Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mortgage debt in the United States has hit a record high, and at first glance, that looks like a warning sign for the housing market.

It’s an attention-grabbing headline for sure. After all, when people hear “record debt,” most think back to the 2008 housing crash and wonder if today’s market is heading in the same direction.

But headlines leave out the real story.

It’s true that mortgage debt is higher than ever. But, so are home values and homeowner equity. When you add in those missing pieces, the real picture becomes much less alarming than you might think.

Mortgage Debt Is High, But So Is Homeowner Wealth

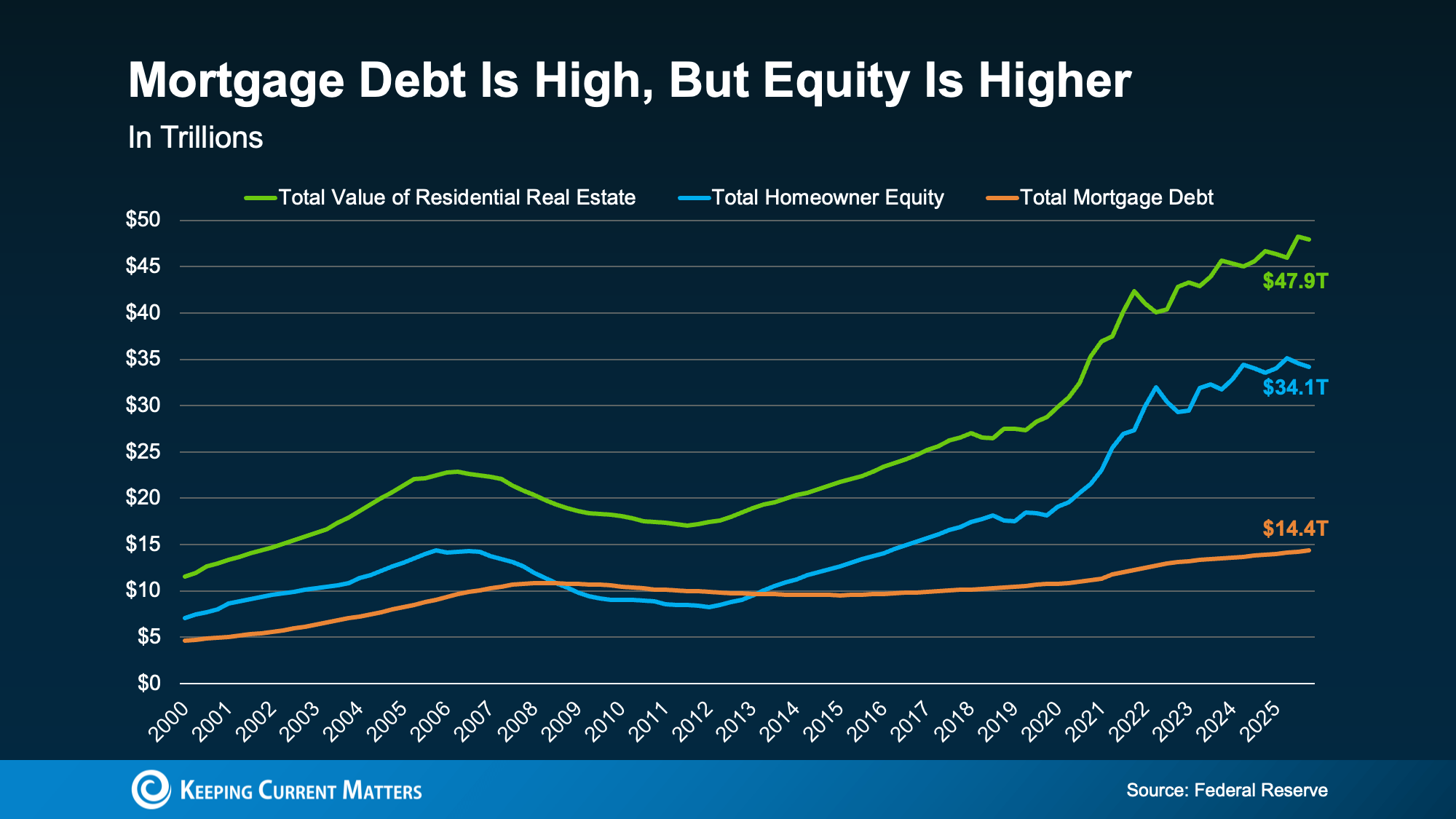

New data from the Federal Reserve says total U.S. mortgage debt is now around $14.4 trillion, and the Federal Reserve Bank of New York found it was $13.19 trillion at the end of March 2026. Both numbers are record highs, but they’re missing some critical perspective.

Meanwhile, the total value of U.S. homes is about $47.9 trillion, while homeowners collectively hold roughly $34.1 trillion in equity. In other words, homeowners owe a lot, but they also own a great deal more.

Mortgage debt has peaked, but that alone doesn’t determine the health of the housing market. What matters more is how much equity homeowners have compared to what they owe.

Right now, homeowner equity is more than double the amount of mortgage debt, and near its own historical peak. That’s a very different situation from the years surrounding the 2008 housing crisis.

Why Today’s Housing Market Is Not Like 2008

During the housing crash, many homeowners owed more on their mortgages than their homes were worth. When home prices fell, they had little to no financial cushion. That caused a wave of serious distress, including short sales and foreclosures.

Today’s market looks very different.

Homeowners have significantly more equity than debt, which gives them options. Even if home prices soften in some areas, many owners still have a substantial financial buffer. They can sell, refinance when conditions improve, or use their equity strategically if needed.

That equity cushion is one of the biggest reasons today’s housing market is on much stronger footing than it was during the last crash.

Many Homeowners Have Little or No Mortgage Debt

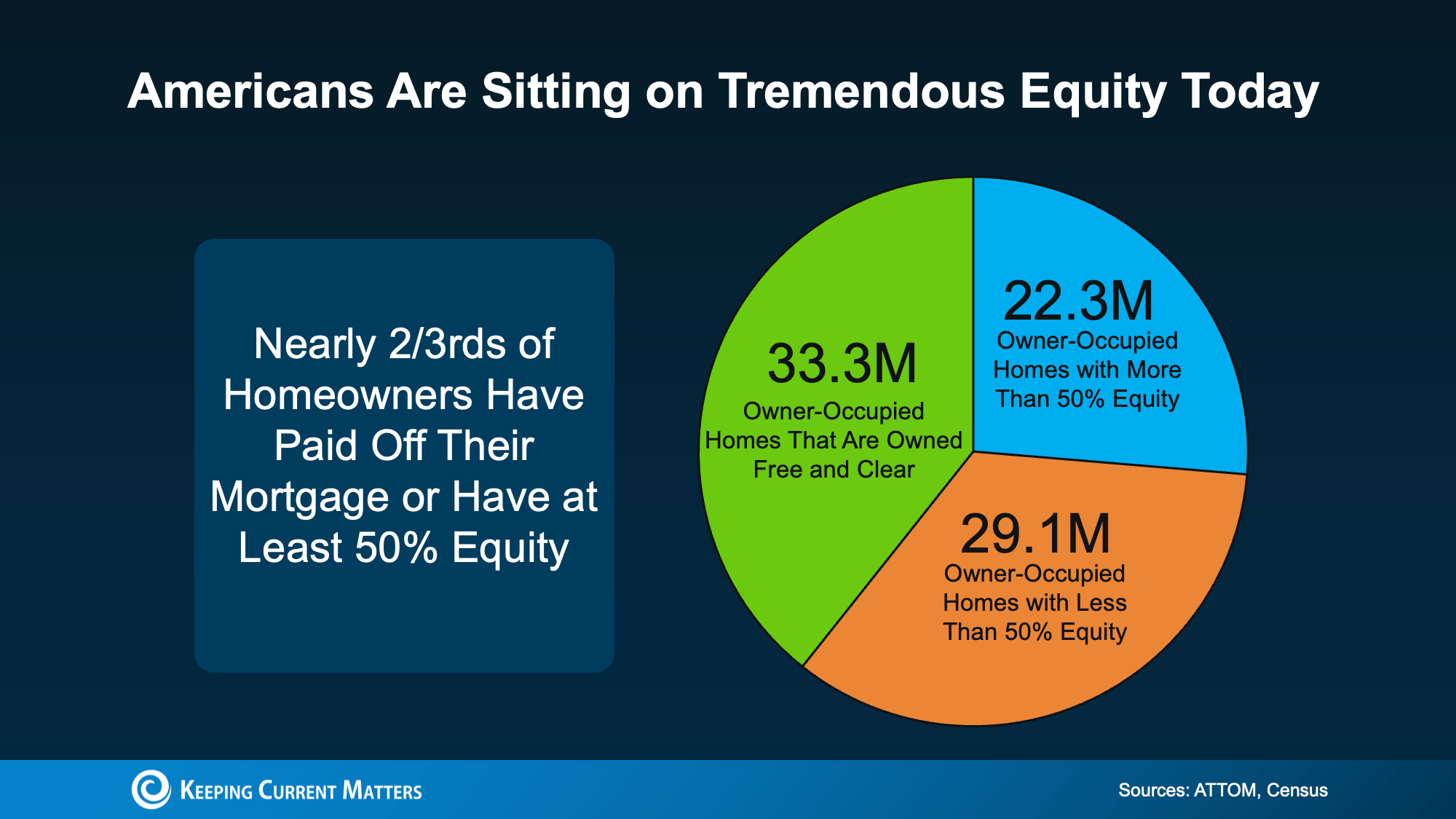

The strength of today’s market is even clearer when you look at homeowners individually. Recent data from ATTOM and Census illustrate this point.

Of all owner-occupied homes in the United States, 33.3 million are owned free and clear, meaning there’s no mortgage on the property at all. On top of that, 22.3 million homeowners have more than 50% equity in their homes.

Put those groups together, and nearly two-thirds of homeowners are in an exceptionally strong financial position. Some owe no mortgage debt, and others owe far less than their homes are worth.

Those are the signs of a strong market, not a fragile one.

What About Homeowners With Less Than 50% Equity?

The remaining group includes homeowners with less than 50% equity. But these homeowners aren’t necessarily in trouble.

Many of these homeowners are simply recent buyers. Since equity builds over time through mortgage payments and home price appreciation, newer buyers naturally tend to have less equity than people who have owned their homes for years.

Low equity doesn’t always signal financial stress or threat of foreclosure. Often, it just means someone is a first-time buyer in early homeownership.

The Real Story Behind Record Mortgage Debt

Mortgage debt is a critical piece of the housing market’s health, but it’s only one piece it.

When you also consider record or near-record home values, strong homeowner equity, and the number of people who own their homes outright, there’s far less cause for alarm.

Homeowners today aren’t severely overleveraged the way they were before the 2008 crash. Many have meaningful equity, and most have no mortgage debt at all.

Bottom Line: Strong Equity Balances High Debt

Dramatic headlines about record mortgage debt can make it seem like the housing market is in trouble, but the actual data tell a more reassuring story.

Home values are high. Homeowner equity is strong. And a large share of homeowners are in a stable financial position.

So while mortgage debt has reached a record level, today’s market has a much stronger foundation than recent headlines would suggest.

No matter if you’re thinking about buying, selling, or simply trying to understand what these numbers mean for your local market, talking with a trusted real estate professional can help you learn the real story.