Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Good News for Buyers: Home Affordability Improving in 2026

If you’ve felt priced out of the market or stuck waiting on the sidelines, there’s finally some encouraging news:

Buying a home is finally becoming more affordable.

Monthly payments have started to come down thanks lower interest rates, and buyers are starting to feel pricing pressures ease. That doesn’t mean homeownership is suddenly easy for everyone, but after a tough stretch, small improvements are meaningful.

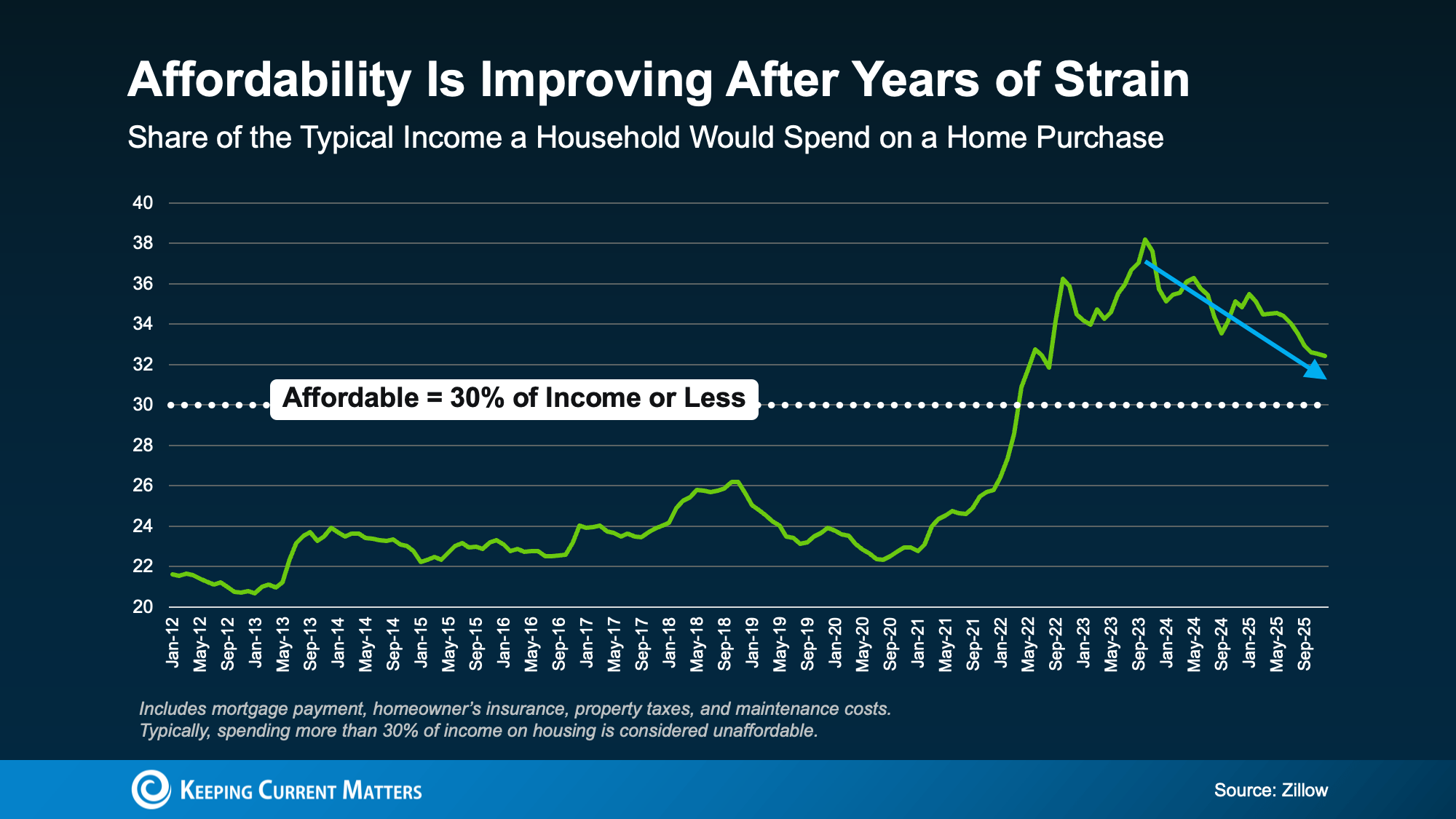

Home Affordability Is Finally Improving

One of the clearest ways to track this change is to look at how much of a household’s income goes toward owning a home.

According to Zillow, housing is typically considered affordable when total housing costs take 30% or less of your monthly income. That includes your mortgage payment, property taxes, insurance, and basic maintenance.

For the past few years, many buyers were well above that mark, which pushed homeownership out of reach for a lot of households. But that’s starting to shift. Zillow research shows it’s taking less of a typical household’s income to buy a home than it did just a few years ago (see graph below):

We’re not all the way back to Zillow’s 30% threshold yet, so affordability is still tight in many markets. But the trend is improving, and that’s a big change from what buyers have been up against.

Why Homebuying Is Becoming More Affordable

Mortgage rates get most of the attention, and yes, rate movement plays a major role in monthly payment size. But it’s not the only reason affordability is improving. Three key trends are working in buyers’ favor right now:

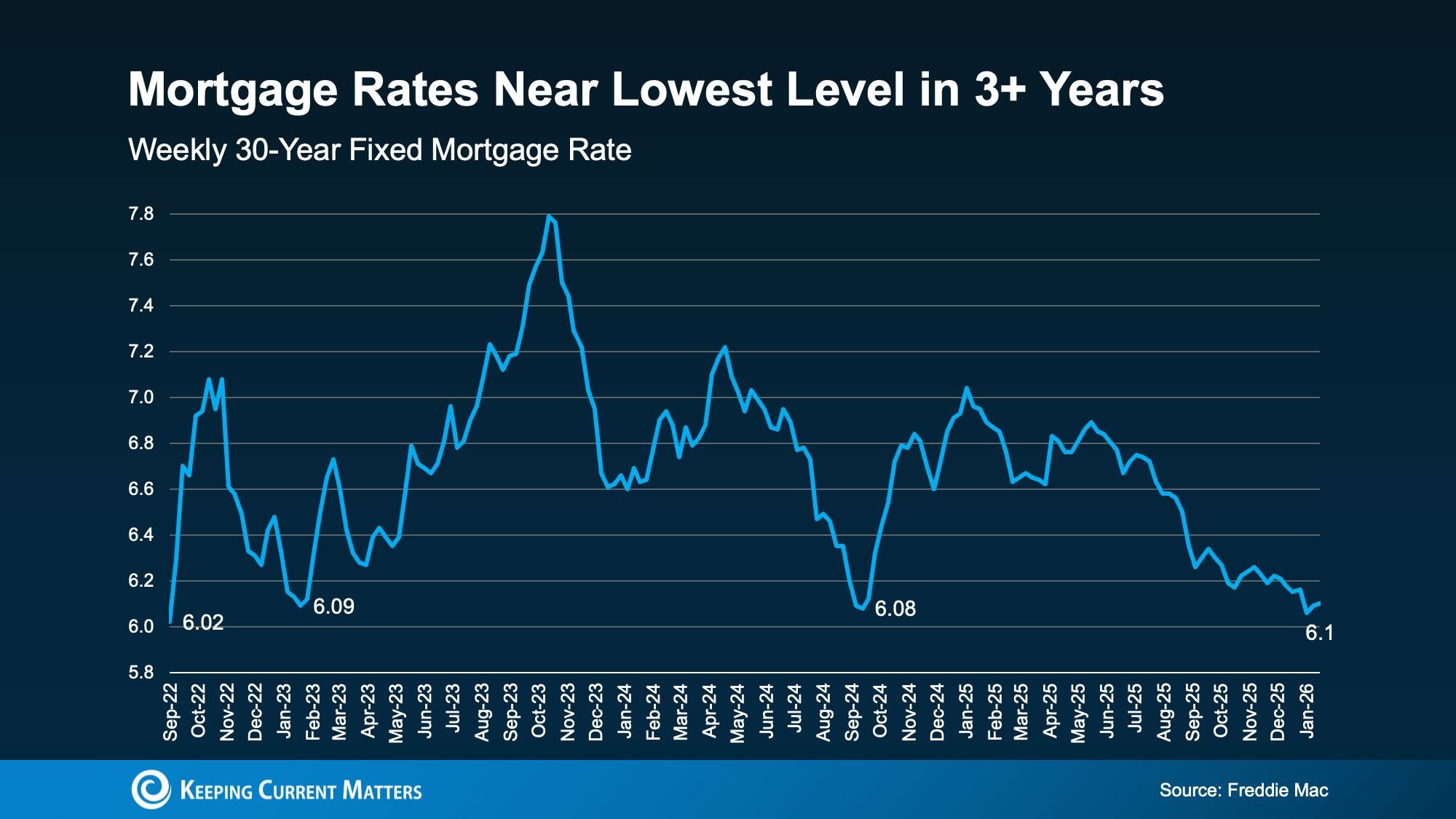

1) Mortgage rates have eased

Rates are near their lowest level in more than three years, which can reduce monthly payments and expand buying power (see graph below):

2) Home price growth has cooled

Home prices aren’t falling nationally, but they’re rising more slowly than they were a few years ago. That matters because slower price growth helps keep purchase prices from jumping as sharply, which can make payments feel more manageable and the overall buying process more predictable.

3) Wages are growing faster than home prices

This is a major factor that often gets overlooked. When incomes rise faster than home prices, buyers can start catching up. Mark Fleming, Chief Economist at First American, explains:

“When income growth exceeds house price growth, house-buying power improves—even if mortgage rates don’t decline meaningfully.”

None of this makes homes “cheap,” but it does help explain why the math is starting to work a bit better than it did even a year ago. In short, some of the forces that curbed affordability are finally easing. As Fleming again explains:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

Because of these combined shifts, many economists expect affordability to continue improving in 2026.

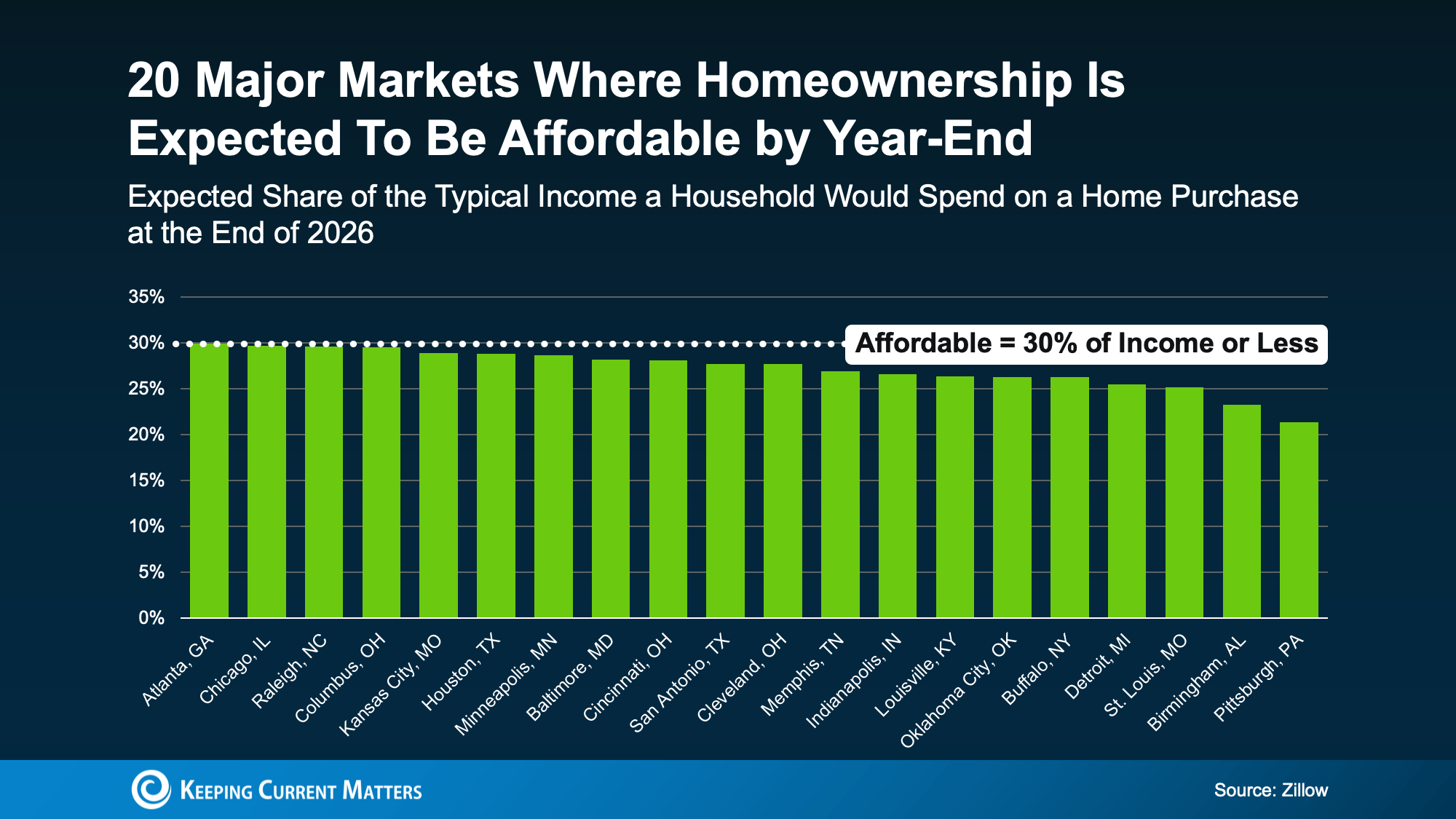

Where Are Homes Becoming Affordable First?

So how much will affordability improve, and where will it show up first? In some places, the difference could be noticeable. Zillow says some markets are expected to fall back under their affordability threshold (30% of income or less) by the end of the year (see graph below):

But you don’t have to live in one of those specific markets, and you may not have to wait until year-end to see improvement. Many areas are already trending in a better direction.

That’s why your next best step is local: talk to a real estate agent who understands what’s happening in your market. The national headlines don’t always reflect what’s going on neighborhood by neighborhood, and you might be closer to buying than you think.

Conclusion

For the first time in a while, home affordability is easing, and that’s an important shift for buyers.

And because the pace of improvement varies by location, understanding what’s changing locally can make all the difference. If you want to see how these trends are playing out where you live, connect with a local real estate agent to talk through your options.

Expert Forecasts Point to Home Affordability Improving in 2026

If the last few years have felt like a constant tug-of-war between home prices, mortgage rates, and “Can we actually afford this?”, you’re not alone. Affordability has been the biggest obstacle for buyers (and a major source of hesitation for sellers), but the outlook for 2026 is more encouraging than what we’ve seen in a while.

In fact, affordability improved meaningfully in 2025, and many industry forecasts expect that progress to continue through 2026. The reason comes down to three forces shaping the market: mortgage rates, housing inventory, and home price growth.

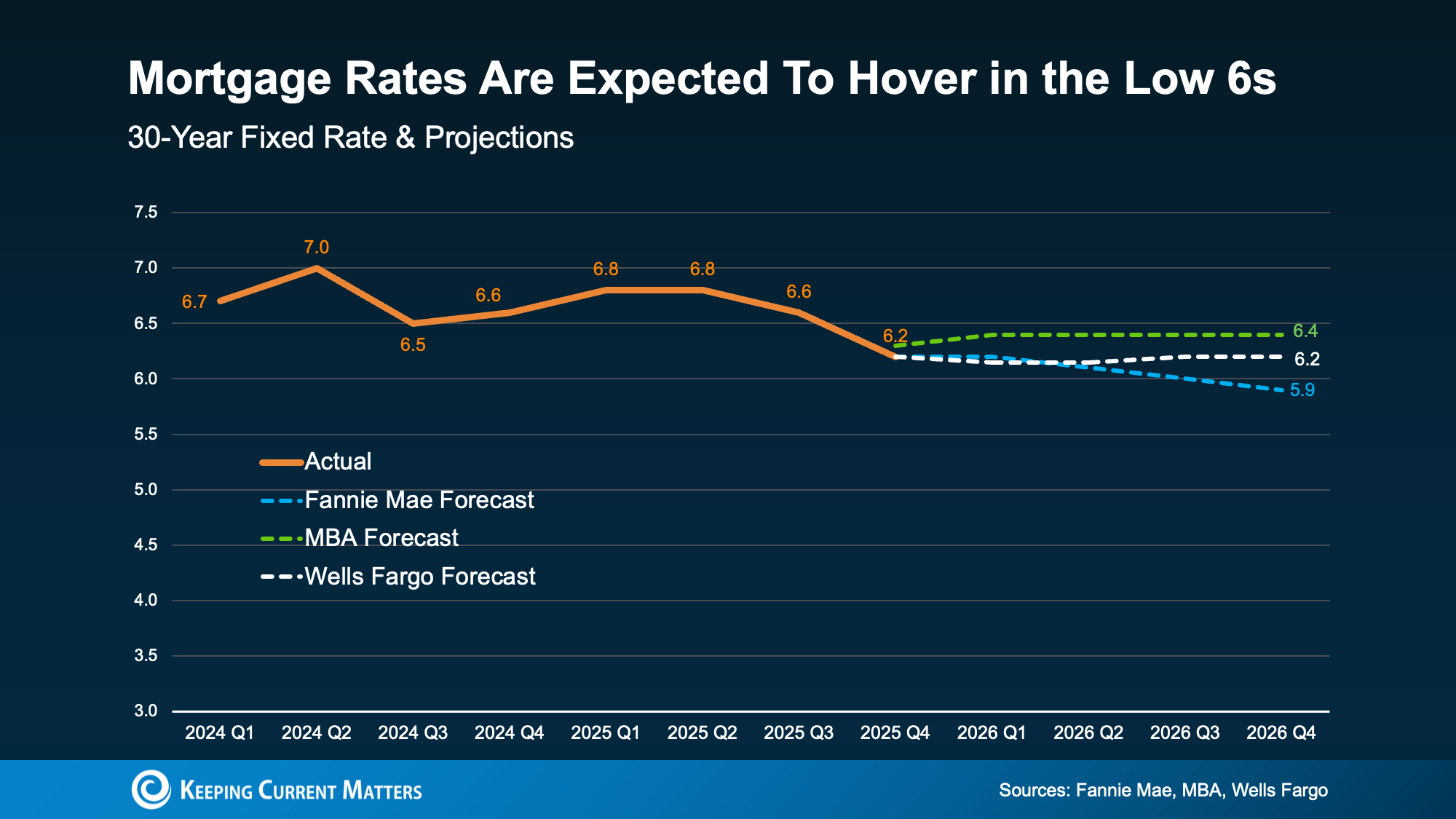

1) Mortgage Rates: Lower Than the Peak, Likely Steadier in 2026

Mortgage rates have already eased from recent highs by nearly a full percentage point over the past year in some measures, and that matters more than most people realize. Even small rate shifts can change monthly payments, buying power, and which homes feel like realistic options.

What experts expect

Forecasts suggest rates may hover in the low 6% range through 2026, though the exact path depends on the broader economy, the job market, and Federal Reserve policy decisions. The key takeaway: rates are already lower than they were a year ago, which helps restore some breathing room for people planning a move in 2026.

What this means for buyers

- Lower rates can reduce monthly payments

- Improved buying power can make more listings qualify as “within reach”

- You may have more flexibility to negotiate when combined with rising inventory

What this means for sellers

- The market is adjusting to the idea that “rates in the 6s” may be the new normal

- If you need to move, it may be more feasible than it looks, especially if you’re sitting on substantial equity

Experts expect mortgage rates to hover in the low 6s or drop even lower as the economy changes in 2026.

2) Housing Inventory: More Homes for Sale, More Leverage for Buyers

One of the biggest changes in 2025 was inventory finally moving in the right direction. With more homes available, buyers got something they haven’t had in years: options—plus more time to compare those options and negotiate.

Inventory is still expected to grow

After a meaningful rise of about 15% in 2025, forecasts call for continued growth in the supply of homes for sale in 2026 (though likely at a slower pace than the last big jump). Realtor.com economists, for example, project additional gains of about 8.9% in active listings this year.

What this means for buyers

- More choices (and fewer “take it or leave it” situations)

- Greater negotiating power—especially on homes that are priced too aggressively or need updates

What this means for sellers

- Pricing strategy becomes critical. In a market with more options, buyers compare everything.

- Strong presentation (clean, staged, repaired) matters more when competition increases

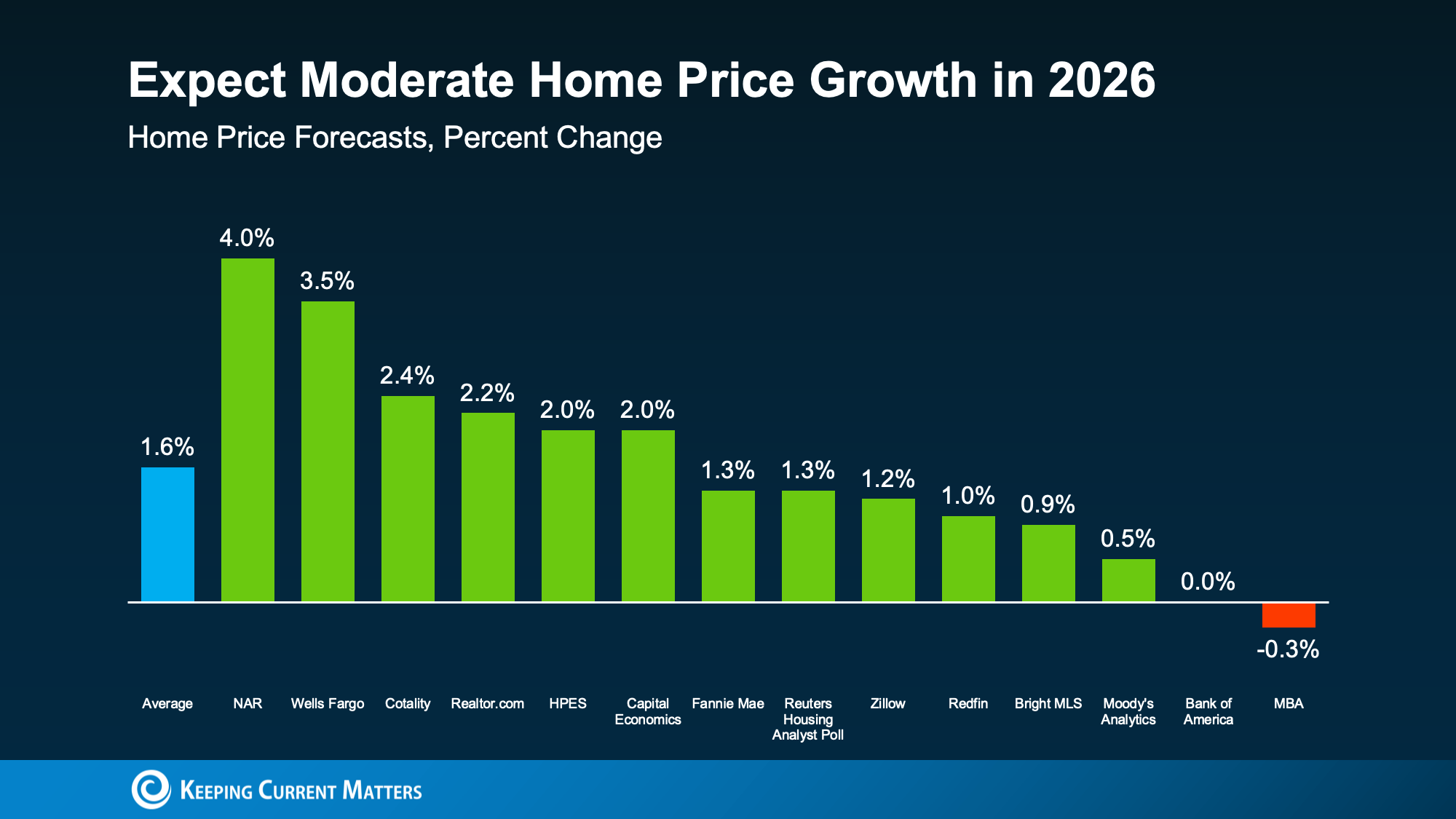

3) Home Prices: Still Rising Nationally, But at a More Sustainable Pace

Here’s what many headlines miss: increasing inventory tends to reduce upward pressure on prices, but it doesn’t automatically mean prices crash. Most national forecasts expect home prices to keep rising in 2026, just more slowly than the rapid spikes of the recent past. On average, experts predict home price growth of about 1.6% in 2026.

Why slower growth can be good news

More moderate appreciation helps buyers plan and budget with fewer surprises, while still supporting overall market stability.

But location is everything. Some areas may outperform the national average, while others could see flat or slightly declining prices depending on local supply, demand, and employment conditions. If you’re serious about a move, a local real estate agent can help you interpret what’s happening in your neighborhood, not just what’s happening nationally.

Home prices are expected to continue rising in 2026, though at a more moderate rate.

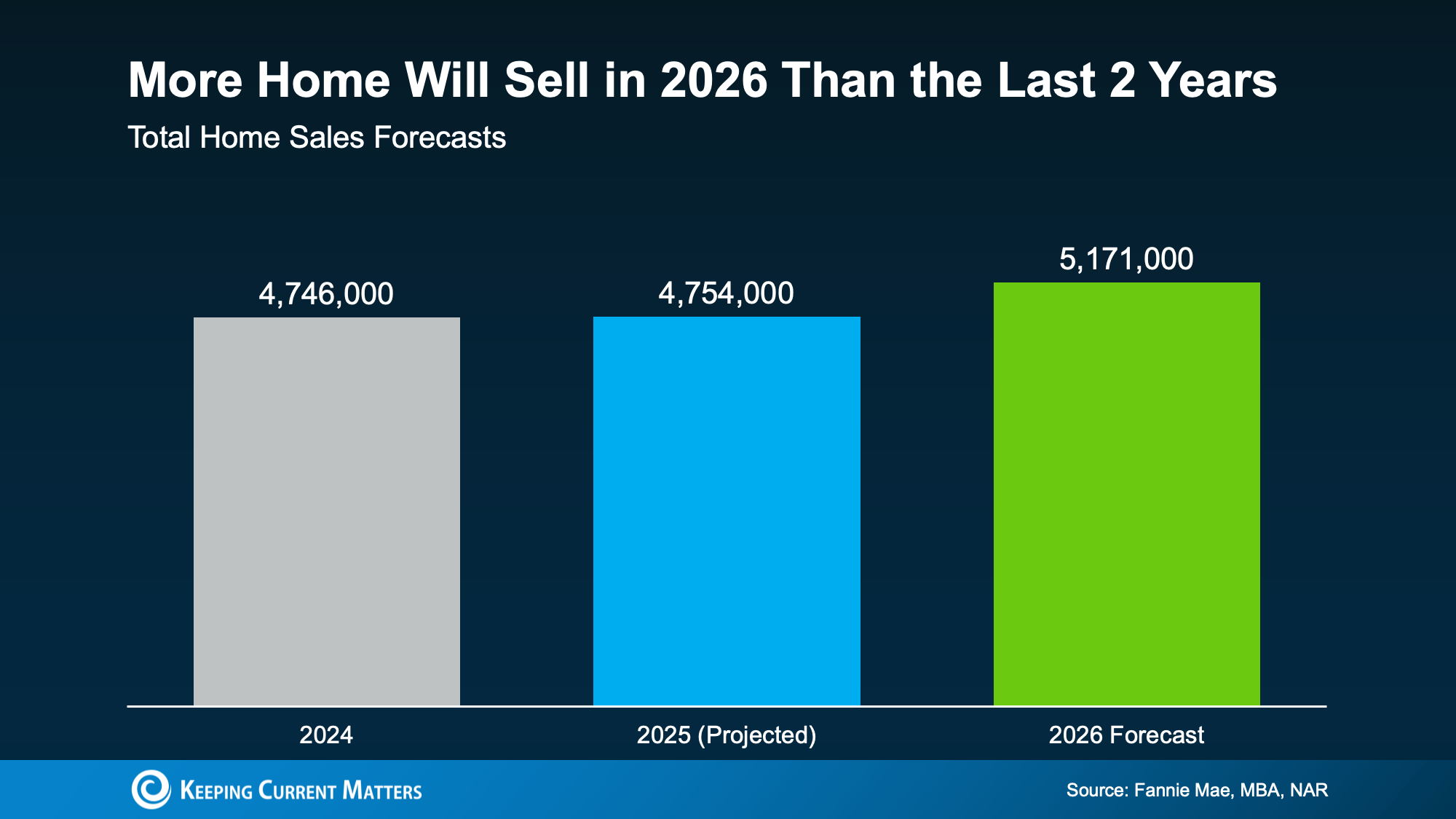

Will More Homes Sell in 2026?

When rates are lower than recent peaks, inventory is improving, and price growth is calmer, you get a healthier affordability equation. That’s why many experts expect more home sales in 2026, as both buyers and sellers find conditions easier to navigate.

As Zillow’s Chief Economist Mischa Fisher notes:

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

Increased affordability in 2026 has experts predicting higher home sales over the past two years.

2026 Could Feel More Balanced Than You’ve Seen in Years

Affordability won’t change overnight. But if current forecasts hold, 2026 is shaping up to be a year with:

- More balance between buyers and sellers

- More predictability in pricing

- More flexibility in negotiations

- More opportunity for people who’ve been waiting on the sidelines

If you’re thinking about buying or selling in 2026, the smartest next step is to get hyper-local: understand neighborhood pricing trends, inventory levels, and what buyers are actually paying (and negotiating) right now.

Ready to start but aren’t sure how? Reach out to us today to connect with an expert agent for all the latest info on your local market.

Renting vs. Buying: Which Home Option Is Right for You?

Between stubborn mortgage rates and rising home prices, you’ve probably mulled over renting vs. buying a home. In market conditions like these, renting and waiting to buy can feel like your only realistic option. This can be the truth in many cases, and buying before you’re ready can be a costly mistake.

But the short-term savings of renting can sometimes trap you in a cycle, preventing you from making wealth-building investments. Over time, this can actually end up costing you more than buying a home early and slowly building equity. Unsurprisingly, a recent survey from Bank of America found that 70% of prospective homebuyers feel renting could hinder their financial future.

Ultimately, the pros and cons of renting and buying come down to your own short-term and long-term financial goals. If you’re feeling torn over whether you should nest or invest, take these major differences into account to decide.

Homeownership Builds Your Wealth Over Time

Apart from giving you your own place to live, homeownership grants the important bonus of building your wealth over time. This is because home prices usually rise as time goes on, meaning waiting longer to buy costs you more. This isn’t always true of every housing market, but the general national trend tends to speak for itself.

The average home sale price has more than tripled in the past 30 years.

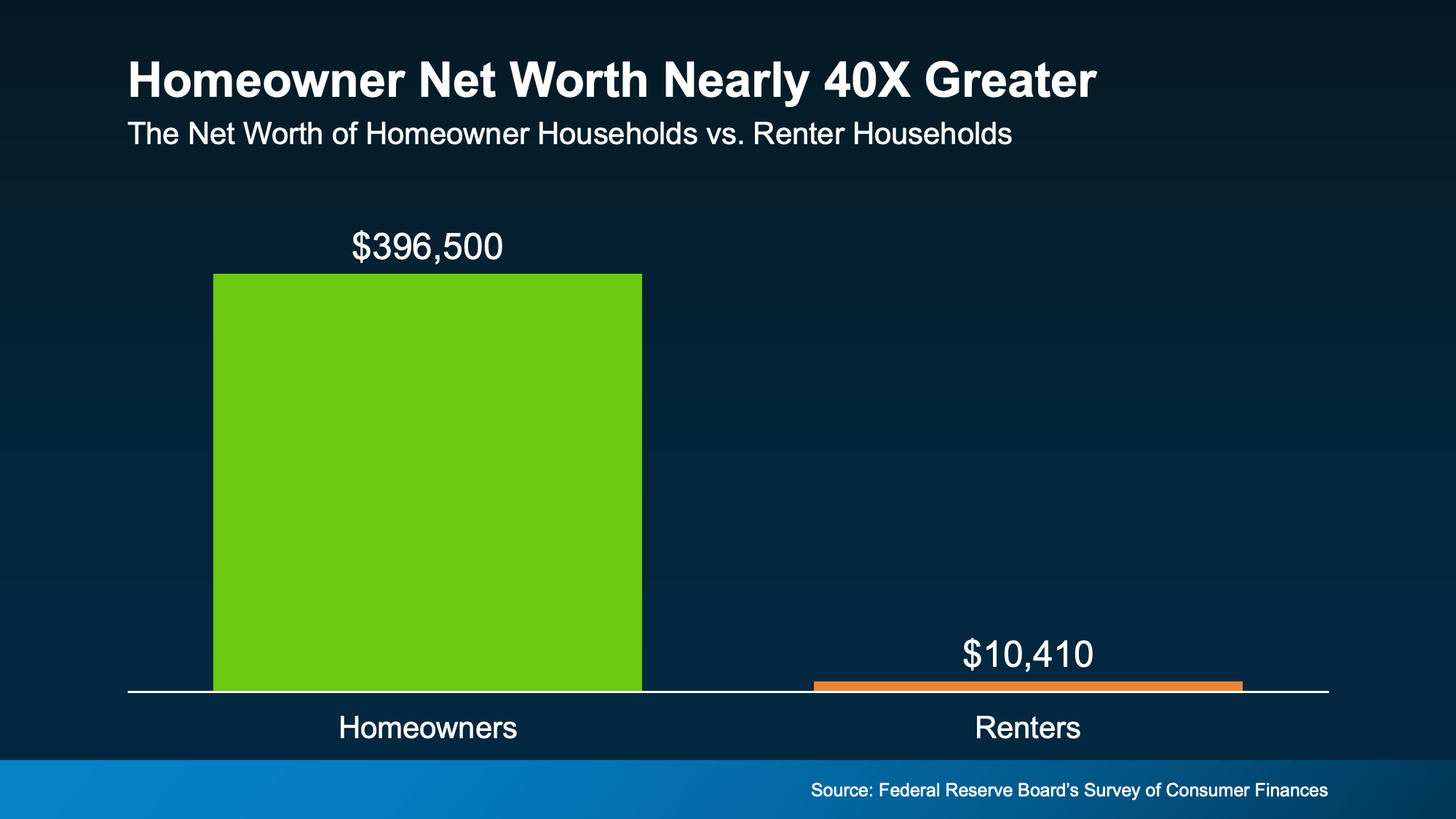

Even better, your home equity also grows over time when you’re a homeowner. Equity is the difference between what your home is worth and what you still owe on your mortgage. Your equity grows with each mortgage payment you make, and this builds your net worth over time.

According to the Federal Reserve, the average homeowner’s net worth is nearly 40 times greater than that of a renter. That’s a life-changing difference, and seeing it represented visually really drives the point home.

The average net worth of a homeowner household is almost 40X greater than that of a renter household.

This massive difference in personal wealth is just one of the reasons that Forbes says:

“While renting might seem like [the] less stressful option . . . owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

Renting Helps You Save in the Short Term

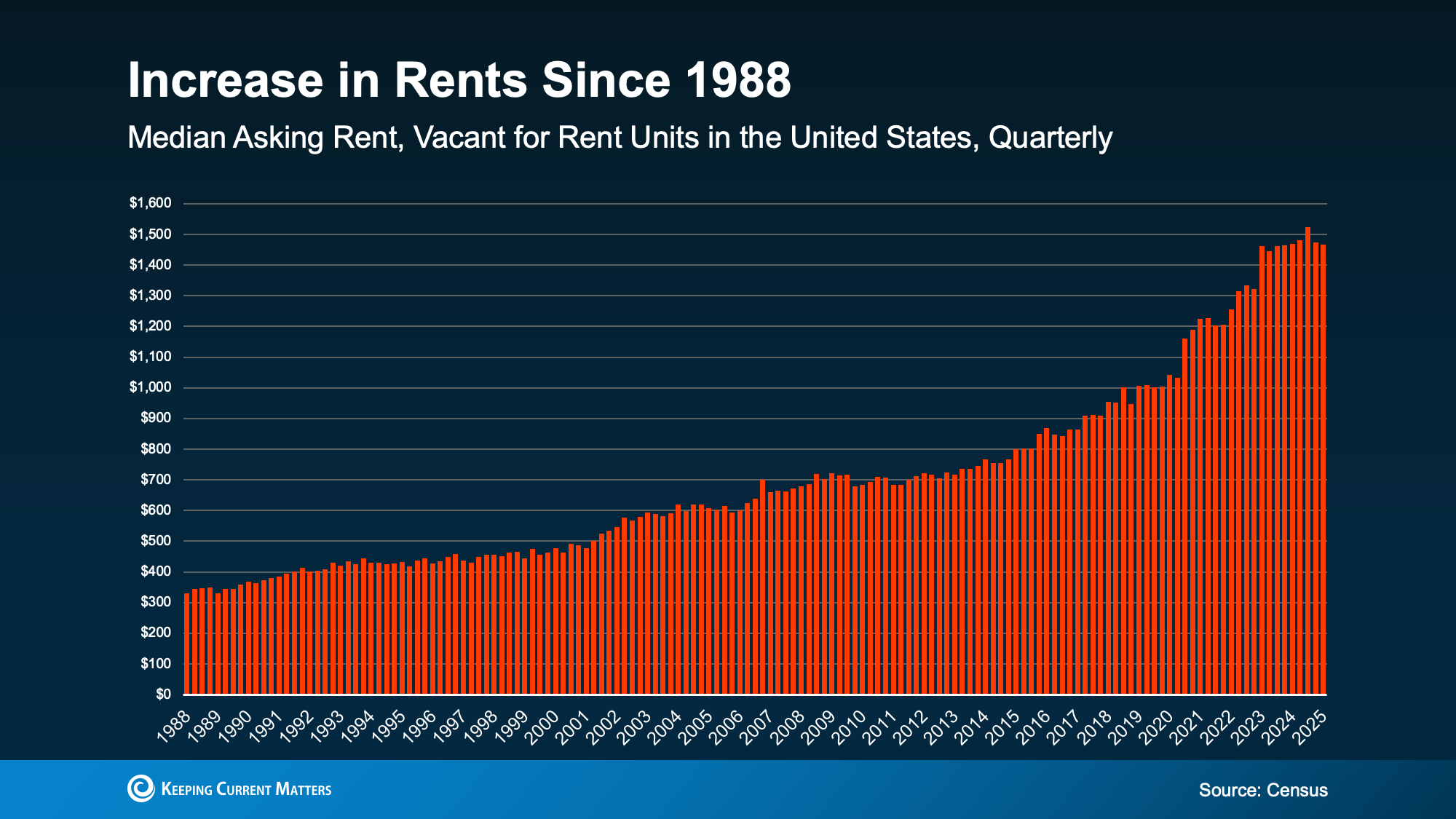

Compared to homeownership, renting offers lower monthly payments and the freedoms of relatively negligible commitment and responsibility. This often makes renting feel like the safer option, and it usually is, at least in the short term. But in the long term, renting can land you in a trap that prevents you from building real wealth.

Rent tends to rise along with home prices, and this has been true for decades. Rental costs have been somewhat stable recently, but they almost never trend downward. This trap of paying increasing rent without building wealth can make buying a home feel impossible.

Like home prices, rental costs have risen dramatically in the past several years.

Financial uncertainty like this can have a real, lasting impact on any of your financial decisions. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

Rent money doesn’t come back to you, and that means it doesn’t grow your wealth. The only mortgage it’s paying is your landlord’s.

So, whether you’re renting or owning, you’re paying off a mortgage. The question is: whose mortgage do you want to pay?

Renting vs. Buying: What Really Matters

Here’s another way to look at renting vs. buying. Rent money is gone once you pay it. Payments toward your own house build equity, like a savings account you can live in. Obviously, buying comes with higher upfront costs and more long-term responsibility. But the reward is a stable investment that grows over time. And while buying a home often feels out of reach, a solid plan can get you there.

As Realtor.com Senior Economist Joel Berner explains:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

Conclusion

Renting may be cheaper in the short term, but it can cost you more over time without building your wealth. If you’re weighing the pros and cons of renting vs. buying, consider your long-term financial goals. Short-term saving can trap you in an endless cycle of renting, but buying without planning can be financially overwhelming.

If you’re ready to make the leap from renting into buying a home, contact us today. We’d be happy to connect you with a local agent who can make your dreams a reality.

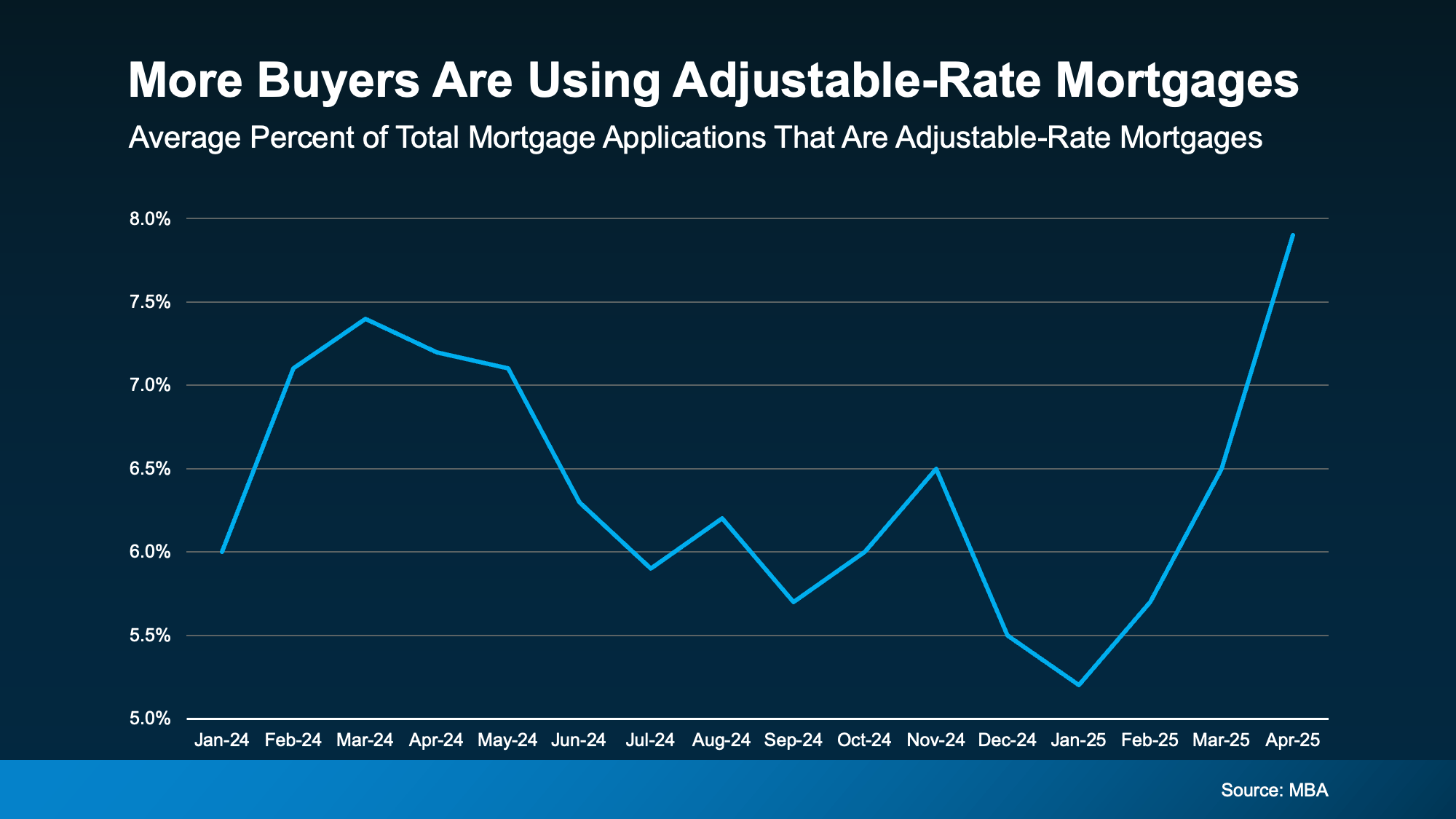

Adjustable-Rate Mortgages on the Rise: Should You Jump In?

If you’re in the market for a house, you’re probably not encouraged by today’s mortgage rates. Elevated rates and rising home prices have many homebuyers starting to explore other financing options that make more sense. One type of loan gaining popularity is adjustable-rate mortgages (ARMs).

If you remember the 2008 market crash, you may be wary of new types of loans. It’s wise to be cautious, but there’s no need to worry. Today’s ARMs much safer and stricter than the ones you may remember from 2008.

During that time, some buyers held loans they couldn’t afford once their rate adjusted. Today, lenders are more careful, and determine whether you can afford an increased rate before the loan is ever offered. This time, ARMs are returning thanks to creative buyers looking for affordable ways to buy a home..

According to recent data from the Mortgage Bankers Association (MBA), more buyers are using ARMs to buy this year.

How Does an Adjustable-Rate Mortgage Work?

If you’ve never heard of ARMs before, you may be wondering what they are, and if they’re right for you. Here’s how Business Insider explains the main difference between a traditional fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Taxes or homeowner’s insurance can still influence a fixed-rate loan, but your baseline mortgage payment typically changes very little. Meanwhile, adjustable-rate mortgages can potentially change drastically in either direction after your initial payment period ends. Depending on your situation and anticipated market trends, this could either work for you, or be far too risky.

Pros and Cons of Adjustable-Rate Mortgages

With ARMs on the rise in 2025, it’s clear that more buyers are finding them appealing. Under the right conditions, they may offer attractive upsides, like a lower initial rate. According to Business Insider again:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

Remember that if you have an ARM, your rate will change over time. As Barron’s explains, they can potentially cost you more in the long run:

“Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up.”

While the upfront savings can be helpful now, consider what could happen if your initial rate ends before you move. Even though rates are projected to ease a bit over the next couple years, nothing is ever guaranteed. Before you choose an ARM, talk with your lender and financial advisor about all your options, and the potential risks.

Conclusion

For certain buyers, adjustable-rate mortgages can offer some big advantages, but this won’t be true for everyone. Understand how they work and whether their pros and cons make sense for you financially. Always talk to a trusted lender and a financial advisor before making entering into a new mortgage.

Need help connecting with a trustworthy lender in your area? Reach out to us for help today.

Are You Waiting To Buy? This Spring May Be Your Time To Move

Between low inventory, high home prices, and unpredictable mortgage rates, 2024 was a rocky year for real estate. It should come as no surprise then that 70% of buyers stopped their home search last year. If you were one of them and are still waiting to buy in 2025, this spring could be your time.

The Drive of Housing Inventory

Many homeowners who put their move on pause last year are reentering the market this year. This means higher, stronger listing inventory, and with builders finishing more homes, new construction inventory is growing as well. Together, this creates more options for buyers like you, and better chances of finding the home you’ve waited for.

But that’s only part of the story. When you’re selling, you want to feel confident that you’ll find a home you’ll be thrilled to move into. At the same time, you don’t want housing inventory so high that your current house sits on the market. Fortunately, the spring 2025 market is striking a balance between supply and demand that many have waited for.

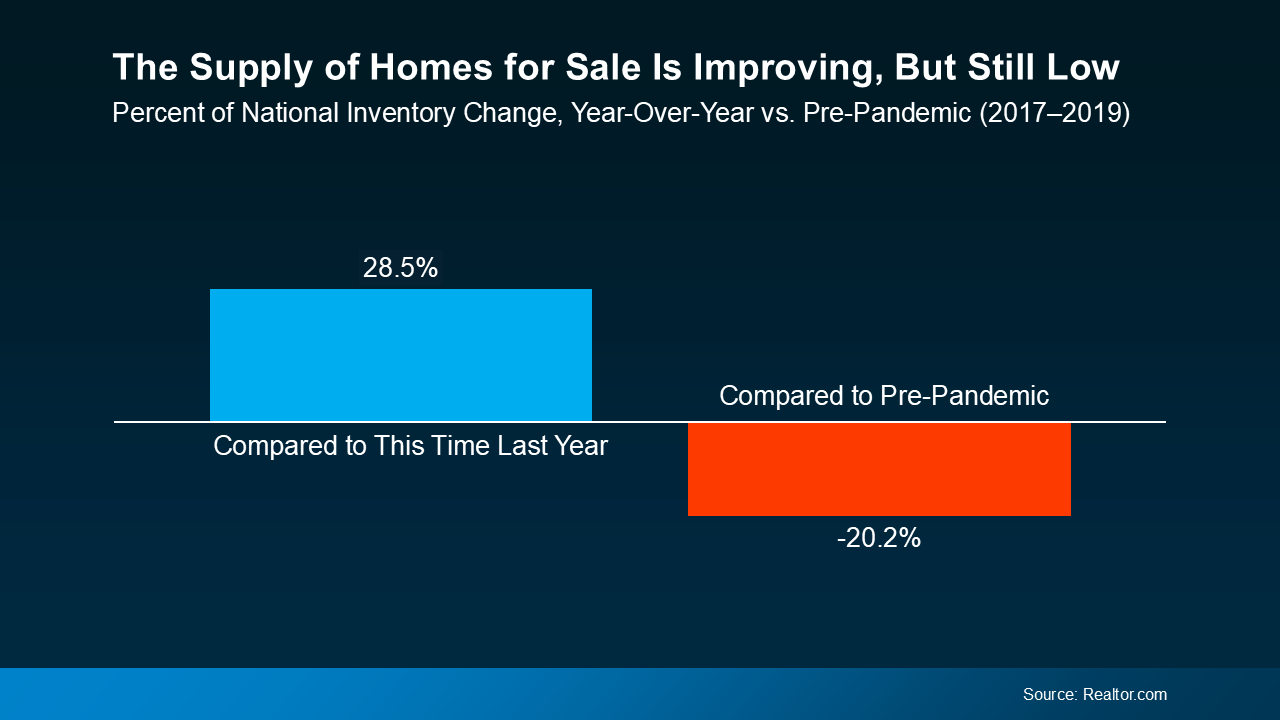

According to research from Realtor.com, housing inventory has jumped 28.5% year-over-year, making March the 17th straight month of inventory growth. This is still below pre-pandemic levels in most markets, but it’s a sweet spot for anyone waiting to buy.

For patient buyers, this means you’ll have more options when moving, but not so many that your current house won’t sell. As long as there’s a healthy demand for homes in your area, your house should still sell relatively quickly. Especially if you work with a local agent to make sure it’s priced right and fixed up to maximize value.

The Sweet Spot: More Options and Steady Demand

Here’s another promising point to think about. As we said, Realtor.com‘s March 2025 data shows that housing inventory has been rising for 17 consecutive months. What’s better, industry experts agree that listing inventory is likely to continue climbing through 2025. According to Lance Lambert, the Co-Founder of ResiClub:

“The fact that inventory is rising year-over-year . . . strongly suggests that national active housing inventory for sale is likely to end the year higher.”

If this prediction proves correct, this spring may be a better time to sell than you think. Listing now could help your house may stand out more than it would later in the year as inventory grows. With more homeowners reentering the market, waiting too long could make it all the more difficult to stand out.

Conclusion

If you’re one of the many who have been waiting to buy a house this past year, here’s your chance. Housing supply is growing but hasn’t caught up to demand yet, meaning new listings are still getting extra buyer attention. Meanwhile, increasing inventory is giving current homeowners more opportunities to scale up, further driving supply and activating buyers.

For both first time buyers and homeowners waiting to sell, this spring’s market is trending toward an ideal sweet spot. If you have questions keeping you from making your move, reach out to us for answers today. We can get you the info you need, or connect you with an agent to navigate your unique local market.

Should You Buy a Home This Spring or Wait for Lower Prices?

You’re probably familiar with the saying “The best time to plant a tree was yesterday, but the next best time is today.” It’s a valuable lesson about future planning and investment that, surprisingly, applies to the decision to buy a home too.

Even though buying a home is a major financial expense, it’s also a major investment that grows over time. As the price of your home increases over time, the value of the equity you’ve built grows with it. And while waiting for prices to drop may be an attractive option, trying to time the market rarely works.

But here’s something to consider: the longer you wait to buy a home, the more your patience could cost you. Let’s explain why.

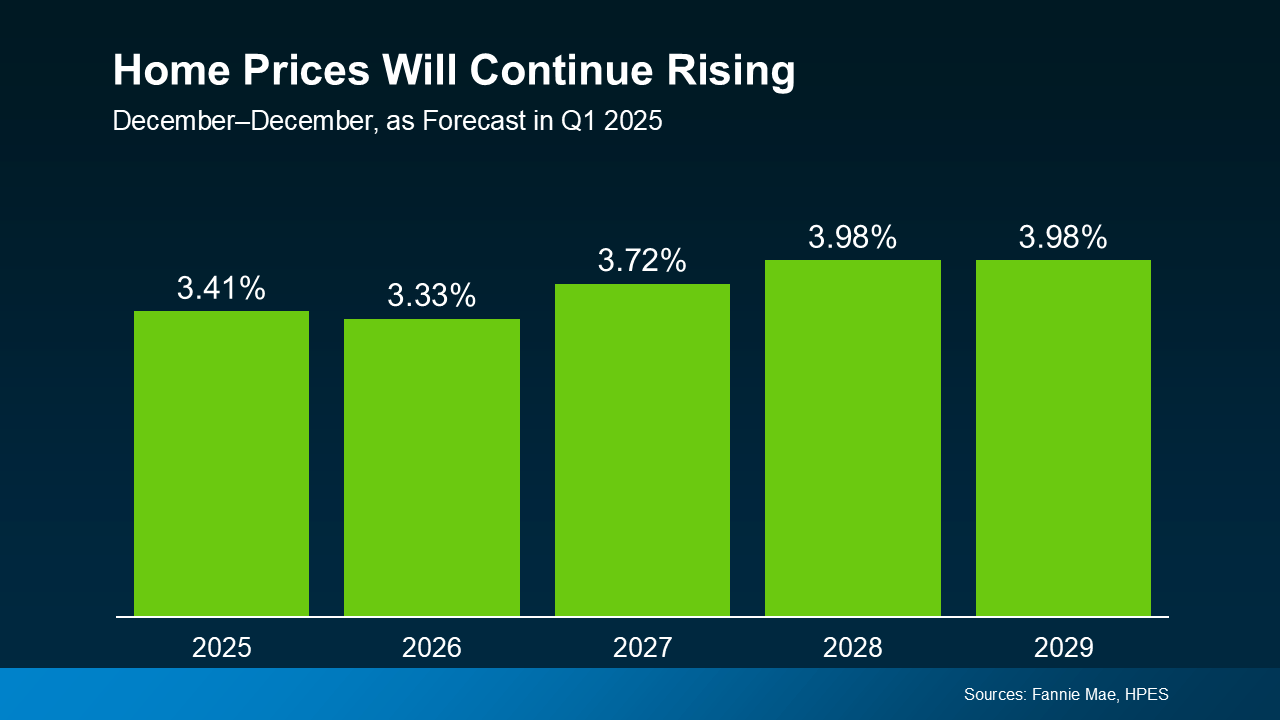

Home Prices Are Expected To Continue Climbing

Each quarter, over 100 housing market experts respond to Fannie Mae‘s Home Price Expectations Survey (HPES). Consistently, the survey results show experts agreeing that home prices will continue to rise through 2029 or even longer.

Sharp price increases may be behind us, but experts predict steadier, healthier increases of 3-4% per year moving forward. This rate of increase will vary by market from year to year, but it’s much closer to normal. Reliable growth is a promising sign for hopeful buyers, and the housing market at large, as the graph below demonstrates.

Even in markets experiencing slower price growth or short-term decreases, the steady gains of homeownership eventually win in time. After all, a growing, long-term financial investment will always beat a one-time discount.

Here are the main points to remember:

- Home prices will be higher next year. Experts don’t expect home prices to fall any time soon, at least at the national level.

- Waiting for a perfect mortgage rate or price drops is a gamble. With only slight dips in mortgage rates expected in the near future, price increase could outpace any potential mortgage savings. Unless home price growth is slow or mortgage rates are low in your area, waiting will likely be more expensive.

- Buying early means building more equity. When you invest in homeownership early, your equity and appreciating home value reward you in the long run.

The Costs of Waiting To Buy

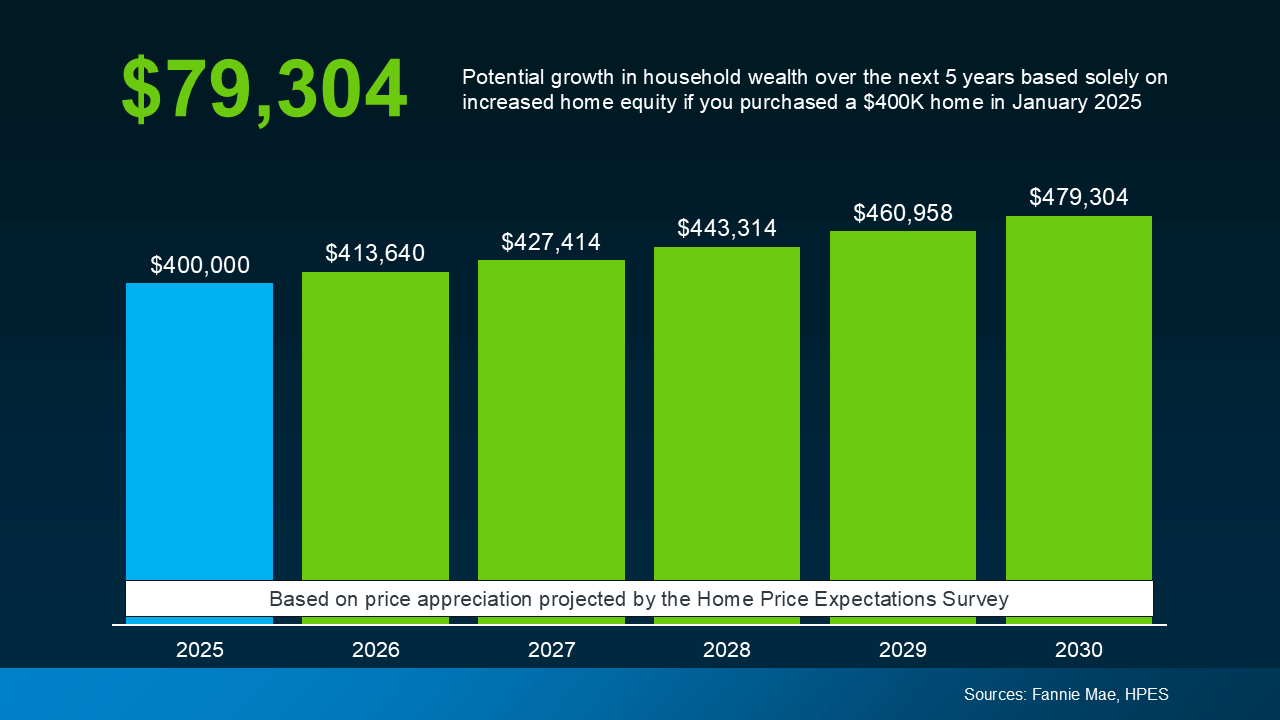

To demonstrate how these theories play out in real-world numbers, here’s a typical example. If you were to buy a $400,000 house in 2025, it could gain almost $80,000 in value by 2030. The graph below demonstrates how this value appreciates year by year based on the expert data we mentioned earlier.

This can be a considerable difference in your future wealth and why buyers who invest early are often glad they did. When it comes to building wealth through long-term investment, time in the market matters.

The question to consider isn’t “Should I wait to buy?” It’s really “Can I afford to buy now?” Just like planting a tree, making short-term sacrifices to buy a home will eventually pay off in the long-term.

Between rising prices and stubborn mortgage rates, today’s housing market is challenging, but achieving homeownership is far from impossible. Exploring different neighborhoods, seeking alternative financing options, or applying for down payment assistance programs can all make a critical difference.

What’s most important is acting decisively when you’re able to, instead of waiting for a perfect opportunity that never comes.

Conclusion

If you’re interested in buying but still undecided, take the time you need to make the right choice. But, remember that realizing an investment takes time, and the sooner you make one, the sooner you’ll be rewarded.

If you’re curious about what’s happening with prices in our local area, then reach out to us. Even if you’re not ready to buy, an expert local agent can fill you in with the info you need.

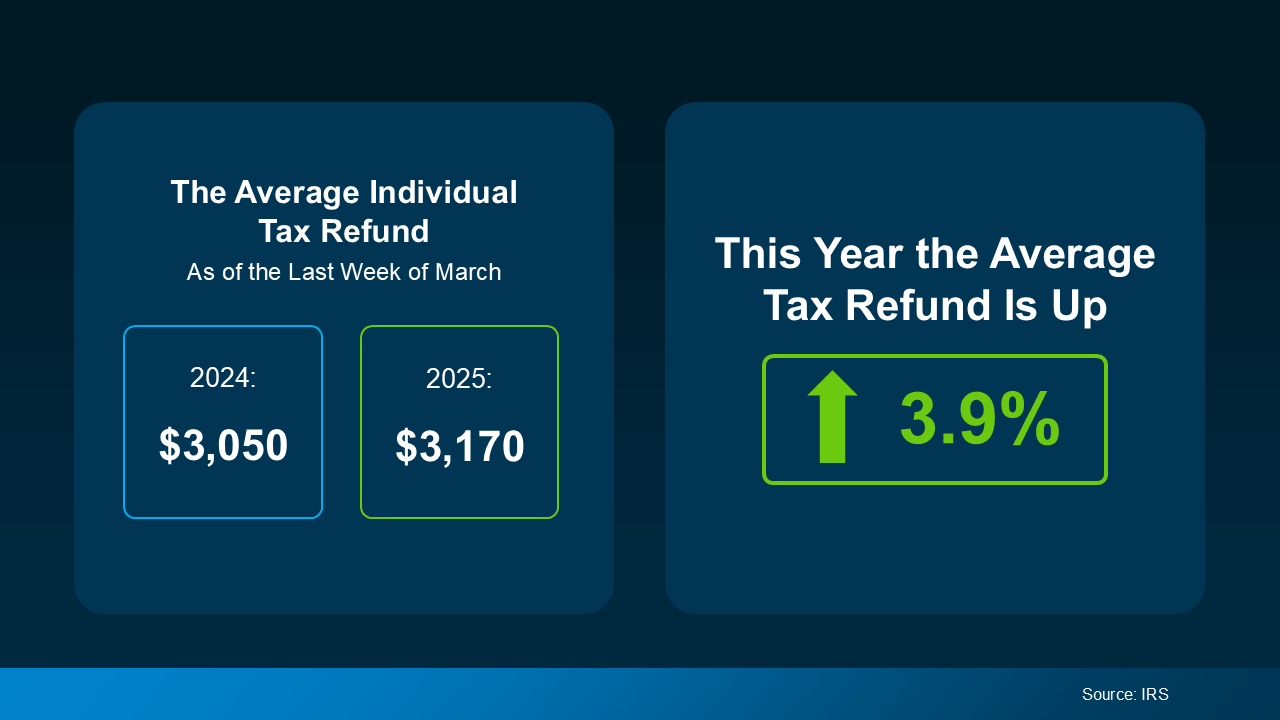

It’s Tax Day – Here’s How a Refund Can Help You Save For a Home

If you’ve been planning to buy a house, you know how hard it can be to save for a home. What you might not know is that your tax return can be a helpful boost to your savings and budget. According to a recent post by Freddie Mac:

“ . . . your tax refund from the IRS can be a useful supplement to your homebuying budget.”

So if you’re planning to get a tax refund this year, consider the difference that extra funding can make. A refund can help you pay for the upfront costs of homebuying, like a down payment or closing costs. And, according to the IRS, your tax refund may even help you out this year more than ever.

How a Tax Return Can Help You Buy a Home in 2025

Recent data from the Internal Revenue Service (IRS) has found that the average individual’s refund is 3.9% higher this year. And while that’s not a huge increase, it can make a big difference if you’ve been struggling to save. The graphic below visualizes the new IRS data, comparing the average tax return in March 2024 to March 2025.

Your own personal tax refund will likely vary, but any financial boost helps when you’re saving for a home. According to Freddie Mac, the following are several ways you can put your tax return to good use when homebuying:

- Saving for a down payment – A down payment on a home is often one of the biggest obstacles to homeownership that buyers face. Saving your tax refund for a down payment can be a smart way to make this major step easier. Keep in mind while a 20% down payment may be common, it’s not typically a hard requirement to buy.

- Paying for closing costs – Usually due at closing, closing costs include fees for services like the appraisal, title insurance, and underwriting of your loan. While these vary by state, they’re often between 2% and 6% of your home’s total final purchase price. As a much lower percentage of your home’s price, closing costs can be a great use of your yearly refund..

- Lowering your mortgage rate – Lenders sometimes give buyers the option to buy down their mortgage rate if they qualify. This allows buyers to pay an upfront fee to lower their initial mortgage rate, reducing monthly payments in the short-term. This option can be particularly helpful if interest rates and mortgage payments are a major homebuying hurdle you’re facing..

Financially speaking, this may be more complicated in practice, but there’s no need to do it all on your own. Working with an experienced, trustworthy real estate professional can simplify your financial planning, helping you reach the best decision possible. An agent who understands the homebuying process, your unique financial needs, and your personal goals can make all the difference.

Conclusion

If you’ve been saving for a home, you already know well that every penny counts. Your tax return probably won’t be the final financial boost you need, but there are ways to use it effectively. Planning and identifying how to best spend that money can give you a real, meaningful step toward buying your home.

Are you eager to buy a home but having trouble making things work? Contact us today. We can connect you with local lenders and agents to help make your dream of homeownership a reality.

Get Ready: The Best Time to List Your House This Year Is Coming Soon

If you’re waiting for the best time to list your house this year, then wait no longer. Experts have looked at the data, and the best week to list your house in 2025 is almost here.

A recent study from Realtor.com analyzed years of housing market trends and found that April 13–19 is expected to be the best week this year to list your house:

“. . . we’ve identified April 13-19 as the best week to list for sellers . . . a seller listing a well-priced, move-in ready home is likely to find success. Because spring is generally the high season for real estate activity and buyers are more plentiful earlier rather than later in the year, listing earlier in the spring raises a seller’s odds of a successful sale.”

Why Is This the Best Time?

Spring is typically a strong season for sellers and when the housing starts to really take off every year. But according to Realtor.com, this window could be particularly advantageous in 2025 thanks to a few key factors. Here are the biggest influences that make April 13-19 the ideal week for new listings:

- More potential buyers are looking at your home since demand is usually highest in the spring and summer every year.

- A faster, easier sale since many serious, committed buyers are eager to move before summer.

- Higher chances of getting the best offer. According to Realtor.com, you could get $4,800 more on average this week, and $27,000 more than earlier in the year.

Want Your House Listed at the Best Time? Start Now

Only a couple weeks are left before the year’s prime listing week, but you can still make the deadline. If you’ve been planning to list for a while, a smart plan and quick action can make it happen. This is where working with a great local real estate agent can make all the difference between selling and not. An expert agent can help you:

- Figure out exactly what you need to do to get your home ready to list and, eventually, sold.

- Prioritize the tasks to make the biggest impact on your listing and chances of selling in the shortest time.

- Identify any quick fixes or easy upgrades to help you attract as many potential buyers as possible.

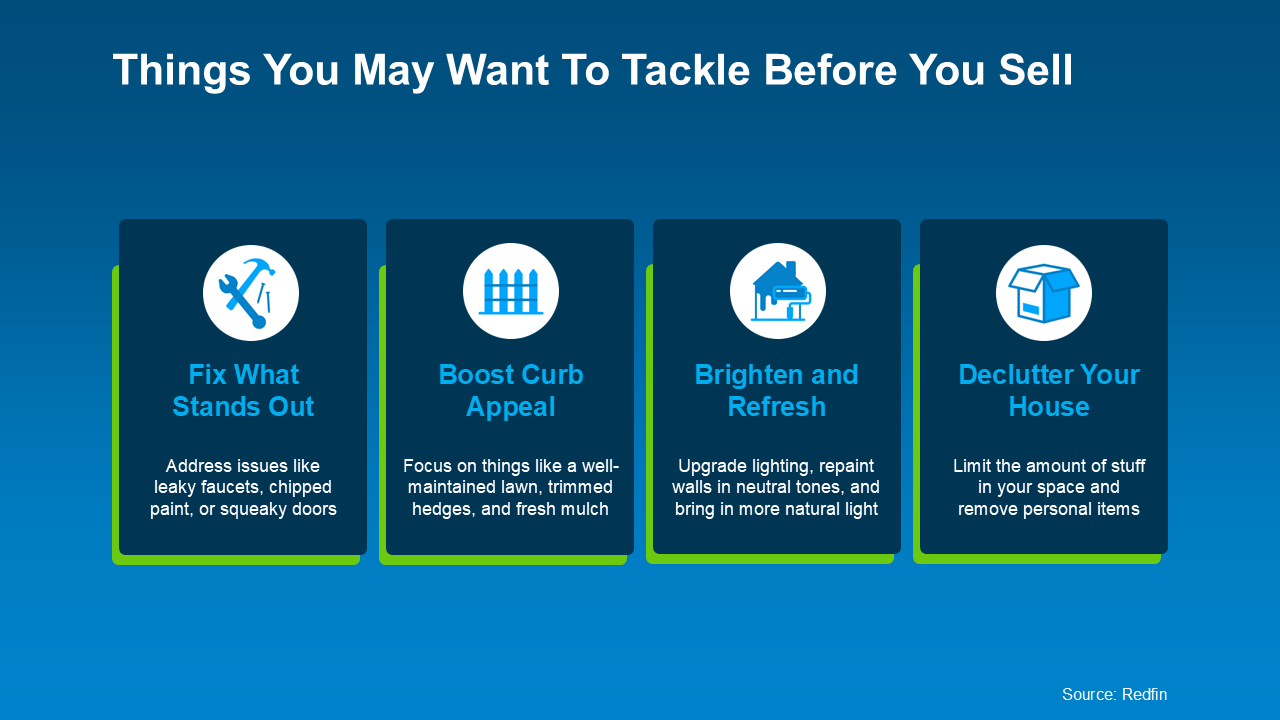

If your house is already in good repair and condition, your focus should be on quick, value-adding updates. The idea is to eliminate any potential dealbreakers for interested buyers, as Investopedia says:

“You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”

With the April 13-19 window fast approaching, the quicker you can finish these projects, the better. Here are some small projects recommended by Redfin you can do that can make a big difference to interested buyers:

What if You’re Not Ready to List?

If you don’t think you’ll be ready to list before this windows passes, then don’t worry. Even though Realtor.com expects April 13–19 to be the best time to list, it’s not the only good time to sell. What’s most important is getting your home ready to maximize its attractiveness to buyers when you do decide to list. Even if you list a bit late, there’s still plenty of opportunity before prime homebuying season is over.

Conclusion

If you’ve been waiting for just the right moment to sell, April 13-19 could be the perfect time. Realtor.com projects this as the best time to list your house this year, but there’s a bit more to consider. Making sure your home is fully prepped and priced competitively for your local market can make the difference.

Ready to list but need a real estate agent’s advice and expertise first? Reach out today and we’ll connect you with a local expert who can help you list and sell your home fast.

The Spring 2025 Housing Market: 4 Things To Expect

Spring is in full swing, and the spring 2025 housing market is swinging along with it. Wondering whether now is the right time to finally buy a house or sell your home? Here are four trends you can expect in the market this year, and what they mean for you.

1. More Homes on the Market

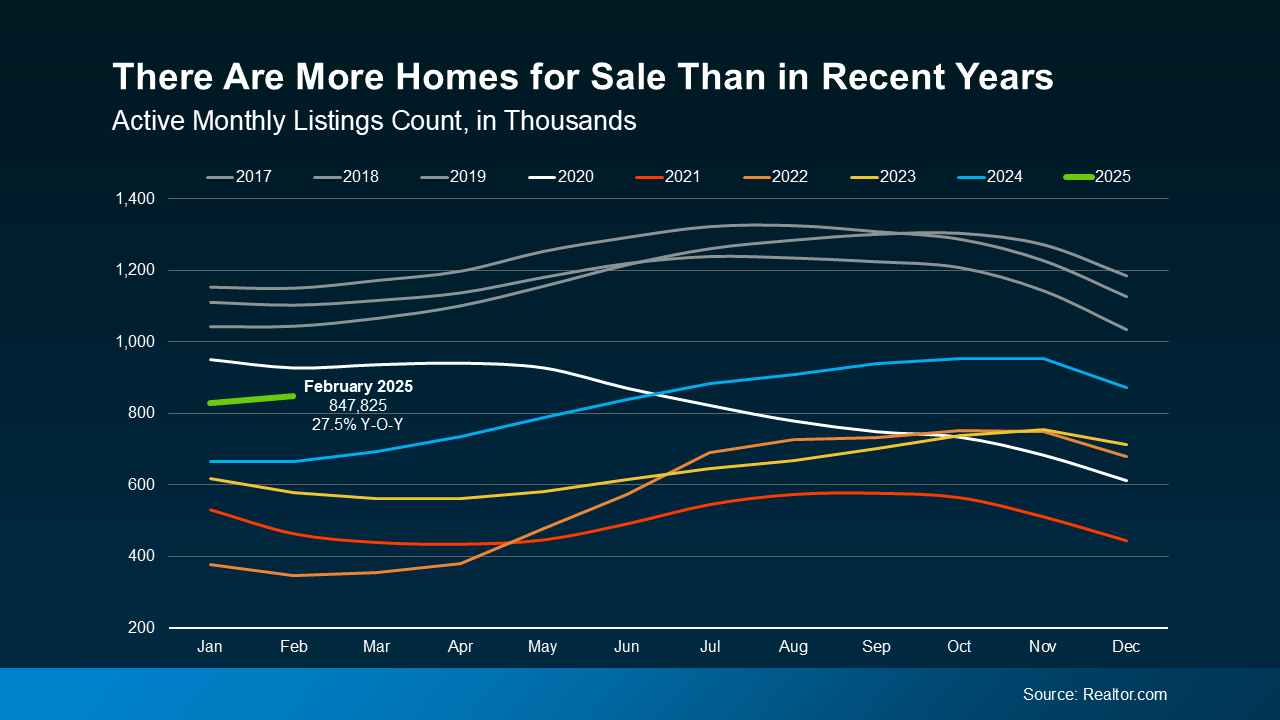

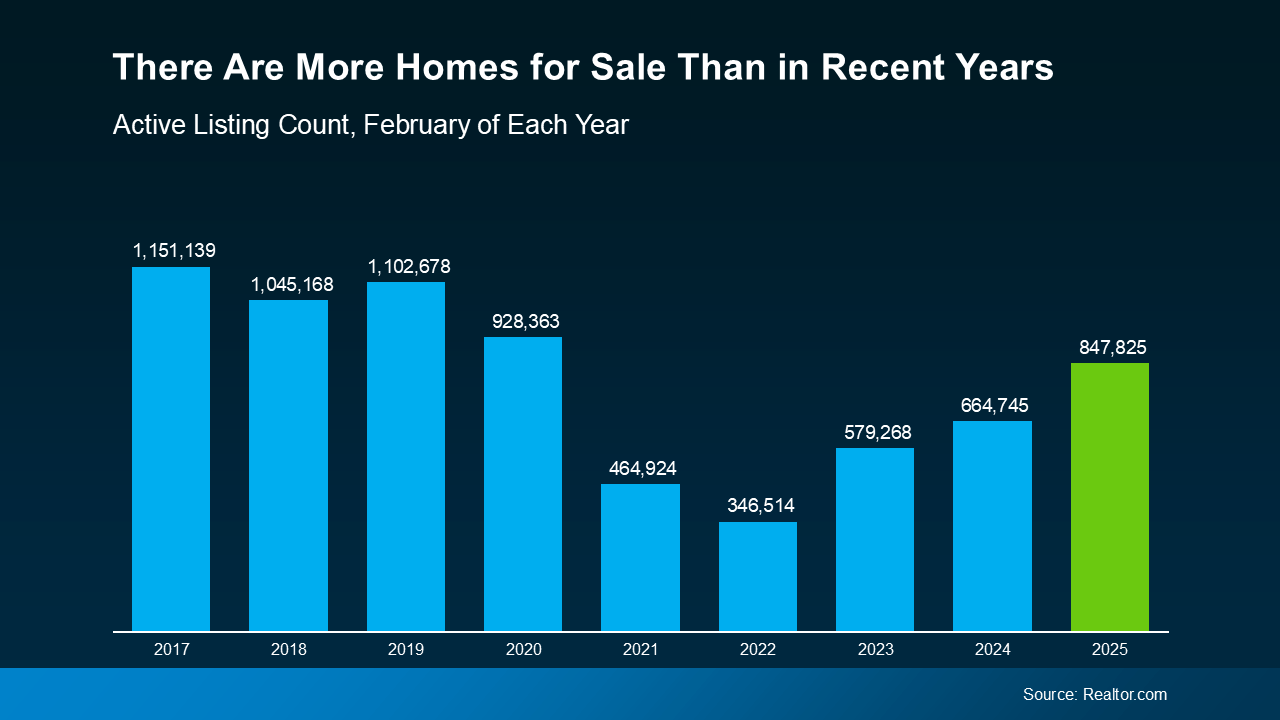

After years of housing shortages nationwide, the number of homes for sale is finally improving. According to recent national data from Realtor.com, active home listings are up 27.5% compared to this time last year. Housing inventory took a tremendous dive in 2020, but at long last, it’s close to reaching pre-pandemic levels this spring.

The graph below shows monthly active listing count for each year dating back to 2017. As you can see, even though inventory levels still haven’t quite returned to pre-pandemic norms, they’ve improved over last year. In fact, they’re almost at 2020 levels, and will likely exceed them this summer if their upward trend continues.

For Buyers: More housing inventory means you have more options and choices. Having options means you can be more selective, and that sellers may be more willing to negotiate with you.

For Sellers: With more homes available, you’re more likely to find the right house to move into. With inventory still below normal levels, your current home will stay in higher demand, at least until home supply normalizes.

2. Home Price Growth Is Slowing

As inventory increases, the rate of home price growth is slowing down as prices respond to buyer demand. This will continue through the spring 2025 housing market and beyond into 2026 if the current trend holds steady. With more homes for sale, eager buyers are less pressured to compete for limited inventory. Price growth will continue to slow as supply rises and buyers enjoy more options, but it will generally remain positive. A recent projection from Freddie Mac says:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

Every housing market is different, so while home prices are rising nationally, this may not be true everywhere. Some markets are actually seeing stronger price growth, while others are slowing or even seeing home prices decline.

For Buyers: Slower home price growth means prices aren’t rising as quickly as before. Still, any home you buy now is likely to appreciate in value over time, helping you build equity.

For Sellers: Home prices are still rising, but you may need to temper your expectations in terms of pricing your home. Pricing too high in a more competitive market could mean your house takes longer to sell. Listing at a price point competitive with your local market is going to become a key factor as prices normalize.

3. Mortgage Rates Are Falling and Stabilizing

One of the biggest obstacles for buyers – especially new ones – since the pandemic has been higher, less predictable mortgage rates. Fortunately, rates have been slowly stabilizing so far in Q1 of 2025, and have even dropped faster than experts anticipated. These aren’t the 3% rates of 2020, but less volatile rates give buyers more reason to buy with confidence. As Chief Economist at CoreLogic Selma Hepp says:

“With the spring homebuying season upon us, the recent improvements in mortgage rates may help invite homebuyers back into the market.”

For Buyers: When mortgage rates are stable, planning ahead is easier because your future payments are likely to be more predictable. But keep in mind that even though mortgage rates are stabilizing, they’re still far from being completely static. When buying, consult your agent and lender to stay current with rates and how they might affect your plans.

For Sellers: Lower rates starting to stabilize means more buyers are becoming active – especially those who have been patiently waiting. This means increases in housing demand and more potential interested buyers for your house.

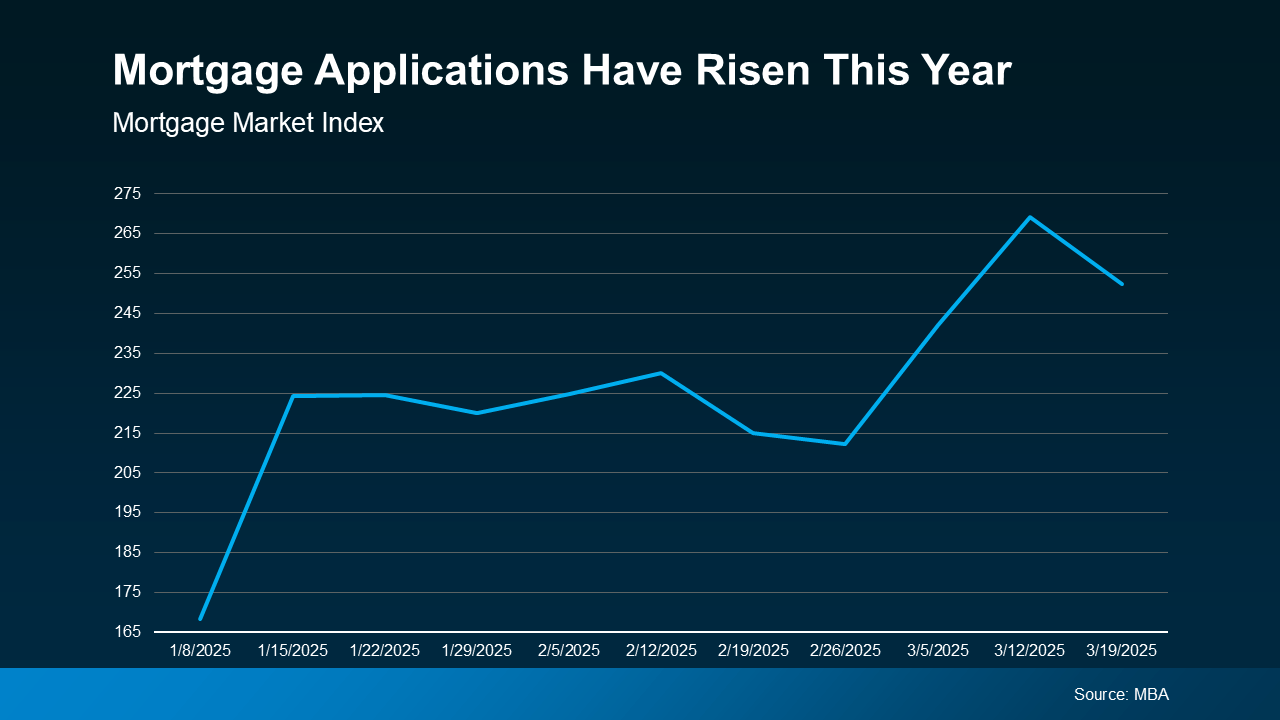

4. More Buyers Are Entering the Market

With more inventory, slowing price growth, and stabilizing mortgage rates, buyers are gaining confidence and finally reentering the market. Demand is increasing, and recent data from the Mortgage Bankers Association (MBA) shows an uptick in mortgage applications compared to the start of the year.

For Buyers: The spring 2025 housing market buying season is quickly heating up. Making your move now and getting a leg up on your competition could be a wise strategy this spring.

For Sellers: Eager buyers wanting to buy a home in the spring or summer are entering the market quickly. Naturally, this is great news for you: more buyers means a better chance of selling your home fast.

Conclusion

Between more homes for sale, slowing price growth, and stabilizing mortgage rates, there’s plenty reason to be positive this spring. Buyers can expect higher housing inventory at more reasonable rates, while sellers can count on a busier market with more activated homebuyers. If you’re wondering how this spring’s trends might affect you, contact us today to get started with an expert agent in your area.

Spring Home Inventory Hits Highest Level in Five Years

The spring 2025 housing market is shaping up to be a great time for buyers. Home inventory has risen to the highest level in five years, which puts more pressure on sellers to negotiate. This grants buyers more power and more options to get the home they really want at a fairer price. Here are just a couple promising things that more houses on the market could mean for you as a buyer.

1. More Homes on the Market To Choose From

The number of homes for sale in February this year was higher than it’s been in five years, dating back to February 2020. This is the strongest home supply seen since the COVID-19 pandemic, and it’s great news for any hopeful homebuyer. The following graph shows new data from Realtor.com illustrating a significant 27.5% increase in home inventory since last year.

While inventory hasn’t returned to pre-2020 levels yet, experts say that inventory is expected to continue rising this year. More houses available means more choices, more options, and more chances to find the house you want. And according to Danielle Hale, Chief Economist at Realtor.com, more inventory will bring other welcome changes to the market.

“Buyers will not only have more home options . . . but they are also likely to find somewhat lower asking prices and more time to make decisions – all buyer-friendly factors as we inch closer to the busy homebuying season.”

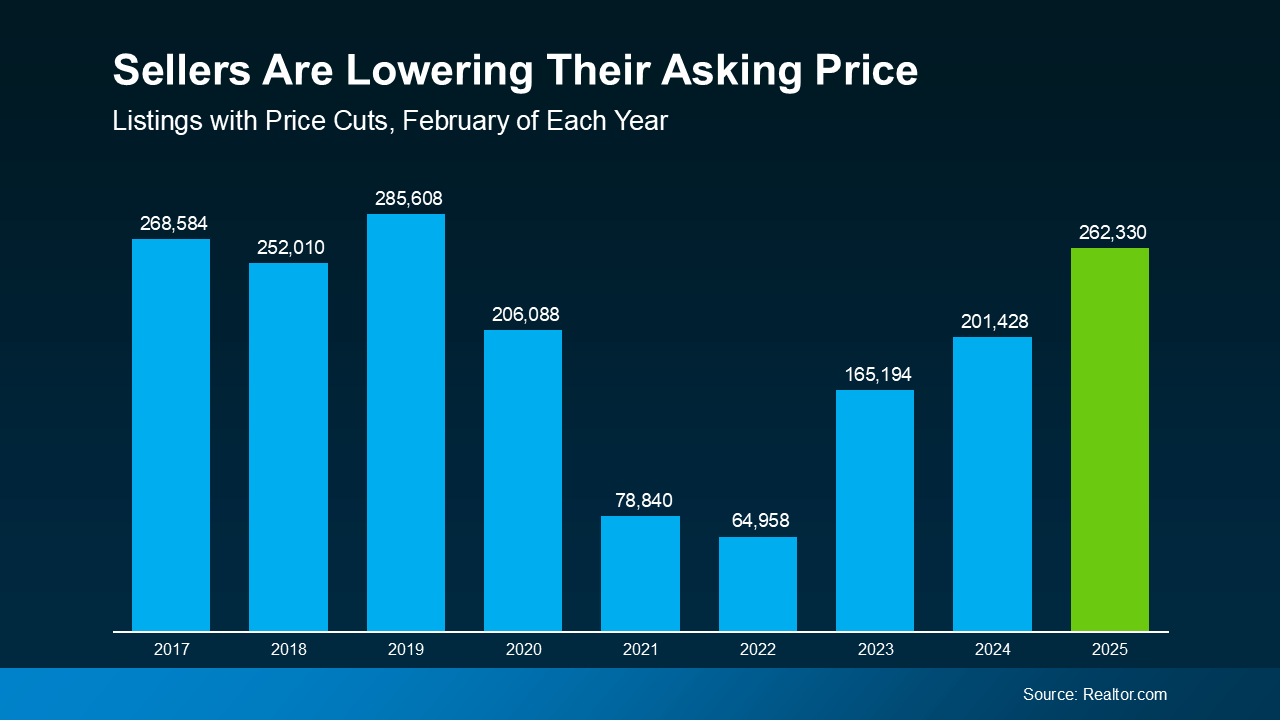

2. Sellers Are More Likely To Accept Price Cuts

When buyers have more options, some homes tend to stay on the market for longer than they otherwise would. This is especially true of homes that are initially priced too high and out of some buyers’ ideal range. When this happens, sellers are forced to drop prices to keep their listing competitive with other houses on the market. And combined with falling mortgage rates, it means a more normalized market and better deals for buyers.

Based on data from Realtor.com, the number of listings with price reductions has increased over the last few years. In fact, price reductions have even risen above the levels seen in 2020, as the graph below illustrates.

Price reductions are a great sign that sellers are more willing to negotiate and compromise today. Compared to the market’s more normal years of 2017–2019, today’s number of price cuts is much closer to what’s typical. For most buyers, this is a welcome relief, and a promising sign of where the market is headed.

For you, this could mean fewer compromises and a better chance to negotiate on price, closing costs, or even repairs. Not every seller is willing to adjust their price, but a higher home inventory means many more will. Either way, healthier inventory levels mean you have more leverage in the market than buyers have had in years.

Conclusion

If you’ve been watching the market and waiting for the right moment to buy, this spring could be the perfect time. Home supply is up, mortgage rates are down, and more sellers are cutting prices to attract eager buyers. Best of all, these trends are expected to continue into the spring, making for a stronger, healthier market for everyone.

For help navigating your unique local housing market, consider connecting with an expert real estate agent. They can talk to you about what’s happening in your area and get you started on your home search. Reach out today and we’ll connect you with a local expert who can find the home you’re looking for.