Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Condos vs. Townhomes: Affordable Buying Options in 2026

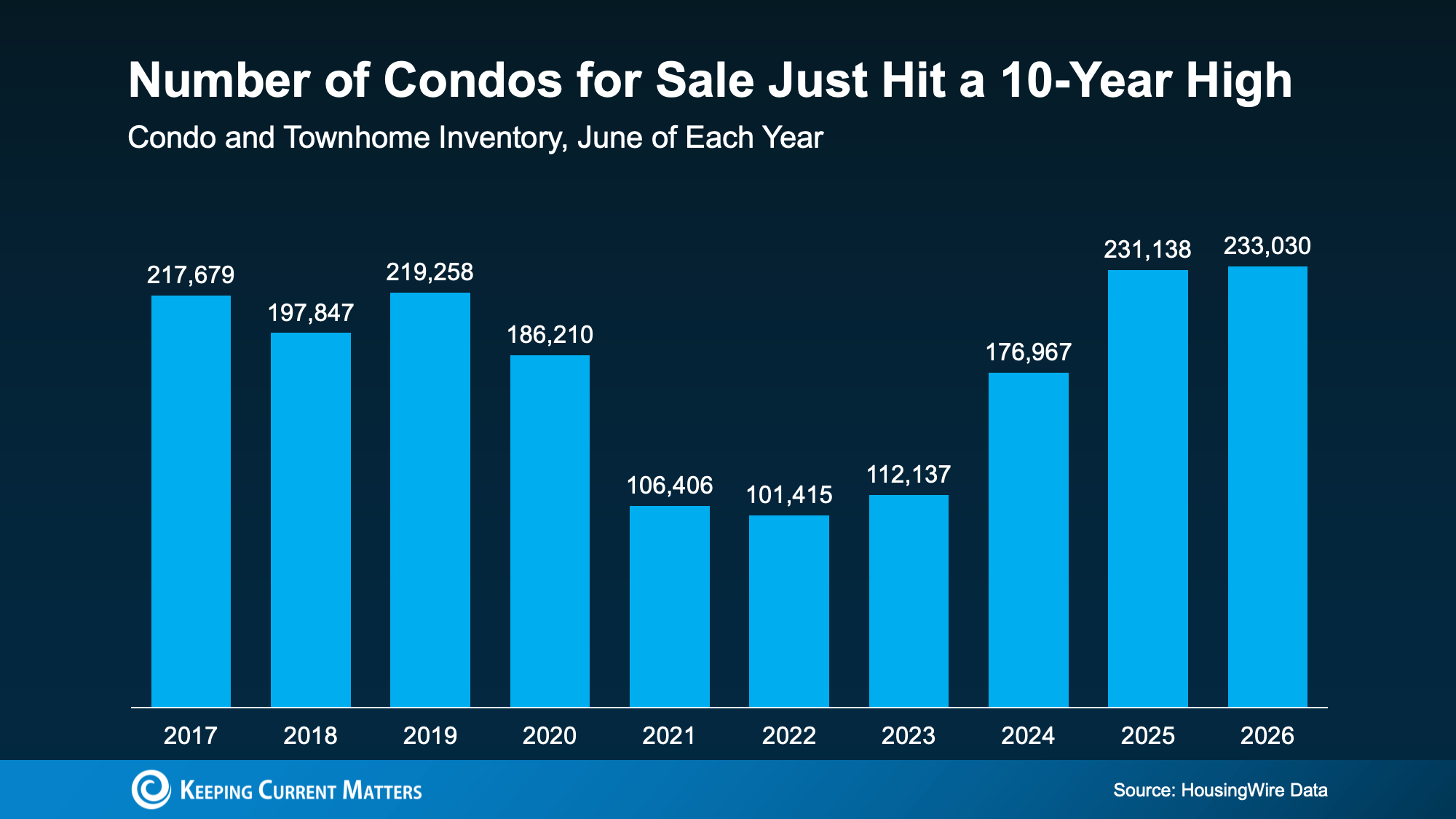

The number of condos and townhomes for sale reached 233,030 in June 2026, giving buyers the most inventory shown in a decade. Source: HousingWire.

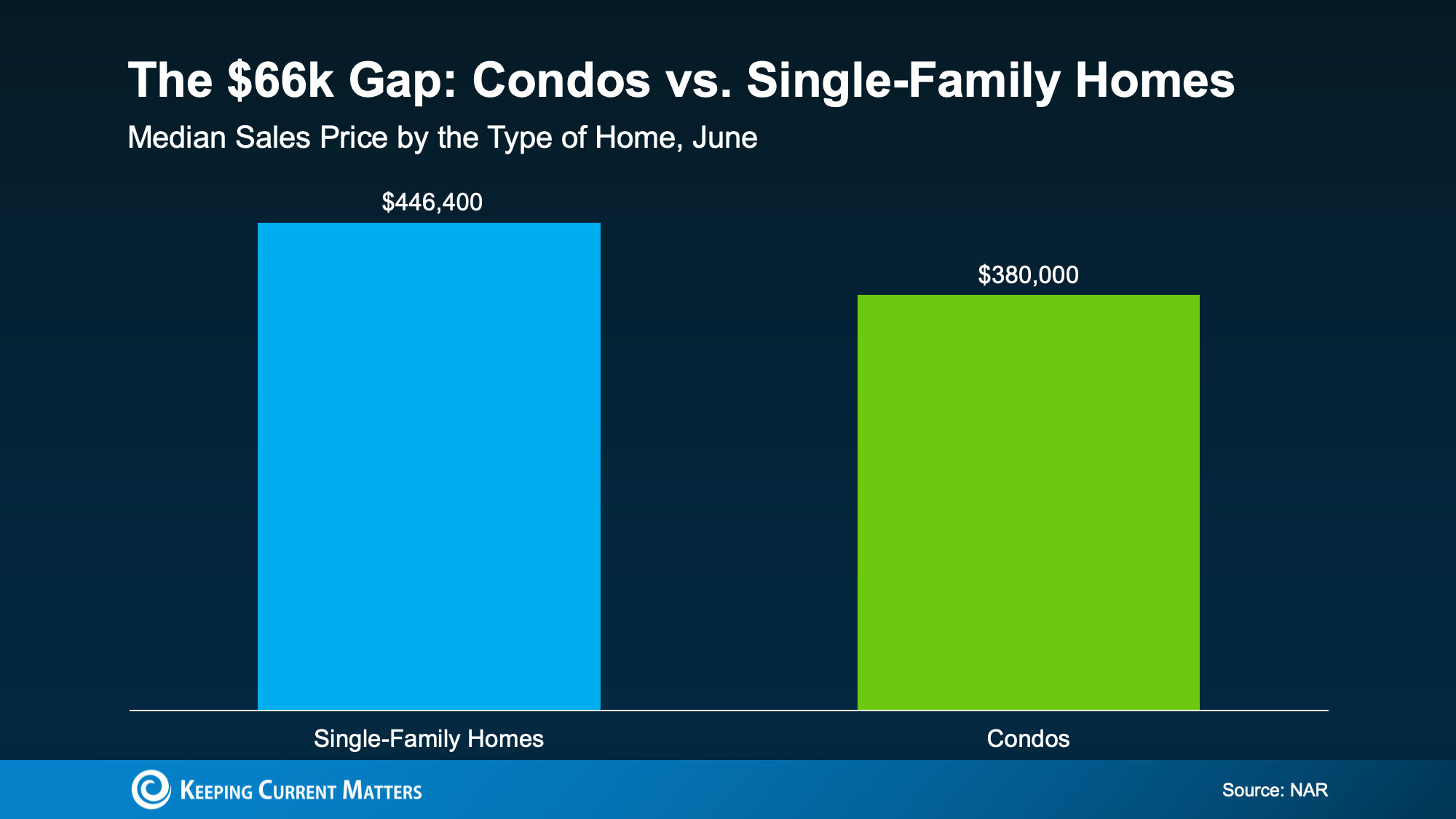

A lower median sales price may make condos a more attainable alternative for buyers priced out of single-family homes. Source: NAR.

Although the terms are sometimes used interchangeably, condos and townhomes aren’t necessarily the same.

Condos

-

Ownership: You own the interior living area of your specific unit. Shared building elements and community spaces are jointly owned by all residents.

-

Amenities: Access to shared amenities like workout rooms, pools, or community spaces.

-

Upkeep: Minimal individual exterior maintenance responsibility. Comes with shared building decisions, shared walls, and regular HOA fees to cover common area upkeep and exterior repairs.

Townhomes

-

Ownership: You own the multi-level building structure and the specific lot beneath it.

-

Layout: Typically multi-story attached structures, sharing at most two side walls.

-

Upkeep: Provides greater autonomy over design and repairs, with exterior maintenance duties usually shared or managed under specific HOA guidelines.

A condominium is technically a form of ownership rather than a particular building style. A condo could be located in a multistory building, resemble a traditional townhome, or even be detached. Likewise, a townhome may be sold with its land or organized legally as a condominium.

Summer Housing Market Guide: More Choices, Better Prices

If you paused your home search over the past few years, you likely ran into two major hurdles: asking prices that kept climbing and a frustrating lack of homes for sale.

This summer, both challenges are starting to ease in many markets. Buyers are seeing more homes for sale, while more sellers are reconsidering their asking prices.

Here’s a closer look at current summer real estate market trends and what they mean for your home search.

Sellers Are Pricing Homes to Attract Buyers

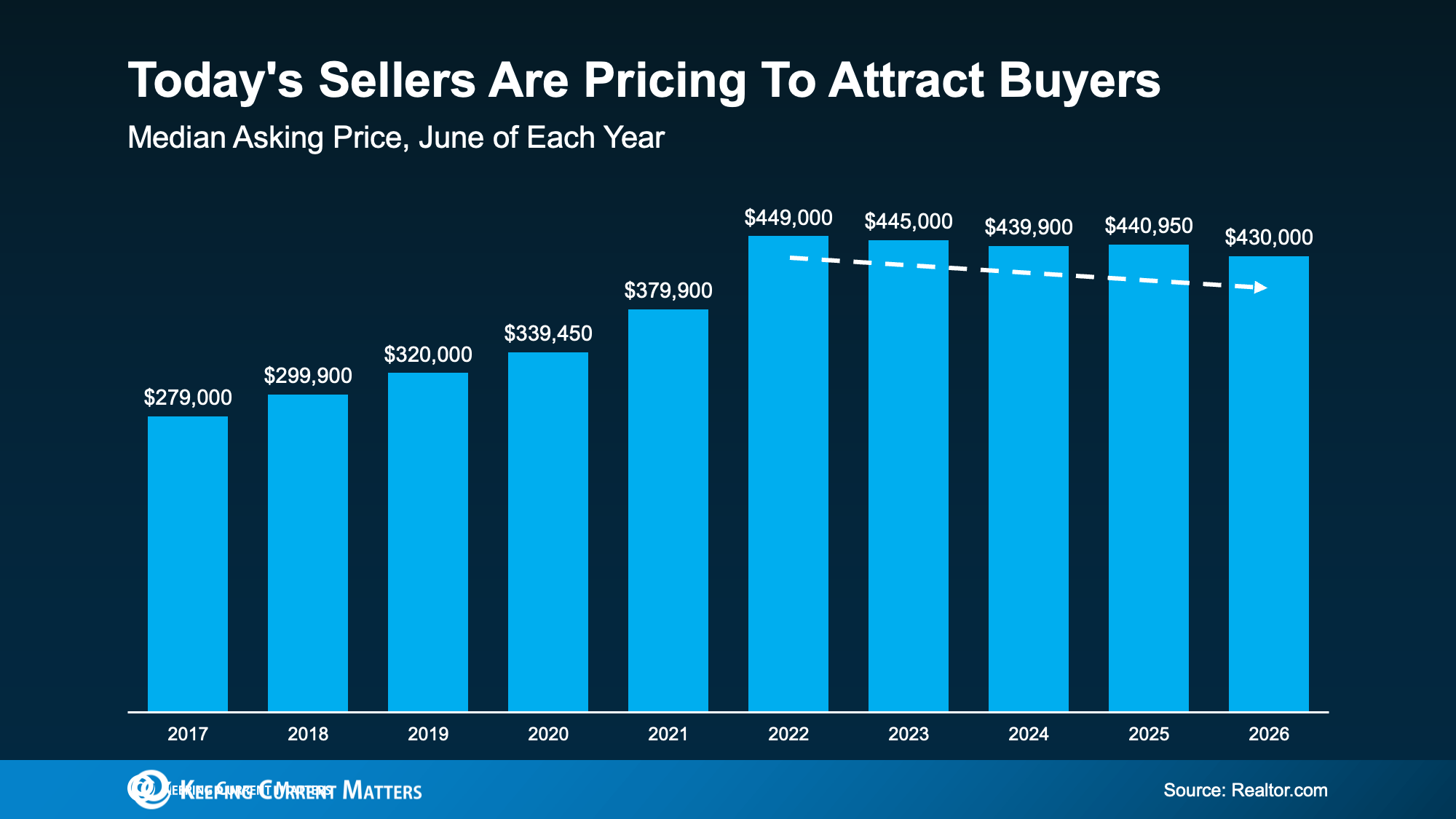

Sellers are adjusting their strategy to meet current market reality. According to Realtor.com data, the national median asking price was $430,000 in June, nearly $11,000 lower than last year.

June also marked the eighth consecutive month in which the typical asking price was lower than it had been during the same period one year earlier.

While ongoing price drops might sound concerning at first, it’s not a sign of a market crash. This data tracks asking prices rather than final sold prices, signaling that sellers are setting realistic expectations right from the start.

As Danielle Hale, Chief Economist at Realtor.com, explains:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to rise indefinitely. Now that listing prices are settling closer to realistic buyer budgets, the market is moving toward a healthier, more balanced state.

Housing Inventory Is Catching Up

If you spent previous seasons watching properties disappear before you could even schedule a showing, this is welcome news.

Realtor.com reports that the number of homes listed for sale in June reached its highest June level in three years.

While overall supply has not fully returned to pre-pandemic levels seen between 2017 and 2019, increased listing activity can give buyers:

- More Options: You can evaluate a wider selection of properties rather than settling for what happens to be available.

- Less Urgency: Reduced competition per property means you do not have to rush an offer just to remain in contention.

- Greater Negotiation Leverage: With more inventory on the market, you have more room to negotiate terms and pricing than buyers had a year ago.

Great News for First-Time Home Buyers

These trends are especially encouraging for first-time buyers looking for homes at lower price points.

Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

In other words, buyers looking for more affordable homes may encounter a little more selection and some additional flexibility on price.

That doesn’t mean every home will be an easy purchase or that competition has disappeared. But it does mean that first-time buyers who paused their home search may be pleasantly surprised by this summer’s market.

Bottom Line

If steep home prices or a lackluster selection caused you to pause your plans, this summer may be a good time to look again.

More homes for sale and lower asking prices could give you additional choices, less pressure, and more room to get a better deal on a house you love.

If you’re ready to restart your search this summer, browse available homes now or contact us today to connect with an expert local agent.

Buying a Home With Student Loans: What You Need to Know

Student loans are back in the news and might be weighing on your mind if you’ve been following the headlines recently. If you’re wondering what your student debt means for your homeownership plans, there’s one important thing to remember:

Having student loans does not automatically mean you can’t buy home.

The Biggest Myth About Student Loans and Mortgages

Many first-time buyers believe they have to completely pay off their student loans before they can qualify for a mortgage.

In most cases, this isn’t true.

According to a Redfin article, student loans are usually evaluated by lenders in the same way as other standard debts, such as car payments or credit cards:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

A student loan on your credit report is not an automatic disqualifier. Instead, lenders look at your broader financial profile, including your:

- Income

- Monthly debt payments

- Credit history

- Overall financial situation

Your student loans matter, but they don’t tell a lender the whole story.

Many Homebuyers Have Student Loan Debt

To really put things into perspective, data from the National Association of Realtors (NAR) proves that you can have student debt and still buy a home.

According to NAR’s research:

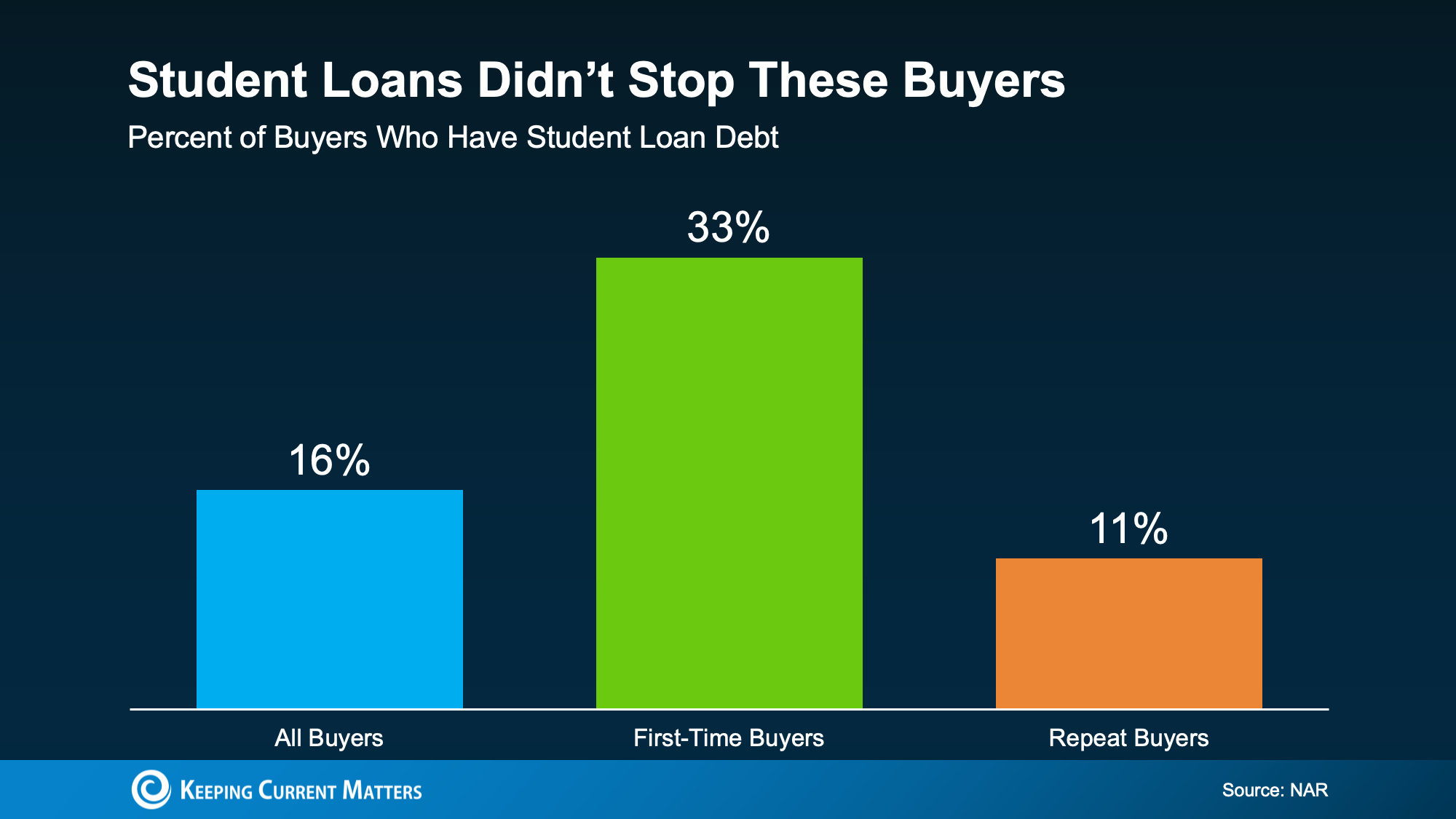

-

33% of first-time homebuyers still had student loan debt when they purchased their home.

-

That translates to 1 out of every 3 first-time buyers.

-

The median amount of student loan debt they owed was $30,400.

Let this reassure you that people are successfully buying homes with student debt every single day. Carrying student loans may affect how much you can borrow, but it doesn’t mean homeownership is beyond your reach.

Explore Your Mortgage Options First

A lot of potential buyers trip themselves up right at the starting line. They assume the worst regarding their loan eligibility and never check what they could actually qualify for. But your financial situation is unique and deserves some exploration.

If your income is steady and your overall finances are in decent shape, buying a home could be far more realistic than you think. The only way to know is to review the numbers with a qualified mortgage professional. You might discover you’re much closer to buying a house than you thought.

Bottom Line

Student loans don’t have to stop you from owning a home. If you’ve been putting off your homebuying plans because of debt, talk to a lender about your options. It may not be the roadblock you think it is.

Contact our team today to connect with trusted local lenders and start exploring your real estate options.

2026 Housing Market Forecast: Second-Half Outlook

If the first half of 2026 left you feeling a bit stuck in your moving plans, you’re definitely not alone. Affordability remained tight, mortgage rates crept higher, and global uncertainty added more pressure to an already cautious market. For many people, that created one big question:

Will the housing market improve in the second half of 2026?

No one can predict the market perfectly, but there are a few signs that the market could start moving in a better direction. Here’s what buyers, sellers, and homeowners should watch in the second half of 2026.

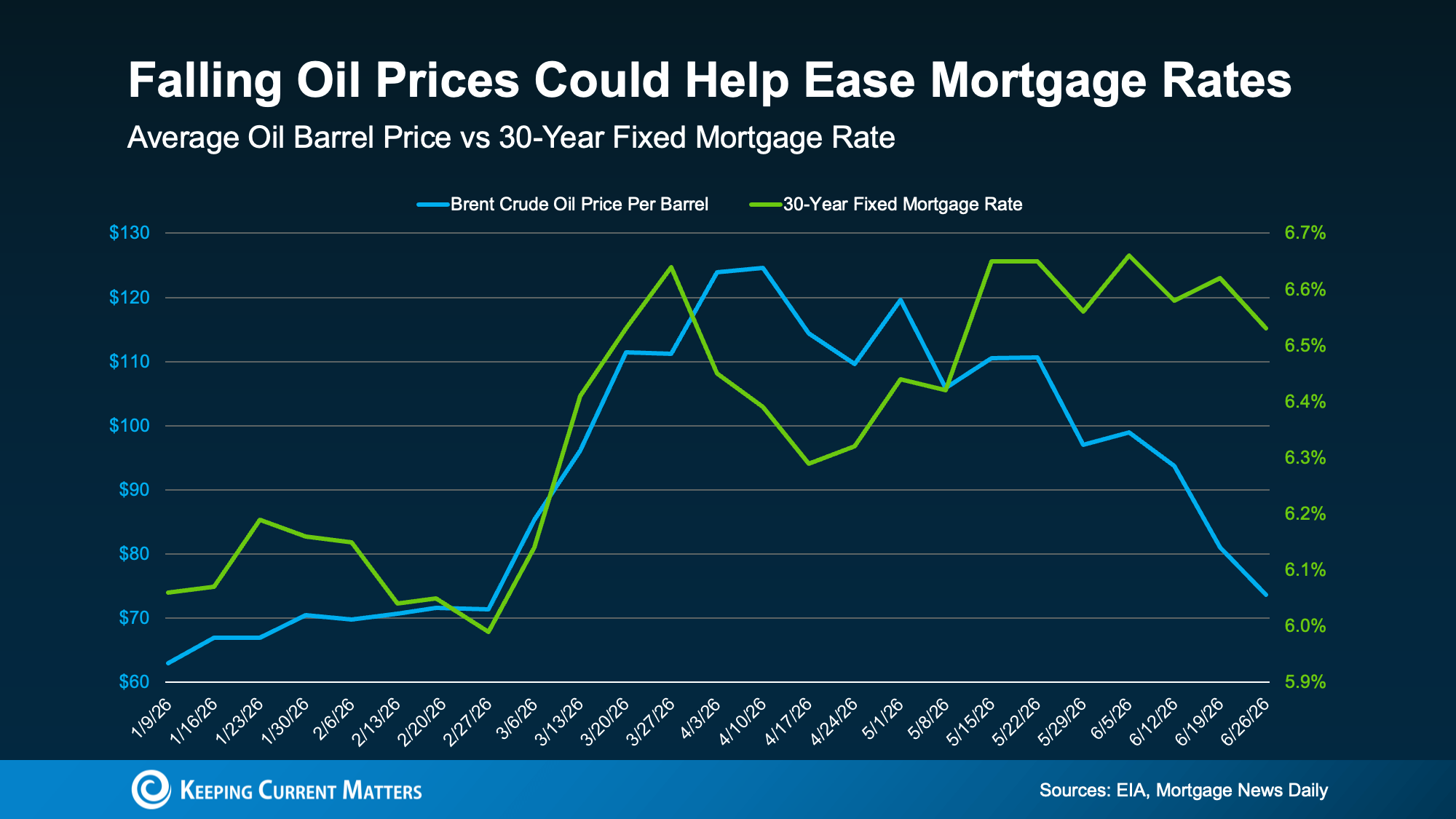

Will Mortgage Rates Finally Drop?

Mortgage rates have been one of the biggest reasons the market has felt stuck, and inflation has been keeping them high. A combination of higher energy prices and global uncertainty has kept inflation higher than ideal. However, there is some encouraging news on the horizon regarding oil prices.

Oil prices have begun to ease a bit, and while that might not seem directly related to buying a home, mortgage rates and oil prices historically tend to move in the same direction. For instance, both oil prices and mortgage rates increased in February when the conflicts overseas started. Despite the recent volatility, experts at the U.S. Energy Information Administration (EIA) predict oil prices will come down. With oil prices trending down, it’s possible that mortgage rates will do the same.

This is by no means a guarantee. But, if energy prices decrease, inflation cools, and overseas tensions ease, we could see mortgage rates come down in the second half of the year. For buyers, even a modest rate improvement could help with affordability. For sellers, lower rates could bring more buyers back into the market.

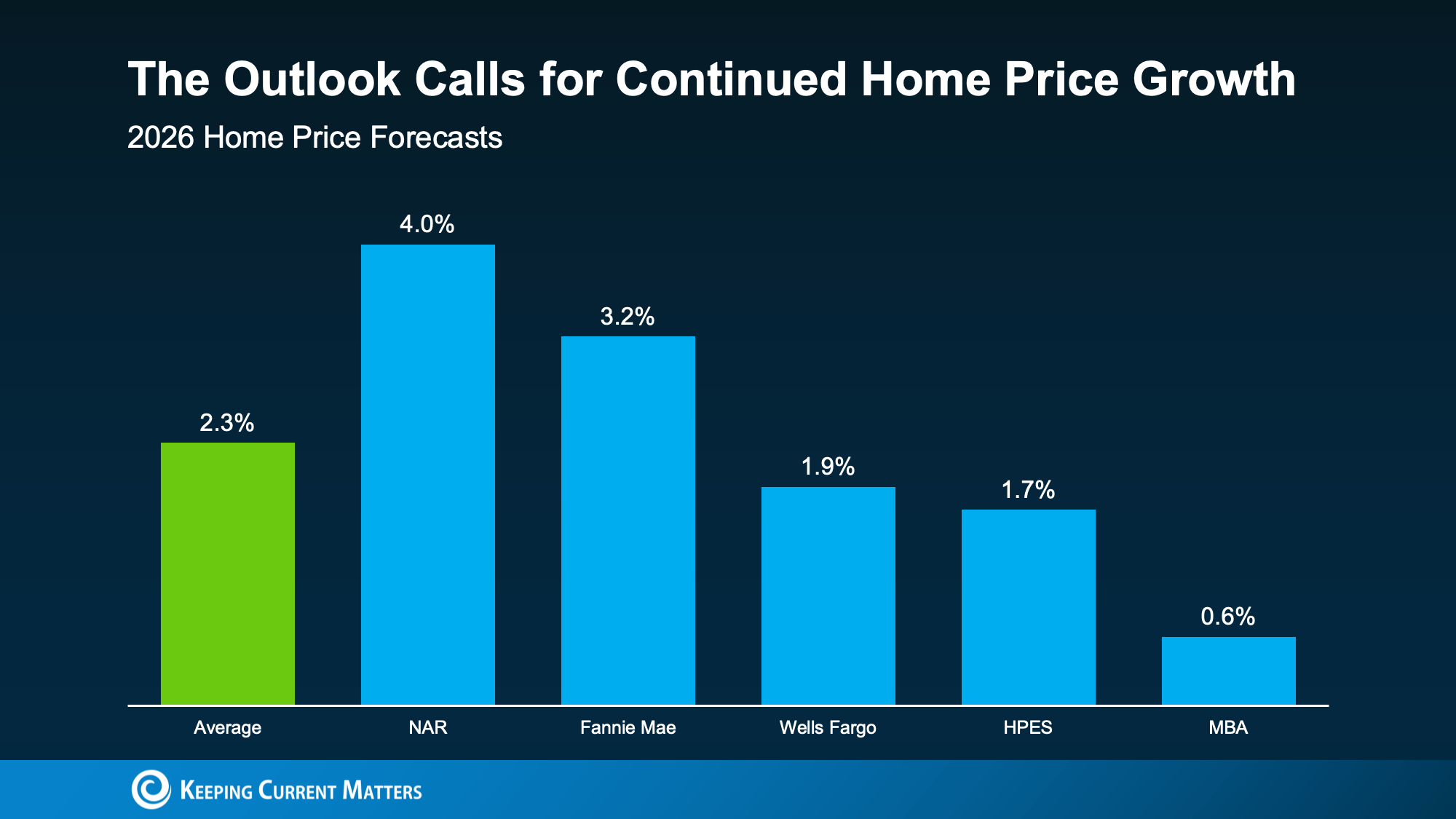

Home Prices Are Projected to Rise

Many buyers are hoping home prices will fall. In some local markets, prices may soften or dip slightly. But nationally, most forecasts still point to positive price growth for 2026. On average, experts are projecting an average price increase of 2.3% in 2026.

According to data from the Federal Housing Finance Agency (FHFA), prices are currently up about 1.7% nationally year-over-year. To reach the projected 2.3% average for the entire year, home price growth will need to pick up slightly during the second half of 2026.

Why might prices continue to rise?

-

Inventory Shifts: The number of homes for sale has grown, but the pace of that growth may be starting to slow down.

-

Returning Buyers: If mortgage rates improve, more buyers are likely to jump back into the market.

-

Increased Competition: More competing buyers could put modest upward pressure on home prices, especially if housing inventory is not growing as quickly as demand.

For buyers, this means that waiting for a lower price later is not a guaranteed strategy. For sellers who have been worried about retaining their home’s equity, these projections are welcome news.

Expect Stronger Home Sales Volume

If the housing market has felt quieter than expected this year, it’s not your imagination. Home sales have been slower than many people hoped. But that doesn’t mean people have given up on moving.

Many hopeful buyers and sellers have simply been waiting for firmer market certainty, better affordability, or a clearer understanding of where real estate is headed. If mortgage rates ease and confidence improves, more people may decide it is time to move forward.

Odeta Kushi, Deputy Chief Economist at First American, explains the current market sentiment:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

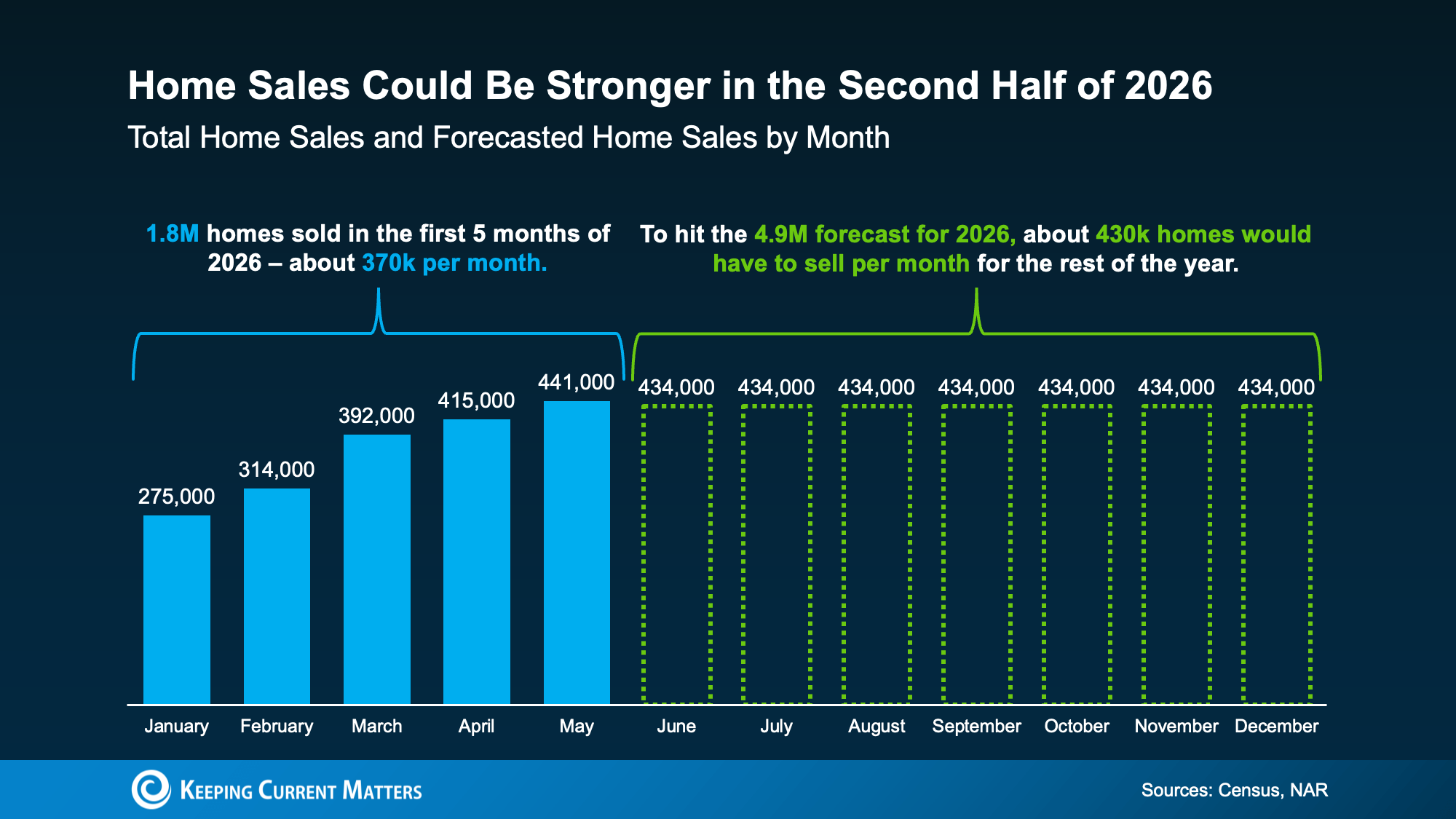

To hit the forecasted 4.9 million home sales expected for 2026, the second half of the year will need to significantly outperform sales in the first half.

Essentially, every month for the rest of 2026 would need to match the momentum of May, which was the strongest month in the first half of the year. This indicates that experts anticipate much more market activity heading into the fall and winter.

The Bottom Line

The second half of 2026 might not be ideal, but conditions are pointing toward improvement. Mortgage rates may ease, home sales could accelerate, and property values are expected to continue rising at a steady, sustainable pace.

If you’re thinking about buying, selling, or relocating this year, connect with our brokerage team. We can help you understand local inventory, pricing, buyer demand, and what these 2026 housing market trends may mean for your plans.

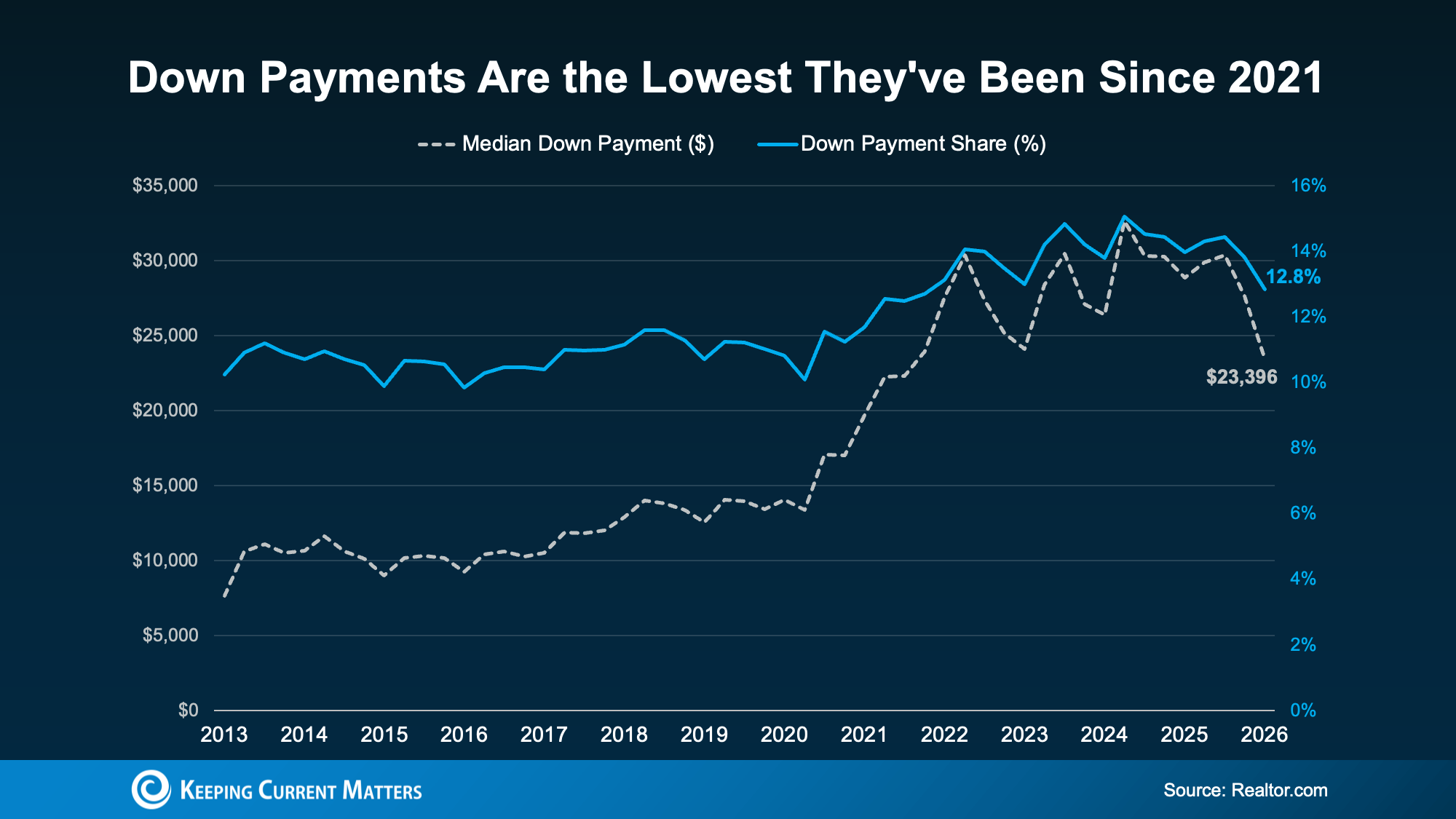

Down Payments Are at Their Lowest Since 2021

Saving for a down payment is often the biggest obstacle to buying a home. With the challenges of affordability today, it’s easy to wonder how anyone manages to save enough cash right now.

But here’s some good news: some buyers are getting into homes with smaller down payments than they may have expected.

According to Realtor.com, the typical buyer put down about $23,400 in early 2026. That’s about $5,000 less than the year before, a 19% year-over-year drop. It’s also the lowest typical down payment level since 2021.

3 Reasons Why Down Payments Are Shrinking

Why are buyers putting less money down today? Three major shifts in the housing market are driving this trend:

-

Less Competition Between Buyers

In the most competitive markets of the past few years, some buyers felt pressure to put more money down to make their offers stand out.

Today, conditions are more balanced in many areas. With less intense competition, buyers are less pressured to offer a huge down payment to make an offer stand out.

-

Home Price Growth Has Moderated

Your down payment is typically based on a percentage of the purchase price. When home price growth slows or levels off, the dollar amount needed for a down payment can shift too.

In many markets, prices have cooled from the rapid pace seen in recent years. Some areas have even seen slight price dips. That can help reduce the upfront amount some buyers need to save.

-

More Buyers Are Using Lower Down Payment Loan Options

More buyers are also turning to loan programs that often require less money upfront. Government-backed loan options, like FHA loans and VA loans, often allow eligible buyers to purchase with a lower down payment or, in some cases, no down payment. According to Mortgage Professional America, FHA loans have made up more than 24% of purchase mortgages for five straight quarters, while VA loans recently reached their highest share in more than a decade.

Of course, not every buyer will qualify for every program, and any down payment is a huge amount of money to save. To make up the difference, buyers are relying on two things: payment assistance programs and family support.

Financial Help You May Not Know You Qualify For

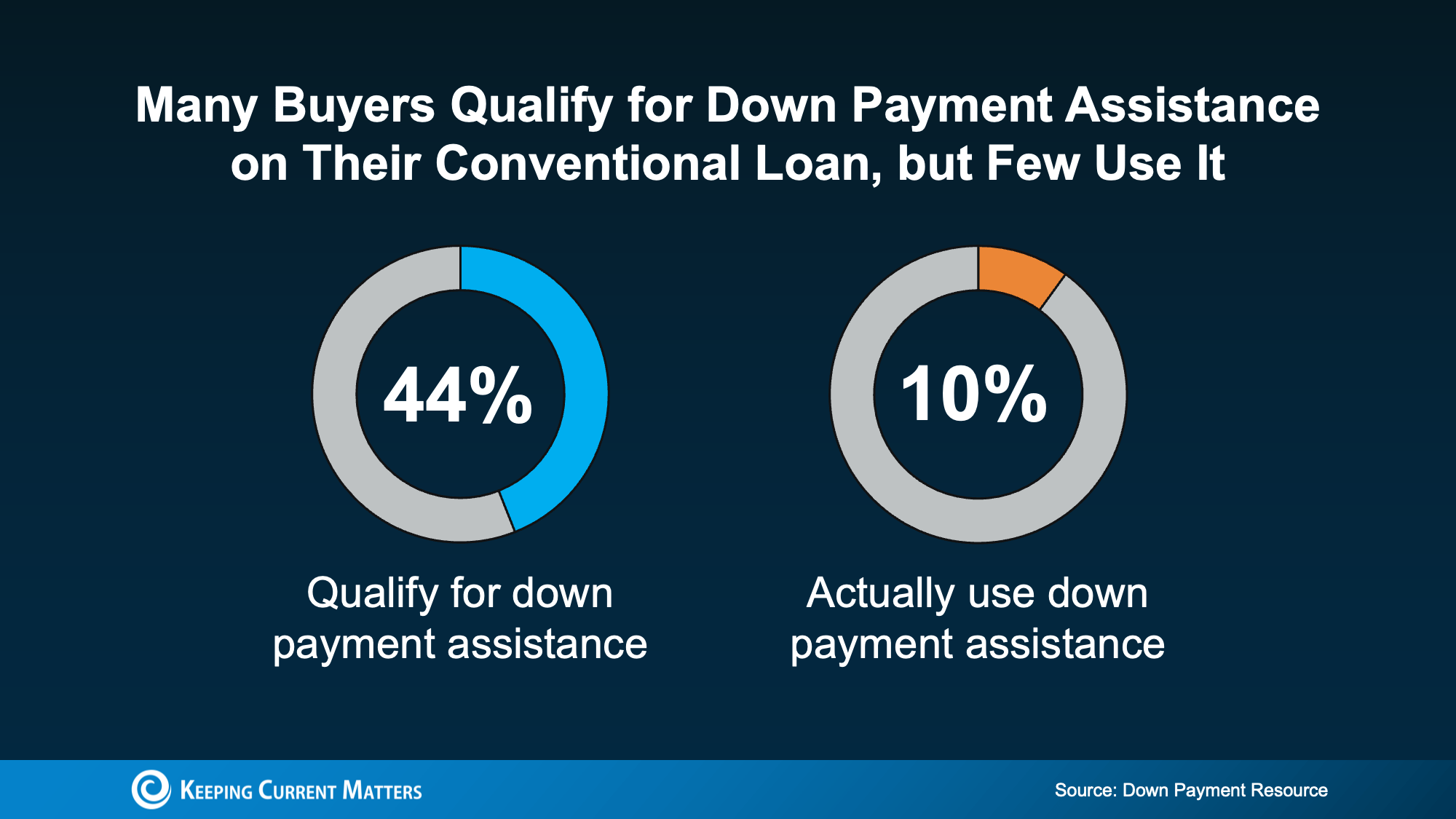

Down payment assistance is one of the most overlooked resources in real estate. A study by the Urban Institute and Down Payment Resource looked at the 10 largest U.S. metros and found that nearly 44% of recent buyers already qualified for a down payment program. Surprisingly, only 10% of those buyers actually used the help when closing on their loan.

There are more options available than many buyers realize. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available.

-

More than half (62%) are designed specifically to help first-time buyers.

-

38% have no first-time buyer requirement, meaning you may qualify even if you’ve owned a home before.

-

62% are open to buyers earning $100,000 or more.

So, don’t assume you’re priced out of a home or ineligible for help. A lender or knowledgeable real estate professional can help you ask the right questions and explore programs that may fit your situation.

A Helping Hand from Loved Ones

A growing number of buyers are also getting help closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support usually goes toward the down payment, followed by helping the buyer qualify for a mortgage and covering closing costs.

Chris Birk, VP of Mortgage Insight at Veterans United, explains it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

Not everyone has family or loved ones who are able to help. But for buyers who do, it can speed up how quickly they’re able to buy a home.

Bottom Line

Down payments are smaller than they’ve been in years, opening the door for more buyers to enter the market. Between down payment assistance programs and support from family, you may have more paths to homeownership than you realize.

Always consult with a trusted mortgage professional to review your financial situation. If you’re ready to start exploring neighborhoods and discussing your goals, contact our brokerage today to connect with an experienced local real estate agent.

Here’s the Number One Factor Impacting Home Prices Today

You might have heard that home prices are cooling off. Nationally, that’s true. But when you look at individual markets, the picture can be very different depending on where you are.

Some regions are seeing solid price growth, while others have flattened out or even dipped slightly negative. So what’s causing these huge variation in the real estate market?

The answer comes down to one major factor: housing inventory.

How Housing Market Inventory Drives Prices

The relationship between housing supply and home prices is straightforward:

- When there are more homes for sale, buyers have more options.

- More options usually mean less competition.

- Less competition can make it harder for sellers to push prices higher.

The opposite is also true. When inventory is tight, buyers are competing for a smaller pool of homes. That competition can help push prices up.

This supply and demand dynamic is currently playing out across the country right now.

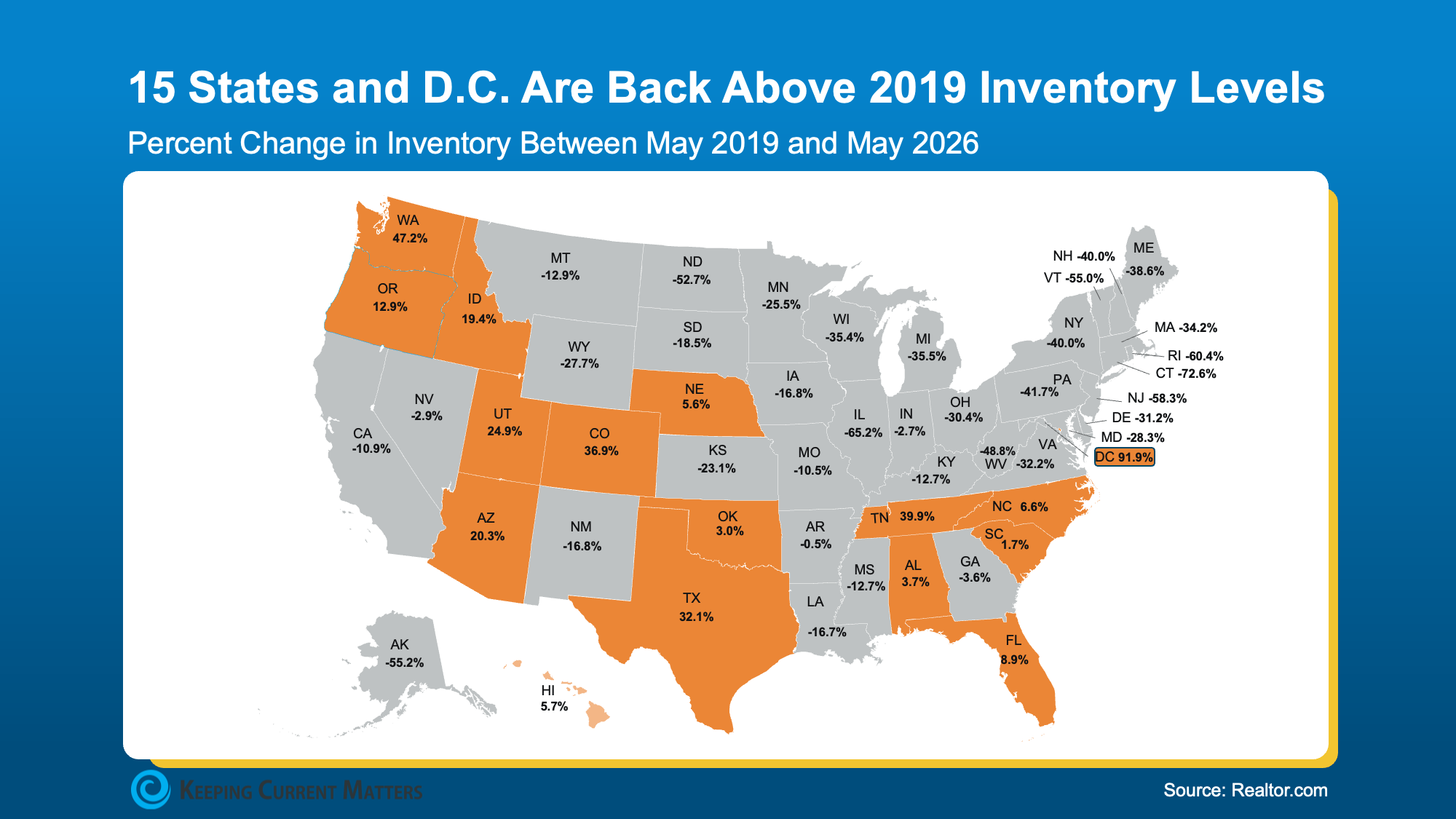

Markets where inventory has climbed back to, or above, normal pre-pandemic levels are seeing prices flatten or fall slightly. Markets where inventory is still well below 2019 benchmarks are generally still seeing prices rise.

As Lance Lambert, CEO of ResiClub, explains:

“Home prices are still climbing a little year-over-year in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest.

In contrast, some pockets in states like Texas, Florida, and Colorado — where active inventory exceeds pre-pandemic 2019 levels by a solid clip — are seeing modest home price pullbacks or flat pricing.”

A Tale of Two Real Estate Markets

To understand current price shifts, we have to look back at normal, pre-pandemic inventory levels from 2019.

In most places, inventory is still below where it was before the pandemic. That is one reason prices are still climbing moderately in the majority of states.

But the markets getting the most attention are the ones where prices are softening. And in many of those areas, inventory has made a much bigger comeback.

According to Realtor.com, 15 states and Washington, D.C. are now above pre-pandemic inventory levels, with some areas well above those benchmarks.

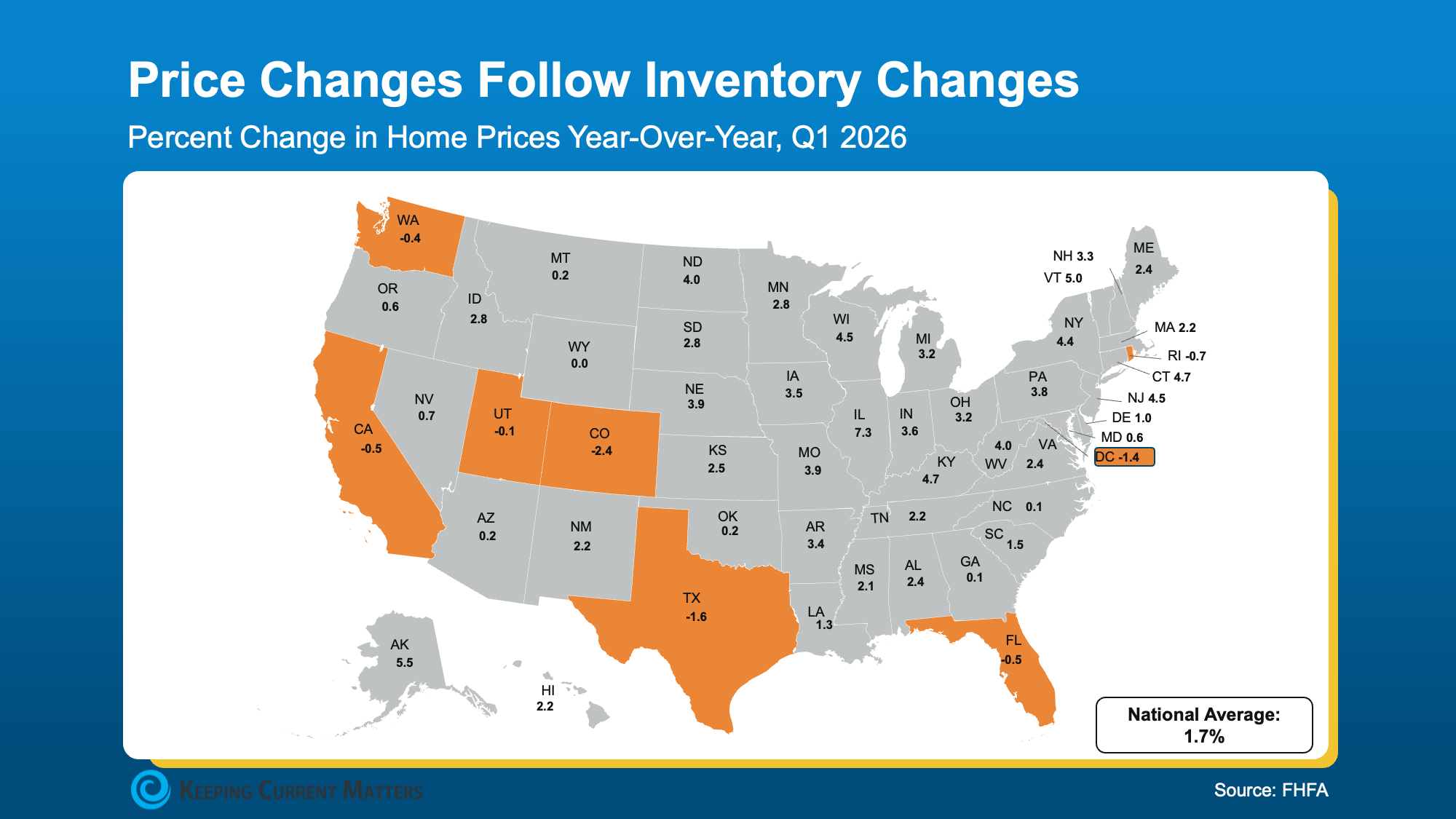

When you compare those inventory trends with the latest Federal Housing Finance Agency (FHFA) data on home prices, the connection becomes much clearer.

The areas with more homes for sale are often the same places seeing prices flatten or dip slightly.

This overlap isn’t a coincidence: it’s direct cause and effect.

The national average of 1.7% price growth is accurate, but it’s a blend of two very different stories. A few areas are experiencing mild price declines, while the overwhelming majority of markets are still seeing prices rise.

What This Means for Home Buyers and Sellers

For both buyers and sellers, local conditions matter more than the national average. The best strategy will depend on your local housing market inventory.

If You’re a Home Buyer:

- In higher-inventory states like Texas, Colorado, or Florida, you may have genuine negotiating power.

- In these areas, you will likely find more choices, face less competition, and encounter sellers who are motivated to make a deal.

- If you’re shopping in tighter markets, like much of the Northeast, you should prepare to face steeper competition.

If You’re a Home Seller:

- Your pricing strategy is everything.

- In markets where inventory has risen, overpricing your home is the fastest way to sit on the market and eventually sell for less than you would have with the right initial price.

- If you live in a market where inventory is still low, you’re in a stronger position.

- Pricing your home correctly from day one still matters if you want to attract serious buyers quickly.

Bottom Line

When it comes to home prices, your location matters more than ever.

Inventory is the key factor shaping today’s market. Areas with more homes for sale are seeing prices flatten or dip slightly, while areas with limited inventory are generally still seeing prices rise.

Whether you’re buying or selling, partnering with an experienced real estate agent is the best way to understand what’s happening in your market.

Ready to make sense of your local market and make a move? Contact our brokerage today to connect with a local agent who can help you compare inventory, pricing, and next steps.

Will Home Prices Crash Soon? What Expert Forecasts Say

A lot of homebuyers are still sitting on the sidelines, waiting for home prices to drop.

Some are waiting for a crash so they can get a better deal. Others are worried they’ll watch their home’s value drop if they buy now.

Nobody wants to feel like they overpaid or bought too early. But there’s an important question to ask:

What if the crash you’re waiting for never happens?

Based on the latest data from experts, a nationwide housing crash isn’t on the horizon.

Experts Are Not Predicting a Housing Market Crash

You’ve probably seen headlines or social media posts lately saying home prices are about to come crashing down.

It’s true that some markets are seeing small price declines. But a local price shifts are not the same as a nationwide housing crash.

According to Realtor.com data, home prices are still rising in 71% of housing markets across the country.

Unfortunately, negative news tends to get more attention. Stories about price declines in a handful of markets can make it seem like prices are falling everywhere, even when most markets show the opposite.

So, how can buyers get a clearer picture of where home prices may be headed?

One trustworthy source is the Home Price Expectations Survey (HPES) from Fannie Mae.

The 5-Year Home Price Forecast

Each quarter, the HPES asks more than 100 economists, housing experts, and market analysts where they believe home prices are headed based on the most current data.

Even amid today’s ongoing market uncertainty, these experts agreed on one key point:

They do not think a housing crash is coming.

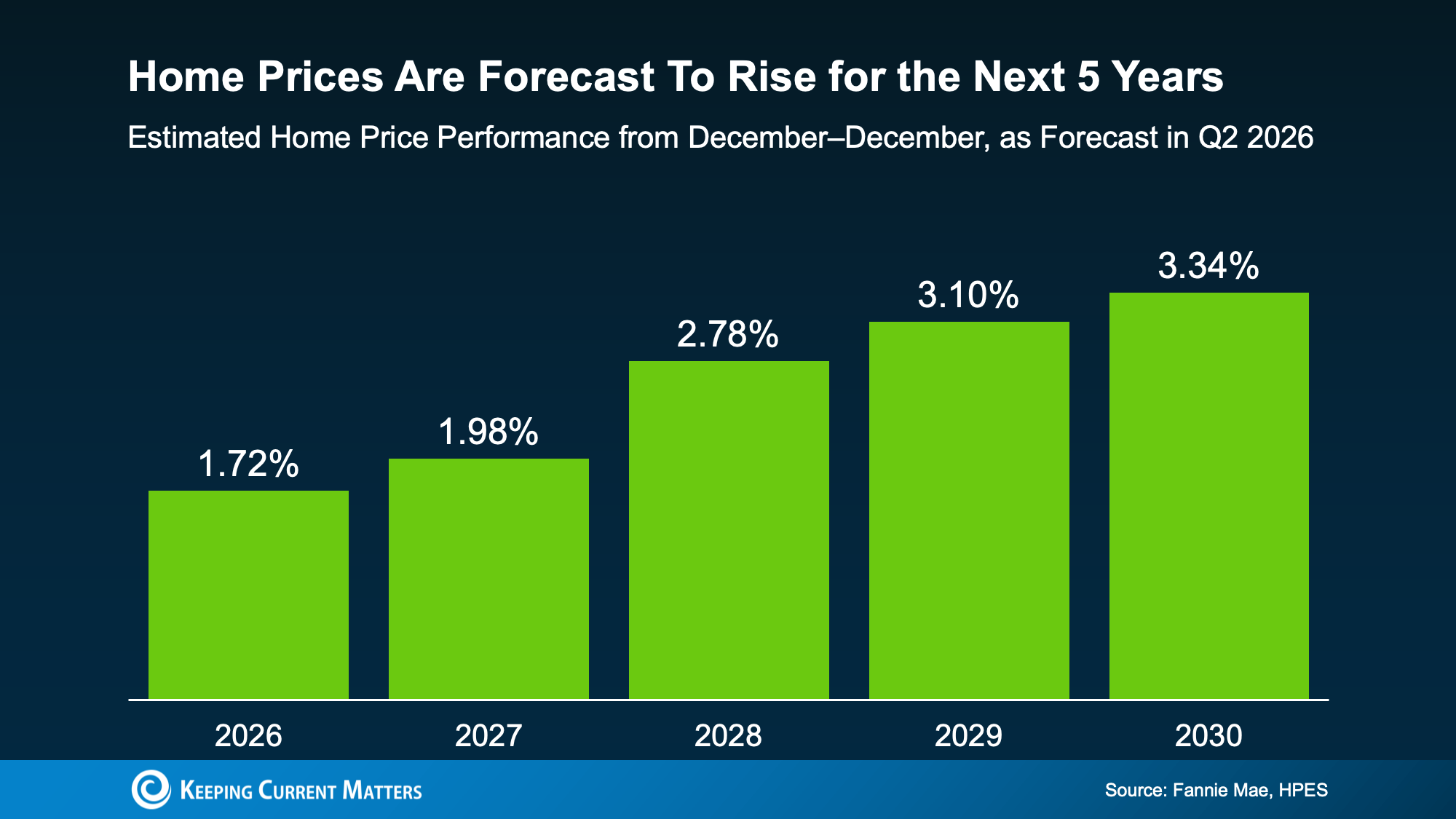

Instead, the average of their forecasts shows home prices rising every year for at least the next five years.

The expectation is for home prices to grow at a more normal pace, unlike the spikes we saw five years ago.

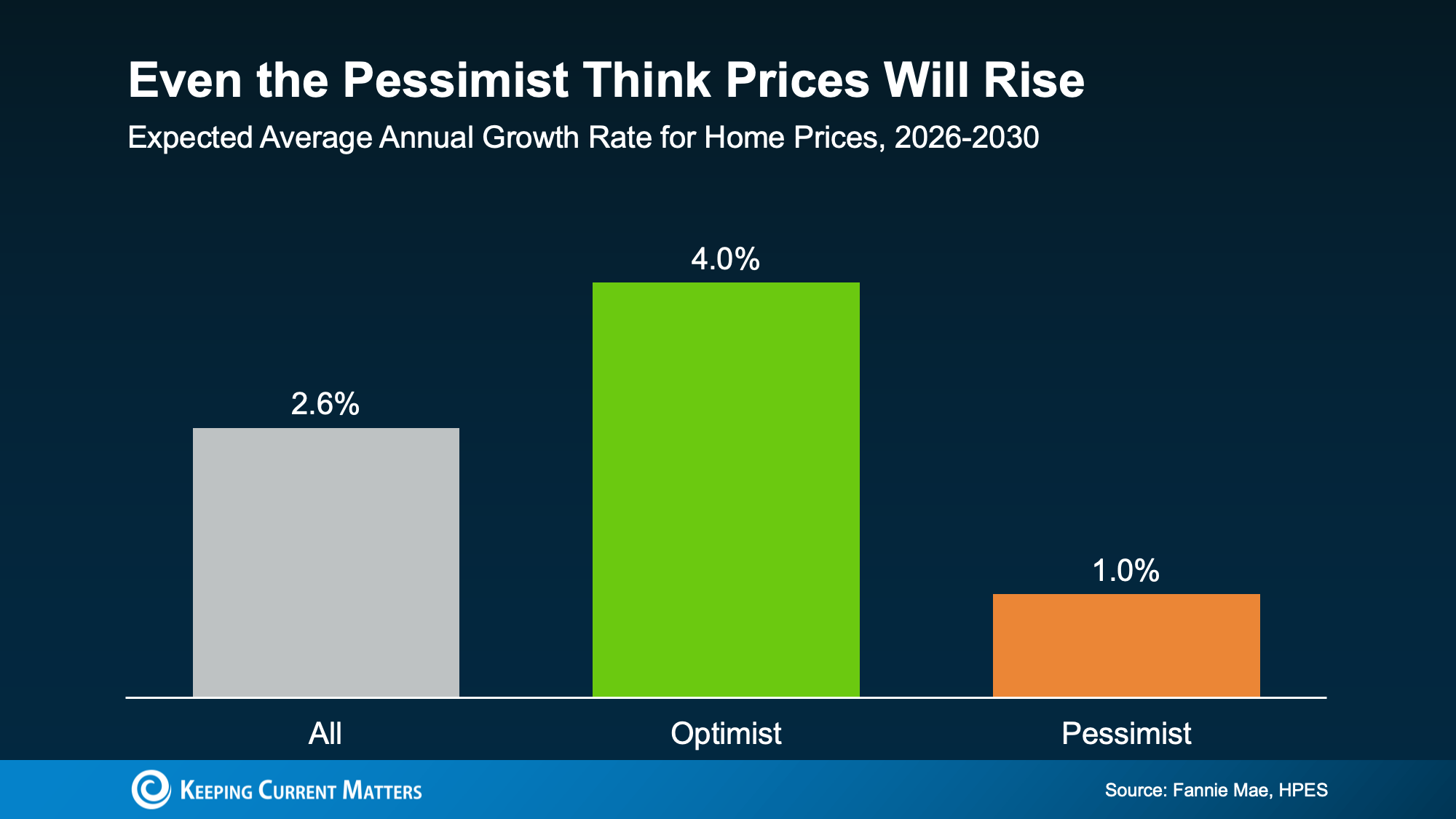

Even the Pessimists Expect Growth

One reason the HPES is useful is that it doesn’t only include optimistic forecasts.

Researchers divided the panel into groups based on how bullish or bearish they were regarding the housing market. Even the most pessimistic group still forecasted that home prices would climb over the next five years.

- The Optimists: Forecast roughly 4.0% annual growth.

- The Pessimists: Forecast roughly 1.0% annual growth.

- The Average: Expects 2.6% annual growth.

The current debate among housing experts isn’t about whether prices will crash, but rather how much they’ll rise.

That is very different from what many buyers may be seeing on social media.

Waiting for Prices To Fall Could Cost You

If you’re waiting to buy until prices come down, you may be disappointed.

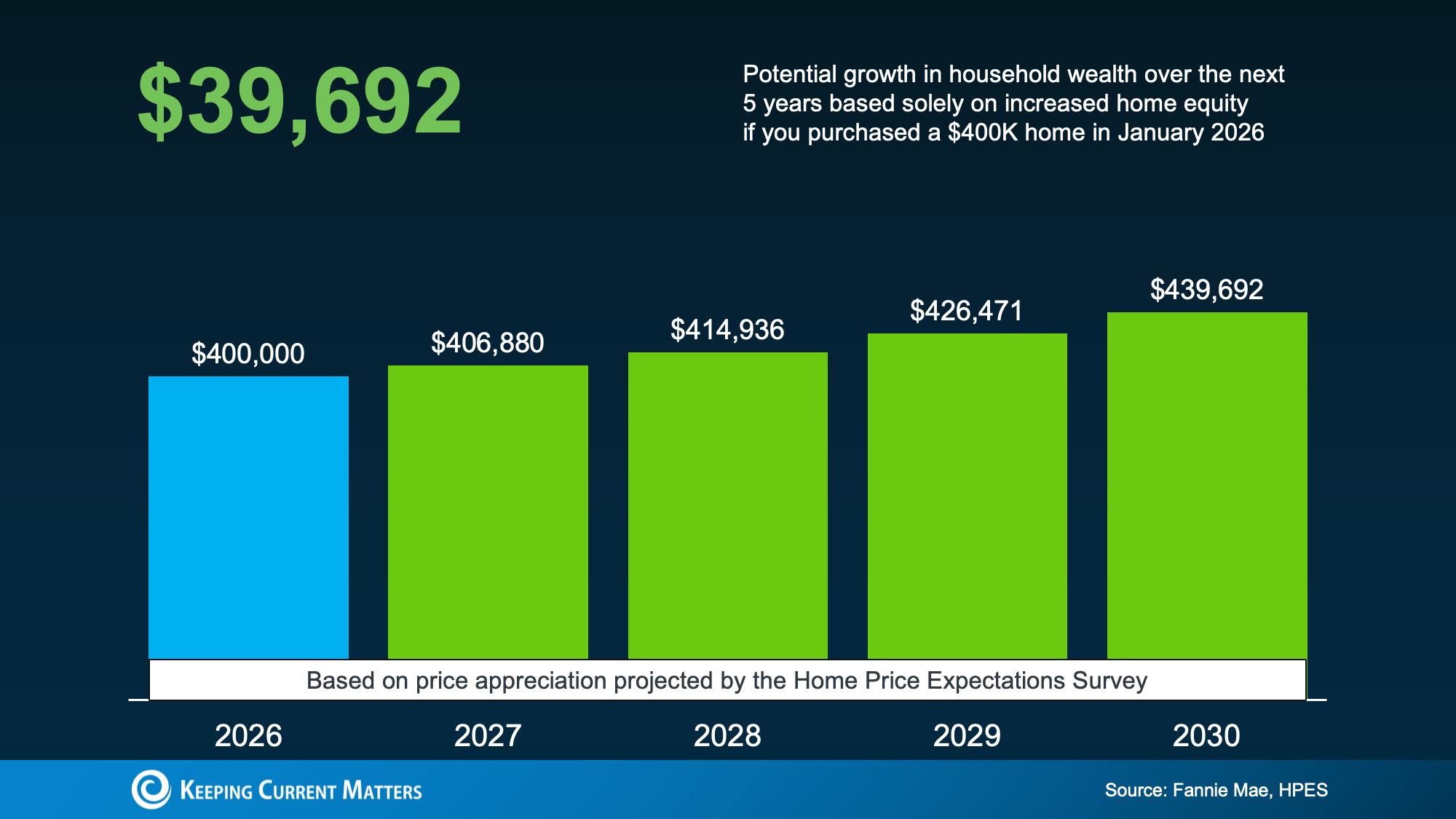

Based on the HPES forecast, a buyer who purchased a $400,000 home this January could gain nearly $40,000 in equity over the next five years from appreciation alone.

Of course, that is based on a national forecast. Real estate is local, and every market behaves differently.

But broadly speaking, the risk for buyers may not be buying before a crash. It may be waiting for a crash that never happens.

Depending on your specific market, holding off could mean missing out on considerable equity or having to pay tens of thousands of dollars more for the same house five years from now.

Bottom Line

Many buyers are waiting because they believe home prices will fall, but that’s not what experts are predicting.

Home prices are expected to rise more moderately over the next several years, and even the more cautious experts don’t expect a major drop.

Before you put your plans on hold, talk with a local real estate agent who can walk you through what’s happening in your market and help you decide what makes sense for your next move.

Two Big Reasons This Summer May Be the Right Time To Move

A lot of hopeful buyers and sellers are asking the same question right now: “Should I move this summer, or wait until later this year?”

Waiting can feel like the safer choice, especially if you’re hoping mortgage rates will drop or market conditions will feel more predictable. But there’s something important to keep in mind: rates aren’t expected to change much, so waiting may not create the advantage you’re hoping for.

Summer has historically been one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until fall or winter, some of the best seasonal opportunities may start to fade.

Here are two big reasons a summer move may be worth considering.

1. Buyers May See More Fresh Inventory in Summer

One of the biggest challenges buyers have faced in recent years is a lack of affordable options.

Maybe this sounds familiar:

- You find a home you like, but it’s outside your budget.

- You find something in your price range, but it doesn’t fit your needs.

- Or nothing new and interesting hits the market for weeks.

The Summer real estate market often helps with this.

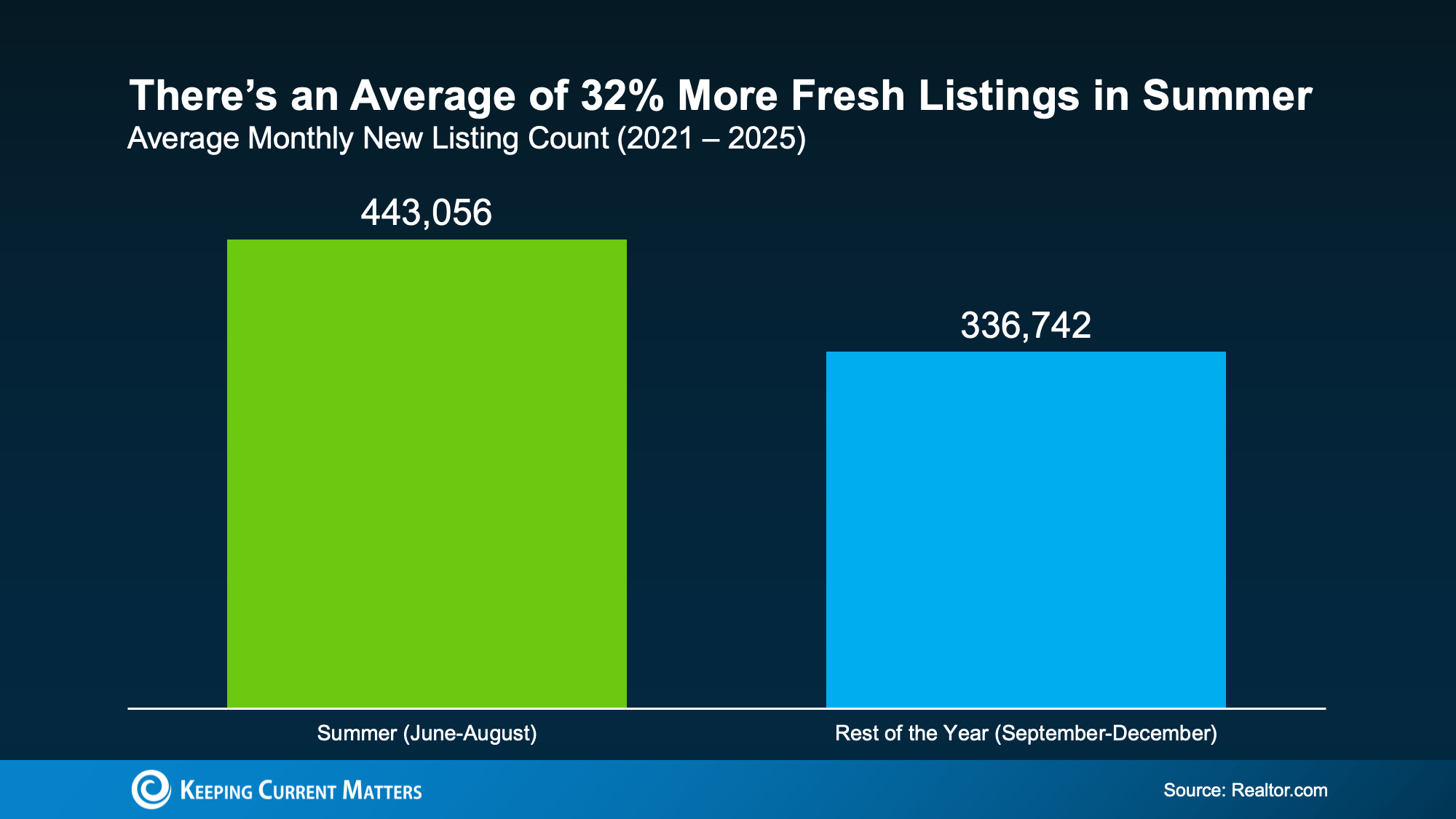

Looking at data from the Realtor.com, summer months consistently bring more sellers into the market than later in the year. This gives buyers a real window of opportunity to see fresh listings.

According to the data, any given summer month typically sees about 32% more fresh options than the average month from September through December.

As a buyer, more newly listed homes can increase your chances of finding one that fits both your wish list and your budget. After all, it takes is the one right home hitting the market to change your whole search.

Why Waiting May Limit Your Choices

The summer listing window doesn’t stick around: new inventory tends to slow once summer ends.

By fall, many homeowners who planned to sell have already listed. Some buyers and sellers who were aiming to move before school-year schedules resume may have already made their move or started the process. As a result, new listing activity usually cools heading into fall and winter.

Every year is different, and every local market has its own patterns. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options.

2. Sellers Often Benefit From Summer Seasonality

If you’re thinking about selling, you may be wondering whether now is the right time. Headlines about lower asking prices, price reductions, and softer market conditions in some areas can make it feel like the moment has passed.

But those headlines don’t tell the full story.

The market is becoming more balanced, and some areas may be experiencing price declines. Still, that does not mean sellers have missed their chance. Seasonality can still work in your favor, depending on your local market and your pricing strategy.

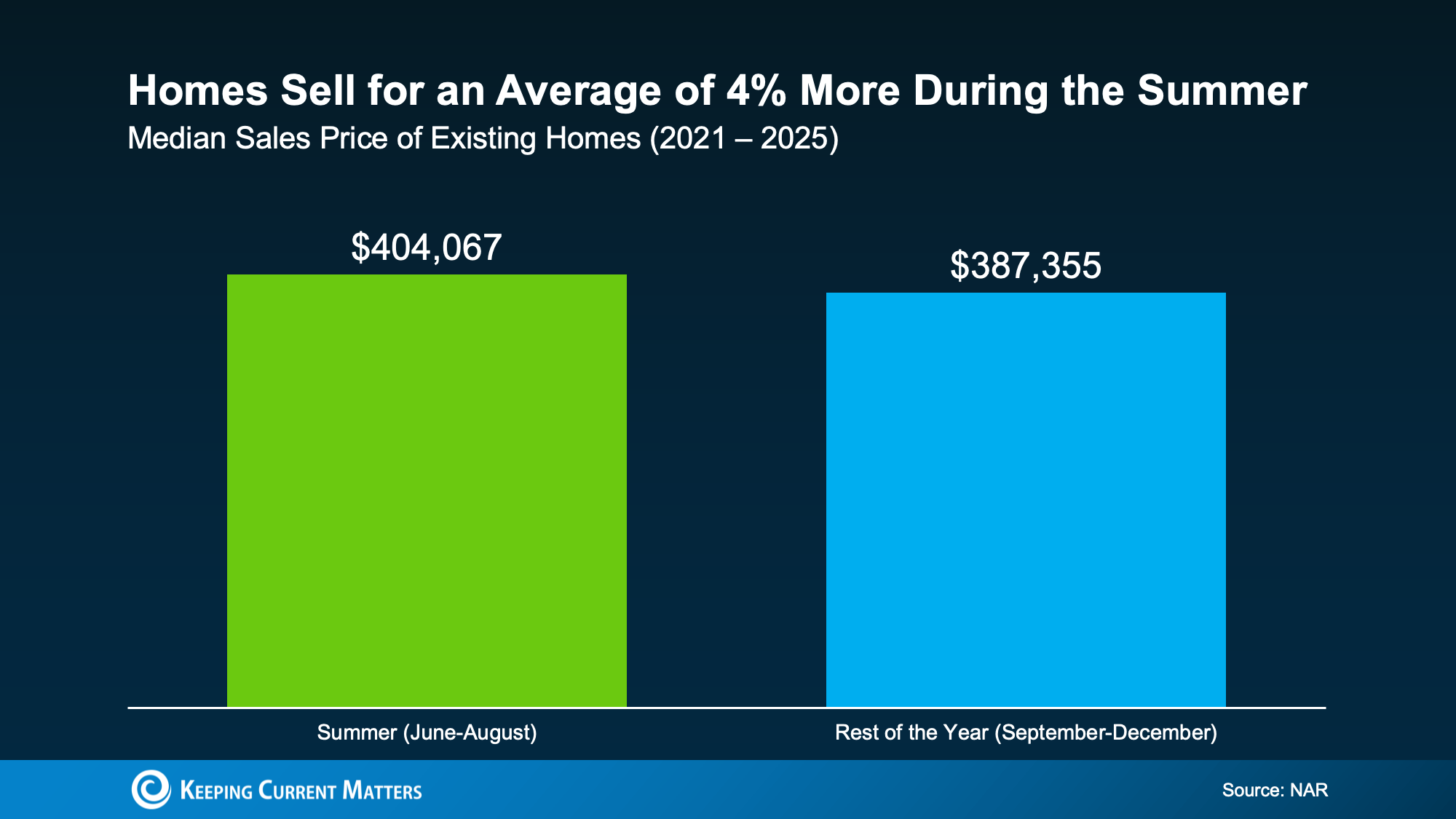

According to the National Association of Realtors (NAR), homes sold during a summer month usually sell for about 4% more than homes sold during the typical month from September through December.

With that said, this doesn’t mean you should price your home 4% higher. In today’s market, overpricing can turn buyers away and cause your home to sit longer than expected.

Instead, consider the timing of your listing. If your goal is to sell for as much as you reasonably can, listing during summer may be a stronger move than waiting until later in the year, when there are typically fewer active buyers.

Why Summer Buyers May Be Motivated

Summer buyers often have a timeline in mind. They may want to move before the next school year, take advantage of warmer weather, or use available time off to tour homes and coordinate a move.

That sense of timing can lead to stronger activity and, in some cases, better offers.

Again, this depends on your local market, your home’s condition, and how well it is priced. But if you were already considering a move in 2026, summer timing deserves a closer look.

Bottom Line

Can you still buy or sell later this year? Of course. But understanding the strengths of the summer market could make a big difference.

For buyers, summer can bring more fresh listings and better odds of finding a home you like. For sellers, summer seasonality may support stronger buyer activity and better pricing opportunities than later in the year.

If you’re planning a move in 2026, connect with a local real estate professional to talk through your goals, timeline, and market conditions. Depending on what matters most to you, summer could be the right time to make your move.

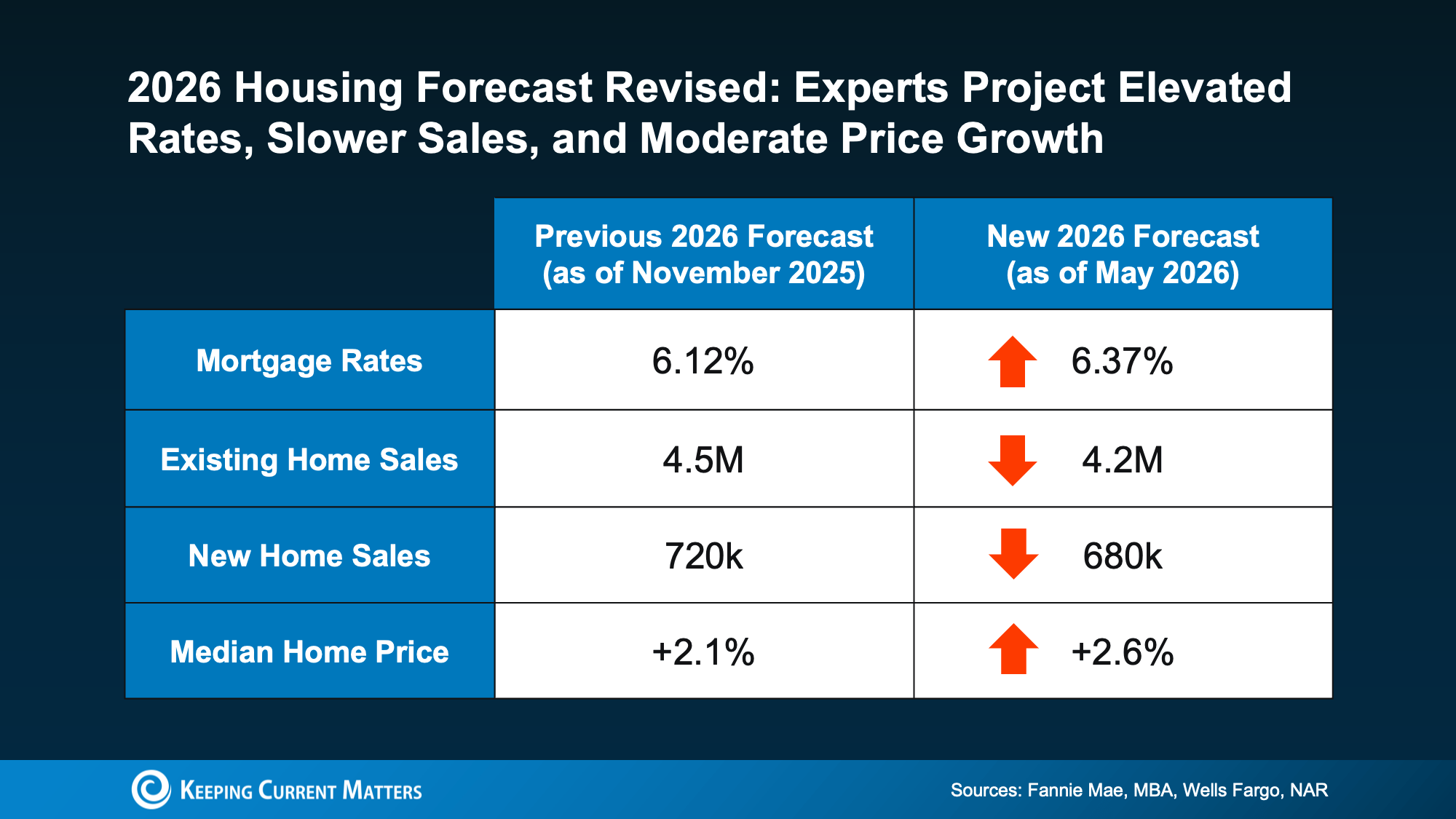

Mid-Year Housing Market Update 2026

If you’re feeling confused by the housing market right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up as quickly as many experts expected. And buyers and sellers are still waiting for affordability to improve and market activity to turn up.

The short answer? A lot changed during the first half of 2026.

At the end of 2025, economists were forecasting a stronger housing market for the year ahead. Many expected mortgage rates to come down, affordability to improve more noticeably, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. With rates staying elevated for longer, many buyers have continued to wait on the sidelines.

Unexpected factors like these have forced experts to revise their housing forecasts for the rest of the year.

Experts are now projecting elevated mortgage rates (6.37%) and a dip in total home sales. However, home values remain resilient with a projected 2.6% growth in median prices.

So, what does this mid-year housing market update actually mean for you? Let’s break it down.

Mortgage Rates May Stay Elevated Longer Than Expected

Just about everyone would like to see mortgage rates return to the upper 5s or low 6s we saw earlier in the year. But based on current forecasts, experts don’t expect that to happen this year.

Instead, many industry organizations now expect mortgage rates to stay closer to the mid-6% range in 2026. The good news is that this is still lower than rates were a year ago.

Of course, forecasts can change. If inflation cools or overseas conflicts ease, mortgage rates could shift again. But for buyers waiting for a major rate drop, the payoff may not be as big or as immediate as hoped.

For many buyers, the better question may be: Can you comfortably afford a home at today’s rate? If the answer is yes, waiting may not automatically put you in a stronger position.

Existing Home Sales Were Revised Lower

At the end of 2025, experts expected existing home sales to average around 4.5 million in 2026. That forecast has now been revised down to about 4.2 million.

That change tells us something important: affordability is still a challenge, and many buyers remain hesitant.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. As a result, the market has moved more slowly than originally expected.

But there is still some positive news. Even with the revised forecast, experts still expect more homes to sell this year than last year.

There’s also a pool of buyers who may re-enter the market once rates settle and uncertainty eases. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

Recent improvements in pending home sales also suggest some buyers are starting to move forward again, even with rates still elevated.

For today’s buyers, that’s a big deal. If you can afford a home now, buying before more buyers return could mean less competition than you might face later.

New Home Sales Also Slowed

Builders also expected a stronger year.

Earlier forecasts projected new home sales would top 700,000 in 2026. Now, economists expect new home sales to come in just under that number.

Once again, mortgage rates are a major reason why.

But for buyers, there may be an upside. When new home sales slow, builders may become more motivated to sell available inventory. Depending on the market, that could create opportunities for:

- Builder incentives

- Closing cost assistance

- Price flexibility

- Negotiation on upgrades or finishes

This doesn’t mean every builder will negotiate, and incentives vary by location. But in areas with more new construction, buyers may have more leverage than they would in a a more active market.

Home Prices Are Still Expected To Rise

Here’s one of the biggest takeaways from this mid-year housing market update: even though sales activity has slowed, experts did not revise national home price forecasts downward.

They still expect home prices to rise nationally this year.

Why? Because buyer demand has softened, but the overall number of homes for sale remains relatively limited. That imbalance continues to support prices, even in a slower market.

Local conditions can vary; some markets are cooling more than others, and pricing trends depend heavily on inventory, buyer demand, property condition, and location.

Still, experts are projecting steady price growth rather than a major decline, at least at the national level.

That can be reassuring whether you’re buying or selling. Sellers generally don’t want to see a sharp drop in values. And buyers may feel more confident about a major purchase when prices aren’t expected to fall significantly right away.

What This Means for Buyers

For buyers, the updated 2026 housing market forecast is a reminder to focus on what you can control.

Mortgage rates may not fall as quickly as hoped, but that doesn’t mean buying is off the table. A local real estate agent can help you understand what’s happening in your specific market, including inventory levels, price trends, and negotiation opportunities.

Before making a move, think about reviewing:

- Your current budget

- Estimated monthly payment at today’s rates

- Available homes in your preferred price range

- Local competition from other buyers

- New construction options and possible builder incentives

You should also speak with a trusted mortgage professional to understand loan options, rate scenarios, and affordability based on your situation.

What This Means for Sellers

For sellers, slower sales activity doesn’t point to a stalled market.

Buyers are still active, but many are more selective thanks to tighter affordability. That makes pricing, preparation, and marketing even more important.

A strong selling strategy should include:

- A realistic pricing plan based on current local data

- Thoughtful preparation before listing

- Professional marketing that highlights the home clearly

- Flexibility around buyer questions, timelines, and negotiations

With home prices still expected to rise nationally, many sellers may still be in a strong position. A successful sale will depend on understanding your local market, not relying on broader national headlines.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. Still, the market hasn’t totally stalled.

Higher inflation, economic uncertainty, and global tensions caused economists to revise their 2026 housing market forecasts. Mortgage rates are expected to remain higher than originally projected, and home sales forecasts have been adjusted lower.

Even so, more homes are still expected to sell this year than last year, and national home prices are still projected to rise.

The key is to make decisions based on your own local market, budget, and goals.

If you want to understand what this mid-year housing market update means for your next move, connect with our team. We can help you review local trends, explore your options, and decide what makes sense for the rest of 2026.

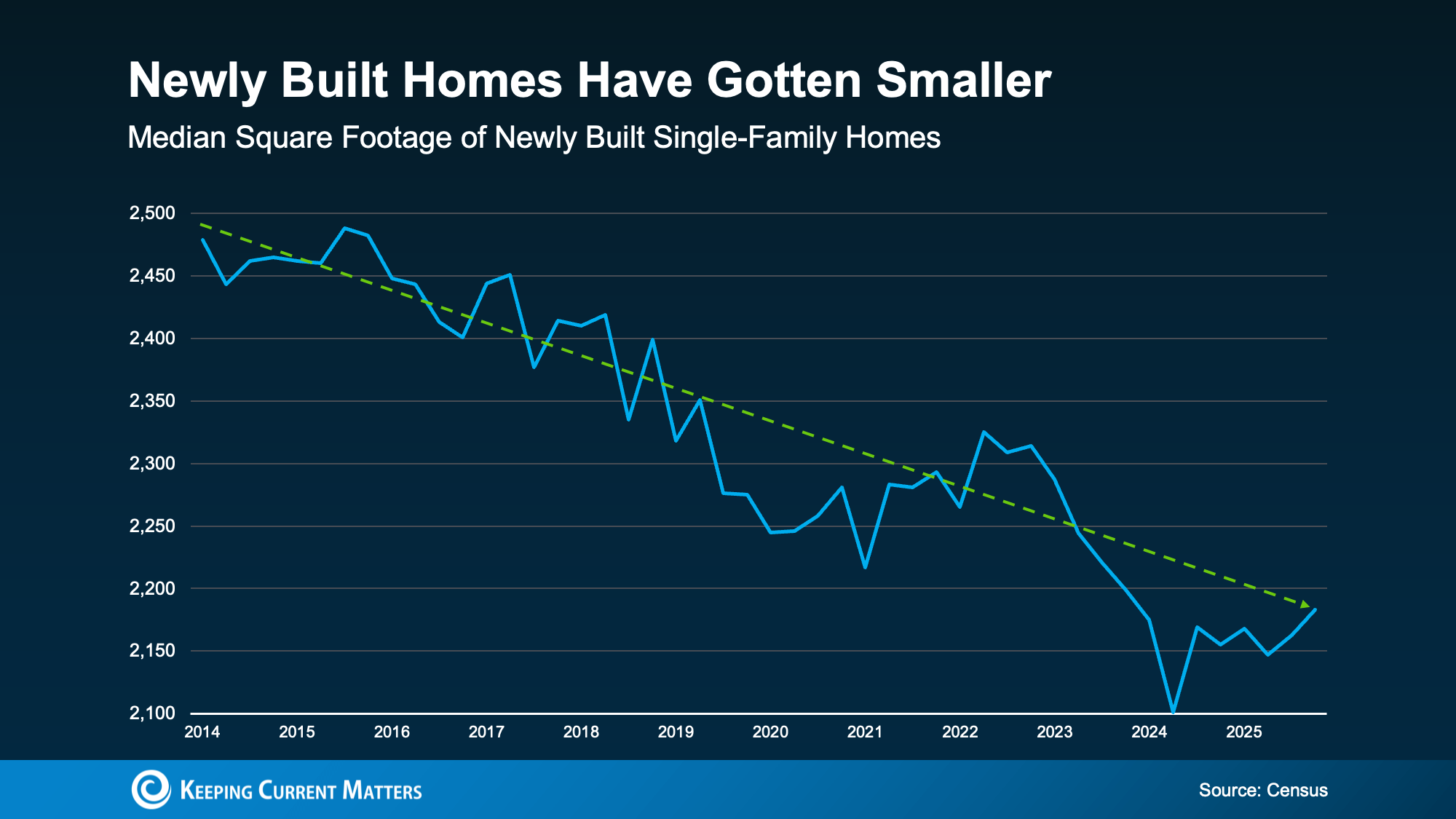

Smaller Homes, Bigger Value for Today’s Buyers

You might have started your home search with a simple picture in mind: a certain number of bedrooms, a spacious layout, maybe even a home office or dedicated workout room.

Then reality sets in. The homes that fit your budget may be smaller than what you originally imagined.

That’s a common experience for many buyers right now. Affordability is tight, and buyers are taking a closer look at what they truly need in a home. But going smaller doesn’t need to feel like a compromise.

In fact, smaller homes for buyers can offer real advantages in today’s market, especially when considering newer construction, condos, and communities designed with shared amenities.

Why Smaller Homes Are Getting More Attention

Smaller homes are not just a backup plan. They have become a more practical path for many buyers who want to balance comfort, location, and budget.

In fact, newly built homes have been getting smaller for years, and the median square footage of new single-family homes has generally declined since 2014, based on US Census data.

This shift makes sense. Builders pay close attention to what buyers are not only willing, but able to purchase. When affordability becomes a bigger concern, smaller floor plans can help bring new homes within reach for more shoppers.

Smaller New Construction Homes May Be Worth a Look

If the existing homes in your price range aren’t checking enough boxes, it may be time to explore new construction.

Many builders are focusing on smaller homes with modern layouts, updated finishes, and move-in-ready features. Smarter designs can make a smaller footprint feel more functional than an older home with a less efficient floor plan.

A smaller, newer home may offer:

- Modern appliances and finishes

- Open, practical layouts

- Less unused space

- Move-in-ready convenience

- A price point that may better fit your budget

Shifting buyer preferences are a big reason that new home prices have hit a five-year low. If you’ve ruled out new construction in the past, you want to take another look at what builders are offering in your area.

Condos Can Open Another Path to Homeownership

New construction isn’t available everywhere, and in some markets, it may still be outside your budget. That is where condos can be worth considering.

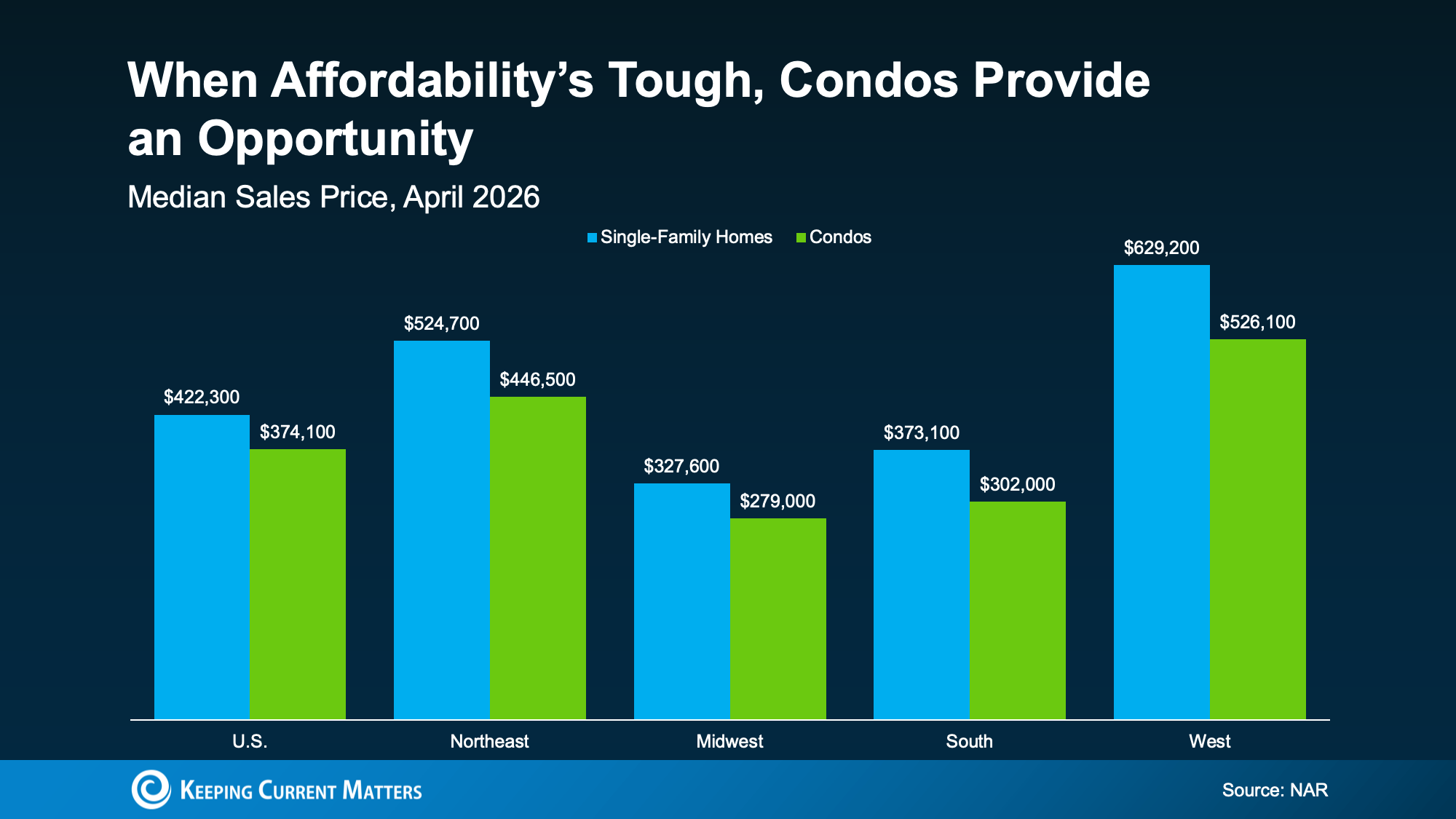

Condos are often smaller than single-family homes, which can help reduce the overall purchase price. According to data from the National Association of Realtors (NAR), the median condo price is lower than the median single-family home price in every region.

For buyers trying to make the numbers work, this is a considerable difference.

According to NAR, condo sales rose 2.7% last month, and were up year over year. And value is a driving factor. Ali Wolf, Chief Economist for New Home Source, explains:

“In addition to favoring smaller floor plans, more consumers are showing a willingness to live in an attached home. This shift is not driven by a preference for shared walls, but by a pursuit of value.”

For buyers focused on affordability, condos can offer a way to stay active in the market without stretching too far for a detached single-family home.

The Right Community Can Make a Smaller Home Feel Bigger

Square footage is important, but it’s only one part of a home’s blueprint.

A smaller home may still work well if the surrounding community gives you access to amenities that extend how you live day to day. In some condo communities, neighborhoods, and master-planned developments, shared spaces help fill in the gaps.

Depending on the community, amenities may include:

- Walking trails

- Pools

- Fitness centers

- Co-working spaces

- Outdoor gathering areas

Features like these can make a smaller home feel more livable, and functional. For example, if there’s no room for a home office, a nearby co-working space can help. If you don’t have space for a dedicated workout room, a shared fitness center can fill the gap.

Buying a Smaller Home Does Not Mean Giving Up Comfort

A smaller home can still support the way you want to live. Focusing less on total square footage and more on how the space works can offer a different perspective.

As you compare options, consider:

- Layout: Does the floor plan make daily routines easier?

- Storage: Are closets, cabinets, and garage space used efficiently?

- Natural light: Does the home feel open and comfortable?

- Shared amenities: Does the community offer spaces you would actually use?

- Location: Does the home keep you close to the places that matter to you?

A smaller home with the right layout, features, and setting may be a better fit than a larger home that stresses your budget or needs more work.

Bottom Line: Smaller Homes Can Offer Bigger Opportunities

Today’s smaller single-family homes and condos have more to offer than their square footage might suggest. They can give buyers more budget flexibility, access to newer features, and opportunities to live in communities designed with useful amenities.

If your current search feels limited, consider widening your options. A smaller home, new build, or condo may offer opportunities you never knew existed.

Curious about smaller homes, condos, or new construction options in your area? Contact our brokerage to explore what’s available and compare homes that fit your budget and goals.