Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

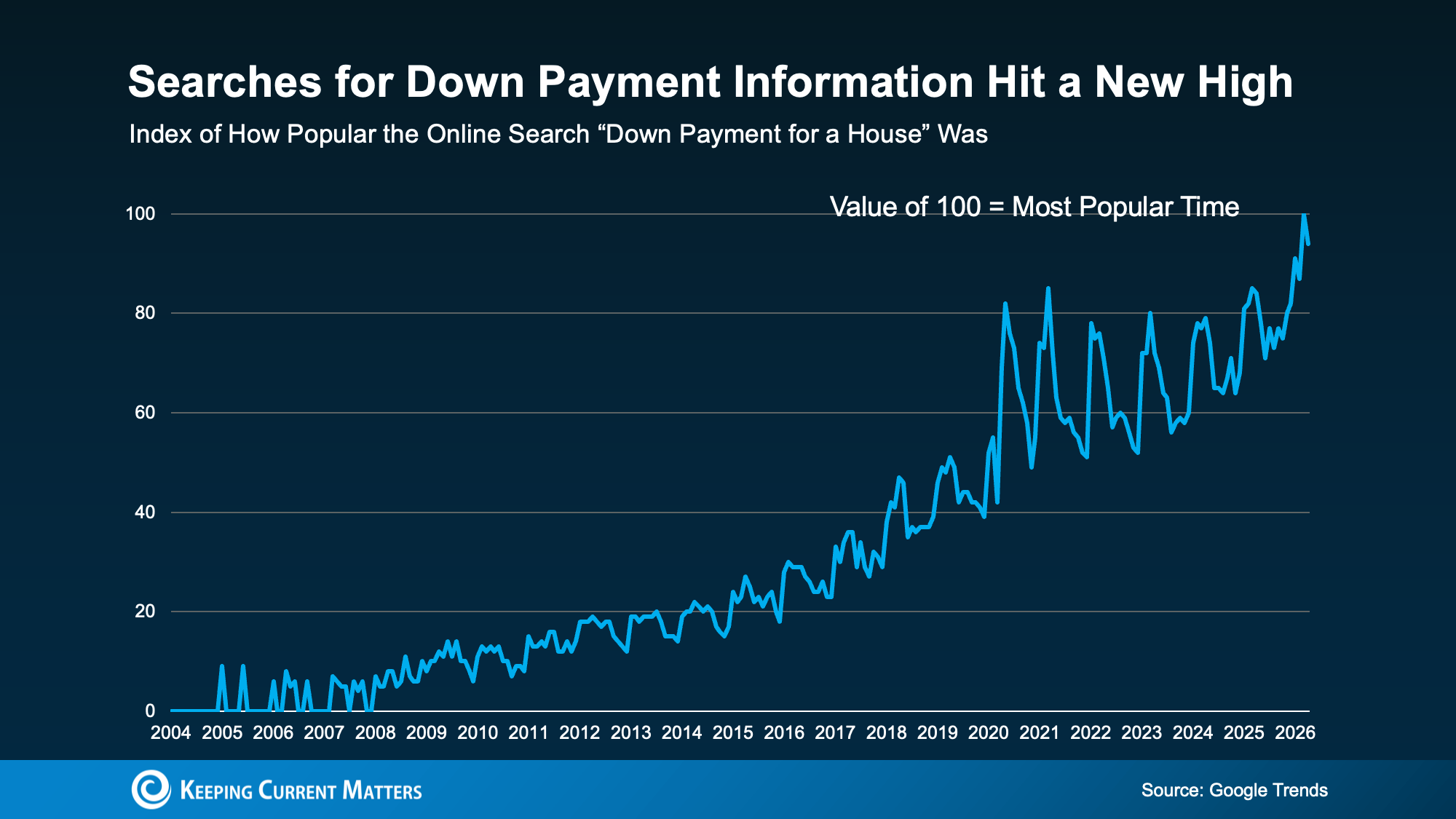

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

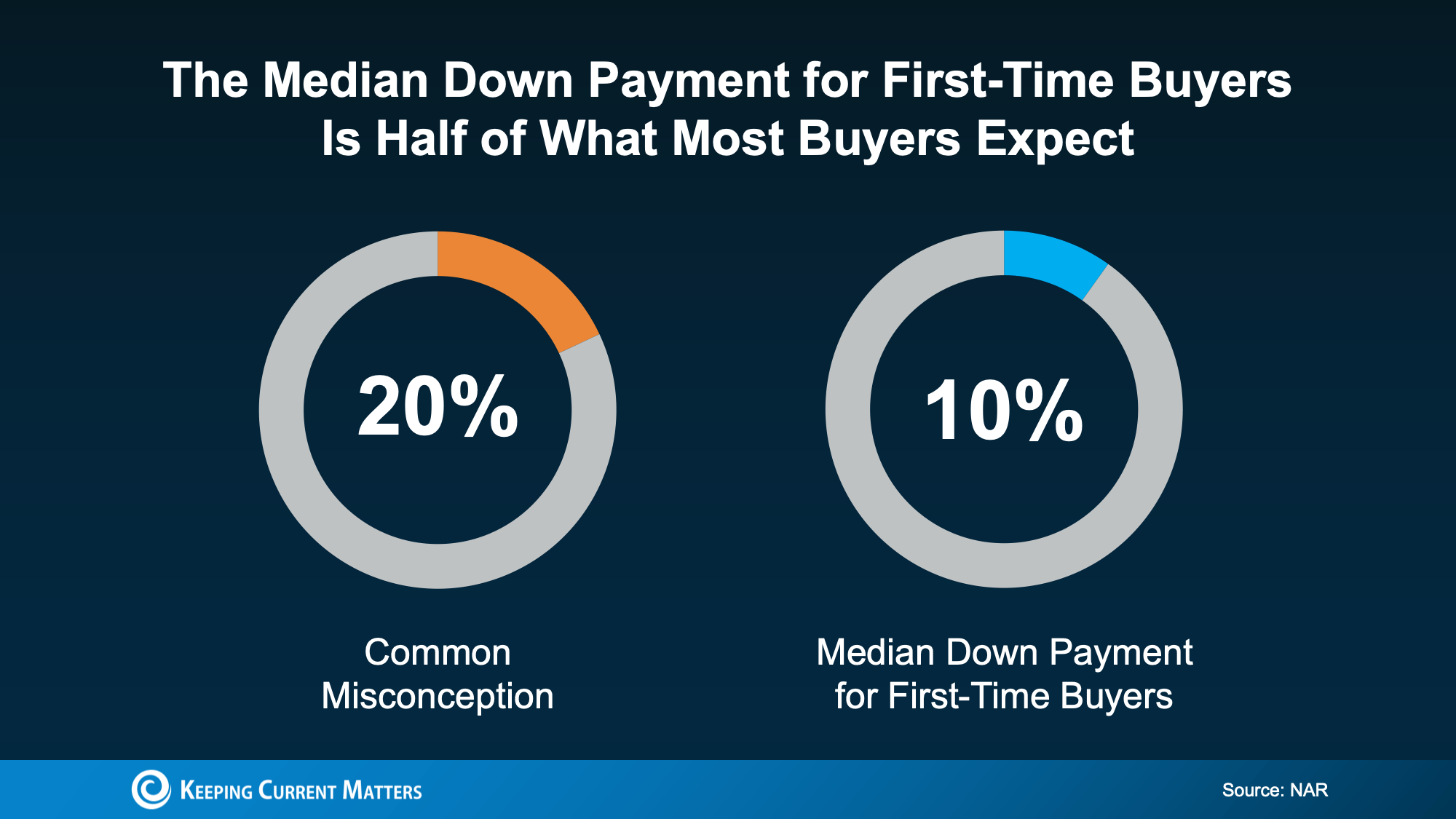

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

Is an Adjustable-Rate Mortgage Right for You? A Homebuyer’s Guide

If you’ve been shopping for a home lately, you’ve likely felt the pressure of today’s affordability challenges. Higher home prices and mortgage rates have made it harder for many buyers to stay within budget. That’s one reason adjustable-rate mortgages, or ARMs, are getting more attention again.

For some homebuyers, an ARM can offer welcome savings upfront. But before you go that route, it’s important to understand how these loans work, why they appeal to certain buyers, and what the long-term risks might be.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage is a home loan that starts with a fixed interest rate for a set number of years. After that initial period ends, the rate can adjust at scheduled intervals based on market conditions.

As Business Insider explains:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

That’s the biggest difference between a fixed-rate mortgage and an ARM. A fixed-rate loan offers predictability, while an ARM may give you a lower payment at first but less certainty later.

It’s true that costs like property taxes and homeowners insurance can still change with a fixed-rate mortgage. But the principal and interest portion of the payment generally stays steady. With an ARM, your monthly payment can rise or fall once the fixed period ends.

Why More Home Buyers Are Considering ARMs

The main reason buyers look at adjustable-rate mortgages is simple: lower initial costs.

Business Insider puts it this way:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

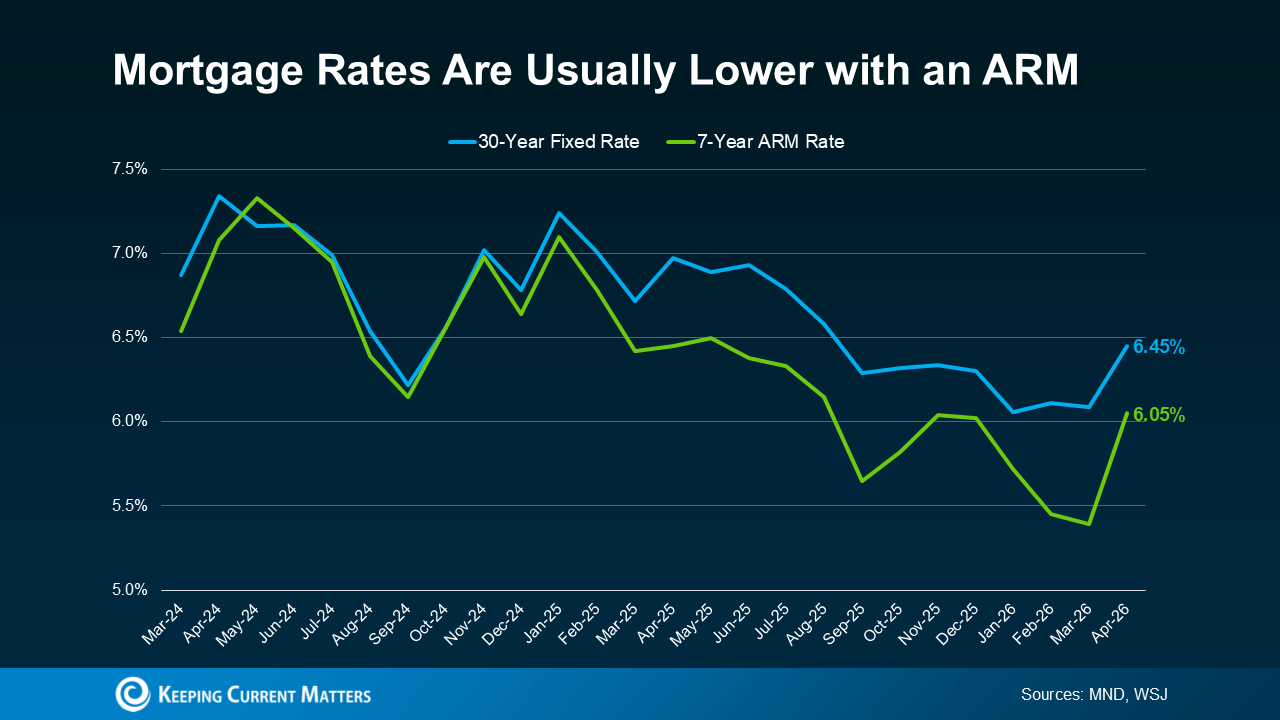

That upfront savings can matter, especially in a market where every dollar counts. Recent reporting from Mortgage News Daily and The Wall Street Journal show that ARM rates have been coming in lower than 30-year fixed mortgage rates.

For many buyers, even modest monthly savings can make a difference. For example, Redfin found that a typical buyer could save about $150 per month by choosing an ARM instead of a 30-year fixed mortgage. Savings like that can help some buyers qualify for a home sooner or make their monthly budget more manageable.

Why Adjustable-Rate Mortgages Are Making a Comeback

More homebuyers are deciding that a lower payment today is worth considering, even if it means taking on more uncertainty later.

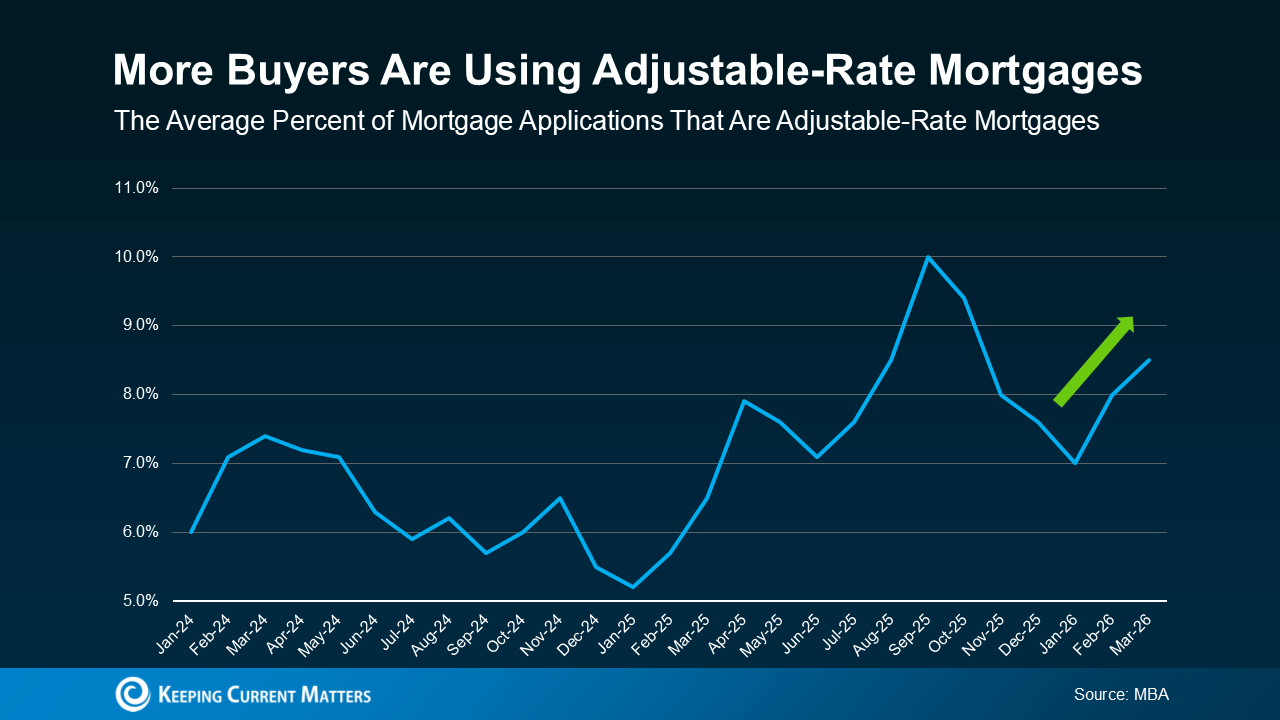

Recent reports from the Mortgage Bankers Association (MBA) show that the share of buyers choosing ARMs has increased in recent years. That doesn’t mean ARMs are becoming the right fit for everyone. But, it shows that some buyers are using them as a strategy to deal with affordability challenges in the current market.

For anyone who remembers the 2008 housing crash, this trend may sound concerning at first. But today’s lending environment is very different.

In the past, some borrowers were approved for loans they couldn’t realistically afford once the interest rate adjusted. Today, lending standards are tighter, and lenders generally evaluate whether borrowers could still manage the payment if rates rise. So while ARMs are becoming more common again, that alone doesn’t point to another housing crisis.

The Pros and Risks of an ARM

An adjustable-rate mortgage can make sense in the right situation, but it depends on your financial plan and your comfort with risk.

An ARM may be worth considering if:

- You expect to move before the rate adjusts.

- You believe your income will increase over time.

- You need a lower initial payment to make homeownership possible now.

Still, there are trade-offs to consider.

Once the fixed-rate period ends, your interest rate can change, and your monthly payment could increase significantly depending on where mortgage rates are at that point. There’s also no guarantee rates will fall in the future, which means refinancing later may not be as easy or as beneficial as some buyers hope.

That’s why it’s important to think beyond the introductory rate. Make sure you understand how long the fixed period lasts, how often the rate can adjust, and how much your payment could increase over time. Most importantly, talk through your options with a trusted lender and financial advisor before making a decision.

Bottom Line: Is an ARM Right for You?

Adjustable-rate mortgages are regaining popularity because they can make buying a home more affordable in the short term. For some buyers, that lower upfront payment can be a helpful tool. But an ARM isn’t necessarily the right move for everyone.

The best decision comes down to understanding how the loan works, weighing the risks, and making sure it fits your long-term goals.

If you’re considering an adjustable-rate mortgage yourself but are still on the fence, reach out to us today. We can connect you with a qualified lender in your area who explore your options with you.

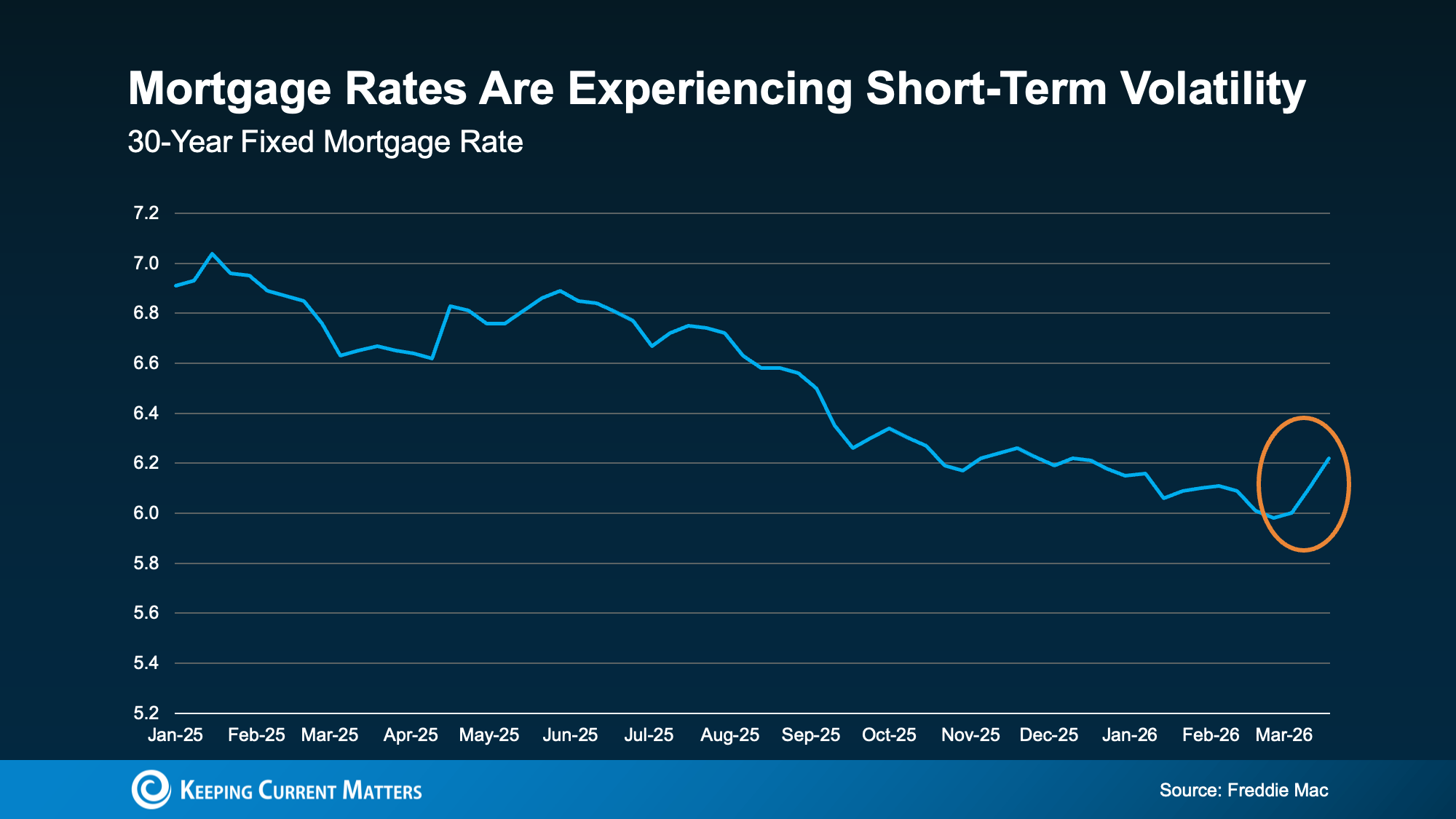

Mortgage Rate Volatility: What You Can Control as a Buyer

Mortgage rates have been moving up and down lately, and that can make buying a home feel harder to plan for. When rates are unpredictable, many buyers wonder whether they should wait, move forward, or try to time the market.

Here’s the good news: while you can’t control where mortgage rates go next, you can control several factors that may help you secure a better rate. The first step is understanding what’s driving today’s market and knowing where to focus your time and effort.

Mortgage Rate Volatility Is Normal

Recent data from Freddie Mac show that mortgage rates have been fluctuating. After trending downward for well over a year, rates ticked up again this month.

That kind of movement can feel frustrating, especially when you’re doing your best to budget for a home purchase. But occasional increases and decreases are a normal part of the mortgage market. Even over the past year, there have been periods when rates jumped before settling back down.

This is another one of those moments, and it helps to keep that in mind.

When there’s economic uncertainty or major global events unfolding, mortgage rates often respond quickly. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

That’s exactly why trying to predict the perfect time to buy usually doesn’t pay off. Rates can change fast, and waiting for the market to cooperate may not give you the outcome you want.

Focus on What You Can Control

You may not be able to influence the market, but you can take steps put yourself in a better position as a buyer. If your goal is to get the best mortgage rate possible, these are the areas that matter most.

Your Credit Score

Your credit score is one of the biggest factors that affects the rate you qualify for. In many cases, even a modest improvement in your score can lead to better loan terms and a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That’s why it’s worth taking steps to strengthen your credit before applying for a mortgage. Paying bills on time, reducing outstanding debt, and avoiding new credit inquiries can all help. If you’re not sure where your score stands or what improvements would make the biggest difference, a trusted loan officer can help you create a plan.

Your Loan Type

The type of mortgage you choose also affects your rate. There are many different types of loans, and each comes with different eligibility requirements, benefits, and pricing.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why exploring your mortgage options is so important. A conventional loan may be the right fit for one buyer, while an FHA, USDA, or VA loan may offer better advantages for another. Comparing programs and speaking with more than one lender can help you understand which path makes the most sense for your financial situation.

Your Loan Term

The length of your loan term matters, too. Most lenders offer 15-year, 20-year, and 30-year mortgage options, and the term you choose can affect both your interest rate and your monthly payment.

Freddie Mac explains it this way:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A shorter loan term may come with a lower interest rate, but the monthly payment is often higher. A longer term may give you more flexibility in your monthly budget, even if you pay more interest over time. The right choice depends on your goals, your budget, and how long you plan to stay in the home.

Conclusion

If you’re in the market for a home right now, the best strategy is not to focus on trying to predict where mortgage rates will go next.

Instead, focus on what you can control. Improve your credit score, explore different loan types, and choose a loan term that fits your needs. Most importantly, work with a trusted lender who can guide you through your options. If you need help connecting with trustworthy lender, reach out to us today.

Mortgage rates may be out of your hands, but the steps you take to prepare are not. And when you focus on what you can change, you give yourself a much better chance to move forward with confidence.

Renting vs. Buying: What The Numbers Say

Renting often feels like the simpler move these days. There’s no down payment to save up for, no surprise repair bills, and no long-term commitment if life changes.

But then your lease renews and the rent jumps. Then it happens again. Eventually, what felt flexible suddenly starts to feel expensive, especially when you realize every monthly payment is going to your landlord, not building wealth for you.

A big reason this stings is because there’s been so much talk about how homeownership is “out of reach.” And in some markets, it absolutely can be. But here’s the part that doesn’t get said enough: when you compare the numbers side by side, buying can cost less per month than renting in more places than most people expect.

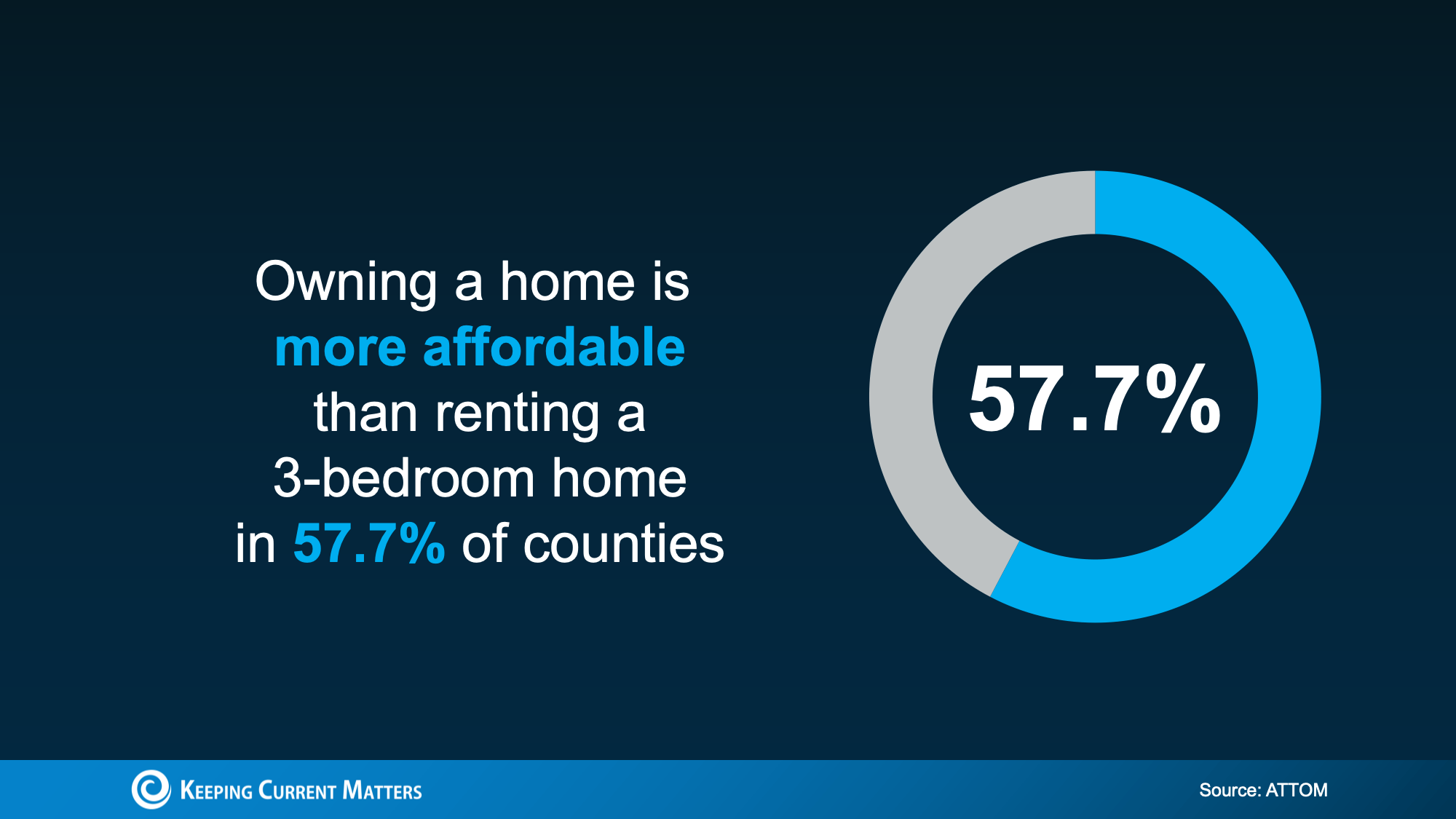

Buying Can Be More Affordable Than Renting in Many Areas

In a lot of markets today, owning a home may actually have a lower monthly cost than renting a 3-bedroom home. New data from ATTOM suggest this is true in nearly 58% of counties across the United States.

And this comparison isn’t just a mortgage payment versus rent. It also takes into account common ownership costs like insurance and regular maintenance.

So if you’ve assumed buying automatically means a higher monthly bill, it may be worth a second look. Recent changes in home price growth, housing inventory, and mortgage rates have been shaking certain markets. Depending on where you live, buying might be finally in your favor.

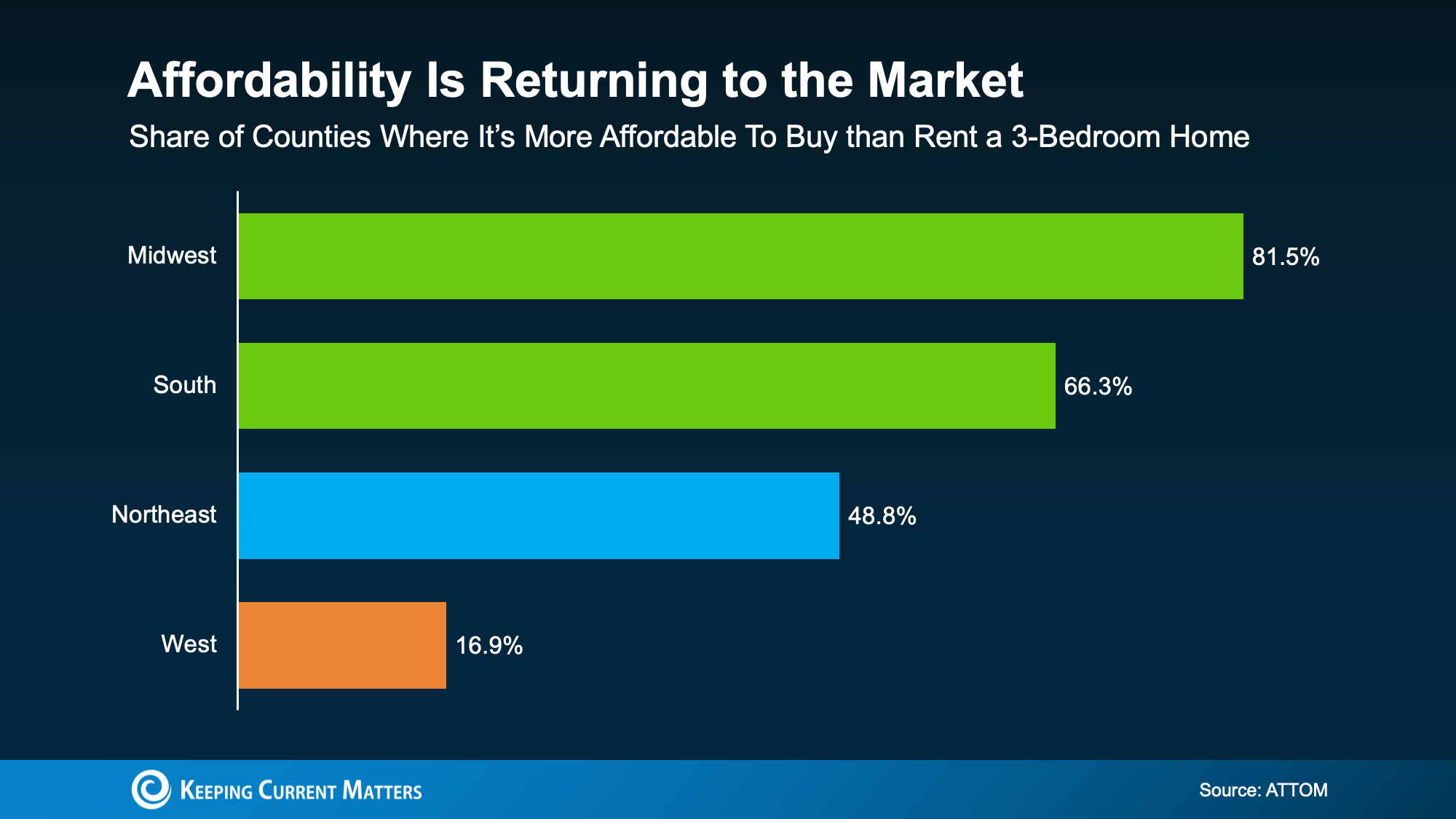

Affordability Depends on Where You Live

Even though the national picture has shifted, it doesn’t mean buying is cheaper everywhere, or that every renter will have the same experience.

That “nearly 58%” figure looks very different depending on the region. The biggest improvement is happening in the Midwest and South, while the West can still feel tight for many households.

The key takeaway is simple: real estate is local. A national headline can’t tell you what the rent-versus-buy equation looks like in your zip code. The only way to know is to run the numbers based on your local prices, rents, taxes, and insurance.

What’s Still Holding Buyers Back?

If you’re thinking, “Even if the monthly payment works, I can’t afford the upfront costs,” you’re not alone.

For many renters, the biggest hurdle isn’t the monthly payment. It’s the down payment (and often closing costs) that feels like a wall.

Here’s the good news: there are thousands of down payment assistance programs across the country, and many buyers qualify without realizing it. The average benefit is around $18,000, which can help cover part of your down payment or closing costs.

Support like this can make buying feel a lot more realistic, because it reduces how much cash you need to get in the door.

How to Figure Out What’s Right for You

If you want clarity instead of guesswork, focus on a simple comparison:

- Your current rent (and how often it’s rising).

- An estimated monthly ownership cost (mortgage, taxes, insurance, HOA if applicable).

- A realistic maintenance cushion.

- Upfront costs (and any down payment assistance you may qualify for).

When you combine potential assistance with monthly costs that may be closer than expected, the gap between renting and buying can shrink quickly, or even flip in favor of buying.

Conclusion

The bottom line isn’t that everyone should buy a home as soon as possible.

The idea is that renting isn’t always the cheaper option people assume it is, and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feel stuck saying “someday”, consider a quick conversation with a local real estate agent or lender. Not a commitment, just a way to see what’s possible and whether it makes sense for you.

Renting vs. Buying: Which Home Option Is Right for You?

Between stubborn mortgage rates and rising home prices, you’ve probably mulled over renting vs. buying a home. In market conditions like these, renting and waiting to buy can feel like your only realistic option. This can be the truth in many cases, and buying before you’re ready can be a costly mistake.

But the short-term savings of renting can sometimes trap you in a cycle, preventing you from making wealth-building investments. Over time, this can actually end up costing you more than buying a home early and slowly building equity. Unsurprisingly, a recent survey from Bank of America found that 70% of prospective homebuyers feel renting could hinder their financial future.

Ultimately, the pros and cons of renting and buying come down to your own short-term and long-term financial goals. If you’re feeling torn over whether you should nest or invest, take these major differences into account to decide.

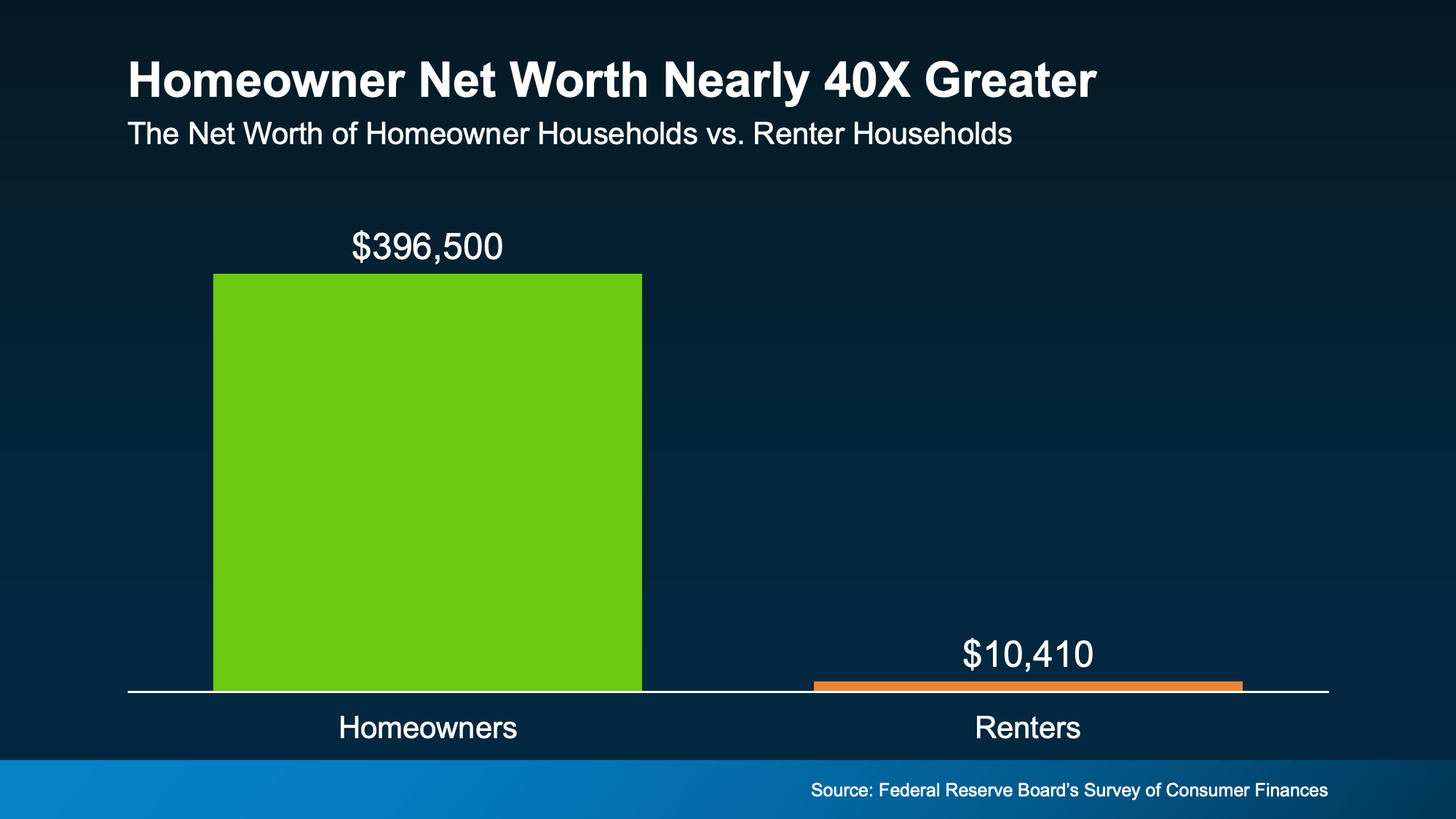

Homeownership Builds Your Wealth Over Time

Apart from giving you your own place to live, homeownership grants the important bonus of building your wealth over time. This is because home prices usually rise as time goes on, meaning waiting longer to buy costs you more. This isn’t always true of every housing market, but the general national trend tends to speak for itself.

The average home sale price has more than tripled in the past 30 years.

Even better, your home equity also grows over time when you’re a homeowner. Equity is the difference between what your home is worth and what you still owe on your mortgage. Your equity grows with each mortgage payment you make, and this builds your net worth over time.

According to the Federal Reserve, the average homeowner’s net worth is nearly 40 times greater than that of a renter. That’s a life-changing difference, and seeing it represented visually really drives the point home.

The average net worth of a homeowner household is almost 40X greater than that of a renter household.

This massive difference in personal wealth is just one of the reasons that Forbes says:

“While renting might seem like [the] less stressful option . . . owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

Renting Helps You Save in the Short Term

Compared to homeownership, renting offers lower monthly payments and the freedoms of relatively negligible commitment and responsibility. This often makes renting feel like the safer option, and it usually is, at least in the short term. But in the long term, renting can land you in a trap that prevents you from building real wealth.

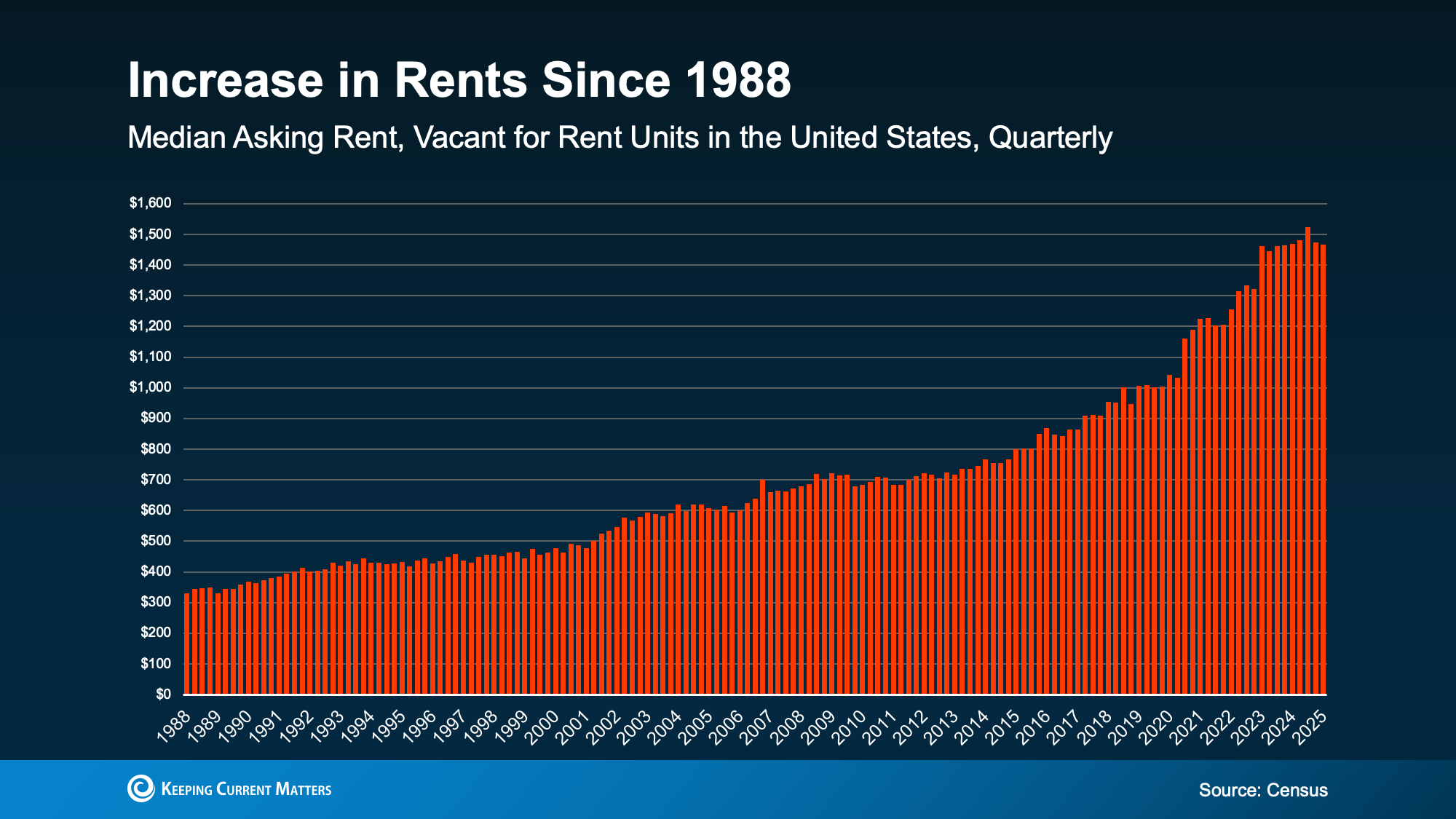

Rent tends to rise along with home prices, and this has been true for decades. Rental costs have been somewhat stable recently, but they almost never trend downward. This trap of paying increasing rent without building wealth can make buying a home feel impossible.

Like home prices, rental costs have risen dramatically in the past several years.

Financial uncertainty like this can have a real, lasting impact on any of your financial decisions. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

Rent money doesn’t come back to you, and that means it doesn’t grow your wealth. The only mortgage it’s paying is your landlord’s.

So, whether you’re renting or owning, you’re paying off a mortgage. The question is: whose mortgage do you want to pay?

Renting vs. Buying: What Really Matters

Here’s another way to look at renting vs. buying. Rent money is gone once you pay it. Payments toward your own house build equity, like a savings account you can live in. Obviously, buying comes with higher upfront costs and more long-term responsibility. But the reward is a stable investment that grows over time. And while buying a home often feels out of reach, a solid plan can get you there.

As Realtor.com Senior Economist Joel Berner explains:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

Conclusion

Renting may be cheaper in the short term, but it can cost you more over time without building your wealth. If you’re weighing the pros and cons of renting vs. buying, consider your long-term financial goals. Short-term saving can trap you in an endless cycle of renting, but buying without planning can be financially overwhelming.

If you’re ready to make the leap from renting into buying a home, contact us today. We’d be happy to connect you with a local agent who can make your dreams a reality.

Should You Buy a Home This Spring or Wait for Lower Prices?

You’re probably familiar with the saying “The best time to plant a tree was yesterday, but the next best time is today.” It’s a valuable lesson about future planning and investment that, surprisingly, applies to the decision to buy a home too.

Even though buying a home is a major financial expense, it’s also a major investment that grows over time. As the price of your home increases over time, the value of the equity you’ve built grows with it. And while waiting for prices to drop may be an attractive option, trying to time the market rarely works.

But here’s something to consider: the longer you wait to buy a home, the more your patience could cost you. Let’s explain why.

Home Prices Are Expected To Continue Climbing

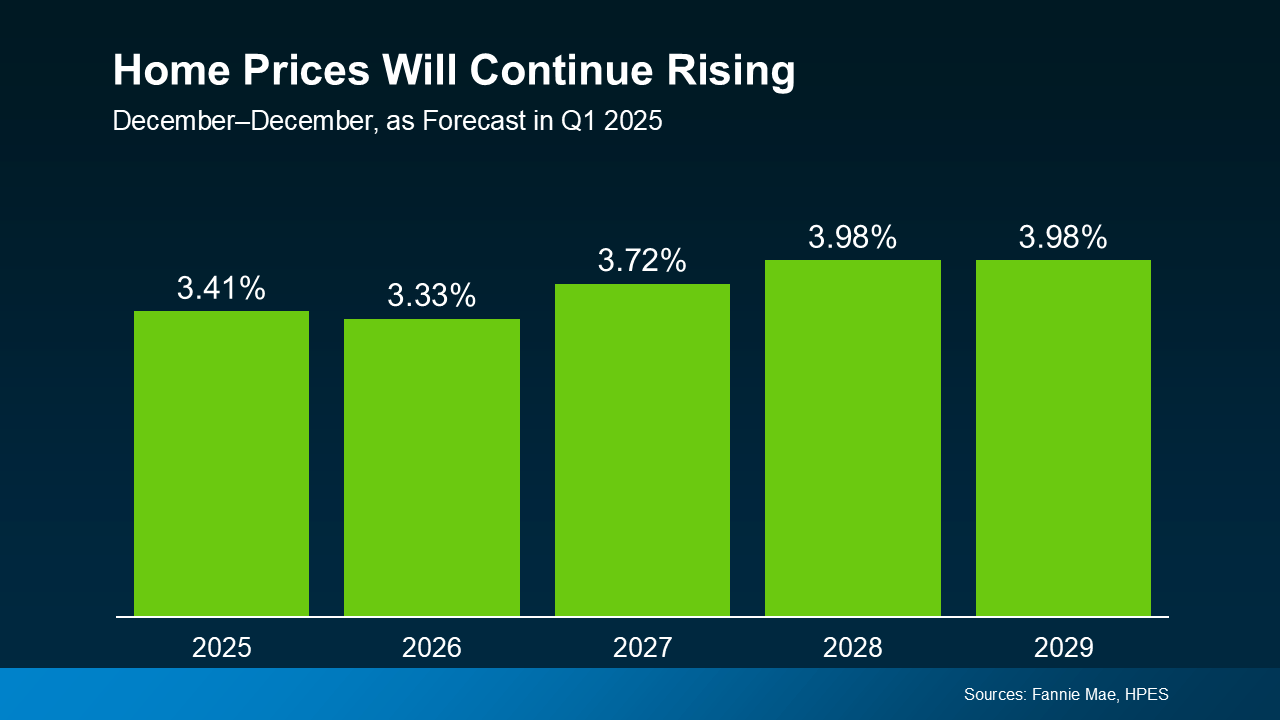

Each quarter, over 100 housing market experts respond to Fannie Mae‘s Home Price Expectations Survey (HPES). Consistently, the survey results show experts agreeing that home prices will continue to rise through 2029 or even longer.

Sharp price increases may be behind us, but experts predict steadier, healthier increases of 3-4% per year moving forward. This rate of increase will vary by market from year to year, but it’s much closer to normal. Reliable growth is a promising sign for hopeful buyers, and the housing market at large, as the graph below demonstrates.

Even in markets experiencing slower price growth or short-term decreases, the steady gains of homeownership eventually win in time. After all, a growing, long-term financial investment will always beat a one-time discount.

Here are the main points to remember:

- Home prices will be higher next year. Experts don’t expect home prices to fall any time soon, at least at the national level.

- Waiting for a perfect mortgage rate or price drops is a gamble. With only slight dips in mortgage rates expected in the near future, price increase could outpace any potential mortgage savings. Unless home price growth is slow or mortgage rates are low in your area, waiting will likely be more expensive.

- Buying early means building more equity. When you invest in homeownership early, your equity and appreciating home value reward you in the long run.

The Costs of Waiting To Buy

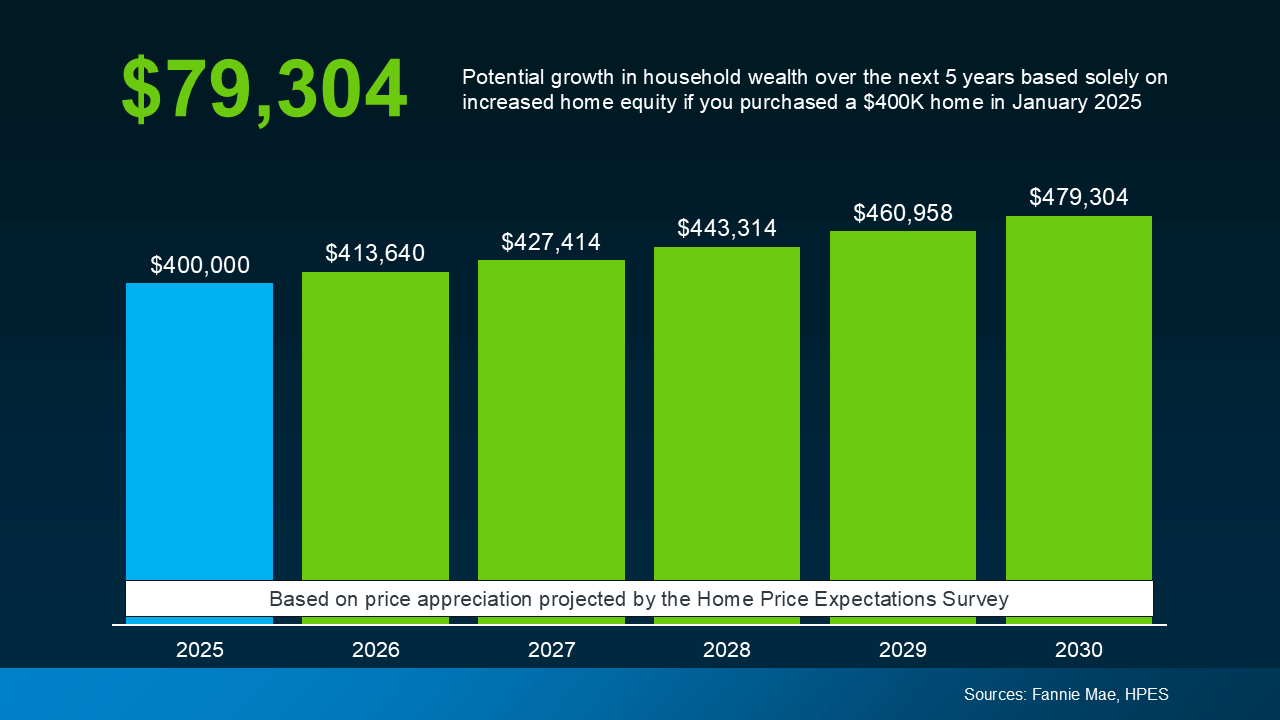

To demonstrate how these theories play out in real-world numbers, here’s a typical example. If you were to buy a $400,000 house in 2025, it could gain almost $80,000 in value by 2030. The graph below demonstrates how this value appreciates year by year based on the expert data we mentioned earlier.

This can be a considerable difference in your future wealth and why buyers who invest early are often glad they did. When it comes to building wealth through long-term investment, time in the market matters.

The question to consider isn’t “Should I wait to buy?” It’s really “Can I afford to buy now?” Just like planting a tree, making short-term sacrifices to buy a home will eventually pay off in the long-term.

Between rising prices and stubborn mortgage rates, today’s housing market is challenging, but achieving homeownership is far from impossible. Exploring different neighborhoods, seeking alternative financing options, or applying for down payment assistance programs can all make a critical difference.

What’s most important is acting decisively when you’re able to, instead of waiting for a perfect opportunity that never comes.

Conclusion

If you’re interested in buying but still undecided, take the time you need to make the right choice. But, remember that realizing an investment takes time, and the sooner you make one, the sooner you’ll be rewarded.

If you’re curious about what’s happening with prices in our local area, then reach out to us. Even if you’re not ready to buy, an expert local agent can fill you in with the info you need.

It’s Tax Day – Here’s How a Refund Can Help You Save For a Home

If you’ve been planning to buy a house, you know how hard it can be to save for a home. What you might not know is that your tax return can be a helpful boost to your savings and budget. According to a recent post by Freddie Mac:

“ . . . your tax refund from the IRS can be a useful supplement to your homebuying budget.”

So if you’re planning to get a tax refund this year, consider the difference that extra funding can make. A refund can help you pay for the upfront costs of homebuying, like a down payment or closing costs. And, according to the IRS, your tax refund may even help you out this year more than ever.

How a Tax Return Can Help You Buy a Home in 2025

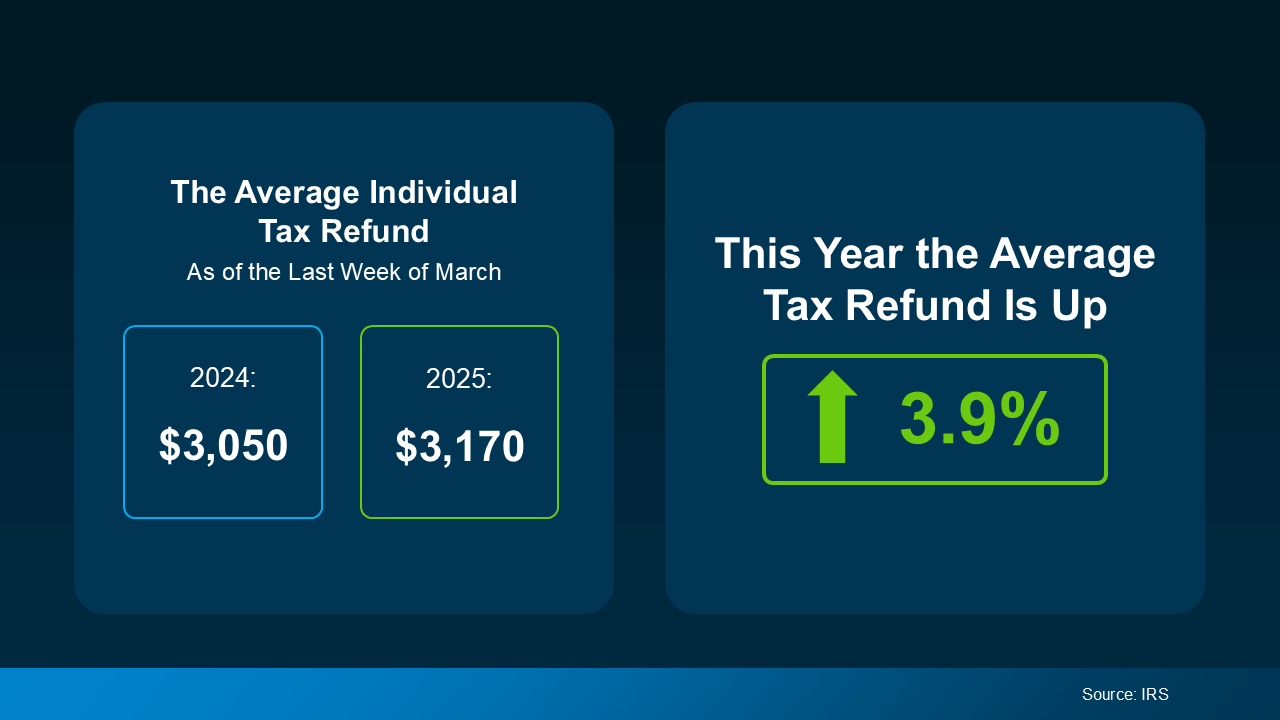

Recent data from the Internal Revenue Service (IRS) has found that the average individual’s refund is 3.9% higher this year. And while that’s not a huge increase, it can make a big difference if you’ve been struggling to save. The graphic below visualizes the new IRS data, comparing the average tax return in March 2024 to March 2025.

Your own personal tax refund will likely vary, but any financial boost helps when you’re saving for a home. According to Freddie Mac, the following are several ways you can put your tax return to good use when homebuying:

- Saving for a down payment – A down payment on a home is often one of the biggest obstacles to homeownership that buyers face. Saving your tax refund for a down payment can be a smart way to make this major step easier. Keep in mind while a 20% down payment may be common, it’s not typically a hard requirement to buy.

- Paying for closing costs – Usually due at closing, closing costs include fees for services like the appraisal, title insurance, and underwriting of your loan. While these vary by state, they’re often between 2% and 6% of your home’s total final purchase price. As a much lower percentage of your home’s price, closing costs can be a great use of your yearly refund..

- Lowering your mortgage rate – Lenders sometimes give buyers the option to buy down their mortgage rate if they qualify. This allows buyers to pay an upfront fee to lower their initial mortgage rate, reducing monthly payments in the short-term. This option can be particularly helpful if interest rates and mortgage payments are a major homebuying hurdle you’re facing..

Financially speaking, this may be more complicated in practice, but there’s no need to do it all on your own. Working with an experienced, trustworthy real estate professional can simplify your financial planning, helping you reach the best decision possible. An agent who understands the homebuying process, your unique financial needs, and your personal goals can make all the difference.

Conclusion

If you’ve been saving for a home, you already know well that every penny counts. Your tax return probably won’t be the final financial boost you need, but there are ways to use it effectively. Planning and identifying how to best spend that money can give you a real, meaningful step toward buying your home.

Are you eager to buy a home but having trouble making things work? Contact us today. We can connect you with local lenders and agents to help make your dream of homeownership a reality.