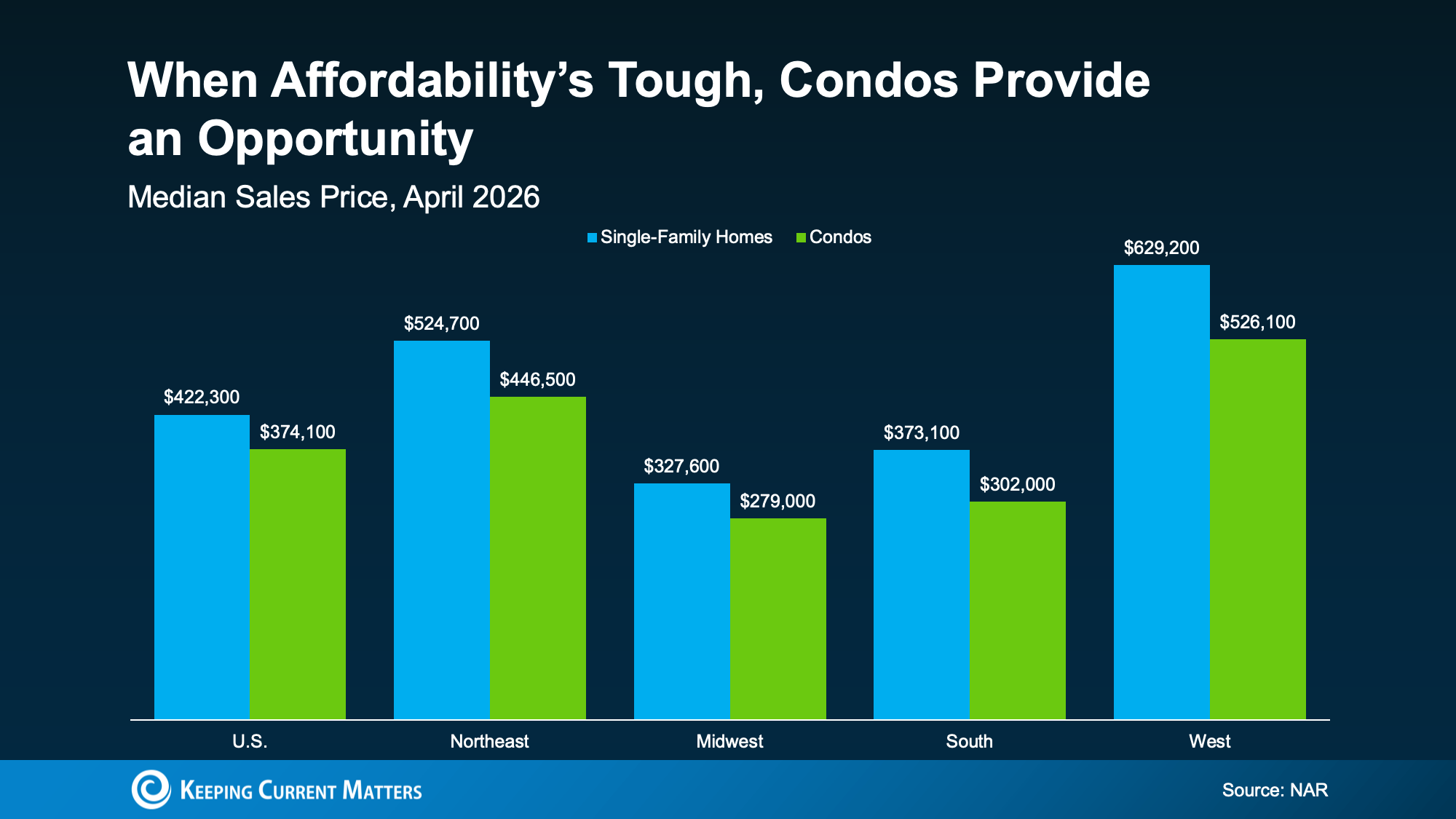

Condos Can Open Another Path to Homeownership

New construction isn’t available everywhere, and in some markets, it may still be outside your budget. That is where condos can be worth considering.

Condos are often smaller than single-family homes, which can help reduce the overall purchase price. According to data from the National Association of Realtors (NAR), the median condo price is lower than the median single-family home price in every region.

For buyers trying to make the numbers work, this is a considerable difference.

According to NAR, condo sales rose 2.7% last month, and were up year over year. And value is a driving factor. Ali Wolf, Chief Economist for New Home Source, explains:

“In addition to favoring smaller floor plans, more consumers are showing a willingness to live in an attached home. This shift is not driven by a preference for shared walls, but by a pursuit of value.”

For buyers focused on affordability, condos can offer a way to stay active in the market without stretching too far for a detached single-family home.

The Right Community Can Make a Smaller Home Feel Bigger

Square footage is important, but it’s only one part of a home’s blueprint.

A smaller home may still work well if the surrounding community gives you access to amenities that extend how you live day to day. In some condo communities, neighborhoods, and master-planned developments, shared spaces help fill in the gaps.

Depending on the community, amenities may include:

- Walking trails

- Pools

- Fitness centers

- Co-working spaces

- Outdoor gathering areas

Features like these can make a smaller home feel more livable, and functional. For example, if there’s no room for a home office, a nearby co-working space can help. If you don’t have space for a dedicated workout room, a shared fitness center can fill the gap.

Buying a Smaller Home Does Not Mean Giving Up Comfort

A smaller home can still support the way you want to live. Focusing less on total square footage and more on how the space works can offer a different perspective.

As you compare options, consider:

- Layout: Does the floor plan make daily routines easier?

- Storage: Are closets, cabinets, and garage space used efficiently?

- Natural light: Does the home feel open and comfortable?

- Shared amenities: Does the community offer spaces you would actually use?

- Location: Does the home keep you close to the places that matter to you?

A smaller home with the right layout, features, and setting may be a better fit than a larger home that stresses your budget or needs more work.

Bottom Line: Smaller Homes Can Offer Bigger Opportunities

Today’s smaller single-family homes and condos have more to offer than their square footage might suggest. They can give buyers more budget flexibility, access to newer features, and opportunities to live in communities designed with useful amenities.

If your current search feels limited, consider widening your options. A smaller home, new build, or condo may offer opportunities you never knew existed.

Curious about smaller homes, condos, or new construction options in your area? Contact our brokerage to explore what’s available and compare homes that fit your budget and goals.

Housing Affordability Today: What Buyers Should Know

Let’s talk honestly about housing affordability today.

If you’ve been thinking about buying a home, selling your current home, or making a move, you’ve probably seen plenty of headlines about mortgage rates, home prices, inflation, and affordability. Some of those headlines are helpful. Others leave out critical information.

The truth is, affordability is not shaped by one factor alone. Mortgage rates matter, but they’re not the only piece of the puzzle. Wages, home prices, inventory, buyer competition, and your personal financial situation all play a role.

Here’s a clearer look at what’s happening right now: the good, the challenging, and what it could mean for your next move.

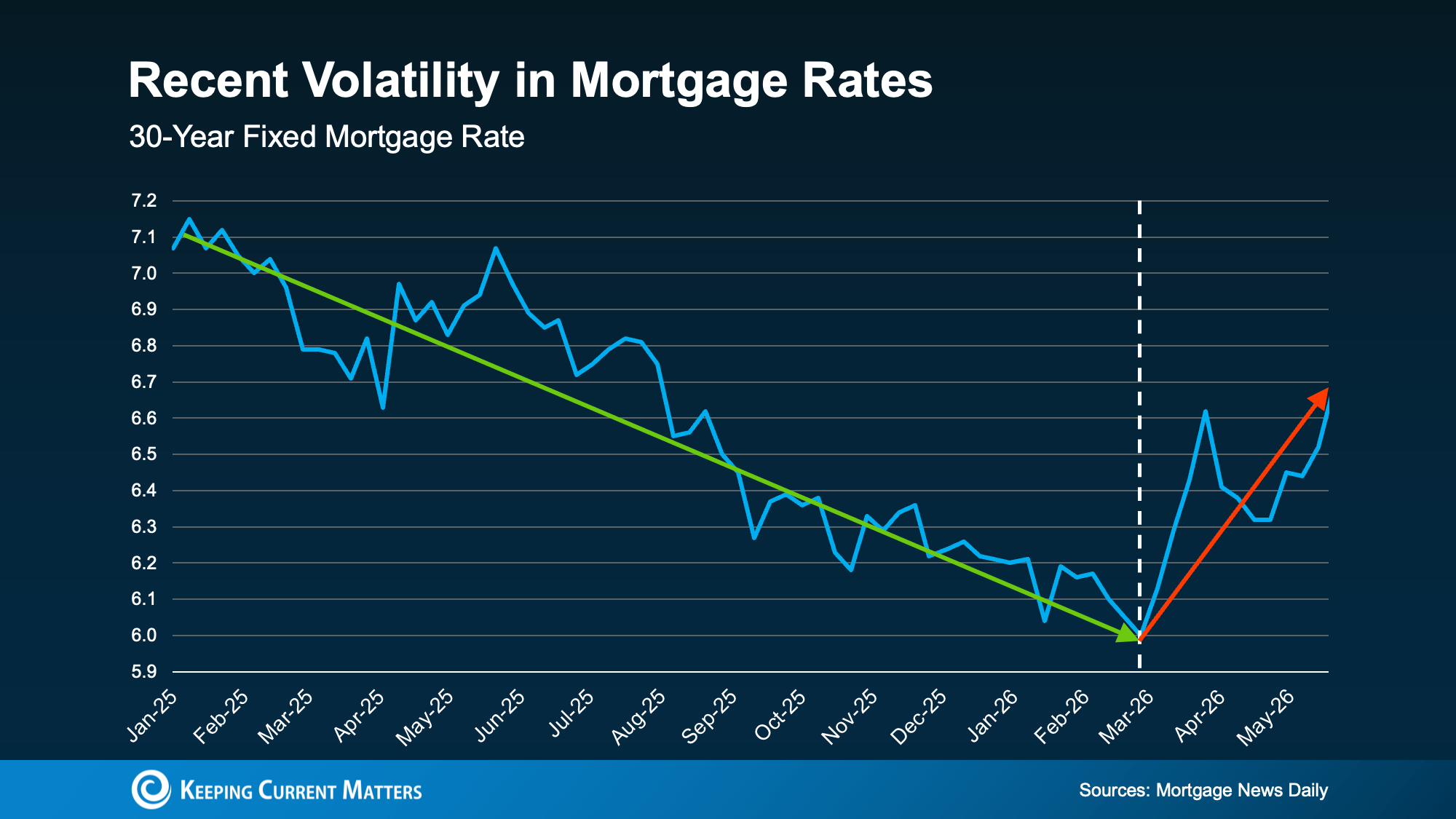

Mortgage Rates Have Been Rising

After a year or more of mortgage rates trending down, they’ve started climbing again. And for buyers, that’s incredibly frustrating.

So, why are rates moving higher?

A big reason is uncertainty. Mortgage rates are heavily influenced by broader economic conditions, and uncertainty often puts upward pressure on rates.

Ongoing global uncertainty, continued tensions in the Middle East, and inflation that has not fully cooled off are all having an impact. Colin Robertson, Founder of The Truth About Mortgage, explained it this way:

“You can’t have $100 a barrel oil and not expect inflation to rise, which translates to higher bond yields and mortgage rates.”

That matters because higher bond yields often lead to higher mortgage rates. And when mortgage rates rise, monthly payments can become more difficult for buyers to manage. Recent data from Mortgage News Daily illustrates the effect this has:

Should Buyers Wait for Mortgage Rates To Fall?

With unpredictable rates, it’s natural to wonder if waiting is the safer move.

If rates are higher now, will they come back down once uncertainty eases? Possibly. But there’s no guaranteed timeline.

Rates aren’t likely to drop until inflation cools further and global uncertainty improves. Even then, many experts believe rates may not drop dramatically. They may return to somewhere in the low- to mid-6% range we were seeing earlier this year.

That means waiting for a major rate drop could keep buyers on the sidelines longer than expected.

For many buyers, the question isn’t, “Will rates fall?”, but:

Can I afford the home and monthly payment based on today’s numbers?

If the answer is yes, and you find a home that fits your needs and budget, buying may still be worth considering. No one can predict exactly when rates will fall, how far they’ll fall, or what home prices and competition will look like when they do.

Wages Are Outpacing Home Prices

On the bright side, there’s also some encouraging news that doesn’t always make the headlines.

While inflation has made many parts of everyday life more expensive, recent data from the Federal Reserve Bank of Atlanta and Redfin show wages have been growing faster than home prices.

According to the data:

- Wages have recently been increasing around 4% year-over-year.

- Home price growth has been closer to 2% year-over-year.

That difference matters for home affordability.

When wages rise faster than home prices, buyers may slowly regain some purchasing power. It doesn’t solve the affordability challenge overnight, but it can help make a home purchase more manageable over time.

For buyers, every little bit of financial breathing room helps.

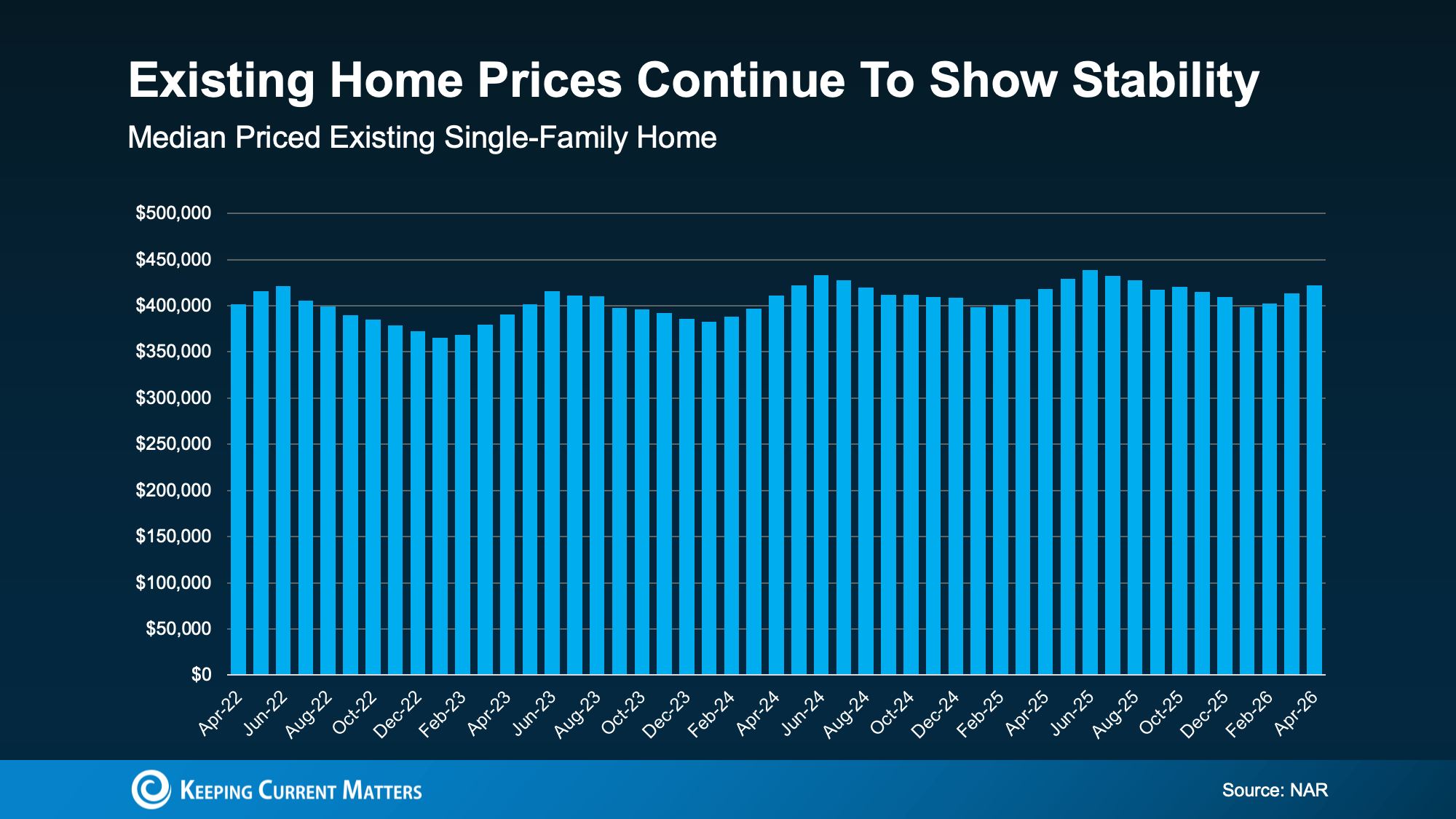

Existing Home Prices Have Held Steady

Another important part of the affordability picture is home prices.

National Association of Realtors data from the past four years show existing home prices have remained relatively steady. There hasn’t been a dramatic runup, but there hasn’t been a crash either. Instead, the market has seen more stability and slower growth.

Price stability like this can give buyers a real helping hand.

Part of what’s keeping prices steadier is that buyers now have more choices than they did in the most competitive parts of the market. More inventory can create:

- Less intense competition

- More time to make decisions

- Better opportunities to compare homes

- More room for negotiation in some situations

Of course, this doesn’t mean every market is a buyer’s paradise. Local conditions always matter. But, having more options can help buyers find a home that better fits their lifestyle and budget.

What Housing Affordability Means for Your Move

Today’s housing market is not simple. Mortgage rates are higher than many buyers hoped they would be, and global uncertainty is keeping rates from settling down quickly.

But the full affordability picture is more balanced than the headlines may suggest.

Rates are still a challenge, but wages are growing faster than home prices, and existing home prices have stayed relatively steady. Buyers today might have more options to make stronger decisions than they did when the market was tighter and more competitive.

As always, the right move depends on your budget, goals, timeline, and local market.

Before deciding whether to buy now or wait, it’s worth running the numbers with today’s information. Not with guesses from last year, last month, or national headlines.

Bottom Line

Housing affordability today is about more than just mortgage rates.

Rates are still a major factor, but wages, home prices, inventory, and local market conditions all matter too. If you can afford the monthly payment and find a home that fit your needs, you may not have to wait for the “perfect” option.

Want to figure out the best move for your situation? Connect with a local real estate professional to review current homes, pricing, and your area’s unique market conditions.

VA Home Loan Benefits All Veterans Should Know

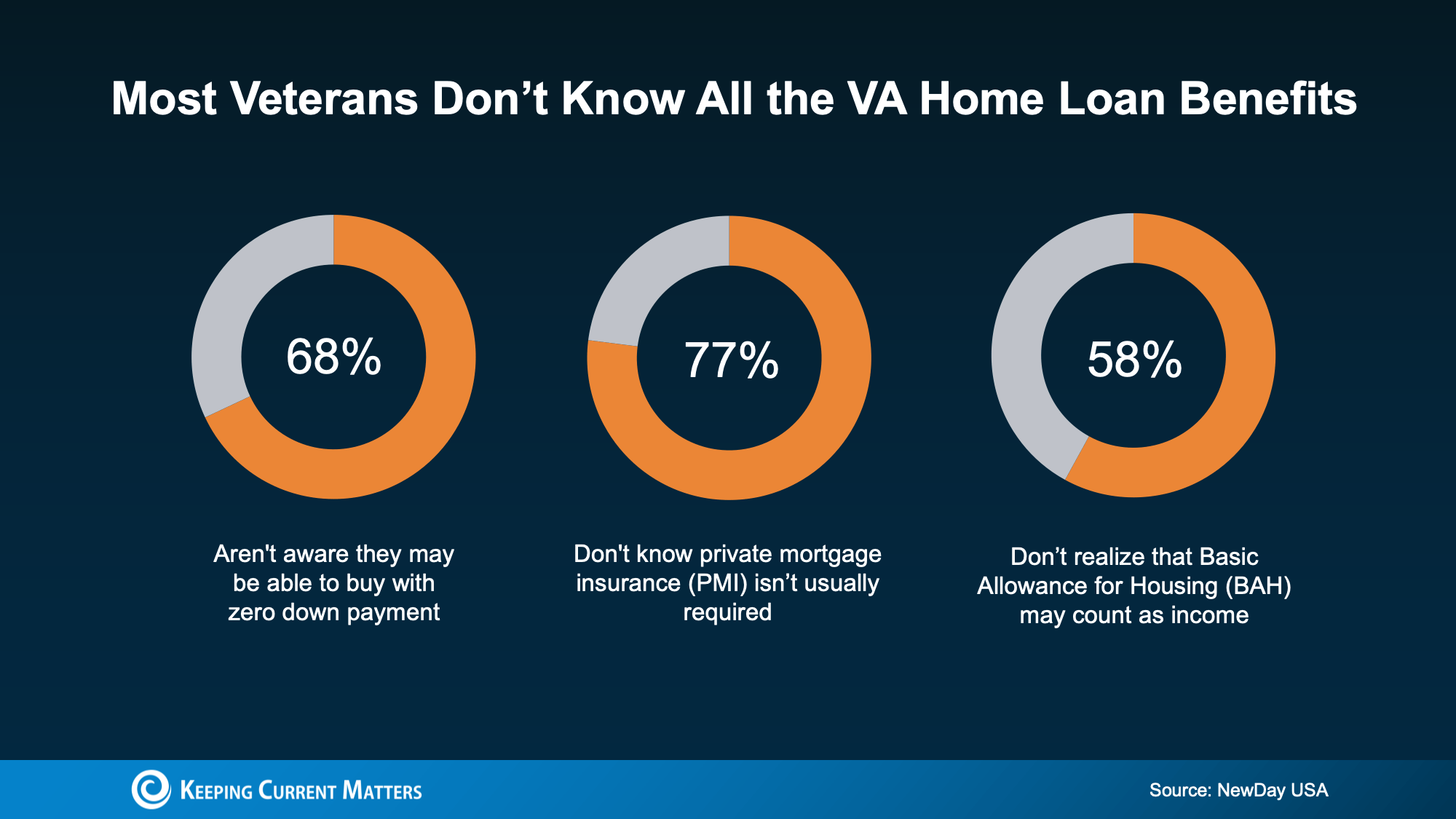

Almost half of Veterans (49%) feel homeownership is beyond their reach, according to a recent NewDay USA survey.

But many Veterans could be closer to buying a home than they think.

VA home loan benefits have been available for more than 80 years, but a lot of confusion remains about what’s actually covered. Some buyers assume they’ll need an impossibly large down payment. Others believe they’ll have high closing costs or monthly private mortgage insurance (PMI).

Misunderstandings like these can make homeownership feel farther away than it may really be.

VA Home Loan Benefits Many Veterans Overlook

A VA loan can offer several advantages for eligible buyers. While every buyer’s situation is different, these benefits may help reduce some of the upfront and monthly costs that often make buying a home feel financially overwhelming.

Let’s walk through a few of the biggest misconceptions.

You May Not Need a Down Payment

One of the most valuable VA home loan benefits is the potential to buy with zero money down.

That surprises many buyers. According to the NewDay USA survey, many respondents thought they would need to save between $10,000 and $19,900 before purchasing a home.

For some buyers, that kind of savings goal can take years. But with a VA loan, a large down payment isn’t always necessary. That can make the path to homeownership feel much more realistic for eligible Veterans and service members.

You May Have Lower Closing Costs

Closing costs are another area where VA loans can make a big difference.

According to the Department of Veterans Affairs, VA loans can include limits on the types of closing costs buyers are required to pay. That may help eligible buyers keep more money in their pocket on closing day.

When combined with the potential for no down payment, this benefit can lower the amount you need to save up before buying a home.

Your Monthly PMI Cost Could Be $0

Many loan programs require private mortgage insurance, commonly called PMI, when a buyer puts less than 20% down.

VA loans typically do not require monthly PMI, even when buyers use low or no money down.

That can make a meaningful difference in your monthly housing costs. If you use a conventional loan instead, you could pay $100 to $300 per month in PMI until you reach 20% equity, according to NewDay USA.

Over time, avoiding that monthly cost could add up to thousands of dollars.

Your BAH and BAS May Help You Qualify

For active-duty service members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan.

Since both BAH and BAS are non-taxable, they can help increase the amount you can qualify for. A trusted lender can help review your full financial picture and explain how these allowances might apply to your situation.

Why This Matters for Veterans and Service Members

If you have been assuming homeownership is out of reach, it may be worth taking a closer look at your VA home loan benefit.

A VA loan may help eligible buyers by offering:

- The potential for no down payment

- Limits on certain closing costs

- No monthly PMI in many cases

- The ability to include qualifying BAH and BAS income

These benefits don’t guarantee approval, and every buyer’s situation is different. But they may help remove some of the common barriers that keep Veterans and service members from exploring homeownership.

Bottom Line

VA home loan benefits can be a powerful tool for eligible Veterans, active-duty service members, and qualifying reservists.

If you’ve served, are currently serving, or know someone who has, connect with a trusted lender who understands VA loans. They can help you review your options, understand what you may qualify for, and decide whether buying a home makes sense for your goals.

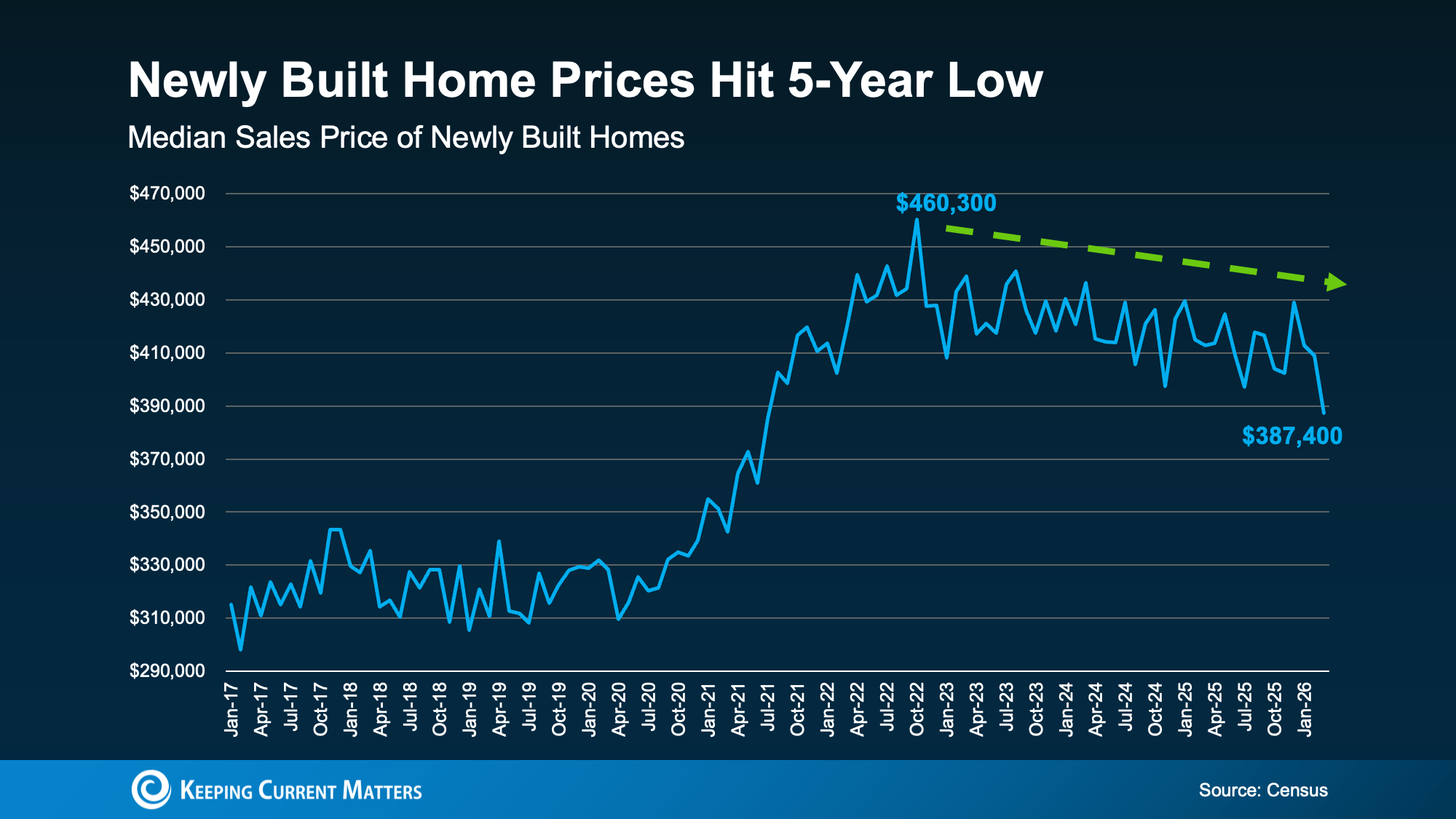

New Home Prices Hit a 5-Year Low

If you’ve assumed a newly built home is out of reach, it may be time to take another look.

The median sale price of a newly built home has dropped to its lowest level since 2021, according to the latest United States Census Bureau data. At the same time, many builders are still offering incentives to help attract buyers.

New Home Prices Have Come Down

After climbing sharply during the pandemic years, new home prices have eased. The median sale price of a newly built home is now around $390,000, which is the lowest level in nearly five years.

Local markets can vary, but the national trend may work in buyers’ favor, especially in the entry-level price range. According to Zonda, prices in the entry-level new construction segment have dropped about 2.7% over the past 12 months, which is more than any other price tier.

This doesn’t mean every newly built home is suddenly affordable now. But, it does mean that buyers may be seeing some of the best new construction pricing since 2021.

Why Lower New Home Prices Do Not Mean a 2008 Repeat

Lower prices can make some buyers wonder whether the new home market is in trouble. But today’s conditions are very different from 2008.

Builders are being more intentional about how much inventory they bring to market. Instead of letting homes pile up, many are using pricing adjustments and incentives to keep inventory moving.

It’s also important to keep perspective. Even with recent price improvements, new home prices are still higher than pre-pandemic norms. This isn’t a market crash. It’s a builder strategy designed to match today’s buyer demand.

Builders Are Still Offering Buyer Incentives

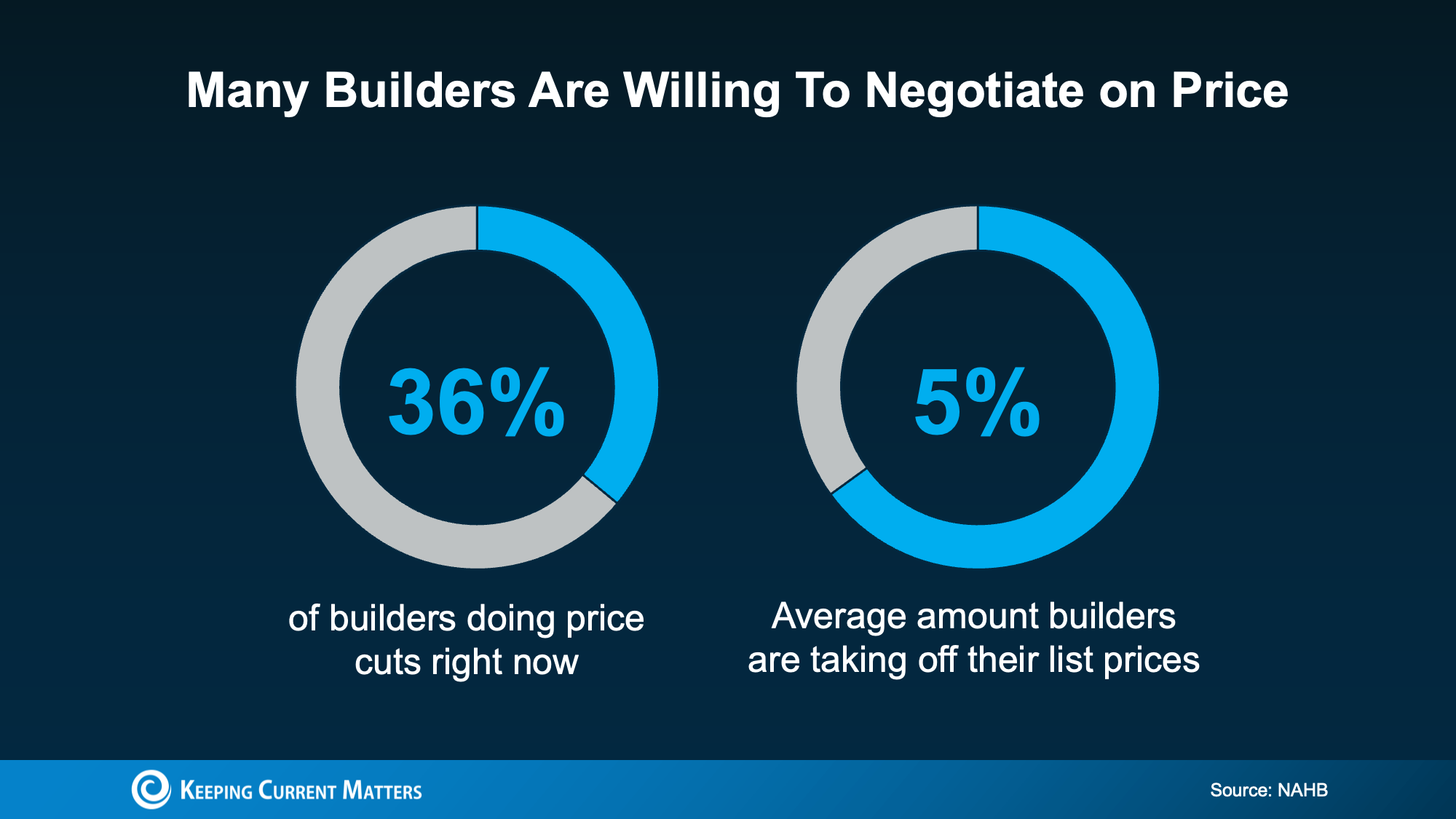

Lower prices aren’t the only potential advantage for buyers. According to the National Association of Home Builders (NAHB), 60% of builders are currently offering some form of incentive to attract buyers.

Common builder incentives include:

- Closing cost assistance: Some builders may help cover upfront costs, which can reduce the cash buyers need at closing.

- Upgrade packages: Builders might include premium finishes, appliance packages, or design features at no additional cost.

- Mortgage rate buydowns: Some builders might pay to reduce a buyer’s mortgage rate, which can lower the monthly payment.

- Price cuts: More than one in three builders, or 36%, are cutting prices right now, with reductions averaging around 5% off list price.

Why Builders May Be More Flexible Than Sellers

Many buyers assume builders won’t negotiate on price. But builders often have different motivations than individual homeowners.

A homeowner may decide to take a listing off the market rather than accept a lower price. Meanwhile, builders usually need to sell the homes they’ve already built so they can keep projects moving.

As Joel Berner, Senior Economist at Realtor.com, explains:

“. . . many existing-home sellers resort to taking down their listing instead of taking less than their desired price, but builders are more motivated to sell their inventory than owner-occupants . . .”

That doesn’t mean every builder will negotiate the same way. But it does mean buyers should ask about current pricing, incentives, rate buydowns, and available inventory before assuming a new build is outside their budget.

What This Means for Home Buyers

If you’re shopping for a home, newly built homes may deserve a closer look. Between lower new home prices and ongoing builder incentives, some buyers may find opportunities they did not expect.

Before you make a decision, look at the whole picture:

- The purchase price

- Builder incentives

- Closing cost assistance

- Mortgage rate buydown options

- Included upgrades

- Monthly payment estimates

- Location, commute, and long-term housing needs

A local real estate agent can help you compare new construction homes with existing homes in your market, review builder incentives, and understand what questions to ask before you make a move.

Bottom Line

New home prices have eased, and many builders are still offering incentives to attract buyers. That could give today’s home shoppers more room to explore newly built homes than they’ve had in recent years.

If you’re curious about new construction homes in your area, connect with a local real estate professional to see what’s available and what builder incentives might be offered in your market.

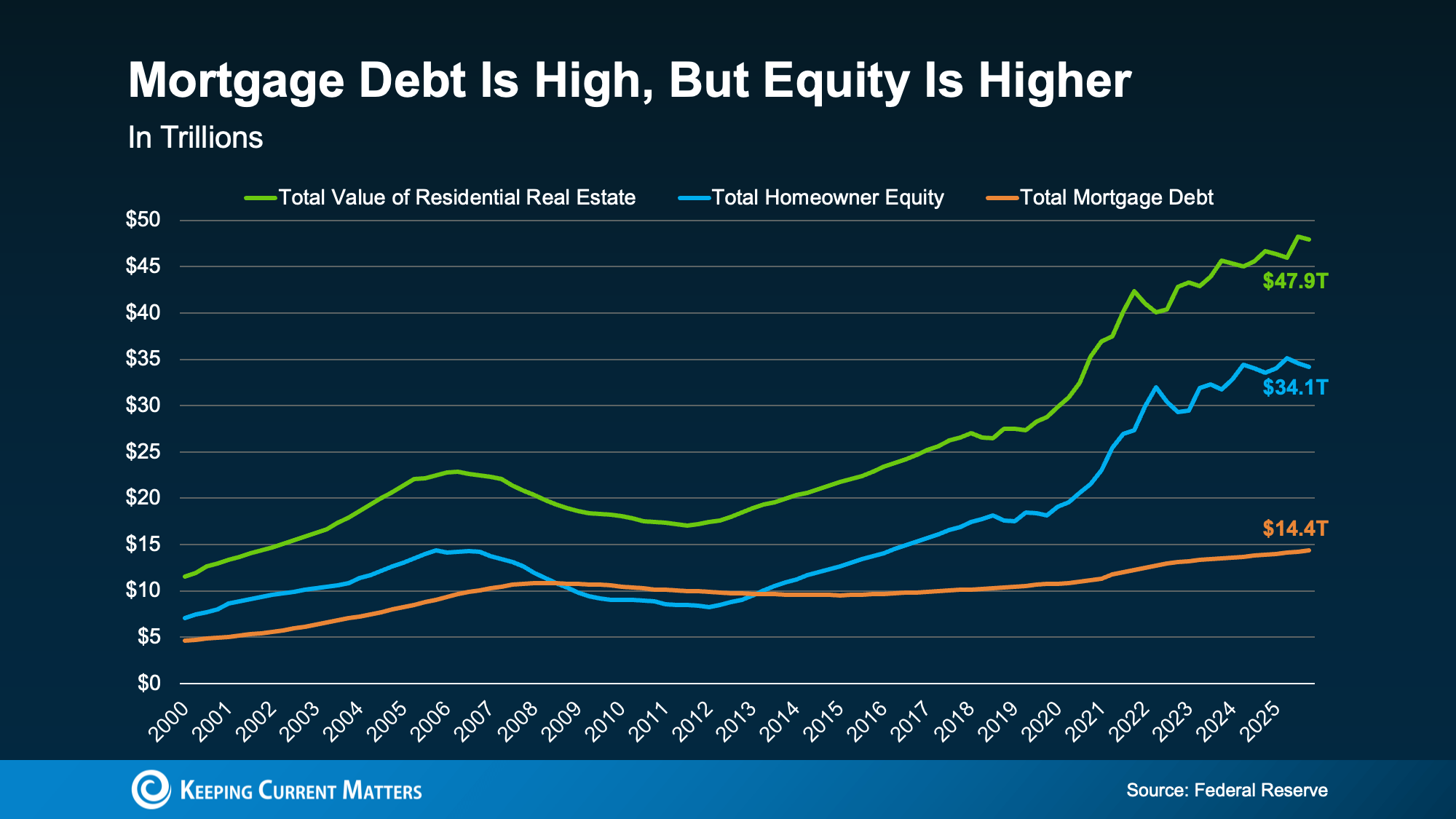

Record High Mortgage Debt: What Do Buyers Need To Know?

Mortgage debt in the United States has hit a record high, and at first glance, that looks like a warning sign for the housing market.

It’s an attention-grabbing headline for sure. After all, when people hear “record debt,” most think back to the 2008 housing crash and wonder if today’s market is heading in the same direction.

But headlines leave out the real story.

It’s true that mortgage debt is higher than ever. But, so are home values and homeowner equity. When you add in those missing pieces, the real picture becomes much less alarming than you might think.

Mortgage Debt Is High, But So Is Homeowner Wealth

New data from the Federal Reserve says total U.S. mortgage debt is now around $14.4 trillion, and the Federal Reserve Bank of New York found it was $13.19 trillion at the end of March 2026. Both numbers are record highs, but they’re missing some critical perspective.

Meanwhile, the total value of U.S. homes is about $47.9 trillion, while homeowners collectively hold roughly $34.1 trillion in equity. In other words, homeowners owe a lot, but they also own a great deal more.

Mortgage debt has peaked, but that alone doesn’t determine the health of the housing market. What matters more is how much equity homeowners have compared to what they owe.

Right now, homeowner equity is more than double the amount of mortgage debt, and near its own historical peak. That’s a very different situation from the years surrounding the 2008 housing crisis.

Why Today’s Housing Market Is Not Like 2008

During the housing crash, many homeowners owed more on their mortgages than their homes were worth. When home prices fell, they had little to no financial cushion. That caused a wave of serious distress, including short sales and foreclosures.

Today’s market looks very different.

Homeowners have significantly more equity than debt, which gives them options. Even if home prices soften in some areas, many owners still have a substantial financial buffer. They can sell, refinance when conditions improve, or use their equity strategically if needed.

That equity cushion is one of the biggest reasons today’s housing market is on much stronger footing than it was during the last crash.

Many Homeowners Have Little or No Mortgage Debt

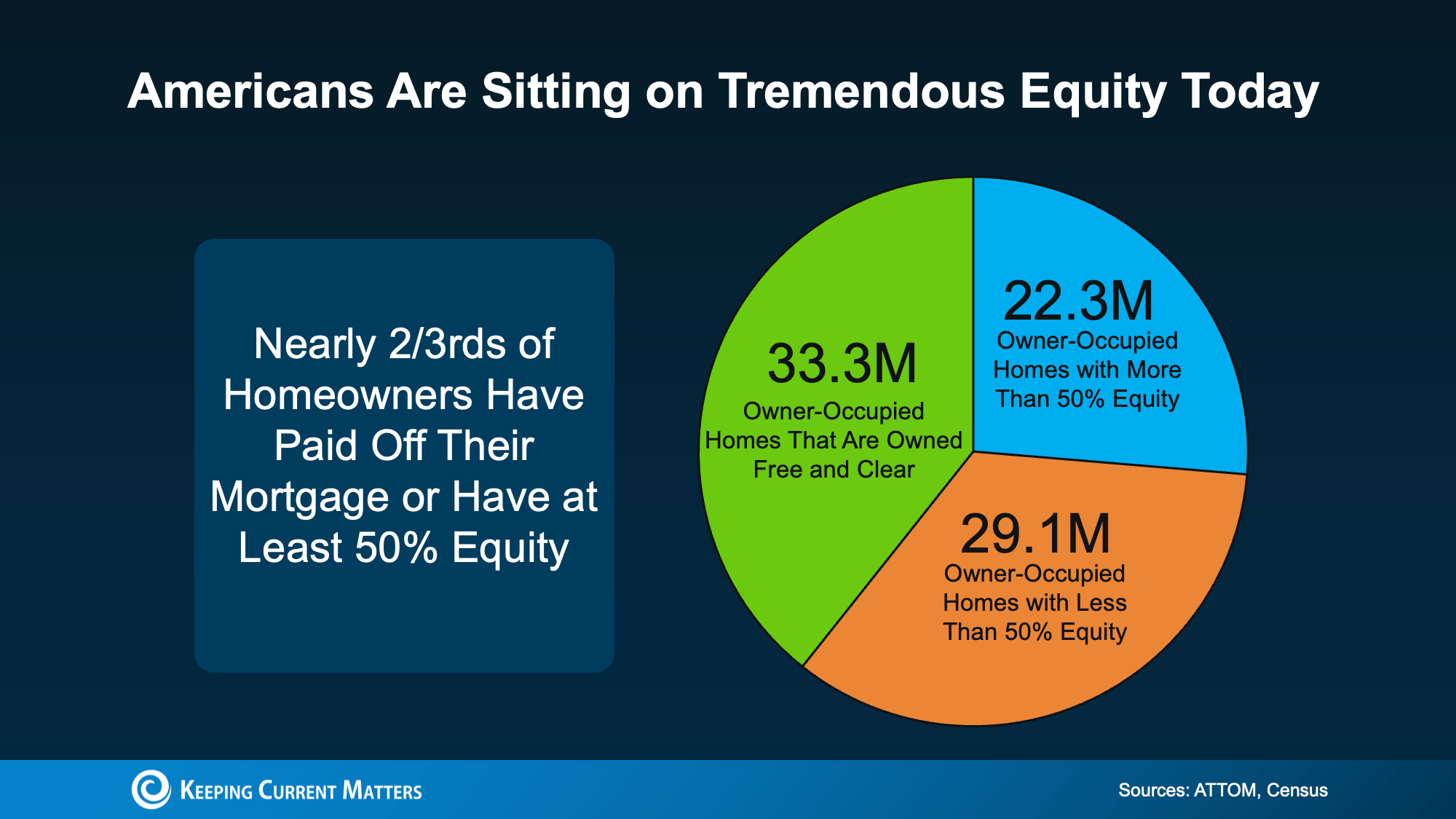

The strength of today’s market is even clearer when you look at homeowners individually. Recent data from ATTOM and Census illustrate this point.

Of all owner-occupied homes in the United States, 33.3 million are owned free and clear, meaning there’s no mortgage on the property at all. On top of that, 22.3 million homeowners have more than 50% equity in their homes.

Put those groups together, and nearly two-thirds of homeowners are in an exceptionally strong financial position. Some owe no mortgage debt, and others owe far less than their homes are worth.

Those are the signs of a strong market, not a fragile one.

What About Homeowners With Less Than 50% Equity?

The remaining group includes homeowners with less than 50% equity. But these homeowners aren’t necessarily in trouble.

Many of these homeowners are simply recent buyers. Since equity builds over time through mortgage payments and home price appreciation, newer buyers naturally tend to have less equity than people who have owned their homes for years.

Low equity doesn’t always signal financial stress or threat of foreclosure. Often, it just means someone is a first-time buyer in early homeownership.

The Real Story Behind Record Mortgage Debt

Mortgage debt is a critical piece of the housing market’s health, but it’s only one piece it.

When you also consider record or near-record home values, strong homeowner equity, and the number of people who own their homes outright, there’s far less cause for alarm.

Homeowners today aren’t severely overleveraged the way they were before the 2008 crash. Many have meaningful equity, and most have no mortgage debt at all.

Bottom Line: Strong Equity Balances High Debt

Dramatic headlines about record mortgage debt can make it seem like the housing market is in trouble, but the actual data tell a more reassuring story.

Home values are high. Homeowner equity is strong. And a large share of homeowners are in a stable financial position.

So while mortgage debt has reached a record level, today’s market has a much stronger foundation than recent headlines would suggest.

No matter if you’re thinking about buying, selling, or simply trying to understand what these numbers mean for your local market, talking with a trusted real estate professional can help you learn the real story.

Are Home Prices Going To Fall? Here’s What Buyers Should Know

One of the biggest questions buyers are asking right now is: Will home prices fall after I buy?

It’s a common concern. Buying a home is a major financial decision, and no one wants to feel like they bought too early, or too late. With headlines pointing to changing prices in some markets, it’s easy to want to play it safe by waiting.

But the short-term noise isn’t the whole story. While some local markets may see temporary dips, the bigger, long-term picture is much different: home prices historically rise over time.

What Housing Market Data Shows

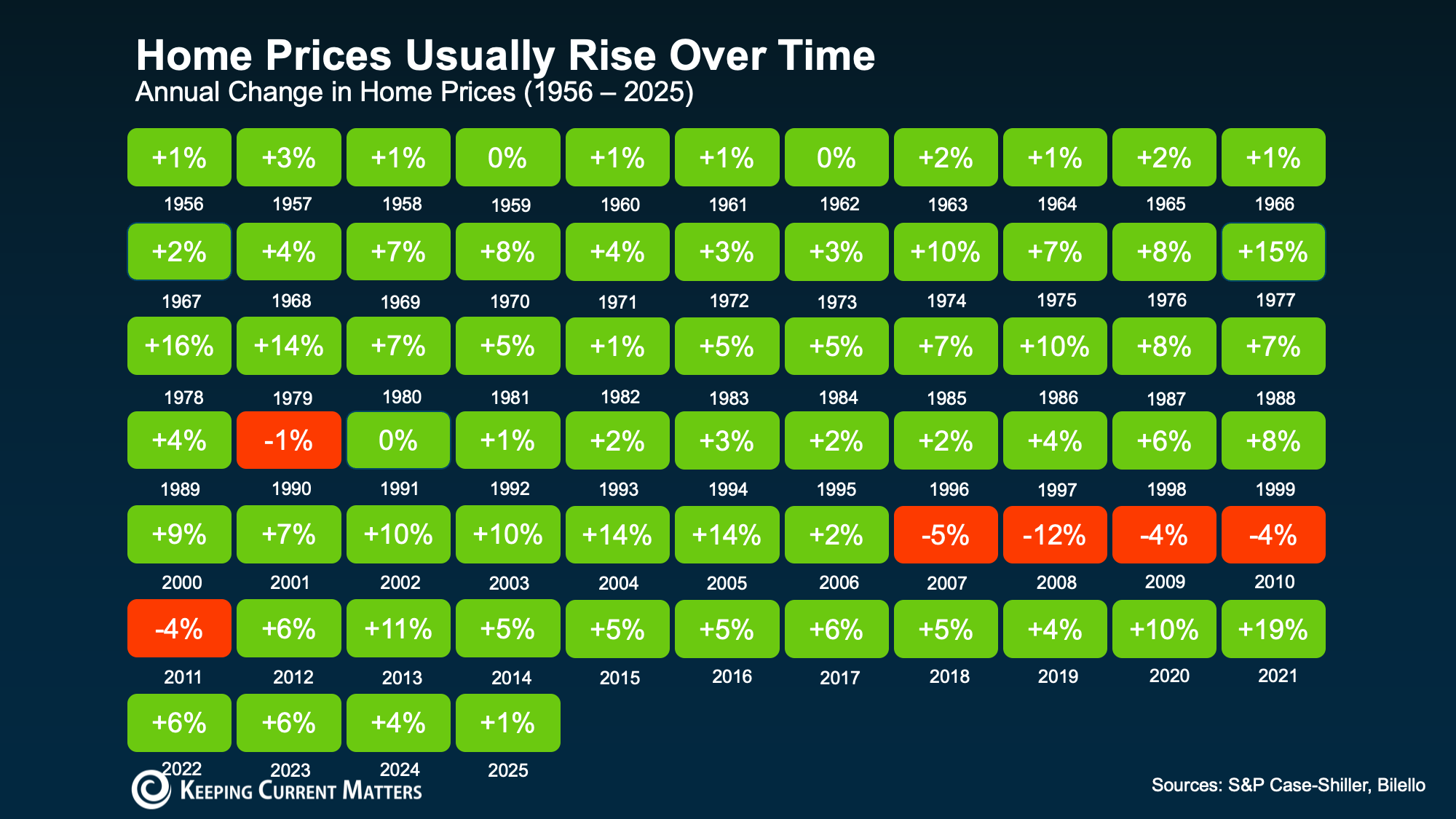

When you look at long-term housing data, one trend becomes clear. Home values have generally moved upward for decades.

Yes, there have been exceptions. The housing crash of 2008 is the most dramatic example. And in some years, certain markets have seen slight declines. But outside of major disruptions, home prices have typically either held steady or increased, and data from Case-Shiller and Biello shows this.

That long-term track record is important for buyers to understand. Real estate is not usually about what happens over the next few weeks or months. It’s about what happens over several years.

Short-term price drops can happen, especially in markets where inventory is rising or buyer demand has cooled. But historically, those dips have proven to be temporary.

Why Home Prices Tend To Rise Over Time

There are several consistent reasons home prices tend to increase in the long run.

People Always Need Homes

Life changes keep the housing market moving. People get married, have children, change jobs, retire, downsize, or relocate to be closer to family. No matter what the market is doing, people always need places to live.

Steady demand like this helps support home values over time.

Housing Supply Is Still Limited

Even though more homes may be available for sale than there were during the tightest years of the market, many areas are still dealing with housing shortages.

When there aren’t enough homes to meet buyer demand, prices tend to stay elevated. Even when demand slows, limited inventory helps prevent dramatic price drops in most markets.

Inflation Plays a Role

Over time, the cost of goods and services tends to rise, and housing is no exception. Land, labor, materials, and construction costs all influence home values.

As the everyday cost of living inflates, home prices naturally move higher too.

What This Means If You’re Thinking About Buying

It’s natural to worry about whether home prices will drop after you buy a home. That concern is especially common among first-time buyers trying to make a smart financial decision.

But what matters most is your own expected timeline.

If you’re planning to buy a home and stay there for several years, short-term market movements matter less. That’s because time gives your home more opportunity to appreciate in value, helping you ride out the kind of ups and downs we’re seeing in some markets.

That’s why many real estate professionals recommend buying only when you expect to stay in the home for at least five years. While there’s no guaranteed timeline, a longer-term approach often gives homeowners a better chance to benefit from rising values.

Real Estate Is Local

Another critical point to remember is that not all housing markets are the same.

Some areas may see home prices soften. Others may continue to rise because demand is strong and inventory remains low. National headlines can give you a general idea of what’s happening, but they don’t always reflect conditions in your specific city, neighborhood, or price range.

That’s why local market insight matters. A trusted real estate agent can help you understand whether prices are rising, flattening, or adjusting in your area.

Don’t Try To Time the Market Perfectly

Trying to buy at the exact bottom of the market is extremely difficult. By the time it’s clear prices have bottomed out, competition may already be increasing again.

Instead of focusing only on timing, focus on whether buying makes sense for your life, your finances, and your long-term goals.

Ask yourself:

- Can I comfortably afford the monthly mortgage payment?

- Do I plan to stay in the home for several years?

- Does buying now support my lifestyle and financial goals?

- Am I prepared for the responsibilities of homeownership?

If the answer is yes, buying may still make sense, even if prices fluctuate in the short term.

Bottom Line: Most Price Drops Are Temporary

So, are home prices going to fall? In some markets, small short-term declines are possible. Historically though, data shows home prices strongly tend to rise over time.

That’s why buying a home is often considered a long-term investment, not a short-term gamble.

You don’t have to buy before you’re ready. But if homeownership fits your goals and you plan to stay put for a while, today’s market headlines shouldn’t scare you away.

For the most reliable picture, talk with a local real estate agent who can explain what home prices are doing in your area and help you decide whether now is the right time to make a move.

4 Ways To Make Your Home Offer Stand Out This Spring

If you’re planning to buy a home this spring, you may have more options than buyers have had in recent years. Home inventory has improved in many markets, and some sellers are more willing to negotiate than they were during the peak of the market.

But that doesn’t mean every homebuyer has an easy path forward.

In popular neighborhoods or areas where there still aren’t enough homes for sale, competition can pick up quickly. And spring is traditionally one of the busiest seasons for real estate, as many buyers hope to move before summer or get settled before the next school year begins.

That’s why making a strong, thoughtful offer still matters. Even in a more balanced market, the right strategy can help your offer stand out when you find a home you love.

Why Strong Offers Still Matter This Spring

Spring often brings more buyers into the market. Experts at Zillow and Realtor.com often say it’s one of the busiest times of year to purchase a home.

More activity can mean more competition, especially for homes that are priced well, located in desirable areas, or move-in ready. So while buyers may have more leverage than they did a few years ago, local market conditions still play a major role.

Here are four ways to give your offer an edge this spring.

1. Start with a Strong and Realistic Offer

It’s always tempting to make a low offer and hope the seller negotiates. In some markets, that approach may work. But if a home is getting a lot of attention, starting too low could cause the seller to move on to another buyer.

Instead, focus on making an offer that is competitive, realistic, and aligned with your local market.

As Bankrate explains:

“There is no magic formula for an optimal home offer. Any offer will be heavily dependent on asking price and local market conditions . . . Your real estate agent will know the local market well and can advise what a competitive — but fair — offer will look like in your area.”

A strong offer doesn’t always mean offering far above asking price. Most times, it means understanding the home’s value, the seller’s position, and how quickly similar homes are selling nearby.

2. Strategize for Multiple Competing Offers

If you find a home that checks all the boxes, another buyer likely feels the same way. That’s why it helps to talk with your agent ahead of time about what you’re willing to do if multiple offers come in.

One option your agent may discuss is an escalation clause. Investopedia defines it this way:

“An escalation clause is a way to automatically escalate your bid by a certain dollar amount, up to a certain ceiling, to compete with other bids.”

This strategy can help you stay competitive without going beyond your comfort zone. The key is setting a clear maximum price before emotions take over.

Still, there are potential risks to understand and keep in mind. If the home appraises for less than your offer price, you may need to cover the difference out of pocket. Your agent can help you decide whether an escalation clause makes sense for your budget and your market.

3. Keep Your Offer as Clean as Possible

Price is important, but it isn’t the only thing sellers consider. The terms of your offer can also make a big difference.

A clean offer is one that feels simple, straightforward, and easy for the seller to accept. That may mean limiting unnecessary requests, being thoughtful about contingencies, or avoiding terms that could make the transaction feel complicated.

As Redfin says:

“Sellers tend to want clean, straightforward offers with minimal strings attached. Keep your requests simple and focus on the essentials.”

This means working with your agent to decide which terms matter most and where you may have flexibility. The trick is to strike a balance, making an attractive offer without giving up important protections.

4. Be Flexible When It Helps the Seller

Sometimes the strongest offer is about more than price. In some cases, there are things that matter to the seller beyond simple dollar amount.

As NerdWallet explains:

“As you prepare an offer, you tend to focus on what the seller has (a house) and what you want (their house). But you’ll gain a competitive edge by viewing the transaction from the seller’s eyes: What does the seller want?”

For example, does the seller need extra time to move? Are they hoping for a quick closing? Would a flexible possession date make the offer more appealing?

Your agent can communicate with the seller’s agent to better understand what matters most. When you can align your offer with the seller’s priorities, you may have a big advantage over buyers who only focus on price.

Bottom Line: The Right Offer Strategy Can Help You Win

Today’s housing market may offer buyers more breathing room, but strong offers still matter, especially during the busy spring season.

If you’re getting ready to buy, work with a trusted local real estate agent who understands your market. The right strategy can help you move quickly, make a competitive offer, and feel confident when the right home comes along.

3 Things That Aren’t Going To Happen in Today’s Housing Market

There’s no shortage of uncertainty in today’s housing market, and that’s naturally fueling a lot of dramatic headlines. And if you’re trying to buy a home, that kind of noise can make your decision feel a lot more complicated.

In fact, a recent CNBC study asked homebuyers what they’re most concerned about, and the same three topics kept rising to the top:

- Mortgage rates

- The number of homes for sale

- Home prices

The challenge is that much of what people are hearing about these topics is driven by misconceptions, not facts. Let’s separate the headlines from what the data is really showing.

Misconception #1: “I Should Wait Because Mortgage Rates Are Going To Fall Dramatically”

One of the most common ideas circulating on social media is that mortgage rates are about to drop sharply, so waiting to buy is the smarter move.

But is that what experts are expecting?

While mortgage rates have eased a little in recent weeks, forecasts still aren’t predicting any major declines. It’s more likely that rates will stay in the low 6% range this year.

And that’s not a remarkable shift from the rates we’re seeing today:

Obviously, a lot depends on inflation and the broader economy. But based on what we know right now, waiting for a big drop in mortgage rates may not play out the way many buyers hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

And even with rates where they are today, buying a home is already more affordable than it was a year ago. Even if rates don’t drop in the near future, home affordability is better now than a year ago.

Misconception #2: “There Are Too Many Homes for Sale”

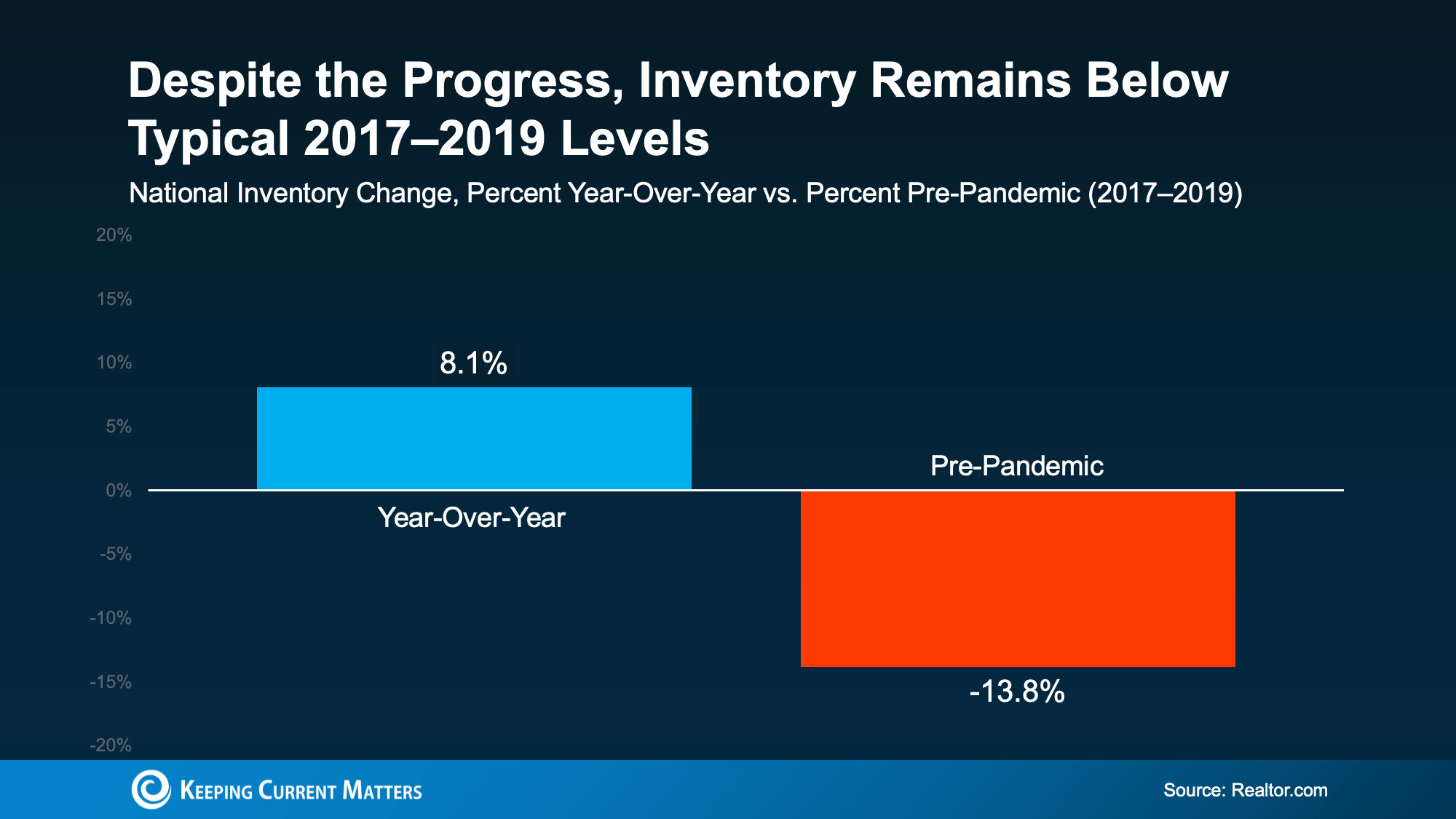

You may have heard that housing inventory is rising. Nationally, that’s true: the number of homes for sale is 8% higher than it was at this time last year. But that’s not bad news. In lots of markets, it’s easing the pressure on buyers.

The problem is that some headlines make good news sound like bad news. They focus on the fact that inventory is at its highest level since 2019 or highlight how many new homes builders are adding. That can make it sound like supply is growing too much, too fast.

But the bigger picture tells a different story.

According to new Realtor.com data, even though inventory is up over last year, it’s still nearly 14% lower than it was in the last normal housing market from 2017 to 2019:

And while local conditions vary, only 9 states have more inventory now than they did before the pandemic. That’s a major reason there aren’t enough homes for sale to trigger anything like the 2008 housing crash.

Misconception #3: “Home Prices Are About To Crash”

This is another common headline you’ve probably seen. This misconception comes from the fact that a few metros are actually seeing small price declines. Influencers are pointing to this to claim home prices are crashing. But this is absolutely not true nationally.

In most markets, home prices are still rising, not falling. Here’s why:

- Many homeowners are choosing not to sell to avoid giving up the low mortgage rate they locked in a few years ago. That continues to limit how much inventory can grow.

- Inventory remains below pre-pandemic norms. There still aren’t enough homes for sale to cause a widespread price crash.

- Even in markets with more listings, some sellers are pulling their homes off the market instead of making major price cuts.

Those are three big reasons home prices are not on track for a crash.

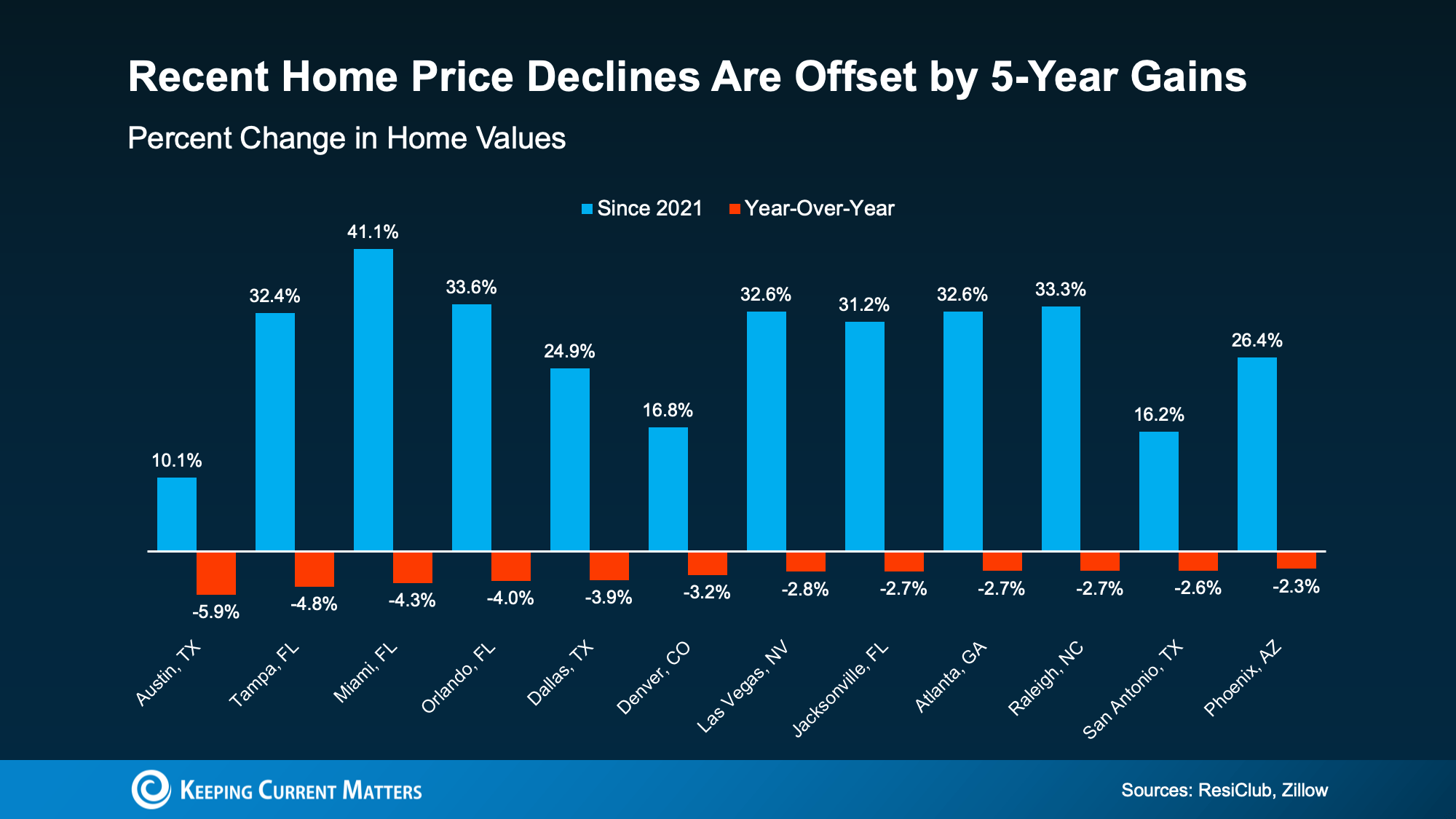

And even in the areas seeing small price declines, those drops are nowhere near enough to erase the huge gains most homeowners have built over the past five years:

These drops don’t signal a crash. They show the market settling after a few years of record-breaking spikes in prices.

Bottom Line: Get the Facts on Your Market

The discussions we see online can often exaggerate the negative and ignore the positive, especially in housing. If you want a clearer, truer idea of what’s happening with mortgage rates, housing inventory, and home prices in your market, talk to a trusted real estate professional.

Connect with a local real estate agent so you have an expert who can give you the real story on your local housing market.

Top 10 Best Housing Markets for First-Time Home Buyers This Spring

For many hopeful buyers, purchasing a first home has lately felt less like a goal and more like a long shot.

Not because you weren’t financially responsible. Not because you weren’t ready to make a move. But because, every time you checked the numbers, homeownership still didn’t feel realistic.

That’s why so many first-time buyers have put their plans on hold.

Now, after years of watching from the sidelines, this spring may finally bring new opportunities. Especially in certain housing markets where affordability and inventory are starting to improve.

The 10 Best Markets for First-Time Buyers

Zillow recently released its list of the top 50 metro areas for first-time home buyers this spring, and the top 10 housing markets stand out for good reason.

Here are Zillow’s top 10 best markets for new buyers in 2026:

- Jacksonville, FL

- Birmingham, AL

- San Antonio, TX

- Atlanta, GA

- Houston, TX

- St. Louis, MO

- Detroit, MI

- Raleigh, NC

- Baltimore, MD

- Louisville, KY

In these higher-ranked metros, Zillow says median-income households can afford 68% of all homes currently for sale.

This is a major shift, and one that could give buyers real options in some areas.

Not long ago, many buyers felt lucky to find even a few homes within reach. Today, in some markets, there are finally more realistic options for first-time buyers trying to break into the market.

What Makes These Housing Markets Stand Out?

These markets aren’t becoming more favorable for any single reason. Rather, several smaller trends are beginning to work together.

As Orphe Divounguy, Senior Economist at Zillow, explains:

“First-time buyers are finally seeing some light at the end of the tunnel. Affordability is still a challenge, but rising incomes, stabilizing prices and improving inventory are creating real opportunities in parts of the country. In the strongest markets for first-time buyers, they’ll find more choices, less competition and a clearer path to homeownership than they’ve had in years.”

That shift comes down to three key factors:

1. More Homes Are Coming to Market

According to Realtor.com, housing inventory is up 8.1% compared to last year.

More homes for sale means buyers have more choices. It can also reduce the pressure that comes with low-inventory markets, where bidding wars and quick decisions often make it harder for new buyers to compete.

2. Home Price Growth Is Slowing

While affordability is still a challenge in many areas, home prices aren’t rising as quickly as they were in recent years.

Slower price growth can help keep more homes within reach, and in some markets, prices may even be easing enough to bring new neighborhoods back into play.

3. Incomes Are Rising

Wage growth is also helping improve the picture for buyers.

When household income increases, it can offset part of the affordability challenge, even when mortgage rates remain elevated. As Mark Fleming, Chief Economist at First American, explains:

“Income growth has outpaced house price growth for 19 straight months, boosting house-buying power even as mortgage rates remain elevated.”

Taken together, these trends are creating better conditions for new buyers in select markets across the country.

What If Your Market Didn’t Make the List?

If your city did not make Zillow’s top 10, or even the top 50, there’s no reason to worry. You’re not out of options.

Opportunities exist in any market. The key is knowing where to look and having the right guidance along the way.

Even within the same metro area, one buyer’s experience can be very different from another’s. A lot depends on local knowledge and strategy. The right real estate agent can help you identify overlooked opportunities, such as:

- Neighborhoods where prices have not climbed as fast.

- Areas with more available inventory.

- New construction communities offering builder incentives.

These kinds of opportunities may not make national headlines, but they can make a meaningful difference when trying to buy your first home.

Bottom Line: More Options for First-Time Home Buyers

For a long time, first-time home buyers have felt stuck, waiting for the market to shift in their favor.

This spring, that may finally be happening in certain markets.

With more inventory, slower price growth, and rising incomes, buying a first home may feel more realistic than it has in years. And even if your market isn’t on Zillow’s list, there may still be neighborhoods or communities nearby offering a better chance to get started.

If you want to find out where those opportunities exist in your local market, connect with a trusted real estate agent who knows where to look.