Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You’ve probably seen the headlines: foreclosures are on the rise. And if that immediately makes you think of the 2008 housing crash, you’re not alone.

For many homeowners and buyers, the word “foreclosure” brings back memories of the Great Recession, when distressed properties flooded the market and home values fell sharply. But today’s housing market is very different.

Yes, foreclosure activity has increased, but the bigger picture doesn’t point to a crash. Rather, it shows a market slowly shifting back to normal after several unusual years.

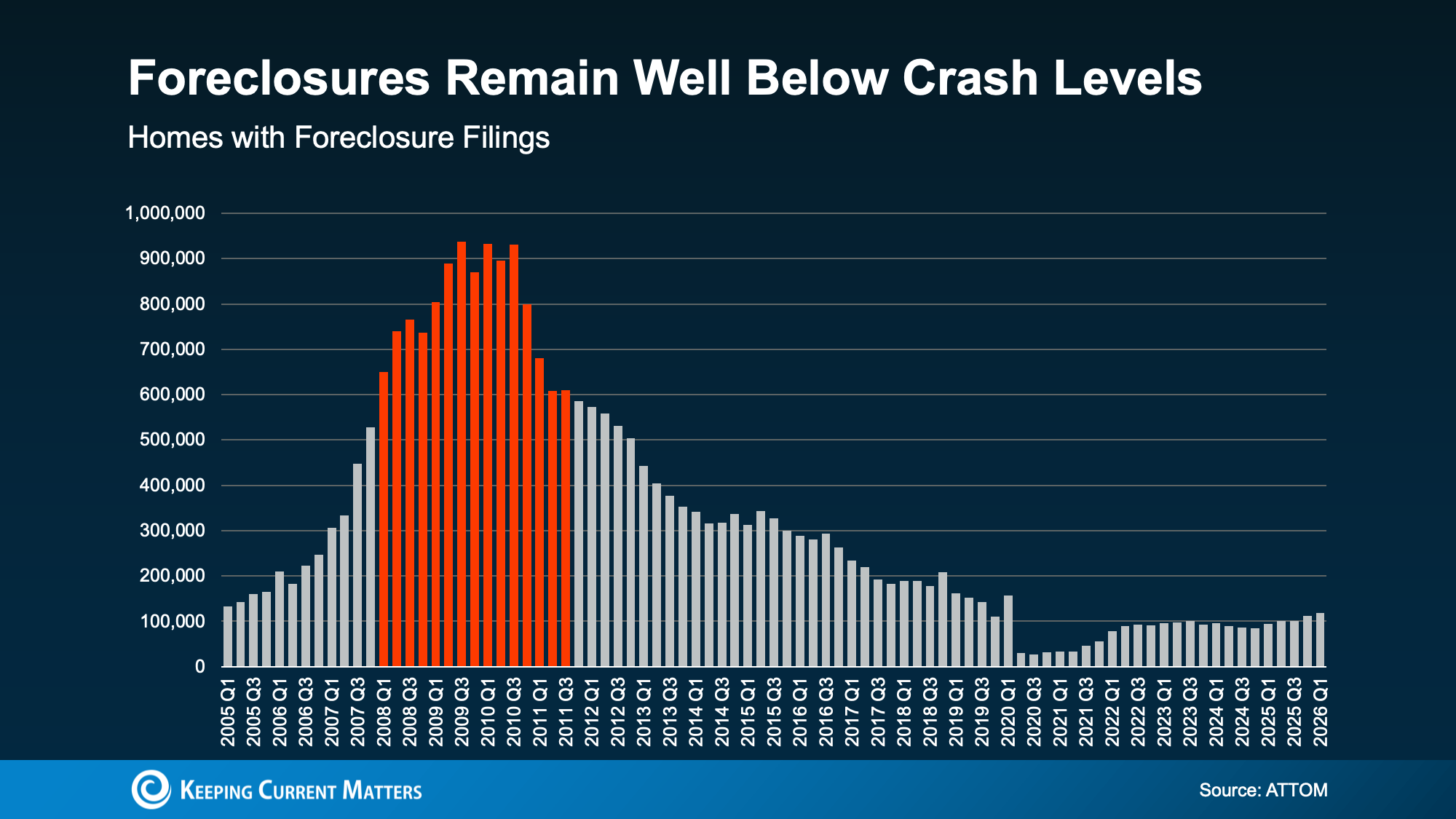

Foreclosures Are Rising, But Still Down Historically

According to data from ATTOM, foreclosure filings are up 26% compared to a year ago and have now increased for five straight quarters. That’s definitely worthy of attention, but it doesn’t mean the housing market is in trouble.

A clear perspective requires a bit of context.

Foreclosure numbers were unusually low in 2020 and 2021 because of pandemic-era protections, including the government’s foreclosure moratorium. Those were exceptional years with totally abnormal market conditions.

A better comparison is 2017, 2018, and 2019, which were the last few years before the pandemic disrupted the housing market. When you compare today’s foreclosure activity to those years, filings are still lower than pre-pandemic levels.

This shows the current increase in foreclosures is more about normalization than distress. The market isn’t returning to 2008 conditions: it’s slowly moving back toward a more typical level of activity.

And compared to the foreclosure wave during 2008 the housing crash, today’s numbers remain far, far lower.

Why Today Is Not Like 2008

One of the biggest differences between now and 2008 is homeowner equity.

During the last housing crash, many homeowners owed more on their mortgages than their homes were worth. That left them with few to no options. Selling often wasn’t possible because selling wouldn’t cover their remaining mortgage balance. For many people, foreclosure became the only path forward.

Today, most homeowners are in a much stronger position.

According to Cotality, the average homeowner has roughly $295,000 in home equity. Home equity like that creates options, even for someone who is struggling financially.

If a homeowner has enough equity to cover their mortgage balance and selling costs, they may be able to sell their home, pay off what they owe, protect their credit, and potentially walk away with money.

That’s a very different picture from 2008, and one that doesn’t point to foreclosures rising out of control.

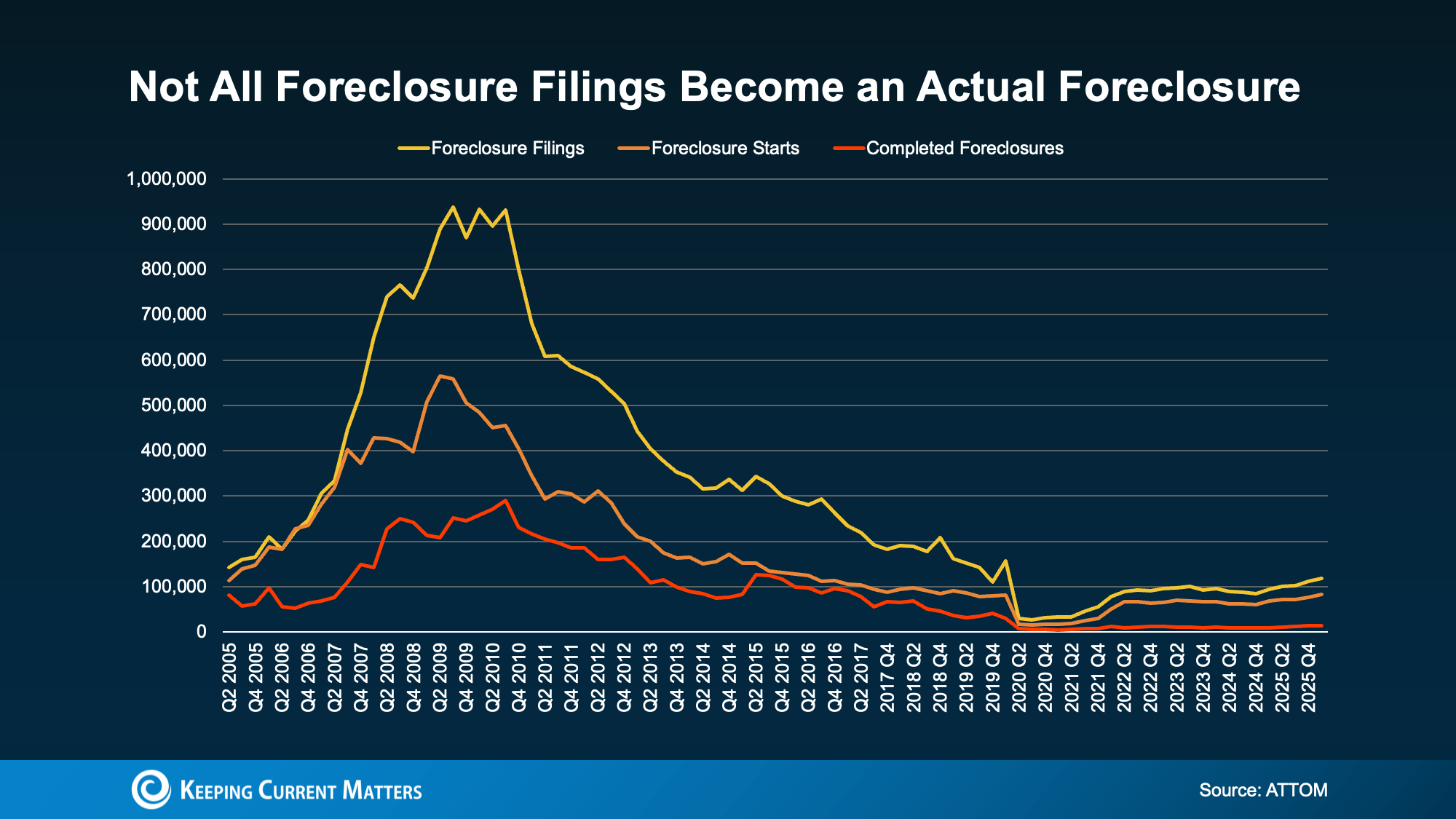

Foreclosure Filings Don’t Always Lead to Foreclosure

Another important point that often gets lost in the headlines is this: a foreclosure filing does not always mean someone loses their home.

Foreclosure filings only show that the process has started, but many homeowners find a solution before the process is completed. Some work out an agreement with their lender. Others sell their home before foreclosure is finalized. Some may qualify for loan modifications or other assistance.

That’s why completed foreclosures are typically much lower than total foreclosure filings.

According to ATTOM’s data, completed foreclosures have barely risen despite the jump in filings. The home equity that many homeowner’s have now is a huge reason for this. Strong homeowner equity gives many people a path forward that doesn’t end in losing their home.

Struggling Homeowners Still Have Options

If you’re behind on mortgage payments or worried you may fall behind soon, the most important thing to know is that you may have more options than you think.

Missing a payment does not automatically mean you’ll lose your home.

Most lenders would rather work with you than go through foreclosure; the process is costly and time-consuming for them too. Depending on your situation, they may be able to discuss options such as:

- A repayment plan

- Temporary forbearance

- Loan modification

- Other hardship assistance programs

The sooner you contact your lender, the sooner you’ll be able to explore your options. Waiting too long can make the situation more difficult, especially in states where the foreclosure process moves quickly.

And if selling your home becomes your best option, talking with a real estate professional can help you understand your home’s current value, your equity position, and whether selling could help you avoid foreclosure.

Bottom Line: Don’t Panic

Foreclosure filings are rising, but that doesn’t mean the housing market is headed for another crash. Today’s numbers are still low compared to historical levels, and the equity homeowners have built gives many people options they didn’t have in 2008.

Online headlines and discussion may sound alarming, but the full story is much more reassuring. This is not a repeat of the last housing crisis. It’s a normalizing housing market, and one supported by much stronger homeowner equity.