Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

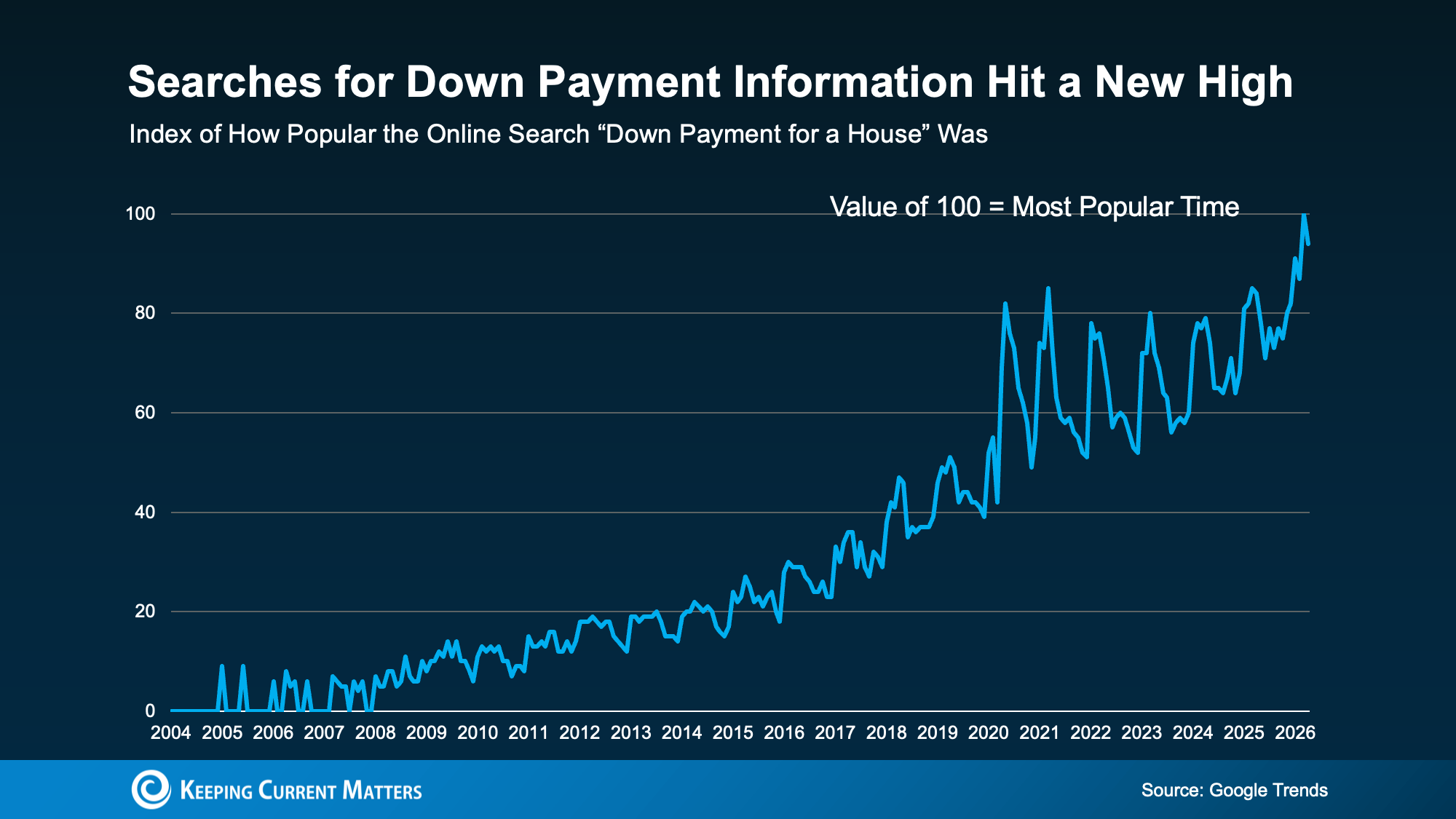

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

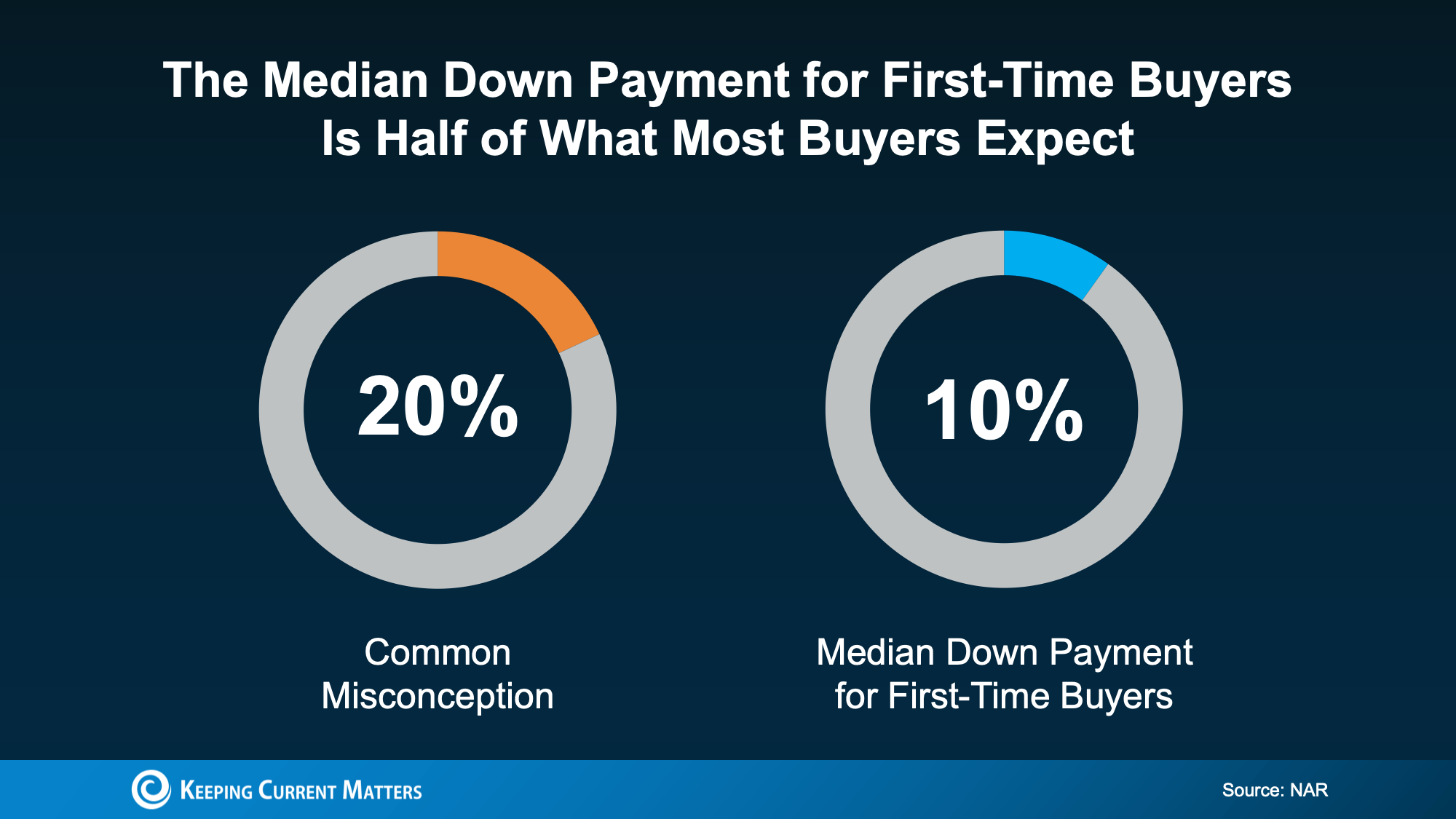

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

Is an Adjustable-Rate Mortgage Right for You? A Homebuyer’s Guide

If you’ve been shopping for a home lately, you’ve likely felt the pressure of today’s affordability challenges. Higher home prices and mortgage rates have made it harder for many buyers to stay within budget. That’s one reason adjustable-rate mortgages, or ARMs, are getting more attention again.

For some homebuyers, an ARM can offer welcome savings upfront. But before you go that route, it’s important to understand how these loans work, why they appeal to certain buyers, and what the long-term risks might be.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage is a home loan that starts with a fixed interest rate for a set number of years. After that initial period ends, the rate can adjust at scheduled intervals based on market conditions.

As Business Insider explains:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

That’s the biggest difference between a fixed-rate mortgage and an ARM. A fixed-rate loan offers predictability, while an ARM may give you a lower payment at first but less certainty later.

It’s true that costs like property taxes and homeowners insurance can still change with a fixed-rate mortgage. But the principal and interest portion of the payment generally stays steady. With an ARM, your monthly payment can rise or fall once the fixed period ends.

Why More Home Buyers Are Considering ARMs

The main reason buyers look at adjustable-rate mortgages is simple: lower initial costs.

Business Insider puts it this way:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

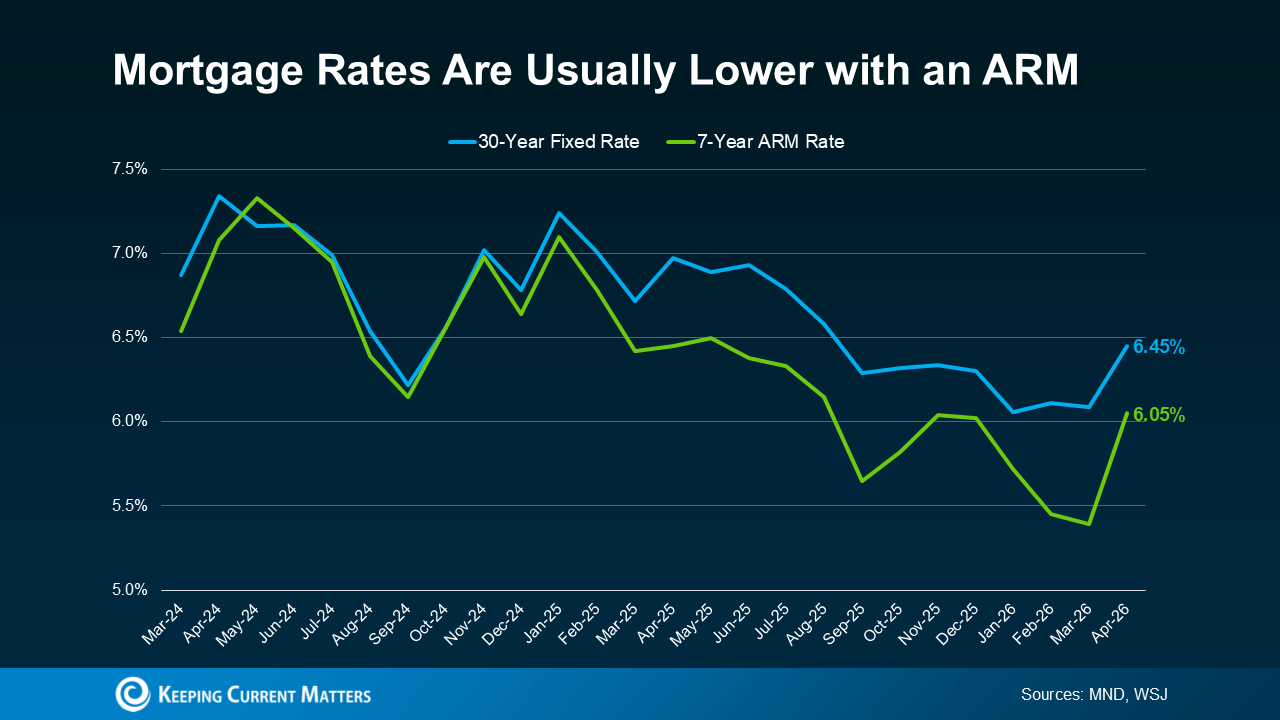

That upfront savings can matter, especially in a market where every dollar counts. Recent reporting from Mortgage News Daily and The Wall Street Journal show that ARM rates have been coming in lower than 30-year fixed mortgage rates.

For many buyers, even modest monthly savings can make a difference. For example, Redfin found that a typical buyer could save about $150 per month by choosing an ARM instead of a 30-year fixed mortgage. Savings like that can help some buyers qualify for a home sooner or make their monthly budget more manageable.

Why Adjustable-Rate Mortgages Are Making a Comeback

More homebuyers are deciding that a lower payment today is worth considering, even if it means taking on more uncertainty later.

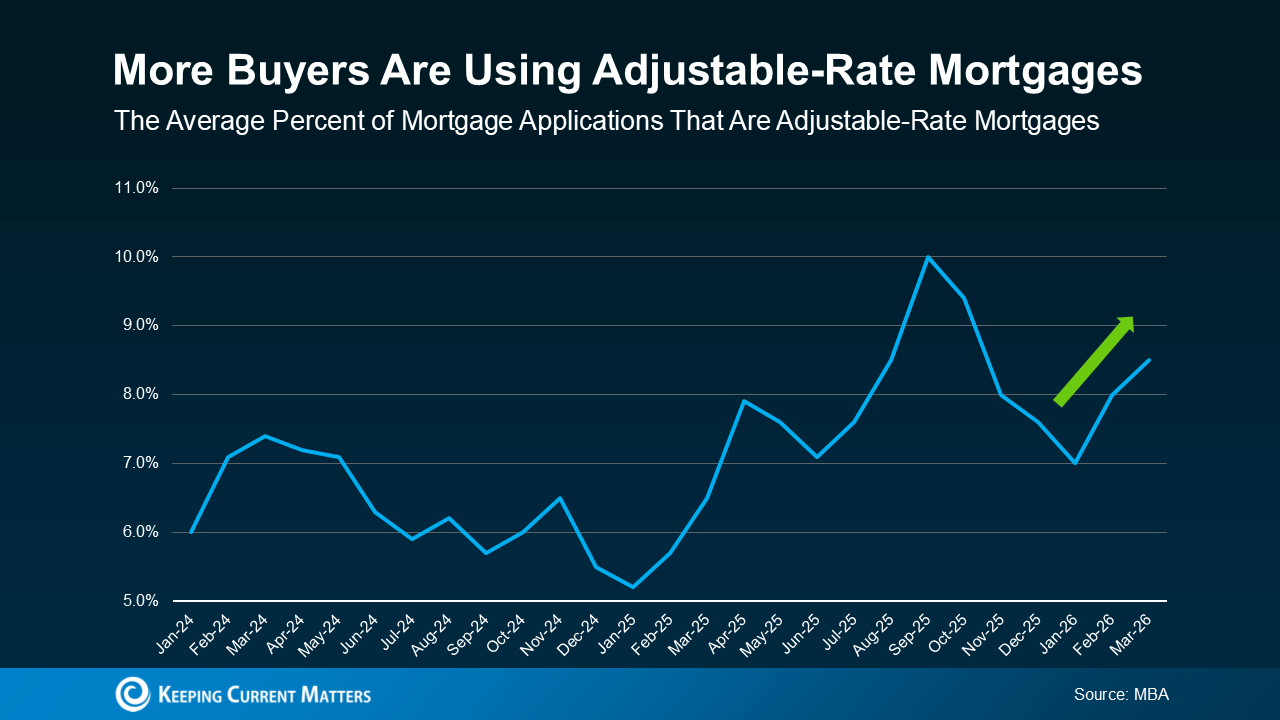

Recent reports from the Mortgage Bankers Association (MBA) show that the share of buyers choosing ARMs has increased in recent years. That doesn’t mean ARMs are becoming the right fit for everyone. But, it shows that some buyers are using them as a strategy to deal with affordability challenges in the current market.

For anyone who remembers the 2008 housing crash, this trend may sound concerning at first. But today’s lending environment is very different.

In the past, some borrowers were approved for loans they couldn’t realistically afford once the interest rate adjusted. Today, lending standards are tighter, and lenders generally evaluate whether borrowers could still manage the payment if rates rise. So while ARMs are becoming more common again, that alone doesn’t point to another housing crisis.

The Pros and Risks of an ARM

An adjustable-rate mortgage can make sense in the right situation, but it depends on your financial plan and your comfort with risk.

An ARM may be worth considering if:

- You expect to move before the rate adjusts.

- You believe your income will increase over time.

- You need a lower initial payment to make homeownership possible now.

Still, there are trade-offs to consider.

Once the fixed-rate period ends, your interest rate can change, and your monthly payment could increase significantly depending on where mortgage rates are at that point. There’s also no guarantee rates will fall in the future, which means refinancing later may not be as easy or as beneficial as some buyers hope.

That’s why it’s important to think beyond the introductory rate. Make sure you understand how long the fixed period lasts, how often the rate can adjust, and how much your payment could increase over time. Most importantly, talk through your options with a trusted lender and financial advisor before making a decision.

Bottom Line: Is an ARM Right for You?

Adjustable-rate mortgages are regaining popularity because they can make buying a home more affordable in the short term. For some buyers, that lower upfront payment can be a helpful tool. But an ARM isn’t necessarily the right move for everyone.

The best decision comes down to understanding how the loan works, weighing the risks, and making sure it fits your long-term goals.

If you’re considering an adjustable-rate mortgage yourself but are still on the fence, reach out to us today. We can connect you with a qualified lender in your area who explore your options with you.

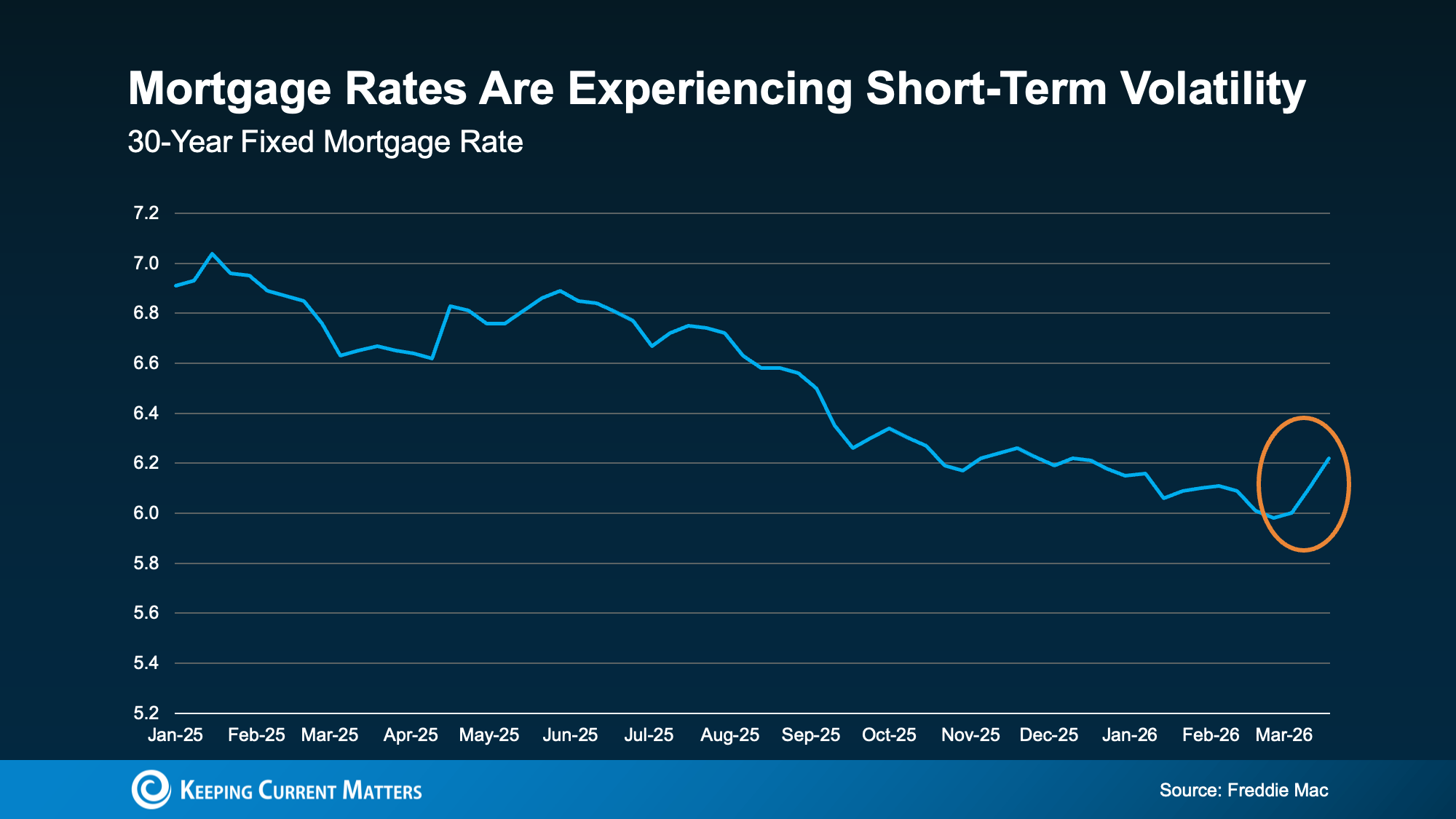

Mortgage Rate Volatility: What You Can Control as a Buyer

Mortgage rates have been moving up and down lately, and that can make buying a home feel harder to plan for. When rates are unpredictable, many buyers wonder whether they should wait, move forward, or try to time the market.

Here’s the good news: while you can’t control where mortgage rates go next, you can control several factors that may help you secure a better rate. The first step is understanding what’s driving today’s market and knowing where to focus your time and effort.

Mortgage Rate Volatility Is Normal

Recent data from Freddie Mac show that mortgage rates have been fluctuating. After trending downward for well over a year, rates ticked up again this month.

That kind of movement can feel frustrating, especially when you’re doing your best to budget for a home purchase. But occasional increases and decreases are a normal part of the mortgage market. Even over the past year, there have been periods when rates jumped before settling back down.

This is another one of those moments, and it helps to keep that in mind.

When there’s economic uncertainty or major global events unfolding, mortgage rates often respond quickly. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

That’s exactly why trying to predict the perfect time to buy usually doesn’t pay off. Rates can change fast, and waiting for the market to cooperate may not give you the outcome you want.

Focus on What You Can Control

You may not be able to influence the market, but you can take steps put yourself in a better position as a buyer. If your goal is to get the best mortgage rate possible, these are the areas that matter most.

Your Credit Score

Your credit score is one of the biggest factors that affects the rate you qualify for. In many cases, even a modest improvement in your score can lead to better loan terms and a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That’s why it’s worth taking steps to strengthen your credit before applying for a mortgage. Paying bills on time, reducing outstanding debt, and avoiding new credit inquiries can all help. If you’re not sure where your score stands or what improvements would make the biggest difference, a trusted loan officer can help you create a plan.

Your Loan Type

The type of mortgage you choose also affects your rate. There are many different types of loans, and each comes with different eligibility requirements, benefits, and pricing.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why exploring your mortgage options is so important. A conventional loan may be the right fit for one buyer, while an FHA, USDA, or VA loan may offer better advantages for another. Comparing programs and speaking with more than one lender can help you understand which path makes the most sense for your financial situation.

Your Loan Term

The length of your loan term matters, too. Most lenders offer 15-year, 20-year, and 30-year mortgage options, and the term you choose can affect both your interest rate and your monthly payment.

Freddie Mac explains it this way:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A shorter loan term may come with a lower interest rate, but the monthly payment is often higher. A longer term may give you more flexibility in your monthly budget, even if you pay more interest over time. The right choice depends on your goals, your budget, and how long you plan to stay in the home.

Conclusion

If you’re in the market for a home right now, the best strategy is not to focus on trying to predict where mortgage rates will go next.

Instead, focus on what you can control. Improve your credit score, explore different loan types, and choose a loan term that fits your needs. Most importantly, work with a trusted lender who can guide you through your options. If you need help connecting with trustworthy lender, reach out to us today.

Mortgage rates may be out of your hands, but the steps you take to prepare are not. And when you focus on what you can change, you give yourself a much better chance to move forward with confidence.

Renting vs. Buying: What The Numbers Say

Renting often feels like the simpler move these days. There’s no down payment to save up for, no surprise repair bills, and no long-term commitment if life changes.

But then your lease renews and the rent jumps. Then it happens again. Eventually, what felt flexible suddenly starts to feel expensive, especially when you realize every monthly payment is going to your landlord, not building wealth for you.

A big reason this stings is because there’s been so much talk about how homeownership is “out of reach.” And in some markets, it absolutely can be. But here’s the part that doesn’t get said enough: when you compare the numbers side by side, buying can cost less per month than renting in more places than most people expect.

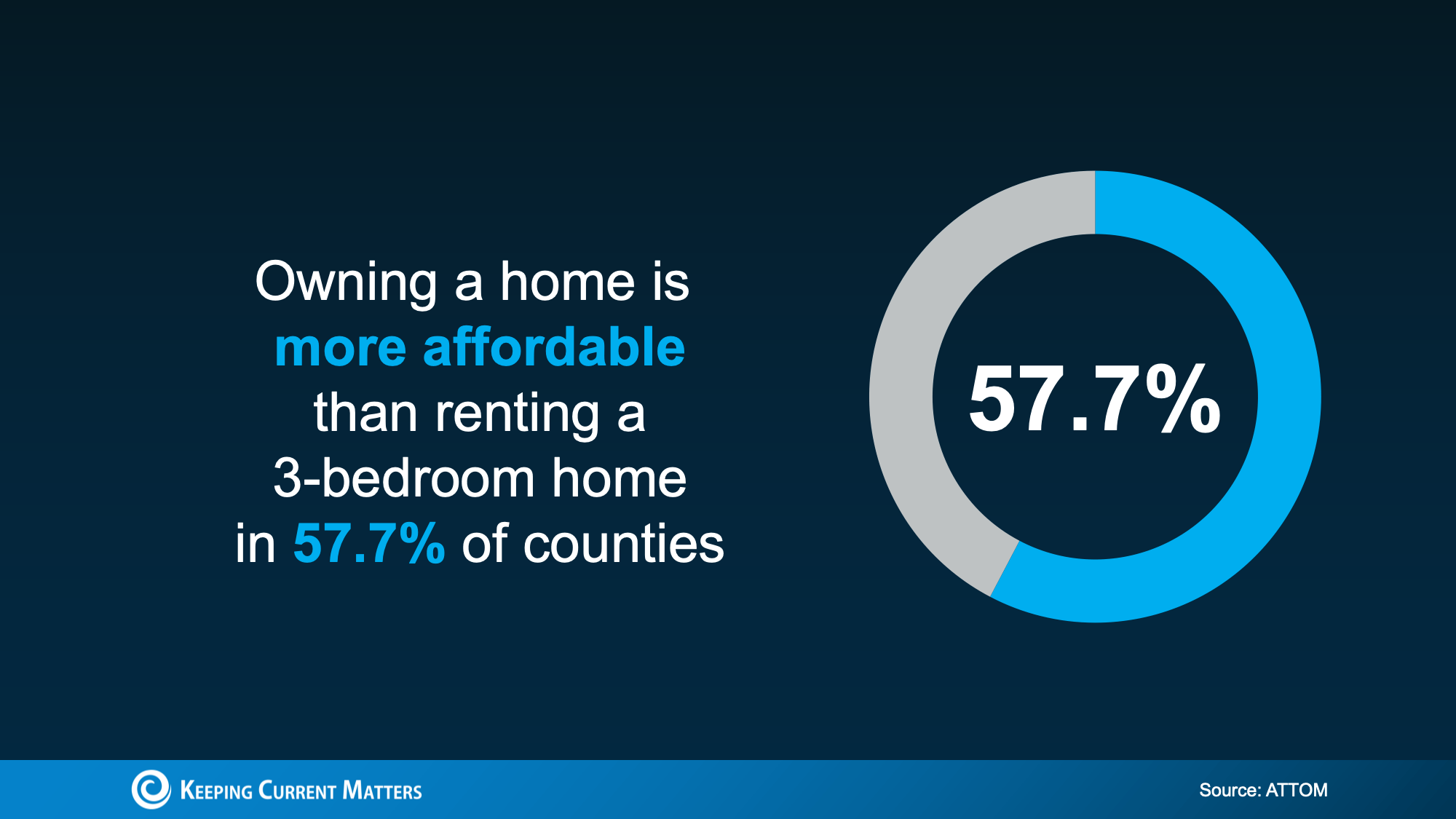

Buying Can Be More Affordable Than Renting in Many Areas

In a lot of markets today, owning a home may actually have a lower monthly cost than renting a 3-bedroom home. New data from ATTOM suggest this is true in nearly 58% of counties across the United States.

And this comparison isn’t just a mortgage payment versus rent. It also takes into account common ownership costs like insurance and regular maintenance.

So if you’ve assumed buying automatically means a higher monthly bill, it may be worth a second look. Recent changes in home price growth, housing inventory, and mortgage rates have been shaking certain markets. Depending on where you live, buying might be finally in your favor.

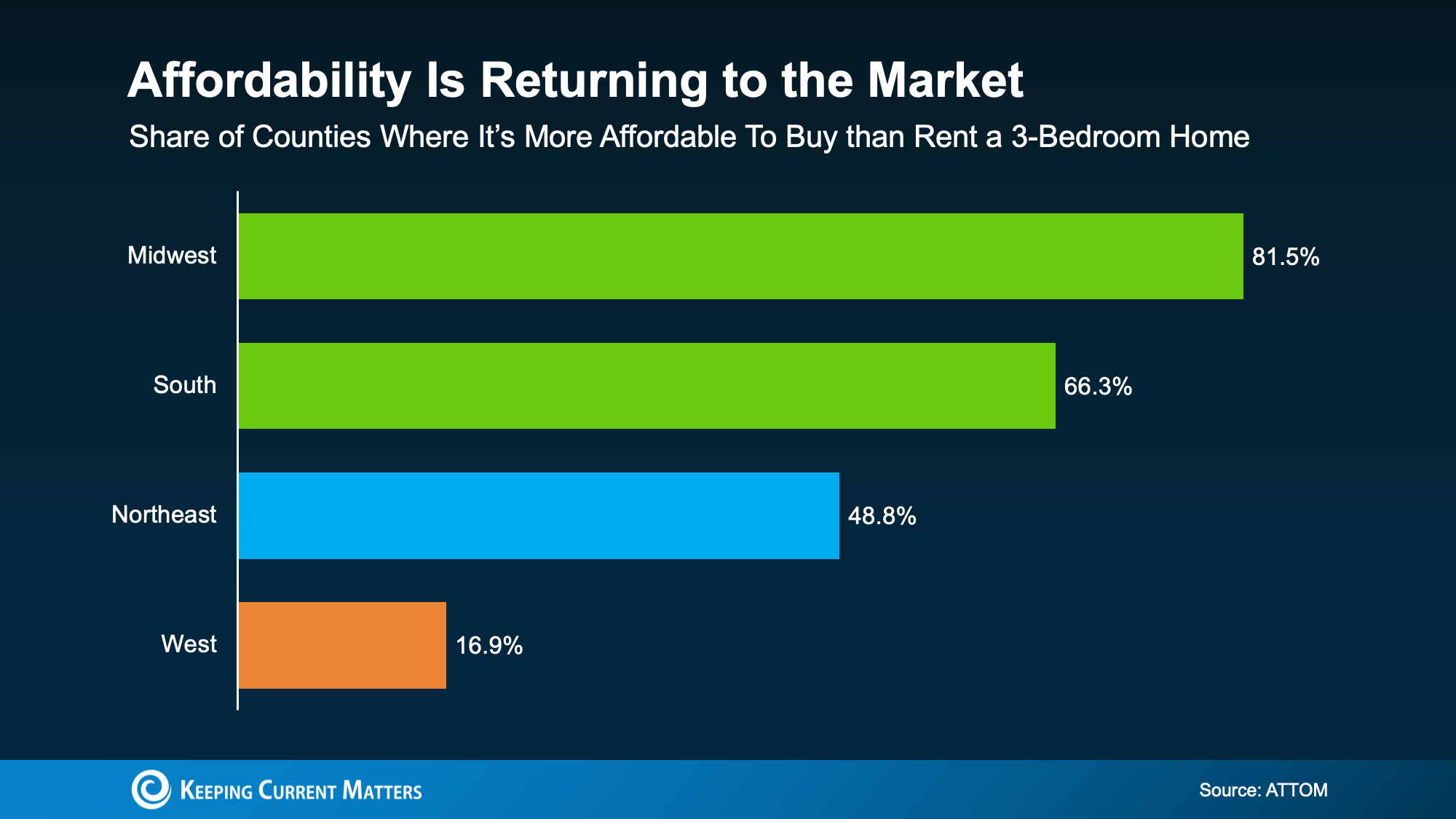

Affordability Depends on Where You Live

Even though the national picture has shifted, it doesn’t mean buying is cheaper everywhere, or that every renter will have the same experience.

That “nearly 58%” figure looks very different depending on the region. The biggest improvement is happening in the Midwest and South, while the West can still feel tight for many households.

The key takeaway is simple: real estate is local. A national headline can’t tell you what the rent-versus-buy equation looks like in your zip code. The only way to know is to run the numbers based on your local prices, rents, taxes, and insurance.

What’s Still Holding Buyers Back?

If you’re thinking, “Even if the monthly payment works, I can’t afford the upfront costs,” you’re not alone.

For many renters, the biggest hurdle isn’t the monthly payment. It’s the down payment (and often closing costs) that feels like a wall.

Here’s the good news: there are thousands of down payment assistance programs across the country, and many buyers qualify without realizing it. The average benefit is around $18,000, which can help cover part of your down payment or closing costs.

Support like this can make buying feel a lot more realistic, because it reduces how much cash you need to get in the door.

How to Figure Out What’s Right for You

If you want clarity instead of guesswork, focus on a simple comparison:

- Your current rent (and how often it’s rising).

- An estimated monthly ownership cost (mortgage, taxes, insurance, HOA if applicable).

- A realistic maintenance cushion.

- Upfront costs (and any down payment assistance you may qualify for).

When you combine potential assistance with monthly costs that may be closer than expected, the gap between renting and buying can shrink quickly, or even flip in favor of buying.

Conclusion

The bottom line isn’t that everyone should buy a home as soon as possible.

The idea is that renting isn’t always the cheaper option people assume it is, and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feel stuck saying “someday”, consider a quick conversation with a local real estate agent or lender. Not a commitment, just a way to see what’s possible and whether it makes sense for you.

Mortgage Rates Just Hit a 3-Year Low. Does It Matter in 2026?

If you’ve been watching mortgage rates and waiting for a “better time” to buy, here’s your chance. Rates just dipped below 6% for the first time in more than three years. Even modest rate movement can change what you can afford, how competitive you can be, and whether buying feels realistic again, especially if last year’s higher rates pushed you to the sidelines.

With rates finally easing up into 2026, here’s a fresh take on why lower mortgage rates are still a big deal, plus what to do next if you’re thinking about making a move.

Why Mortgage Rates Impact More Than Just Interest

A mortgage rate isn’t just a number on a lender’s website. It shapes the entire homebuying experience because it affects:

- Your monthly payment

- How much home you can qualify for

- Your comfort level with your budget

- How competitive your offer can be

When rates jump, affordability tightens fast. That’s why many buyers (especially first-time homebuyers) feel the pinch first. When rates ease, the reverse happens: budgets get a little more breathing room, and choices open up.

The “One-Point” Difference That Changes the Math

One of the easiest ways to understand why rate declines matter is to look at a simple example.

When rates are closer to 7%, monthly payments rise sharply. When rates move closer to 6% (or below), payments can drop meaningfully. On a typical loan amount, that can translate into hundreds of dollars per month in savings compared to the higher-rate environment.

That difference can help you:

-

Stretch your budget without stretching your lifestyle

-

Consider more homes in a neighborhood you actually want

-

Keep cash available for repairs, furnishing, or future goals

In practical terms, the change isn’t just “cheaper interest.” It can be the difference between compromising on your wish list and finding a home that fits.

What Lower Rates Can Unlock for Buyers

When borrowing costs come down, three things usually happen for homebuyers:

1) Lower monthly payments

A lower rate can reduce the monthly principal-and-interest payment, which helps many buyers feel more confident about moving forward.

2) More buying power

When the payment drops, you may qualify for more home at the same monthly budget. That can mean a better location, an extra bedroom, or a property that needs fewer updates.

3) Stronger offers without overextending

More budget flexibility can help you compete without taking on a payment that makes you uncomfortable. That matters in markets where inventory is still tight and desirable homes move quickly.

Why This Can Bring More Buyers Off the Sidelines

Rate changes don’t only affect you. They affect everyone who has been waiting, too.

Industry research suggests that when rates sit around certain thresholds, millions more households can afford a median-priced home. In fact, research from the National Association of Realtors (NAR) points to 5.5 million additional households being able to afford the median-priced home when rates are at 6% or below, and it estimates roughly 550,000 of those households could buy within the next 12 to 18 months.

That matters because it signals something important: pent-up demand can return quickly when affordability improves.

If you’re home-searching now (or preparing to), you may be able to act before competition fully ramps back up.

A Quick Reality Check: Rates Aren’t the Only Factor

Lower rates help, but they don’t magically make every home affordable. Your true monthly cost depends on several moving pieces, including:

-

Home price

-

Local inventory and competition

-

Property taxes

-

Homeowners insurance (which can vary widely by state and ZIP code)

-

HOA dues

-

Your down payment and credit profile

That’s why the smartest next step isn’t guessing. It’s running real numbers to figure out what “affordable” looks like for you.

What To Do Next If You’re Considering Buying

If you’ve been waiting for rates to improve, here’s a simple, practical plan:

-

Get pre-approved (not just pre-qualified).

Pre-approval gives you a clearer budget and shows sellers you’re serious. -

Calculate your comfortable payment range.

Decide what fits your life, not just what a lender says you can qualify for. -

Compare scenarios with your lender.

Ask for payment examples at different price points, down payments, and rate options. -

Watch inventory in your target neighborhoods.

The best “deal” is the home that works for your needs and your budget.

Conclusion

Mortgage rates easing from last year’s highs isn’t just an attractive headline. For many buyers, it can be the shift that turns “maybe someday” into “this could actually work.”

If you paused your search when rates were higher, it’s worth revisiting your numbers now. A quick conversation with a trusted lender can show what today’s rate environment means for your payment, your buying power, and your options.

If you’re thinking of buying, or need help finding a lender, reach out to us today. We can connect you with local agents and lenders to make your journey as simple as possible.

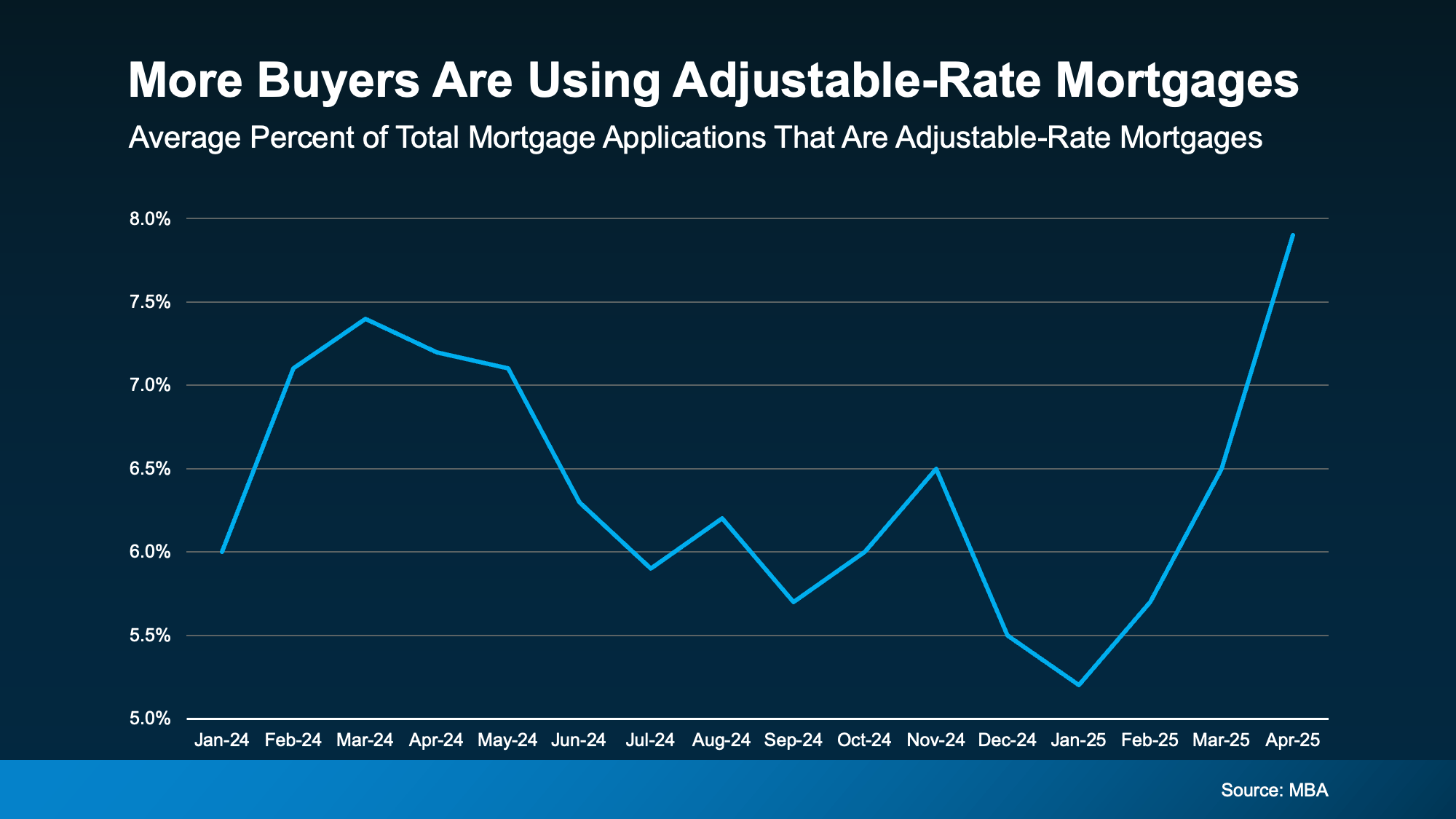

Adjustable-Rate Mortgages on the Rise: Should You Jump In?

If you’re in the market for a house, you’re probably not encouraged by today’s mortgage rates. Elevated rates and rising home prices have many homebuyers starting to explore other financing options that make more sense. One type of loan gaining popularity is adjustable-rate mortgages (ARMs).

If you remember the 2008 market crash, you may be wary of new types of loans. It’s wise to be cautious, but there’s no need to worry. Today’s ARMs much safer and stricter than the ones you may remember from 2008.

During that time, some buyers held loans they couldn’t afford once their rate adjusted. Today, lenders are more careful, and determine whether you can afford an increased rate before the loan is ever offered. This time, ARMs are returning thanks to creative buyers looking for affordable ways to buy a home..

According to recent data from the Mortgage Bankers Association (MBA), more buyers are using ARMs to buy this year.

How Does an Adjustable-Rate Mortgage Work?

If you’ve never heard of ARMs before, you may be wondering what they are, and if they’re right for you. Here’s how Business Insider explains the main difference between a traditional fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Taxes or homeowner’s insurance can still influence a fixed-rate loan, but your baseline mortgage payment typically changes very little. Meanwhile, adjustable-rate mortgages can potentially change drastically in either direction after your initial payment period ends. Depending on your situation and anticipated market trends, this could either work for you, or be far too risky.

Pros and Cons of Adjustable-Rate Mortgages

With ARMs on the rise in 2025, it’s clear that more buyers are finding them appealing. Under the right conditions, they may offer attractive upsides, like a lower initial rate. According to Business Insider again:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

Remember that if you have an ARM, your rate will change over time. As Barron’s explains, they can potentially cost you more in the long run:

“Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up.”

While the upfront savings can be helpful now, consider what could happen if your initial rate ends before you move. Even though rates are projected to ease a bit over the next couple years, nothing is ever guaranteed. Before you choose an ARM, talk with your lender and financial advisor about all your options, and the potential risks.

Conclusion

For certain buyers, adjustable-rate mortgages can offer some big advantages, but this won’t be true for everyone. Understand how they work and whether their pros and cons make sense for you financially. Always talk to a trusted lender and a financial advisor before making entering into a new mortgage.

Need help connecting with a trustworthy lender in your area? Reach out to us for help today.

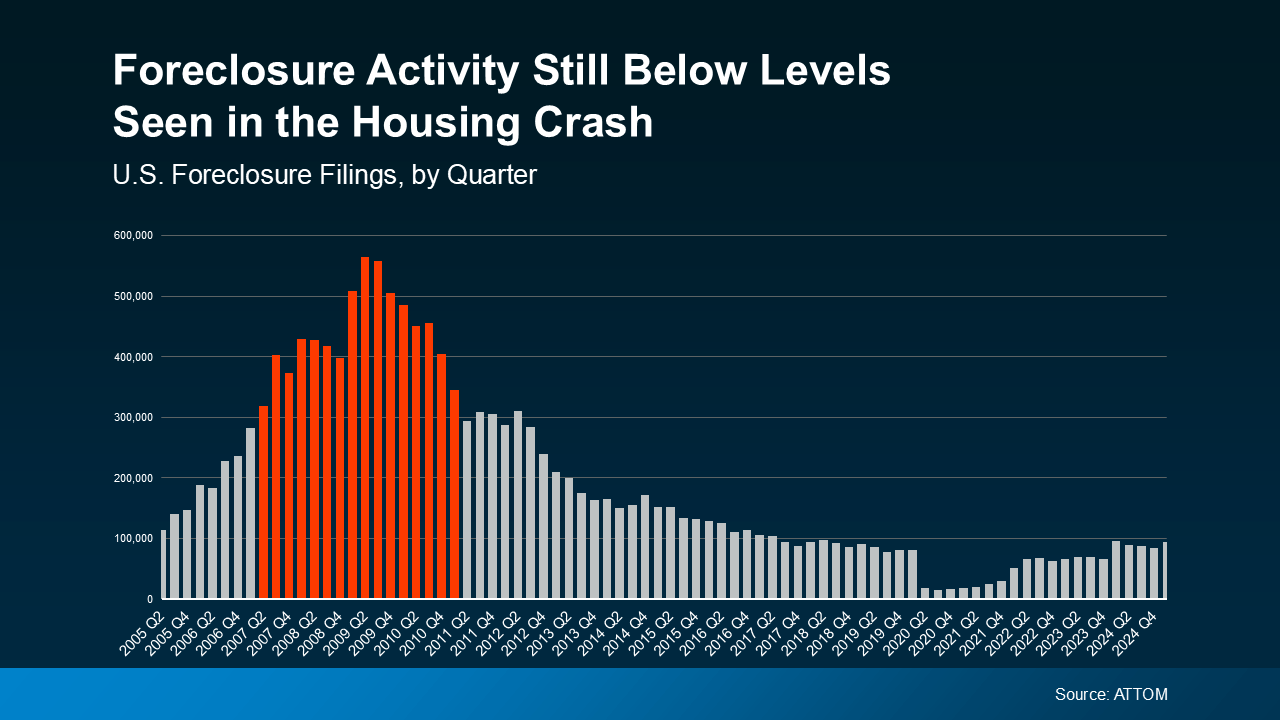

Foreclosures Rose in Q1 2025 – Is It a Warning Sign?

With everyday costs seemingly rising across the board, the state of the housing market is a natural concern. When basic living expenses rise, even critical financial responsibilities like mortgage payments start to slip, leading to increased foreclosures. Unsurprisingly, new data shows filings for foreclosures rose in Q1 2025, stirring worries about another housing crash like in 2008.

But as it turns out, there’s less cause for worry than you might think. When contextualized correctly, it’s clear these new number don’t point to a repeat of the last big housing crash.

The 2008 Market Versus 2025

The latest quarterly report from ATTOM shows that foreclosures did rise in Q1 2025, which is concerning at first glance. However, foreclosure filings were still lower than the normal historical average, and far below the levels seen in 2008. When plotted visually, it’s easy to see the huge difference between 2008 and 2025.

Compare the foreclosure filings in Q1 2025 to the years surrounding the 2008 crash on the graph below. Even in the years preceding and following the 2008 crash, foreclosures were dramatically higher than what we’re seeing now.

Back in 2008, lenders were approving loans using much riskier practices, saddling many homeowners with mortgages they couldn’t afford. This flooded the market with distressed properties, surplus housing inventory, and free-falling home prices that collectively caused the crash.

In the years that followed, lending standards became much stricter and stronger to prevent such a crash from happening again. Today, most homeowners are in a much better financial position, and foreclosures have stabilized as a result.

The graph may appear to show foreclosures ramping up since the lows of 2020 and 2021, but this is deceiving. Foreclosures during those years were unusually low thanks to a moratorium designed to help millions of homeowners through the pandemic. That moratorium has since ended, which has caused foreclosure filings to return to the more normal levels we see now.

Compared to pre-pandemic years like 2017-2019, foreclosures overall are actually relatively down from what’s considered normal. So while foreclosures rose in Q1 2025, this doesn’t point to a troubling surge in the market.

Why Foreclosures Haven’t Surged in 2025

Another reassuring difference in today’s real estate market is the power of increased homeowner equity. As home prices have exploded over these past few years, homeowners have enjoyed a welcome boost to their wealth. According to Rob Barber, CEO at ATTOM:

“While levels remain below historical averages, the quarterly growth suggests that some homeowners may be starting to feel the pressure of ongoing economic challenges. However, strong home equity positions in many markets continue to help buffer against a more significant spike . . .”

In short, if a homeowner can’t make their mortgage payments, they may be able to sell their home to avoid foreclosure. During 2008, many people owed more than their homes were worth and had no choice but to foreclose. Today, most homeowners have much stronger equity that protects them from being forced into foreclosing. As Rick Sharga, Founder and CEO of CJ Patrick Company, recently explained in a Forbes article:

“ . . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Conclusion

It’s true that foreclosures rose in Q1 2025, but they’re nowhere near the levels seen during the 2008 crash. Even as home prices continue rising, strong equity is protecting existing homeowners and bolstering their wealth. This doesn’t discount the struggles some homeowners are facing, but it’s a reassuring fact for the market at large.

If you’re a homeowner facing foreclosure, ask your mortgage provider about what options are available to you. Are you a first time buyer eager to build your equity? Contact us today for the info you need to get started.

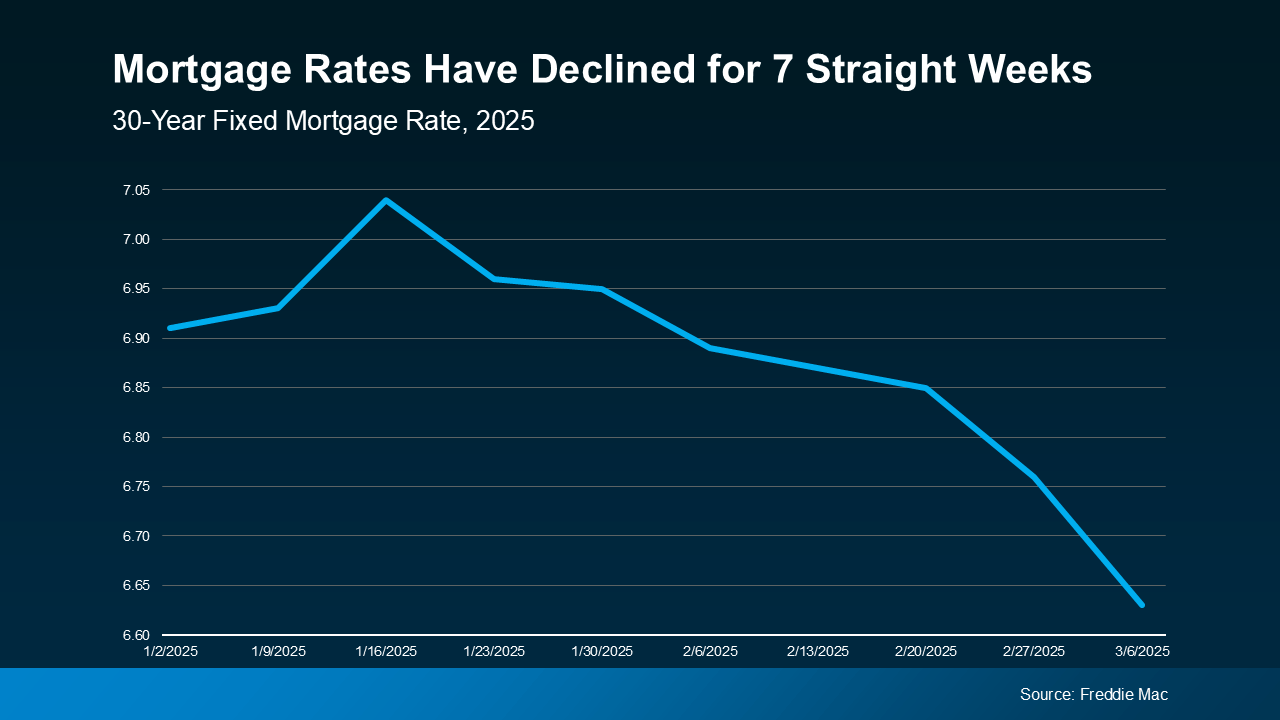

Mortgage Rates Drop to the Lowest Point in 2025 So Far

If you’ve been holding off on buying a home for a lower mortgage rate, take another look at the market. Mortgage rates are trending downward, and they just hit their lowest point of the year so far.

According to a report from Freddie Mac, mortgage rates have been falling for seven straight weeks. The average weekly rate for a 30-year-fixed mortgage is now at the lowest level its been in 2025.

This may not sound significant on its own, but it outlines a remarkable trend. A drop in rates from over 7% to the mid-6’s can make all the difference when buying a home. What’s most significant is that experts previously predicted that rates wouldn’t fall this low until Q3 of this year.

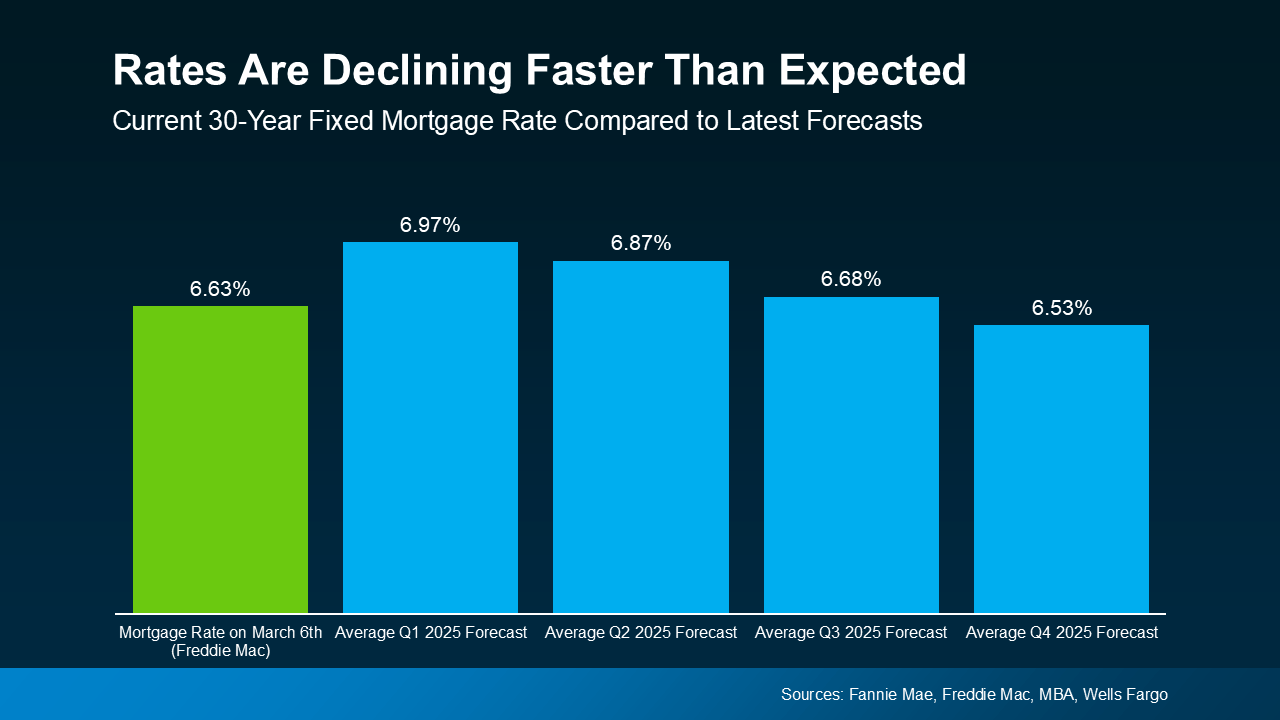

Why Are Mortgage Rates Dropping?

According to Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), ongoing economic uncertainty is a driving force in pushing rates lower:

“Mortgage rates declined last week on souring consumer sentiment regarding the economy and increasing uncertainty over the impact of new tariffs levied on imported goods into the U.S. Those factors resulted in the largest weekly decline in the 30-year fixed rate since November 2024.”

The timing of this rate drop is great for buyers moving into the Spring 2025 market. But remember that mortgage rates can change quickly, and always expect some volatility in markets driven by uncertainty. With that said, this small window of rates dropping into prime buying season might be exactly wait you’ve waited for.

What Falling Mortgage Rates Mean for Your Buying Power

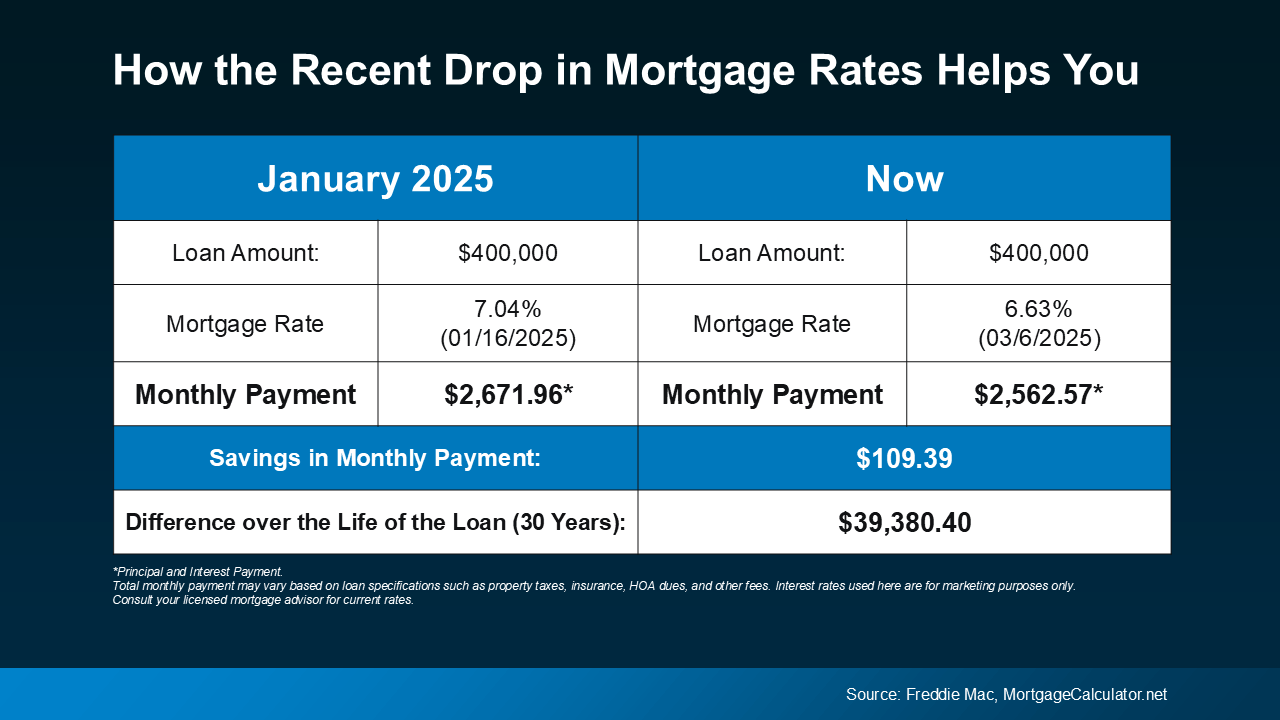

Even a small reduction in your mortgage rate can make a huge difference in your monthly housing payment. The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house when rates were 7.04% back in mid-January (this year’s mortgage rate high). The right side shows what it could look like if you buy a home now at current rates.

In just the past few weeks, the expected payment on a $400K loan has come down by over $100 per month. That’s a significant savings that can make a world of difference when deciding to buy a house.

Recent economic shifts have driven rates down faster than expected, and that’s great news. But remember that this could change at any time in the coming days and months for better or worse. So if you’re waiting for rates to fall further before you buy, think hard about the current window of opportunity before making a decision.

Conclusion

Mortgage rates have dipped to their lowest point in 2025 so far. This grants buyers a great position moving into the spring buying season, especially for those who have been waiting. The unpredictability of the market and larger economy mean volatility, so get expert advice and consider before making a decision.

Can You Buy a Home in 2025 Without Waiting for Lower Rates?

Like many homebuyers, you may be waiting for rates to drop before you finally buy a home this year. The latest expert reports predict that rates will continue to fall, but not as low as many hope. While this may be discouraging, the good news is that there are still ways you can buy a home in 2025 without waiting for lower rates.

Will Rates Keep Dropping?

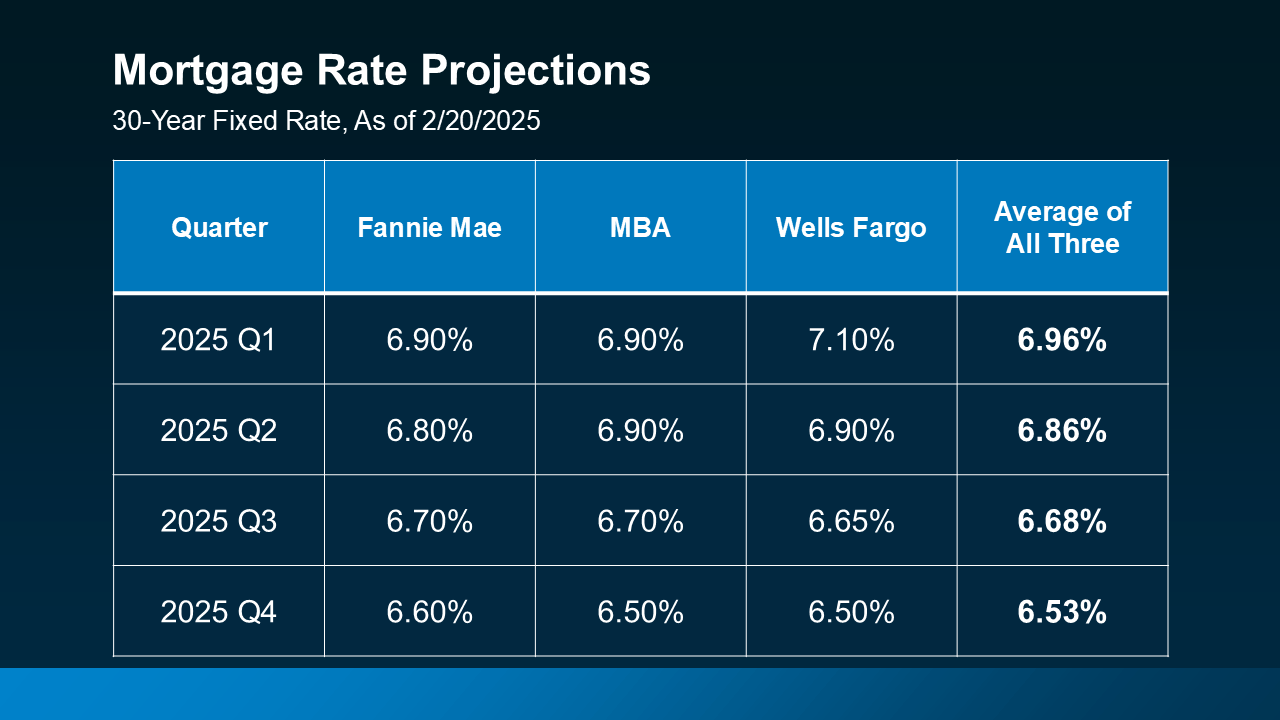

Near the end of 2024, experts were predicting that mortgage rates could dip below 6% by the end of 2025. More recent projections are suggesting that rates will continue to fall but hover somewhere above 6%.

Recent projections from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo now predict that mortgage rates will stabilize around 6.5% by the end of the year.

If you’re holding out for mortgage rates to drop below 6% before buying, you may need to keep waiting into next year at least. But what if you’re a buyer who can’t wait to move because of a major life event, like a new job, a new baby, or a marriage? Don’t panic—you’ll still be able to move this year, but you may need to take advantage of some alternative financing options.

How to Finance a Home in Today’s Market

With rates predicted to hold more stubbornly than expected this year, it’s worth researching different financing options, especially if your move is a non-negotiable one. Here are three unique financing strategies that may be helpful to you depending on your situation. If you’ve already chosen a lender, discuss each of these options with them to decide if any are a good fit. It may make all the difference you need to buy a house in 2025.

1. Mortgage Buydowns

A mortgage buydown allows you to pay an upfront fee—sometimes called “discount points”— to lower your mortgage rate temporarily or sometimes permanently. This can be an especially helpful option if you want or need a lower monthly mortgage payment early on. Of course, the obvious downside is a higher upfront cost.

A recent survey by HomeLight found that 27% of real estate agents day first-time homebuyers are increasingly requesting mortgage buydowns from sellers. This is a new program called RateReduce Sell that allows sellers to pay an upfront cost to lock in a lower mortgage rate for buyers. However, a real estate agent can help negotiate this with a seller, so be sure to mention it if you’re actively looking to buy a house.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) are loans that combine a fixed-rate period with an adjustable-rate period. ARMs typically start with a lower rate than a traditional 30-year fixed mortgage then fluctuate with the market once the fixed-rate period ends. This can make them an attractive option if you expect rates to drop in the future, or plan to refinance your home later.

If you remember the 2008 housing crash, it may be reassuring to know that today’s ARMs aren’t like the volatile loans from back then. Lance Lambert, Co-Founder of ResiClub, describes modern ARMs this way:

“. . . ARM products today are different from many of the products issued in the mid-2000s. Before 2008, lenders often approved ARMs based on borrowers ability to pay the initial lower interest rates. And sometimes they didn’t even check that (remember Ninja loans). Today, adjustable-rate borrowers qualify based on their ability to cover a higher monthly payment, not just the initial lower payment.”

Before 2008, banks used to give loans without checking to see if buyers could realistically afford them. These days, lenders verify income, assets, and employment, reducing the risks previously associated with loans like ARMs.

3. Assumable Mortgages

An assumable mortgage allows you to take over a seller’s existing loan, usually including its lower mortgage rate, repayment period, and remaining balance. This can be a great option if the seller was locked into a low mortgage rate, but few are willing to offer it by default. According to U.S. News, more than 11 million homes qualify for an assumable mortgage, so it’s always worth bringing up with your agent or seller.

Conclusion

With mortgage rates looking unlikely to fall below 6% in this year, waiting for a drop may not work out if you’re eager to buy a house in 2025. Consider options like mortgage buydowns, ARMs, or assumable mortgages depending on what makes the most sense for you. Connect with a local lender or expert agent today to explore your options and get the help you need.

FHA Home Loans in Wisconsin

If you’re in the market for a home in Wisconsin, you may have heard of FHA loans, or Federal Housing Administration loans, as a financing option. These government-backed loans are a popular choice for first-time homebuyers and those with less-than-perfect credit. In this guide, we’ll break down everything you need to know about FHA loans in Wisconsin, along with benefits and requirements of state-specific programs that can help you achieve your dream of homeownership.

What are FHA Home Loans?

FHA loans are mortgages insured by the Federal Housing Administration (FHA) and are designed to make homeownership more accessible, especially for Americans who may not qualify for a traditional mortgage or other loans. This reduces the risk for lenders and allows them to offer lower down payments and more lenient credit requirements. This also makes FHA loans particularly appealing to first-time buyers or those with limited savings.

Here are a few ways that FHA loans stand out from other options:

- Low Down Payment: You can qualify with as little as 3.5% down if your credit score is 580 or higher, meaning that up to 96.5% of a home’s value can be borrowed through an FHA loan.

- Flexible Credit Requirements: FHA loans are more forgiving of lower credit scores compared to conventional loans. Borrowers with scores as low as 500 may still qualify with a 10% down payment.

- Competitive Interest Rates: Being backed by the federal government, FHA loans often have lower interest rates than conventional loans, making monthly payments more affordable.

- Mandatory Mortgage Insurance: FHA loans require both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP), which is paid monthly.

These are just a few ways FHA loans can help homebuyers overcome financial barriers and make homeownership a reality for more Americans. With lower credit score requirements and lower down payments, it’s an easier pathway to securing a loan and finally owning a house.

Current FHA Loan Interest Rates in Wisconsin

As of February 2025, the average interest rate for a 30-year fixed FHA loan in Wisconsin is 6.24%, with an APR of 6.92%. These rates are slightly lower than conventional loan rates, making FHA loans a more cost-effective option. However, rates vary depending on your credit score, the lender, and the loan type and length, so always explore your options and compare offers when possible.

FHA Loan Requirements in Wisconsin

To qualify for a FHA home loans in Wisconsin, several key criteria must be met to ensure that potential borrowers are financially stable and capable of repaying their loan. Most notably, applicants need to demonstrate a reliable employment history and income.

Here’s a summary of the main eligibility criteria:

- Credit Score: As of 2023, a minimum score of 580 is required for a 3.5% down payment. Scores between 500 and 579 require a 10% down payment.

- Debt-to-Income Ratio (DTI): Your total monthly debt, including the mortgage, should not exceed 43% of your income, though some lenders may allow up to 57% in certain cases.

- Employment and Income: You’ll need a steady employment history of at least two years and verifiable income.

- Primary Residence: The home must be your primary residence.

- Property Standards: The property must meet FHA’s minimum standards for safety and livability, as determined by an FHA-approved appraiser.

- Loan Limits: For 2025, the FHA loan limit for a single-family home in most Wisconsin counties is $524,225. In higher-cost areas like Pierce and St. Croix counties, the limit is $529,000.

By meeting these requirements, you better position yourself for loan approval. It can also simplify the loan process, making it smoother and preventing potential setbacks or delays.

Applying for an FHA Loan in Wisconsin

Applying for FHA home loans in Wisconsin is straightforward but involves several basic steps. Borrowers should start by researching and comparing various FHA-approved lenders to find the best loan terms and secure the best deal.

After selecting a lender, borrowers complete the FHA loan application process. This process may vary between lenders, but should follow the same general steps. Here’s an overview of the major stages involved:

- Find an FHA-Approved Lender: Choose a lender approved by the FHA. Most banks, credit unions, and mortgage companies offer FHA loans.

- Pre-Approval: Get pre-approved to determine your budget and show sellers you’re a serious buyer.

- Submit Your Application: Provide details about your income, employment, and the property you want to buy .

- Provide Documentation: Submit tax returns, pay stubs, bank statements, and other financial documents.

- Property Appraisal: The lender will order an appraisal to ensure the home meets FHA standards and is worth the loan amount.

- Underwriting: The lender reviews your application to ensure you meet all FHA requirements.

- Closing: Sign the final paperwork, pay closing costs, and officially become a homeowner.

Wisconsin-Specific Programs to Pair with FHA Loans

Certain areas in Wisconsin may offer programs that can make FHA loans even more affordable. These programs are most common in larger metropolitan areas like Madison and Milwaukee, but some are available statewide through the Wisconsin Housing and Economic Development Authority (WHEDA). Here are a few options to explore if you’re planning to buy a home in Wisconsin:

- WHEDA Down Payment Assistance: The Wisconsin Housing and Economic Development Authority (WHEDA) offers programs like the Easy Close DPA, which provides up to 6% of the home’s purchase price as a second mortgage. Another option is the Capital Access DPA, offering $7,500 with no interest or monthly payments

- City of Madison’s Home-Buy the American Dream Program: Provides up to $35,000 in down payment and closing cost assistance, deferred until the home is sold or refinanced.

- Milwaukee Down Payment Assistance: Offers forgivable grants of up to $7,000 for homes in designated areas, provided the buyer contributes at least $1,000 and lives in the home for five years.

- Local Assistance Programs: Many cities and counties in Wisconsin offer grants or zero-interest loans for first-time buyers. Check with your local housing authority for details.

Conclusion

FHA loans are an excellent choice for hopeful homebuyers, especially first-time buyers or those with limited savings. By combining the benefits of FHA loans with Wisconsin-specific programs like WHEDA’s down payment assistance, you can make your dream of homeownership a reality. Whether you’re buying in Milwaukee, Madison, or a smaller town, understanding the FHA loan process and available resources will help you make informed decisions and secure the best deal for your new home.

If you’re ready to take the next step, start by finding an FHA-approved lender and exploring the down payment assistance programs available in your area. With the right preparation, you’ll be well on your way to owning a home in the beautiful state of Wisconsin!

Ready to buy but not sure how to secure a loan? Reach out to us today for help finding a qualified lender that works for you.