Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

3 Things That Aren’t Going To Happen in Today’s Housing Market

There’s no shortage of uncertainty in today’s housing market, and that’s naturally fueling a lot of dramatic headlines. And if you’re trying to buy a home, that kind of noise can make your decision feel a lot more complicated.

In fact, a recent CNBC study asked homebuyers what they’re most concerned about, and the same three topics kept rising to the top:

- Mortgage rates

- The number of homes for sale

- Home prices

The challenge is that much of what people are hearing about these topics is driven by misconceptions, not facts. Let’s separate the headlines from what the data is really showing.

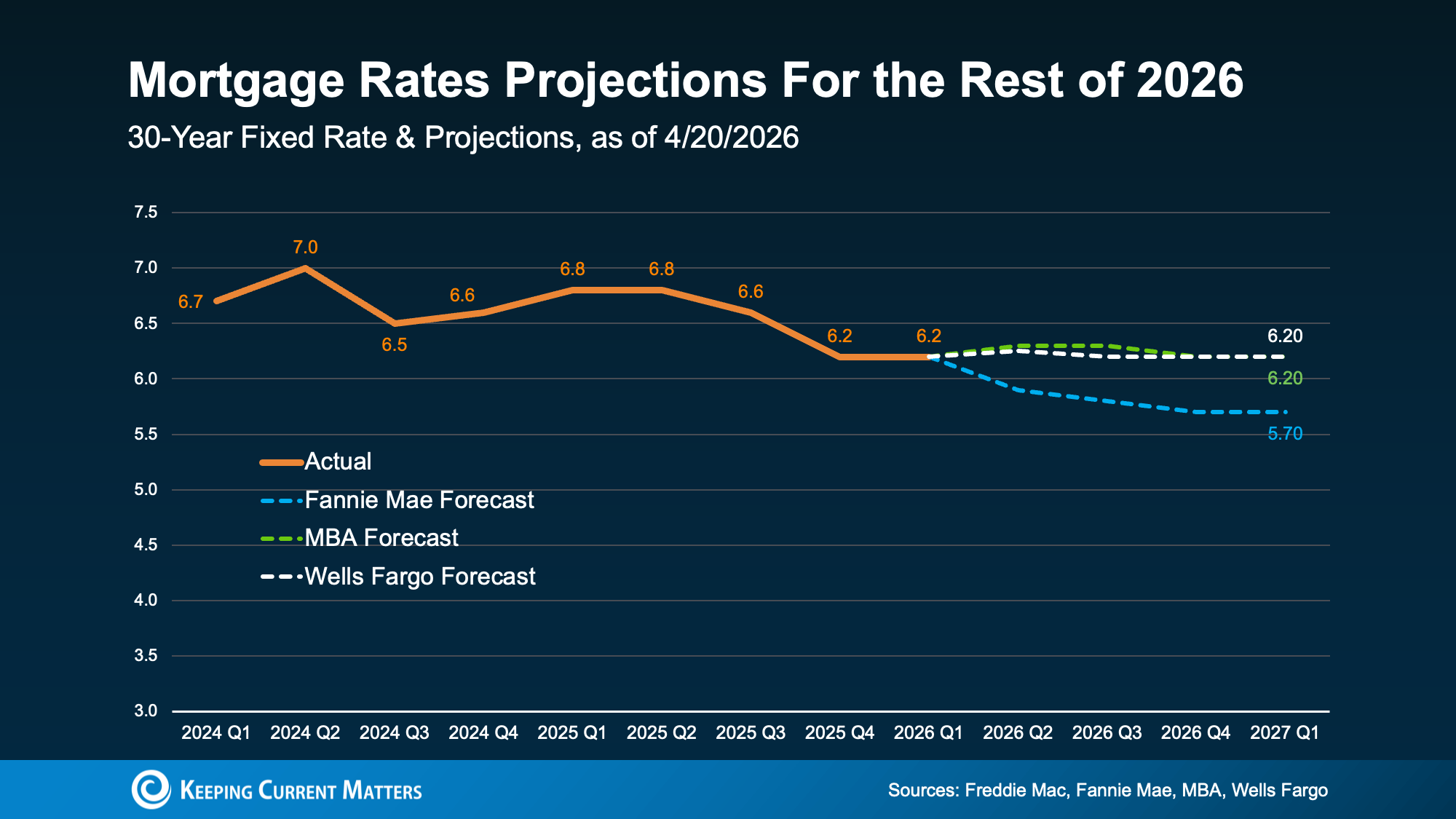

Misconception #1: “I Should Wait Because Mortgage Rates Are Going To Fall Dramatically”

One of the most common ideas circulating on social media is that mortgage rates are about to drop sharply, so waiting to buy is the smarter move.

But is that what experts are expecting?

While mortgage rates have eased a little in recent weeks, forecasts still aren’t predicting any major declines. It’s more likely that rates will stay in the low 6% range this year.

And that’s not a remarkable shift from the rates we’re seeing today:

Obviously, a lot depends on inflation and the broader economy. But based on what we know right now, waiting for a big drop in mortgage rates may not play out the way many buyers hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

And even with rates where they are today, buying a home is already more affordable than it was a year ago. Even if rates don’t drop in the near future, home affordability is better now than a year ago.

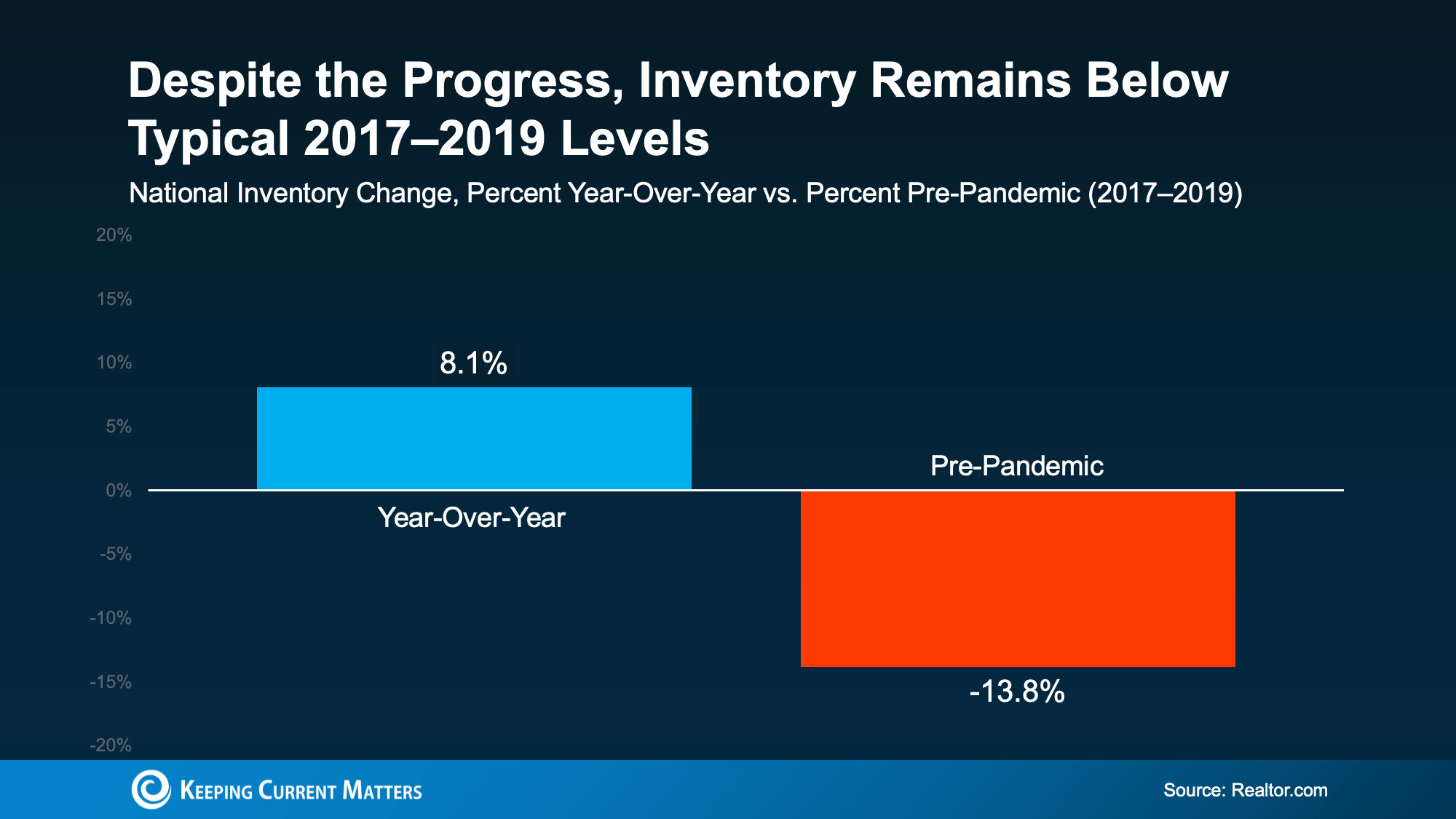

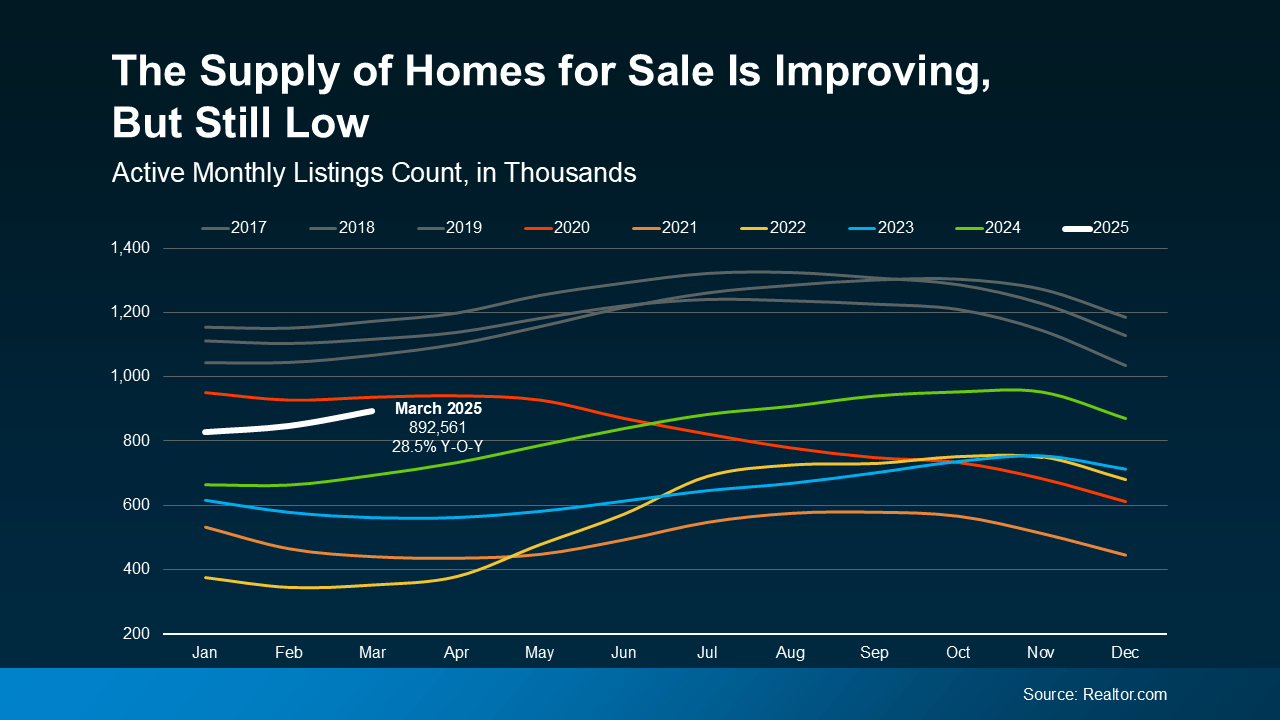

Misconception #2: “There Are Too Many Homes for Sale”

You may have heard that housing inventory is rising. Nationally, that’s true: the number of homes for sale is 8% higher than it was at this time last year. But that’s not bad news. In lots of markets, it’s easing the pressure on buyers.

The problem is that some headlines make good news sound like bad news. They focus on the fact that inventory is at its highest level since 2019 or highlight how many new homes builders are adding. That can make it sound like supply is growing too much, too fast.

But the bigger picture tells a different story.

According to new Realtor.com data, even though inventory is up over last year, it’s still nearly 14% lower than it was in the last normal housing market from 2017 to 2019:

And while local conditions vary, only 9 states have more inventory now than they did before the pandemic. That’s a major reason there aren’t enough homes for sale to trigger anything like the 2008 housing crash.

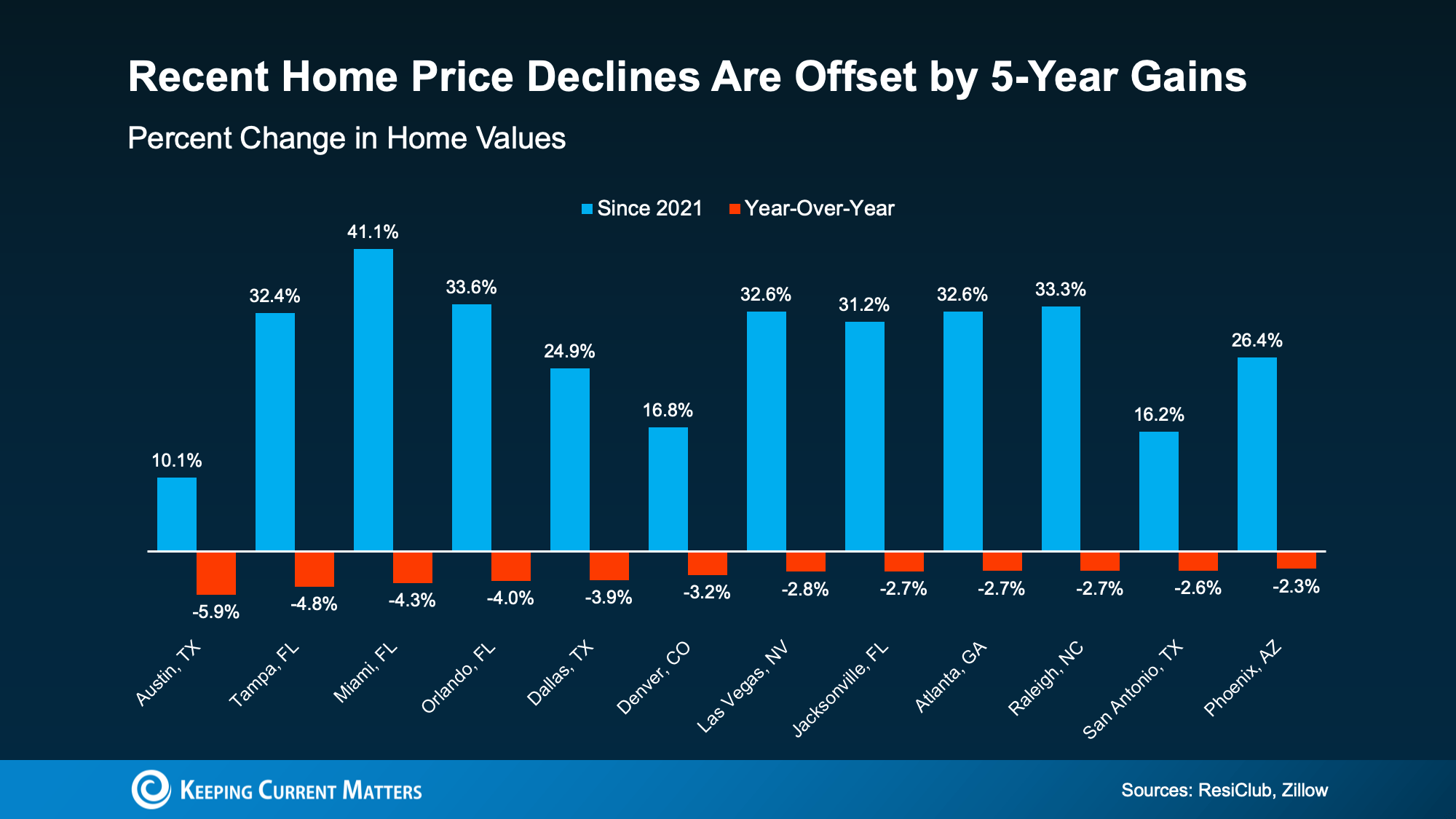

Misconception #3: “Home Prices Are About To Crash”

This is another common headline you’ve probably seen. This misconception comes from the fact that a few metros are actually seeing small price declines. Influencers are pointing to this to claim home prices are crashing. But this is absolutely not true nationally.

In most markets, home prices are still rising, not falling. Here’s why:

- Many homeowners are choosing not to sell to avoid giving up the low mortgage rate they locked in a few years ago. That continues to limit how much inventory can grow.

- Inventory remains below pre-pandemic norms. There still aren’t enough homes for sale to cause a widespread price crash.

- Even in markets with more listings, some sellers are pulling their homes off the market instead of making major price cuts.

Those are three big reasons home prices are not on track for a crash.

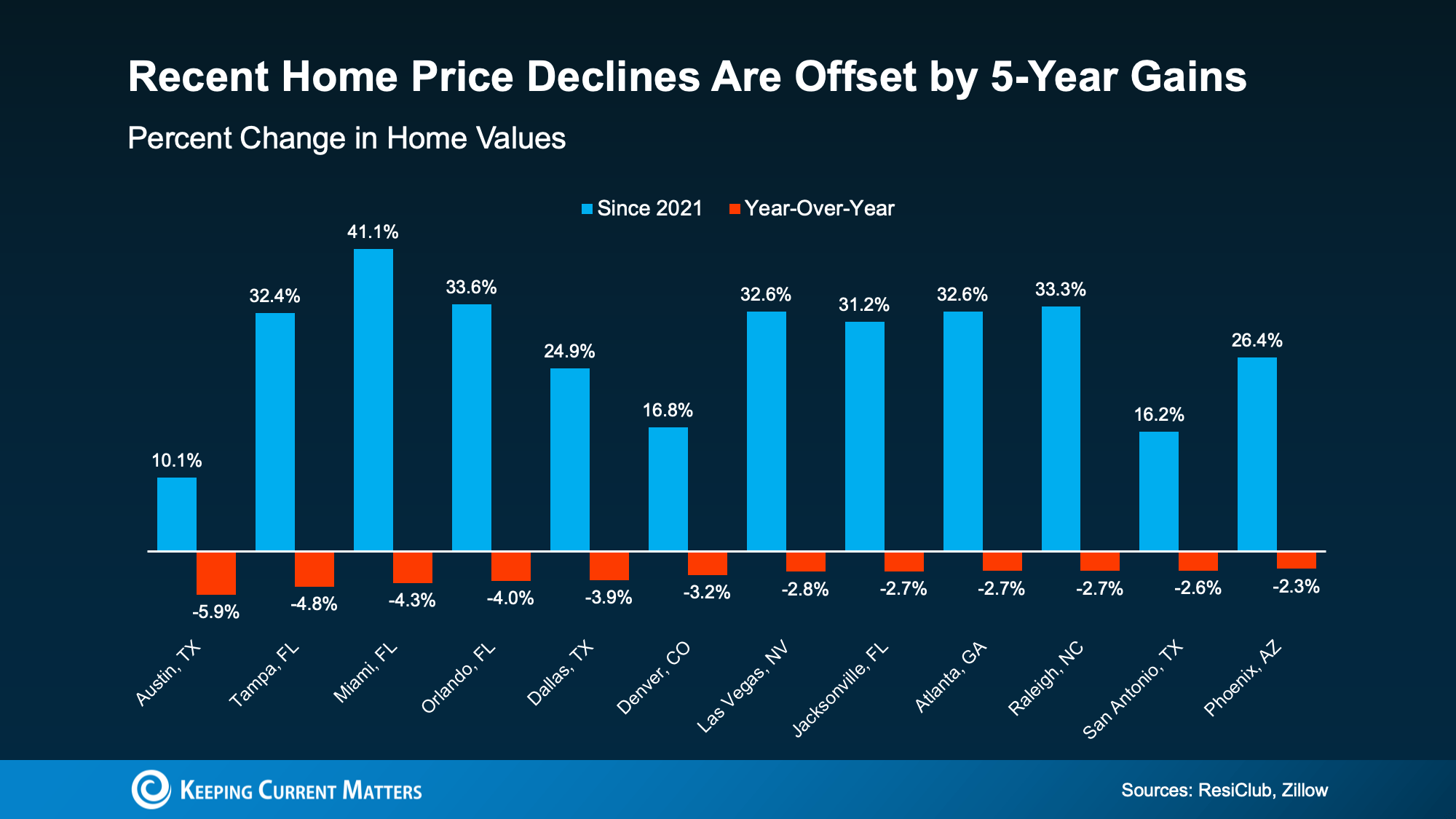

And even in the areas seeing small price declines, those drops are nowhere near enough to erase the huge gains most homeowners have built over the past five years:

These drops don’t signal a crash. They show the market settling after a few years of record-breaking spikes in prices.

Bottom Line: Get the Facts on Your Market

The discussions we see online can often exaggerate the negative and ignore the positive, especially in housing. If you want a clearer, truer idea of what’s happening with mortgage rates, housing inventory, and home prices in your market, talk to a trusted real estate professional.

Connect with a local real estate agent so you have an expert who can give you the real story on your local housing market.

Are Home Prices Dropping? What the Latest Data Show

You’ve probably seen headlines or social posts claiming that home prices are falling. It’s an attention-grabbing message, and it naturally leads to two big questions:

- Is this the start of a crash?

- What does it mean for my home’s value?

Here’s the reality: a few markets are seeing small, normal pullbacks, but this is not a nationwide crash. In most areas, prices are still rising or holding steady, just not at the breakneck pace we saw a few years ago.

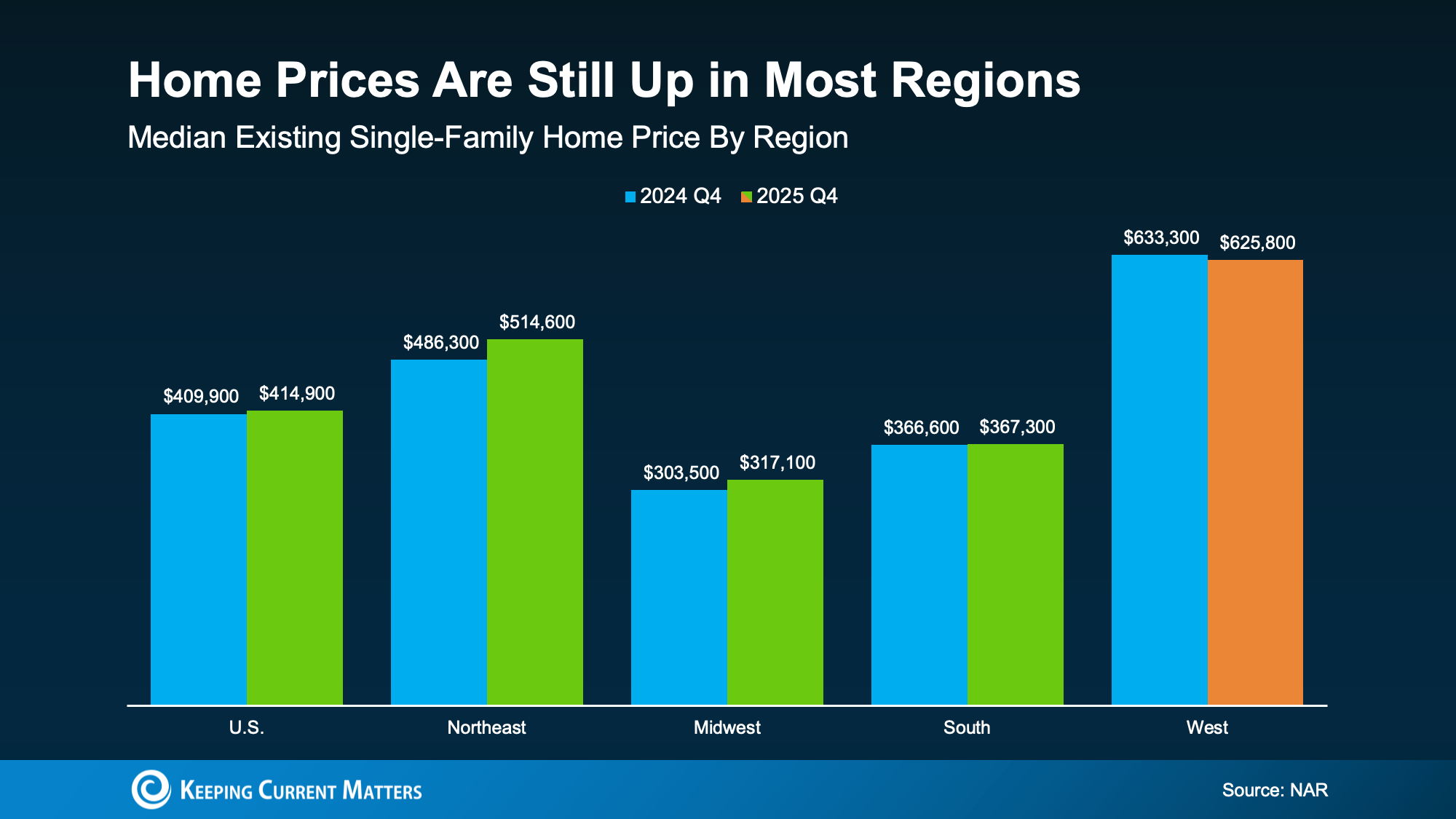

Home Prices Are Still Rising Nationally

A lot of online chatter focuses on isolated price drops without mentioning the broader data. Nationally, prices have continued to trend upward, but at a slower rate than usual.

According to a new report from the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s modest growth compared to the peak “boom” years, but it’s still growth. And regionally, the story varies.

At a glance, the numbers show:

- Northeast, Midwest, and South: prices generally up or steady.

- West: more mixed, with some markets seeing mild price declines.

In other words, the market is cooling and normalizing, not crashing.

Why You’re Hearing So Much About Price Drops

Price declines make for clickable headlines. But a few factors can make a local shift look like a national trend:

- High-profile metros go viral. A dip in one major market can dominate the conversation.

- Seasonality is real. Some months are softer than others, even in healthy markets.

- Affordability has cooled demand. Higher payments can reduce competition and push prices to level off.

Those are signs of a market adjusting, not collapsing.

Some Markets Have Softened, But Context Matters

In the places where prices have dipped, it helps to look at the big picture. Many of those markets saw especially strong appreciation over the last several years. When you compare today’s values to where they were five years ago, homeowners in many “down” markets are still up significantly overall.

According to data from ResiClub and Zillow, price dips in the short-term aren’t always the cause for concern they seem to be. The long-term trends tell a clearer story, and they remain strong for many homeowners.

The key point: a pullback after rapid growth is not the same thing as a crash. It’s often a correction toward something more sustainable.

What This Means for Homeowners and Buyers

If you’re a homeowner:

In most markets, you’re not watching value evaporate overnight. Instead:

- You likely still have meaningful equity compared to pre-2020 values.

- Pricing strategy matters more now that buyers aren’t automatically overbidding.

- The best indicator is recent comparable sales in your neighborhood.

If you’re a buyer:

A cooler market can create more breathing room:

- You may see more negotiability in certain areas.

- You may have more time to decide than during the peak frenzy.

- But waiting for a big “crash” could mean missing the right home if your local market is stable.

Real estate is local. The best move depends on your budget, timeline, and the neighborhood you want.

How to Know What’s Happening Where You Live

National headlines can’t tell you what’s happening on your street. To get a clear picture, look at:

- Recent sold prices (comps) for similar homes.

- Days on market and list-to-sale price ratios.

- Inventory levels and new listings.

- Price reductions on comparable listings.

A local real estate agent can help make sense of your market’s unique trends. That way, you know you’re relying on sound information for any decision you make.

Conclusion

Home prices are rising or holding steady in most parts of the country, and a handful of small declines does not equal a nationwide downturn. If you want to know what your home is worth today, review your local numbers with a trusted real estate professional.

How Could a Recession in 2025 Affect the Housing Market?

As talk about economic slowdowns runs wild, worries about a potential recession in 2025 are on the rise. Naturally, many homeowners are wondering what a recession could do to the value of their home, and their buying power.

Using historical data from recessions of decades past, let’s see how a recession might affect the housing market in 2025.

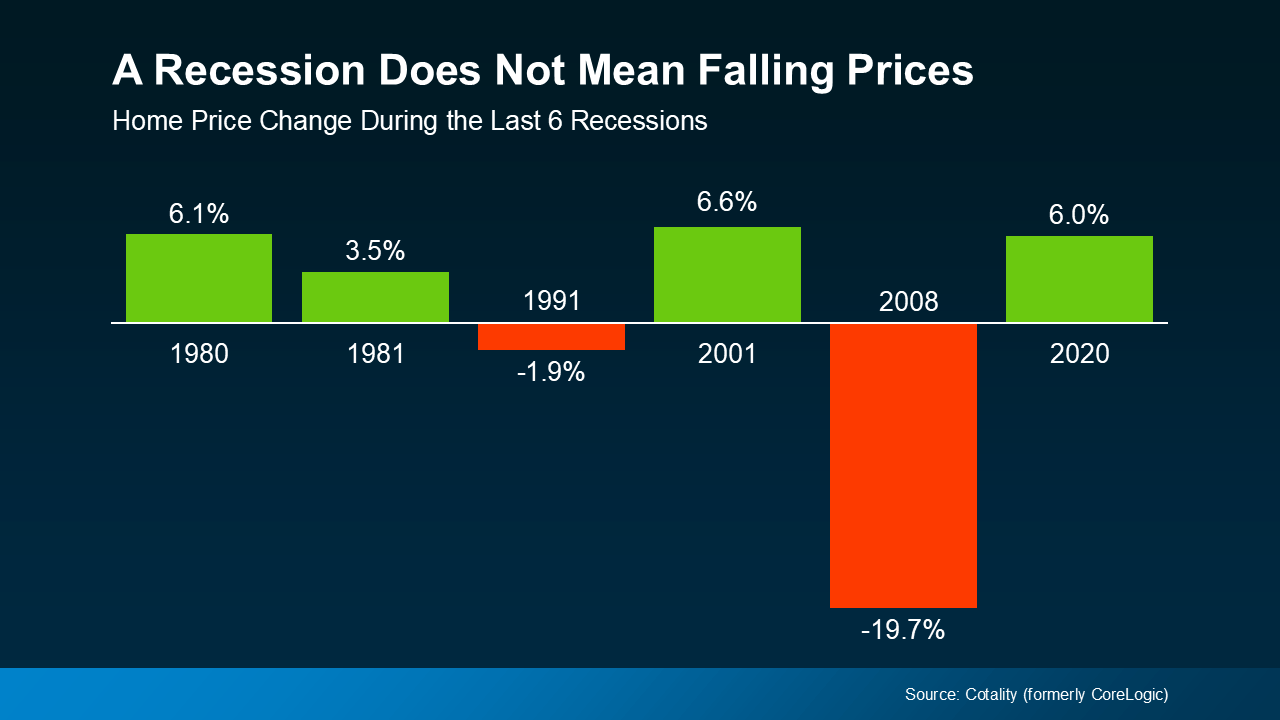

A Recession Won’t Lower Home Prices

It’s a common misconception that a recession will cause home prices to crash, like they did in 2008. In reality, 2008 was the only time the housing market saw such an extreme, dramatic drop in prices. Overflowing home inventory caused that price crash, and conversely, low inventory has prevented a similar crash in the years since.

Even in markets where housing inventory is up, it’s still far below the listing oversupply that caused the 2008 crash. Indeed, according to data from Cotality, home prices actually increased during four of the last six major recessions.

As the graph shows, a recession doesn’t necessarily mean that home prices will crash, or even drop. In reality, historical data shows that home prices usually continue along their current trajectory when a recession hits. And at the moment, home prices are still rising nationally, but at a more normalized rate. So, as the market stands now, a recession in 2025 would most likely drive prices even higher.

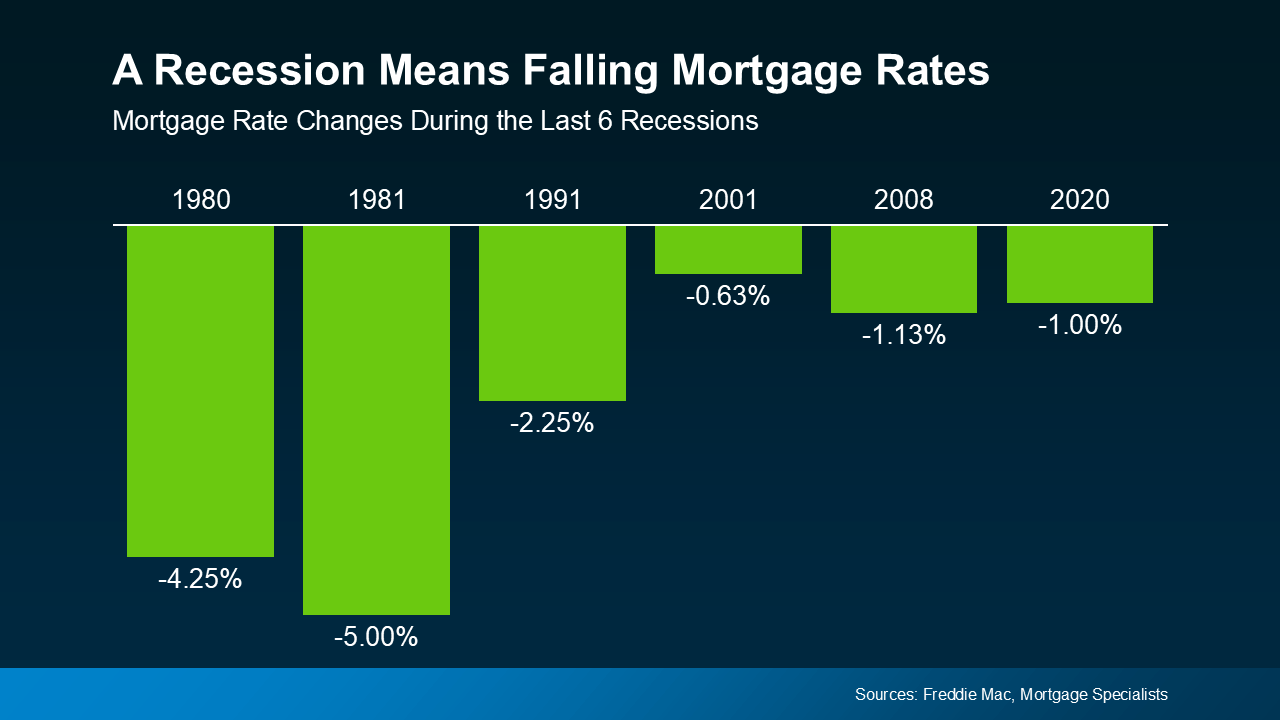

Mortgage Rates Typically Decline During Recessions

Home prices may stay their path during economic slowdowns, but mortgage rates actually tend to drop. Looking again at historical data from the last six recessions, this time from Freddie Mac, mortgage rates fell each time.

Historically speaking, a recession could mean that mortgage rates may even decline this year. However, the last time a recession dramatically lowered mortgage rates was over three decades ago in 1991. So with that said, even if a recession does happen, don’t expect a game-changing drop in mortgage rates.

Conclusion

Nobody ever truly knows what the economy will do, but the odds of a recession in 2025 have increased. Still, a recession doesn’t mean you need to worry about the housing market or the value of your home. The historical data tells us that a recession may even drive home prices higher and mortgage rates lower.

Wondering how an economic slowdown could impact your local market? Connect with us to get the info you need to plan ahead.

Foreclosures Rose in Q1 2025 – Is It a Warning Sign?

With everyday costs seemingly rising across the board, the state of the housing market is a natural concern. When basic living expenses rise, even critical financial responsibilities like mortgage payments start to slip, leading to increased foreclosures. Unsurprisingly, new data shows filings for foreclosures rose in Q1 2025, stirring worries about another housing crash like in 2008.

But as it turns out, there’s less cause for worry than you might think. When contextualized correctly, it’s clear these new number don’t point to a repeat of the last big housing crash.

The 2008 Market Versus 2025

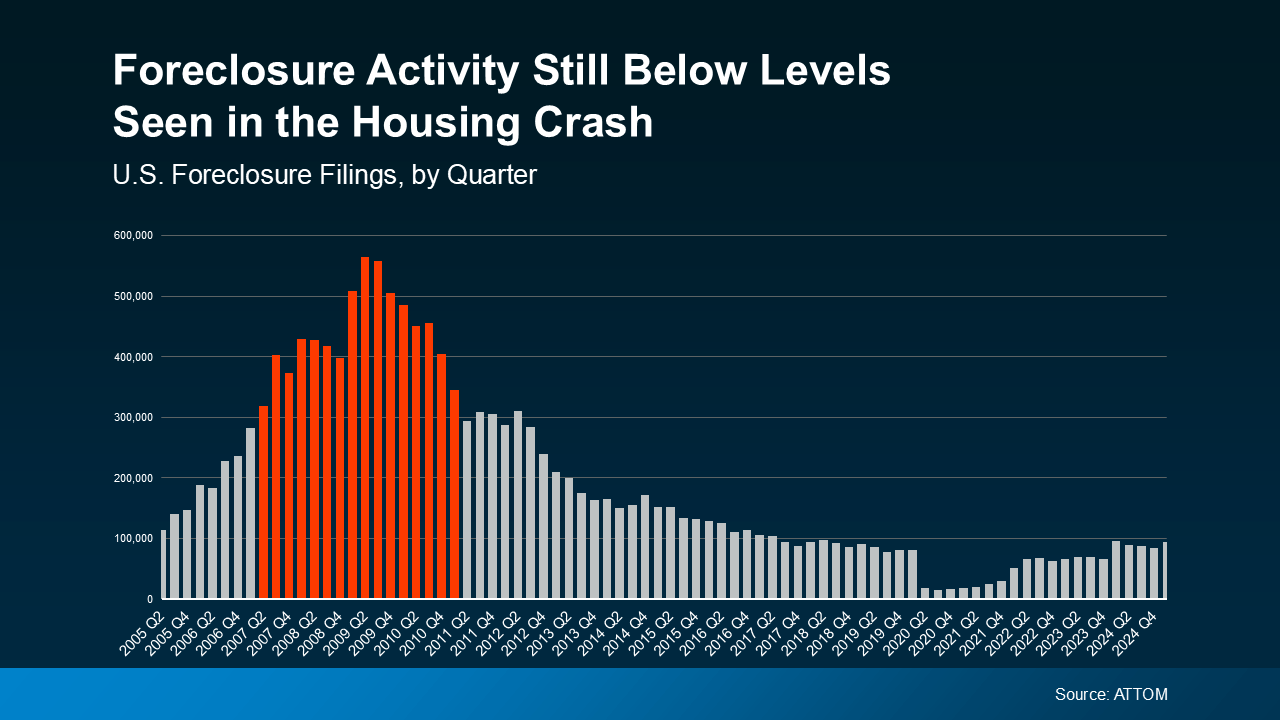

The latest quarterly report from ATTOM shows that foreclosures did rise in Q1 2025, which is concerning at first glance. However, foreclosure filings were still lower than the normal historical average, and far below the levels seen in 2008. When plotted visually, it’s easy to see the huge difference between 2008 and 2025.

Compare the foreclosure filings in Q1 2025 to the years surrounding the 2008 crash on the graph below. Even in the years preceding and following the 2008 crash, foreclosures were dramatically higher than what we’re seeing now.

Back in 2008, lenders were approving loans using much riskier practices, saddling many homeowners with mortgages they couldn’t afford. This flooded the market with distressed properties, surplus housing inventory, and free-falling home prices that collectively caused the crash.

In the years that followed, lending standards became much stricter and stronger to prevent such a crash from happening again. Today, most homeowners are in a much better financial position, and foreclosures have stabilized as a result.

The graph may appear to show foreclosures ramping up since the lows of 2020 and 2021, but this is deceiving. Foreclosures during those years were unusually low thanks to a moratorium designed to help millions of homeowners through the pandemic. That moratorium has since ended, which has caused foreclosure filings to return to the more normal levels we see now.

Compared to pre-pandemic years like 2017-2019, foreclosures overall are actually relatively down from what’s considered normal. So while foreclosures rose in Q1 2025, this doesn’t point to a troubling surge in the market.

Why Foreclosures Haven’t Surged in 2025

Another reassuring difference in today’s real estate market is the power of increased homeowner equity. As home prices have exploded over these past few years, homeowners have enjoyed a welcome boost to their wealth. According to Rob Barber, CEO at ATTOM:

“While levels remain below historical averages, the quarterly growth suggests that some homeowners may be starting to feel the pressure of ongoing economic challenges. However, strong home equity positions in many markets continue to help buffer against a more significant spike . . .”

In short, if a homeowner can’t make their mortgage payments, they may be able to sell their home to avoid foreclosure. During 2008, many people owed more than their homes were worth and had no choice but to foreclose. Today, most homeowners have much stronger equity that protects them from being forced into foreclosing. As Rick Sharga, Founder and CEO of CJ Patrick Company, recently explained in a Forbes article:

“ . . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Conclusion

It’s true that foreclosures rose in Q1 2025, but they’re nowhere near the levels seen during the 2008 crash. Even as home prices continue rising, strong equity is protecting existing homeowners and bolstering their wealth. This doesn’t discount the struggles some homeowners are facing, but it’s a reassuring fact for the market at large.

If you’re a homeowner facing foreclosure, ask your mortgage provider about what options are available to you. Are you a first time buyer eager to build your equity? Contact us today for the info you need to get started.

Many Fear a Housing Market Crash in 2025 – Will It Happen?

Between every economic uncertainty underpinning this year so far, Americans are understandably trepid about the future. Amid market lows and rising prices, many are asking if we’re heading for a housing market crash in 2025.

If talk of tariffs and mercurial markets are giving you pause about your plans, you’re not alone. In fact, new data from Clever Real Estate has found that 70% of Americans are worried about a housing crash in 2025. But how likely is this, and what does the latest data say?

Low Inventory Prevents a Crash in Prices

Before you put your plans to buy or a sell a home on hold, let’s look at the facts. The reality is that the trends in the housing market we’re seeing aren’t signs of crashing, only of shifting. As Chief Economist at First American Mark Fleming explains:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

Consider the basic laws of supply and demand. If the supply of something is low, its prices are bound to go up, and homes are no exception. And even though housing inventory is up in 2025, high demand from buyers is still driving home prices higher.

According to recent data from Realtor.com, the number of homes for sale in 2025 is climbing, but still below normal levels. Even still, home supply is at its highest since pre-pandemic levels, showing a positive trend in the right direction.

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

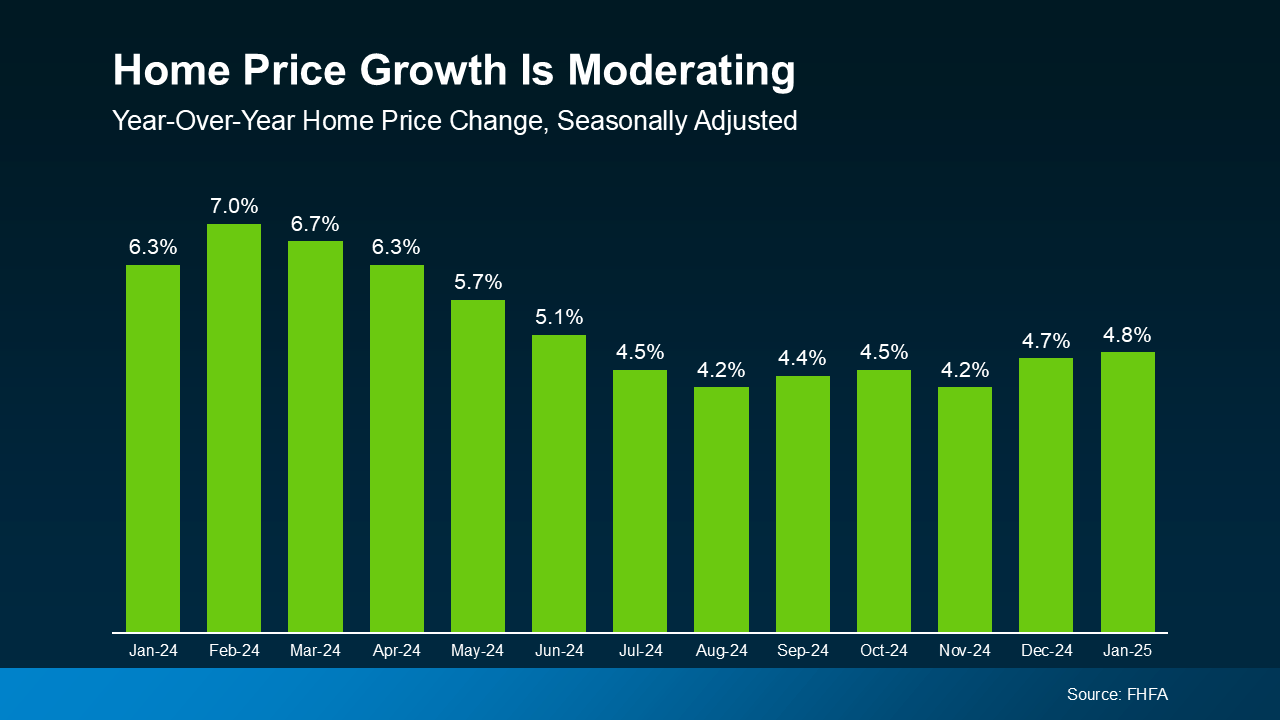

Home Prices Normalize as Inventory Increases

As more homes are listed on the market, upward pressure on home price growth normalizes. Prices may not be falling, but they’re rising at a rate closer to what we’d consider normal for the market.

Even though prices aren’t declining nationally, increased inventory means they’re rising more slowly than they were. The trend we’re currently seeing is what’s considered price moderation.

The good news for buyers is that this price moderation is expected to continue throughout the rest of the year, according to a January report from Freddie Mac:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

This means that home prices will continue rising in most markets, but not as quickly as they did in 2024. This is great news for anyone who’s been priced out of the market thanks to rapid price appreciation these past few years.

These numbers represent national trends, so the true story will vary in individual markets. A local real estate agent can give you the latest details on the market trends in your your own unique area.

Conclusion

Fears of a housing market crash in 2025 abound, but don’t let this worry you. While a little caution is healthy, experts are confident that a housing market crash is unlikely in 2025. As a recent report from Business Insider says:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyond unless the economic outlook changes.”

In reality, this year’s housing market is stabilizing thanks to decreasing price growth and increasing home supply. If you’re curious about the market trends in your local area, contact us today to connect with an agent who can reassure you with the facts.