Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Renting often feels like the simpler move these days. There’s no down payment to save up for, no surprise repair bills, and no long-term commitment if life changes.

But then your lease renews and the rent jumps. Then it happens again. Eventually, what felt flexible suddenly starts to feel expensive, especially when you realize every monthly payment is going to your landlord, not building wealth for you.

A big reason this stings is because there’s been so much talk about how homeownership is “out of reach.” And in some markets, it absolutely can be. But here’s the part that doesn’t get said enough: when you compare the numbers side by side, buying can cost less per month than renting in more places than most people expect.

Buying Can Be More Affordable Than Renting in Many Areas

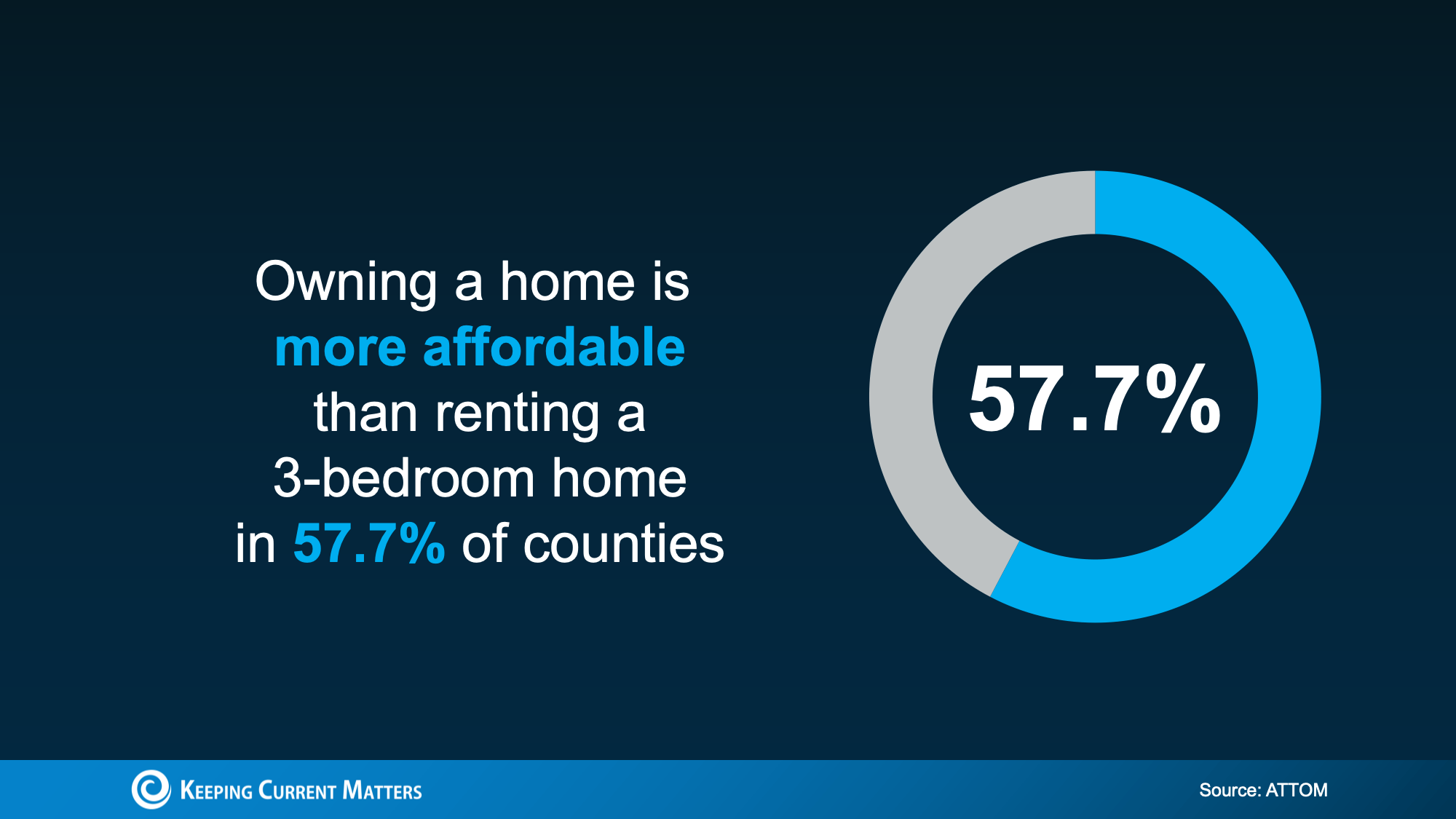

In a lot of markets today, owning a home may actually have a lower monthly cost than renting a 3-bedroom home. New data from ATTOM suggest this is true in nearly 58% of counties across the United States.

And this comparison isn’t just a mortgage payment versus rent. It also takes into account common ownership costs like insurance and regular maintenance.

So if you’ve assumed buying automatically means a higher monthly bill, it may be worth a second look. Recent changes in home price growth, housing inventory, and mortgage rates have been shaking certain markets. Depending on where you live, buying might be finally in your favor.

Affordability Depends on Where You Live

Even though the national picture has shifted, it doesn’t mean buying is cheaper everywhere, or that every renter will have the same experience.

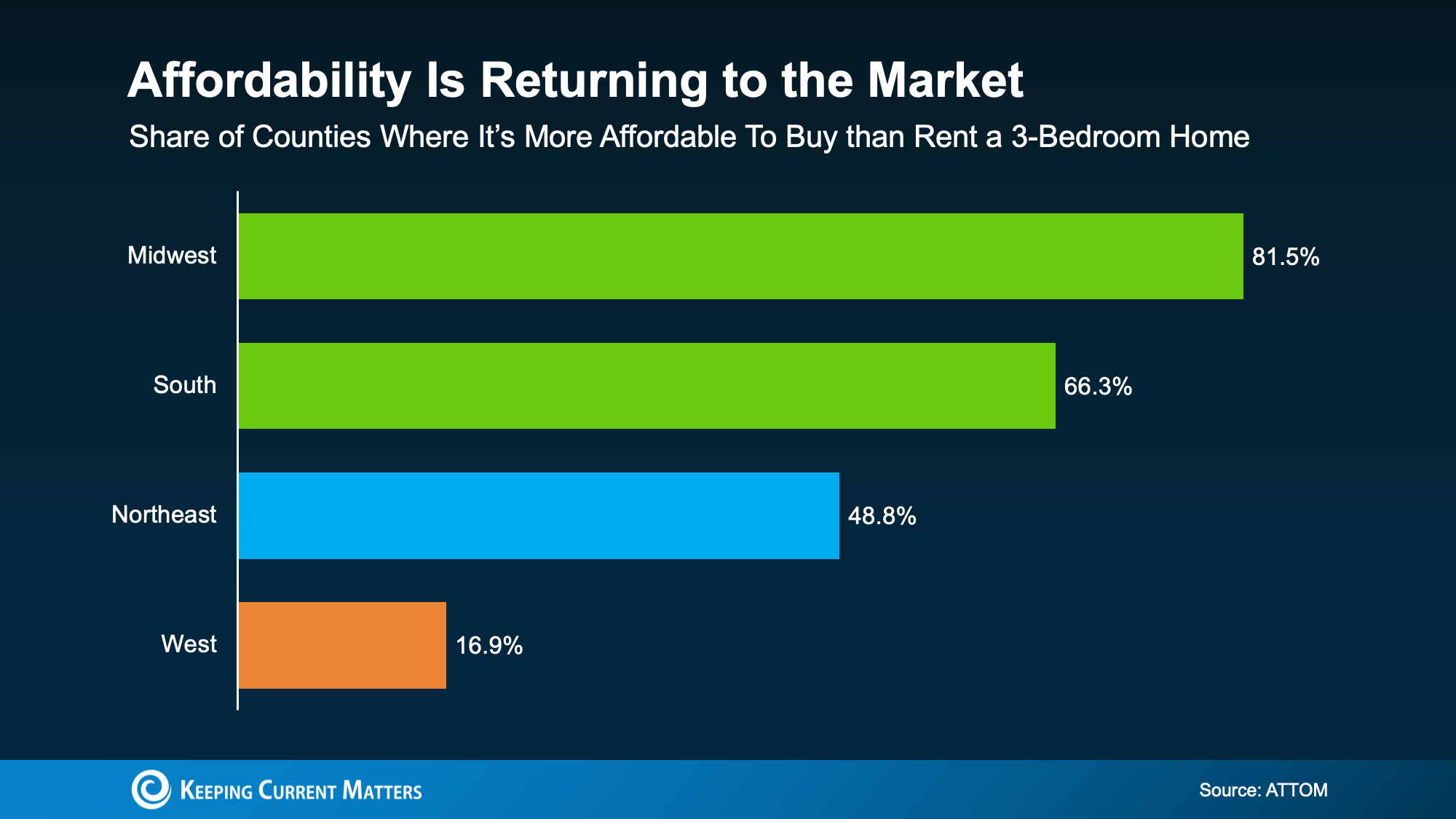

That “nearly 58%” figure looks very different depending on the region. The biggest improvement is happening in the Midwest and South, while the West can still feel tight for many households.

The key takeaway is simple: real estate is local. A national headline can’t tell you what the rent-versus-buy equation looks like in your zip code. The only way to know is to run the numbers based on your local prices, rents, taxes, and insurance.

What’s Still Holding Buyers Back?

If you’re thinking, “Even if the monthly payment works, I can’t afford the upfront costs,” you’re not alone.

For many renters, the biggest hurdle isn’t the monthly payment. It’s the down payment (and often closing costs) that feels like a wall.

Here’s the good news: there are thousands of down payment assistance programs across the country, and many buyers qualify without realizing it. The average benefit is around $18,000, which can help cover part of your down payment or closing costs.

Support like this can make buying feel a lot more realistic, because it reduces how much cash you need to get in the door.

How to Figure Out What’s Right for You

If you want clarity instead of guesswork, focus on a simple comparison:

- Your current rent (and how often it’s rising).

- An estimated monthly ownership cost (mortgage, taxes, insurance, HOA if applicable).

- A realistic maintenance cushion.

- Upfront costs (and any down payment assistance you may qualify for).

When you combine potential assistance with monthly costs that may be closer than expected, the gap between renting and buying can shrink quickly, or even flip in favor of buying.

Conclusion

The bottom line isn’t that everyone should buy a home as soon as possible.

The idea is that renting isn’t always the cheaper option people assume it is, and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feel stuck saying “someday”, consider a quick conversation with a local real estate agent or lender. Not a commitment, just a way to see what’s possible and whether it makes sense for you.