Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Are Home Prices Dropping? What the Latest Data Show

You’ve probably seen headlines or social posts claiming that home prices are falling. It’s an attention-grabbing message, and it naturally leads to two big questions:

- Is this the start of a crash?

- What does it mean for my home’s value?

Here’s the reality: a few markets are seeing small, normal pullbacks, but this is not a nationwide crash. In most areas, prices are still rising or holding steady, just not at the breakneck pace we saw a few years ago.

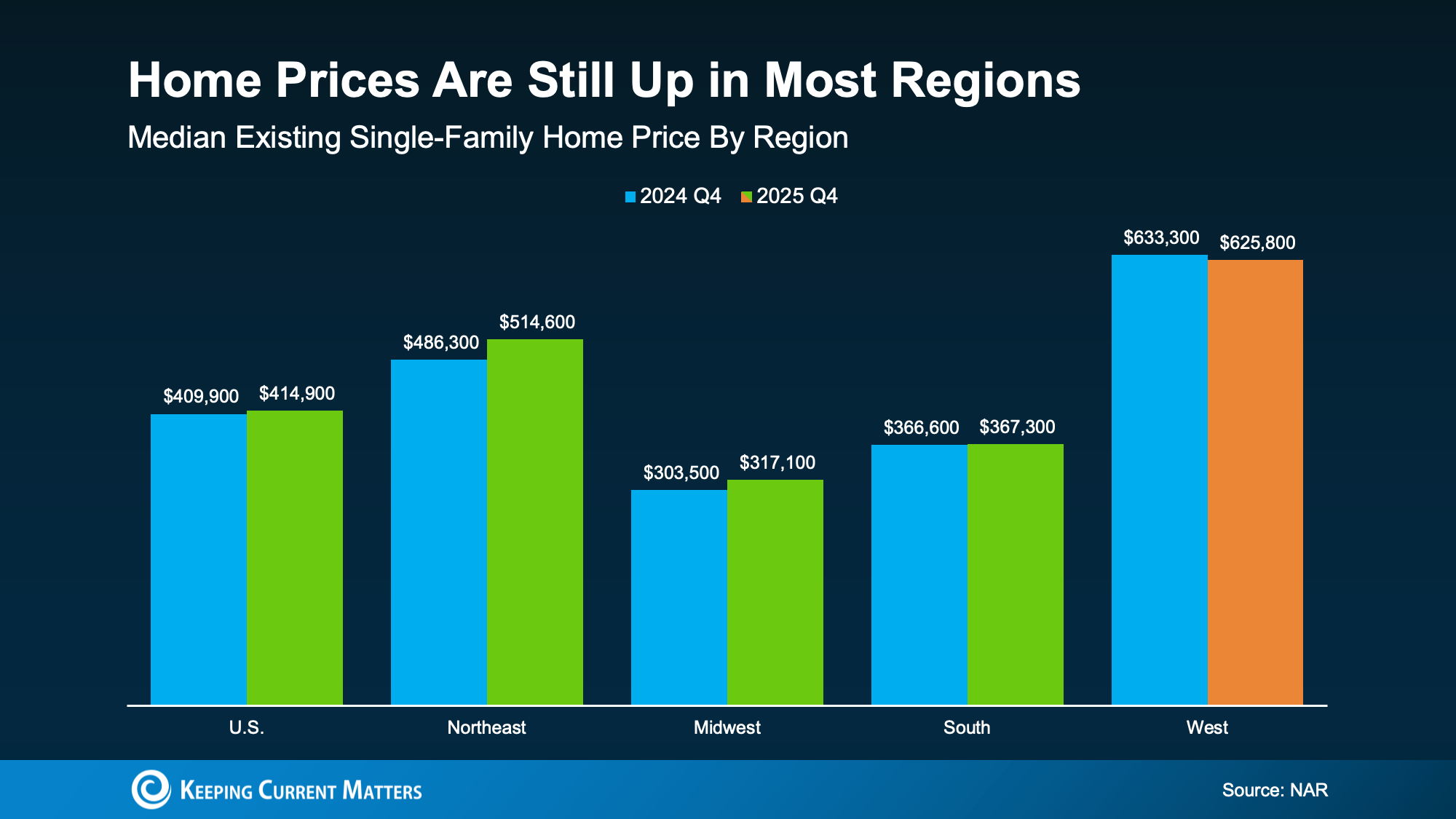

Home Prices Are Still Rising Nationally

A lot of online chatter focuses on isolated price drops without mentioning the broader data. Nationally, prices have continued to trend upward, but at a slower rate than usual.

According to a new report from the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s modest growth compared to the peak “boom” years, but it’s still growth. And regionally, the story varies.

At a glance, the numbers show:

- Northeast, Midwest, and South: prices generally up or steady.

- West: more mixed, with some markets seeing mild price declines.

In other words, the market is cooling and normalizing, not crashing.

Why You’re Hearing So Much About Price Drops

Price declines make for clickable headlines. But a few factors can make a local shift look like a national trend:

- High-profile metros go viral. A dip in one major market can dominate the conversation.

- Seasonality is real. Some months are softer than others, even in healthy markets.

- Affordability has cooled demand. Higher payments can reduce competition and push prices to level off.

Those are signs of a market adjusting, not collapsing.

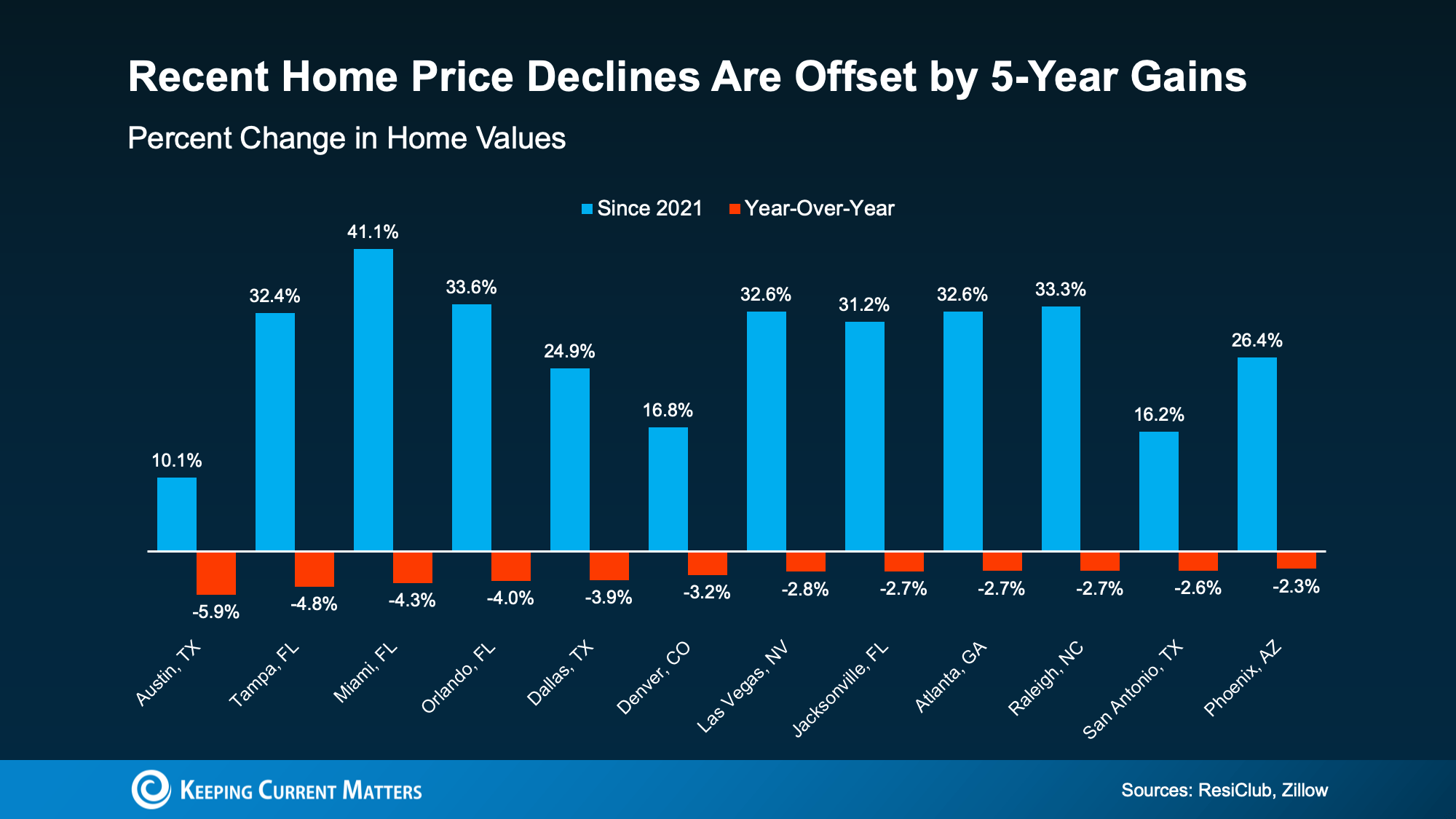

Some Markets Have Softened, But Context Matters

In the places where prices have dipped, it helps to look at the big picture. Many of those markets saw especially strong appreciation over the last several years. When you compare today’s values to where they were five years ago, homeowners in many “down” markets are still up significantly overall.

According to data from ResiClub and Zillow, price dips in the short-term aren’t always the cause for concern they seem to be. The long-term trends tell a clearer story, and they remain strong for many homeowners.

The key point: a pullback after rapid growth is not the same thing as a crash. It’s often a correction toward something more sustainable.

What This Means for Homeowners and Buyers

If you’re a homeowner:

In most markets, you’re not watching value evaporate overnight. Instead:

- You likely still have meaningful equity compared to pre-2020 values.

- Pricing strategy matters more now that buyers aren’t automatically overbidding.

- The best indicator is recent comparable sales in your neighborhood.

If you’re a buyer:

A cooler market can create more breathing room:

- You may see more negotiability in certain areas.

- You may have more time to decide than during the peak frenzy.

- But waiting for a big “crash” could mean missing the right home if your local market is stable.

Real estate is local. The best move depends on your budget, timeline, and the neighborhood you want.

How to Know What’s Happening Where You Live

National headlines can’t tell you what’s happening on your street. To get a clear picture, look at:

- Recent sold prices (comps) for similar homes.

- Days on market and list-to-sale price ratios.

- Inventory levels and new listings.

- Price reductions on comparable listings.

A local real estate agent can help make sense of your market’s unique trends. That way, you know you’re relying on sound information for any decision you make.

Conclusion

Home prices are rising or holding steady in most parts of the country, and a handful of small declines does not equal a nationwide downturn. If you want to know what your home is worth today, review your local numbers with a trusted real estate professional.

The Top Ten 2026 Housing Markets for Buyers and Sellers

Whether you’re buying or selling this year and need to know the top housing markets, you’re in luck. Here are two lists for the 2026 housing market, one for sellers and one for buyers. But before you scroll to the lists, keep this in mind:

If you’re planning a move for 2026, the most important takeaway is this: there are many housing markets to look at this year.

Experts agree 2026 is shaping up to be one of the most geographically split housing markets in years. Some areas are leaning toward sellers, while others are finally opening real doors for buyers. Who has the advantage depends almost entirely on where you live. Selma Hepp, Chief Economist at Cotality, explains it this way:

“Looking ahead to 2026, regional differences will remain pronounced, with demand favoring areas that offer both economic opportunity and relative affordability.”

To show just how divided the landscape is, here’s a look at where sellers may have the upper hand and where first-time buyers may find their opening.

Where Sellers Stand To Win Big in 2026

Zillow identified the following metros as some of the strongest seller markets for 2026, based on buyer demand, pricing momentum, and how quickly homes are expected to sell:

- Hartford, CT

- Buffalo, NY

- New York, NY

- Providence, RI

- San Jose, CA

- Philadelphia, PA

- Boston, MA

- Los Angeles, CA

- Richmond, VA

- Milwaukee, WI

In markets like these, buyers are likely to compete for limited inventory, which can give sellers more leverage.

What sellers can expect in these markets

If you’re a homeowner in a seller-friendly metro, you may see:

- Stronger buyer interest

- Shorter time on market

- Better odds of selling close to (or above) asking price

That doesn’t mean every listing is guaranteed to fly off the shelf. But it does mean sellers who price strategically, prep their home well, and follow a good agent’s guidance can be in a strong position in 2026.

Markets Where There’s More Opportunity for First-Time Buyers

On the other hand, some metros are giving buyers more breathing room, especially first-time buyers who have had the toughest time getting in lately. Realtor.com points to 10 top metros where first-time buyers are expected to enjoy advantages in 2026:

- Rochester, NY

- Harrisburg, PA

- Granite City, IL

- Birmingham, AL

- North Little Rock, AR

- Syracuse, NY

- Baltimore, MD

- St. Louis Park, MN

- Pittsburgh, PA

- Garfield Heights, OH

These housing markets are top contenders thanks to a mix of:

- More affordable home prices

- Better housing availability

- Strong local amenities and economic health

For first-time buyers, that combination matters. It’s often the difference between wishful thinking and a real path to homeownership.

What buyers can expect in these markets

In more buyer-friendly areas, first-time buyers may find:

- Less intense competition

- More room to negotiate

- A clearer path to getting an offer accepted

What Matters More Than Any Top 10 List

Not seeing your city on either list? Don’t worry. This is a snapshot at the national level, not a definitive statement on your local market. These lists simply show how different conditions can be from one metro area to the next.

And remember: you can buy or sell no matter which side your local market favors. All you need is the right strategy for your market’s unique conditions.

Here’s what that can look like:

- Sellers in a more buyer-friendly metro may need to price competitively and focus on strong prep (repairs, staging, and marketing).

- Buyers in a seller-leaning area may still need to come prepared with a clean, compelling offer and a smart plan for competing.

To find out where your market falls and what you should expect, a local expert can help you interpret the trends and build a game plan.

Conclusion

The housing market in 2026 isn’t one-size-fits-all. Local conditions matter more than ever, and knowing whether you’re in a buyer-friendly or seller-friendly area can shape everything from pricing to negotiations.

Whether you’re buying, selling, or just exploring your options, the right strategy (and the right agent) can put you in a strong position this year. If you’re a buyer or seller ready for the next step, search the top housing markets now, or reach out to us for help today.

Good News for Buyers: Home Affordability Improving in 2026

If you’ve felt priced out of the market or stuck waiting on the sidelines, there’s finally some encouraging news:

Buying a home is finally becoming more affordable.

Monthly payments have started to come down thanks lower interest rates, and buyers are starting to feel pricing pressures ease. That doesn’t mean homeownership is suddenly easy for everyone, but after a tough stretch, small improvements are meaningful.

Home Affordability Is Finally Improving

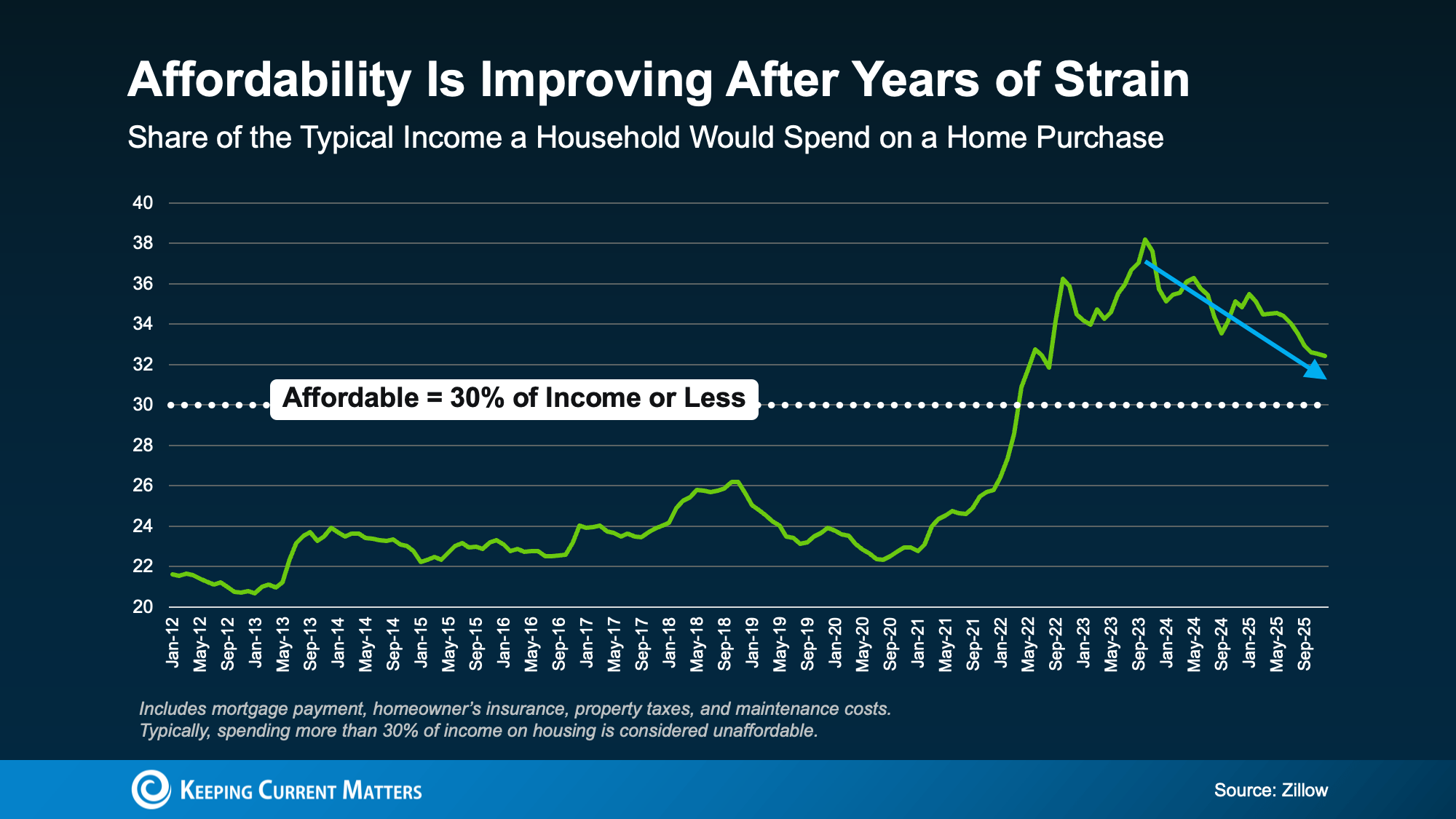

One of the clearest ways to track this change is to look at how much of a household’s income goes toward owning a home.

According to Zillow, housing is typically considered affordable when total housing costs take 30% or less of your monthly income. That includes your mortgage payment, property taxes, insurance, and basic maintenance.

For the past few years, many buyers were well above that mark, which pushed homeownership out of reach for a lot of households. But that’s starting to shift. Zillow research shows it’s taking less of a typical household’s income to buy a home than it did just a few years ago (see graph below):

We’re not all the way back to Zillow’s 30% threshold yet, so affordability is still tight in many markets. But the trend is improving, and that’s a big change from what buyers have been up against.

Why Homebuying Is Becoming More Affordable

Mortgage rates get most of the attention, and yes, rate movement plays a major role in monthly payment size. But it’s not the only reason affordability is improving. Three key trends are working in buyers’ favor right now:

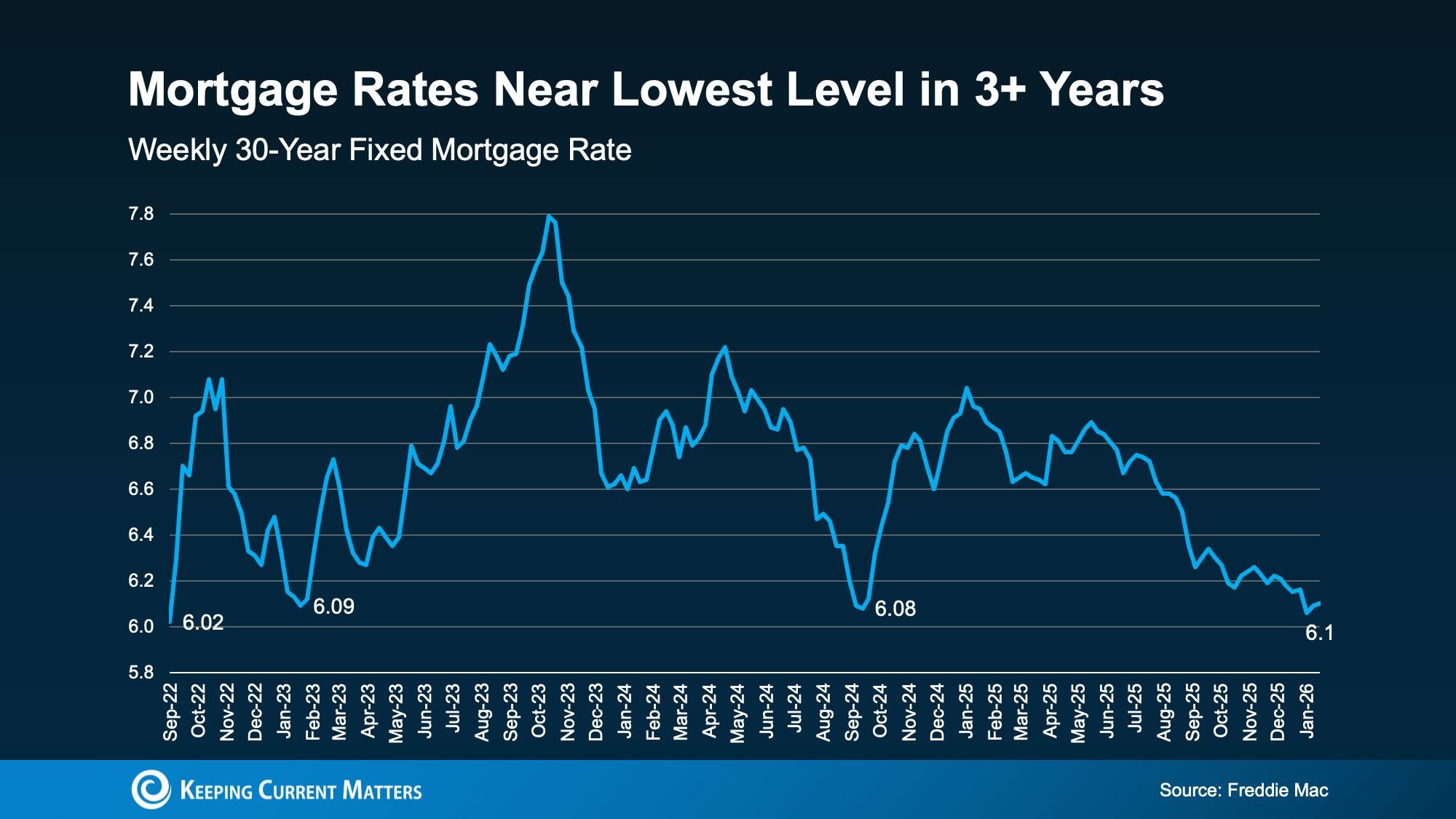

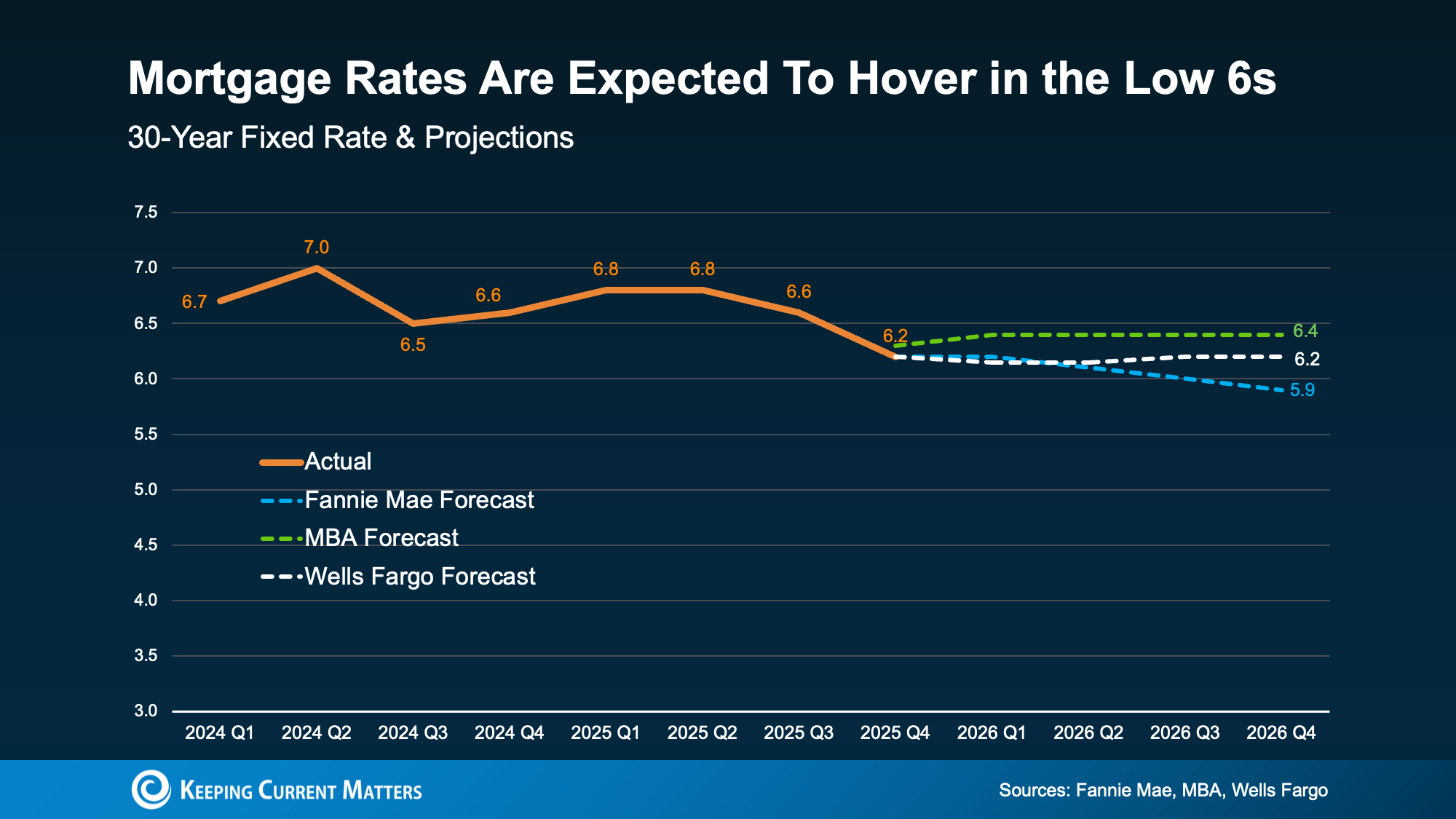

1) Mortgage rates have eased

Rates are near their lowest level in more than three years, which can reduce monthly payments and expand buying power (see graph below):

2) Home price growth has cooled

Home prices aren’t falling nationally, but they’re rising more slowly than they were a few years ago. That matters because slower price growth helps keep purchase prices from jumping as sharply, which can make payments feel more manageable and the overall buying process more predictable.

3) Wages are growing faster than home prices

This is a major factor that often gets overlooked. When incomes rise faster than home prices, buyers can start catching up. Mark Fleming, Chief Economist at First American, explains:

“When income growth exceeds house price growth, house-buying power improves—even if mortgage rates don’t decline meaningfully.”

None of this makes homes “cheap,” but it does help explain why the math is starting to work a bit better than it did even a year ago. In short, some of the forces that curbed affordability are finally easing. As Fleming again explains:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

Because of these combined shifts, many economists expect affordability to continue improving in 2026.

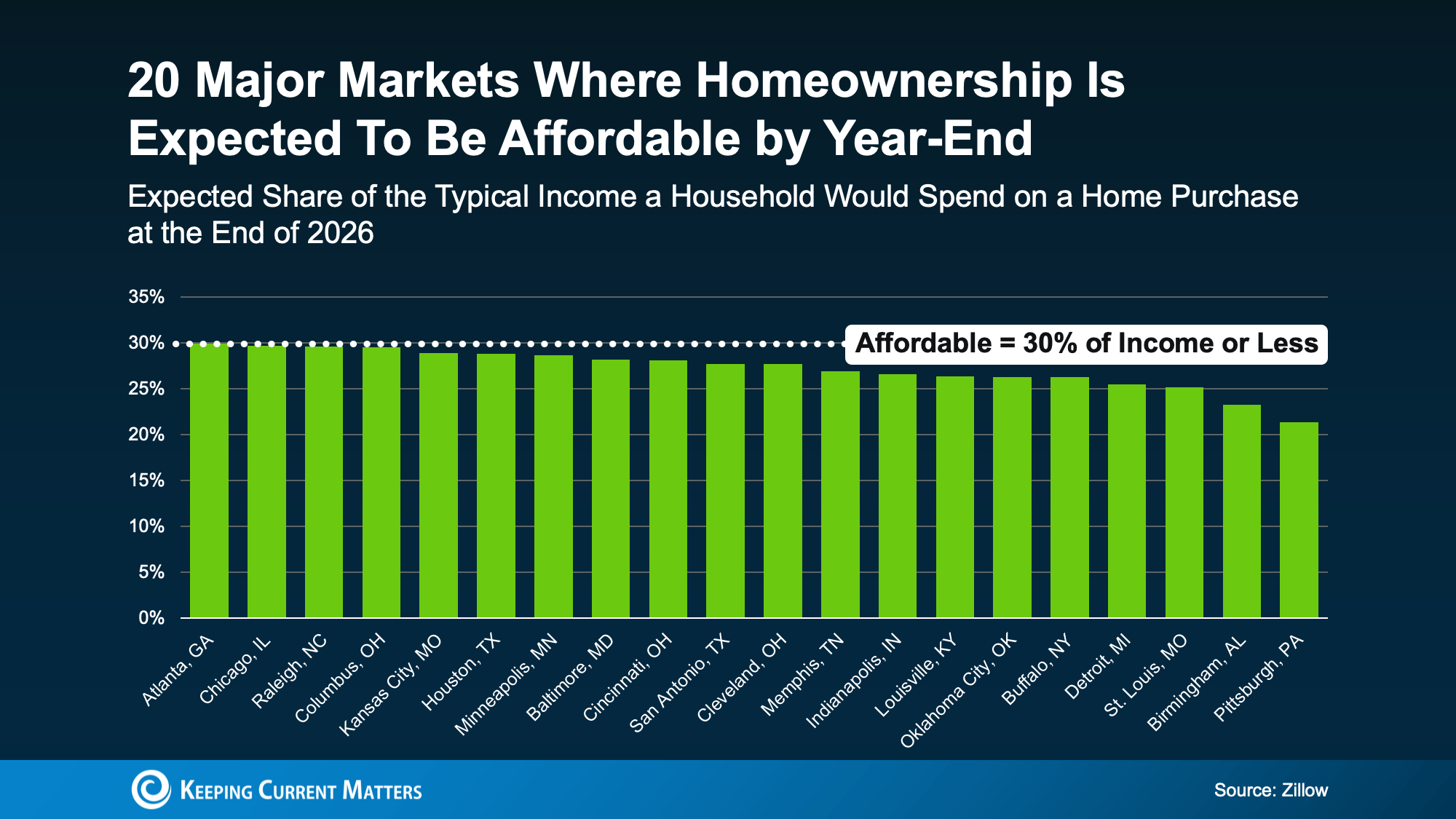

Where Are Homes Becoming Affordable First?

So how much will affordability improve, and where will it show up first? In some places, the difference could be noticeable. Zillow says some markets are expected to fall back under their affordability threshold (30% of income or less) by the end of the year (see graph below):

But you don’t have to live in one of those specific markets, and you may not have to wait until year-end to see improvement. Many areas are already trending in a better direction.

That’s why your next best step is local: talk to a real estate agent who understands what’s happening in your market. The national headlines don’t always reflect what’s going on neighborhood by neighborhood, and you might be closer to buying than you think.

Conclusion

For the first time in a while, home affordability is easing, and that’s an important shift for buyers.

And because the pace of improvement varies by location, understanding what’s changing locally can make all the difference. If you want to see how these trends are playing out where you live, connect with a local real estate agent to talk through your options.

Mortgage Rates Just Hit a 3-Year Low. Does It Matter in 2026?

If you’ve been watching mortgage rates and waiting for a “better time” to buy, here’s your chance. Rates just dipped below 6% for the first time in more than three years. Even modest rate movement can change what you can afford, how competitive you can be, and whether buying feels realistic again, especially if last year’s higher rates pushed you to the sidelines.

With rates finally easing up into 2026, here’s a fresh take on why lower mortgage rates are still a big deal, plus what to do next if you’re thinking about making a move.

Why Mortgage Rates Impact More Than Just Interest

A mortgage rate isn’t just a number on a lender’s website. It shapes the entire homebuying experience because it affects:

- Your monthly payment

- How much home you can qualify for

- Your comfort level with your budget

- How competitive your offer can be

When rates jump, affordability tightens fast. That’s why many buyers (especially first-time homebuyers) feel the pinch first. When rates ease, the reverse happens: budgets get a little more breathing room, and choices open up.

The “One-Point” Difference That Changes the Math

One of the easiest ways to understand why rate declines matter is to look at a simple example.

When rates are closer to 7%, monthly payments rise sharply. When rates move closer to 6% (or below), payments can drop meaningfully. On a typical loan amount, that can translate into hundreds of dollars per month in savings compared to the higher-rate environment.

That difference can help you:

-

Stretch your budget without stretching your lifestyle

-

Consider more homes in a neighborhood you actually want

-

Keep cash available for repairs, furnishing, or future goals

In practical terms, the change isn’t just “cheaper interest.” It can be the difference between compromising on your wish list and finding a home that fits.

What Lower Rates Can Unlock for Buyers

When borrowing costs come down, three things usually happen for homebuyers:

1) Lower monthly payments

A lower rate can reduce the monthly principal-and-interest payment, which helps many buyers feel more confident about moving forward.

2) More buying power

When the payment drops, you may qualify for more home at the same monthly budget. That can mean a better location, an extra bedroom, or a property that needs fewer updates.

3) Stronger offers without overextending

More budget flexibility can help you compete without taking on a payment that makes you uncomfortable. That matters in markets where inventory is still tight and desirable homes move quickly.

Why This Can Bring More Buyers Off the Sidelines

Rate changes don’t only affect you. They affect everyone who has been waiting, too.

Industry research suggests that when rates sit around certain thresholds, millions more households can afford a median-priced home. In fact, research from the National Association of Realtors (NAR) points to 5.5 million additional households being able to afford the median-priced home when rates are at 6% or below, and it estimates roughly 550,000 of those households could buy within the next 12 to 18 months.

That matters because it signals something important: pent-up demand can return quickly when affordability improves.

If you’re home-searching now (or preparing to), you may be able to act before competition fully ramps back up.

A Quick Reality Check: Rates Aren’t the Only Factor

Lower rates help, but they don’t magically make every home affordable. Your true monthly cost depends on several moving pieces, including:

-

Home price

-

Local inventory and competition

-

Property taxes

-

Homeowners insurance (which can vary widely by state and ZIP code)

-

HOA dues

-

Your down payment and credit profile

That’s why the smartest next step isn’t guessing. It’s running real numbers to figure out what “affordable” looks like for you.

What To Do Next If You’re Considering Buying

If you’ve been waiting for rates to improve, here’s a simple, practical plan:

-

Get pre-approved (not just pre-qualified).

Pre-approval gives you a clearer budget and shows sellers you’re serious. -

Calculate your comfortable payment range.

Decide what fits your life, not just what a lender says you can qualify for. -

Compare scenarios with your lender.

Ask for payment examples at different price points, down payments, and rate options. -

Watch inventory in your target neighborhoods.

The best “deal” is the home that works for your needs and your budget.

Conclusion

Mortgage rates easing from last year’s highs isn’t just an attractive headline. For many buyers, it can be the shift that turns “maybe someday” into “this could actually work.”

If you paused your search when rates were higher, it’s worth revisiting your numbers now. A quick conversation with a trusted lender can show what today’s rate environment means for your payment, your buying power, and your options.

If you’re thinking of buying, or need help finding a lender, reach out to us today. We can connect you with local agents and lenders to make your journey as simple as possible.

Expert Forecasts Point to Home Affordability Improving in 2026

If the last few years have felt like a constant tug-of-war between home prices, mortgage rates, and “Can we actually afford this?”, you’re not alone. Affordability has been the biggest obstacle for buyers (and a major source of hesitation for sellers), but the outlook for 2026 is more encouraging than what we’ve seen in a while.

In fact, affordability improved meaningfully in 2025, and many industry forecasts expect that progress to continue through 2026. The reason comes down to three forces shaping the market: mortgage rates, housing inventory, and home price growth.

1) Mortgage Rates: Lower Than the Peak, Likely Steadier in 2026

Mortgage rates have already eased from recent highs by nearly a full percentage point over the past year in some measures, and that matters more than most people realize. Even small rate shifts can change monthly payments, buying power, and which homes feel like realistic options.

What experts expect

Forecasts suggest rates may hover in the low 6% range through 2026, though the exact path depends on the broader economy, the job market, and Federal Reserve policy decisions. The key takeaway: rates are already lower than they were a year ago, which helps restore some breathing room for people planning a move in 2026.

What this means for buyers

- Lower rates can reduce monthly payments

- Improved buying power can make more listings qualify as “within reach”

- You may have more flexibility to negotiate when combined with rising inventory

What this means for sellers

- The market is adjusting to the idea that “rates in the 6s” may be the new normal

- If you need to move, it may be more feasible than it looks, especially if you’re sitting on substantial equity

Experts expect mortgage rates to hover in the low 6s or drop even lower as the economy changes in 2026.

2) Housing Inventory: More Homes for Sale, More Leverage for Buyers

One of the biggest changes in 2025 was inventory finally moving in the right direction. With more homes available, buyers got something they haven’t had in years: options—plus more time to compare those options and negotiate.

Inventory is still expected to grow

After a meaningful rise of about 15% in 2025, forecasts call for continued growth in the supply of homes for sale in 2026 (though likely at a slower pace than the last big jump). Realtor.com economists, for example, project additional gains of about 8.9% in active listings this year.

What this means for buyers

- More choices (and fewer “take it or leave it” situations)

- Greater negotiating power—especially on homes that are priced too aggressively or need updates

What this means for sellers

- Pricing strategy becomes critical. In a market with more options, buyers compare everything.

- Strong presentation (clean, staged, repaired) matters more when competition increases

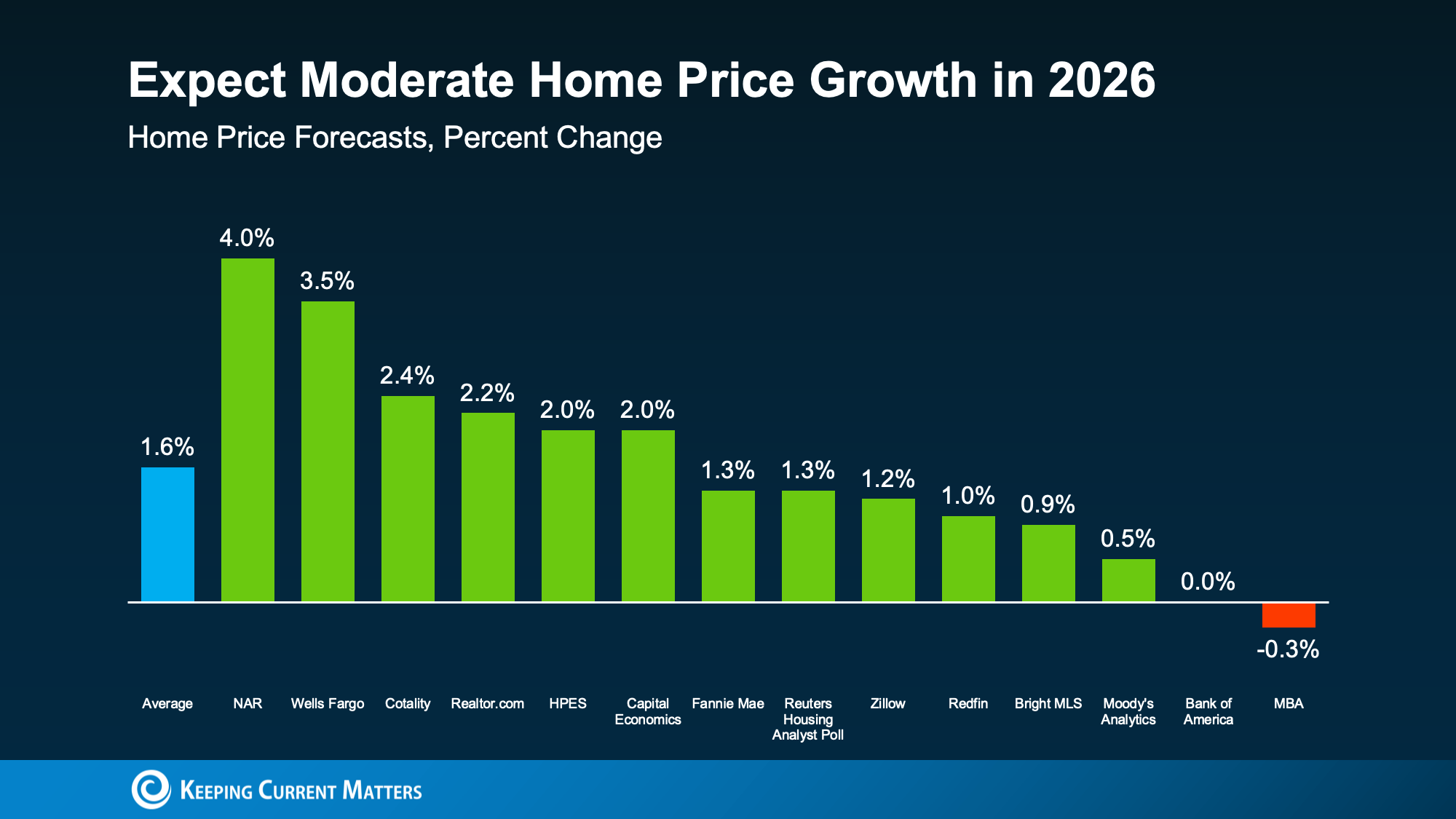

3) Home Prices: Still Rising Nationally, But at a More Sustainable Pace

Here’s what many headlines miss: increasing inventory tends to reduce upward pressure on prices, but it doesn’t automatically mean prices crash. Most national forecasts expect home prices to keep rising in 2026, just more slowly than the rapid spikes of the recent past. On average, experts predict home price growth of about 1.6% in 2026.

Why slower growth can be good news

More moderate appreciation helps buyers plan and budget with fewer surprises, while still supporting overall market stability.

But location is everything. Some areas may outperform the national average, while others could see flat or slightly declining prices depending on local supply, demand, and employment conditions. If you’re serious about a move, a local real estate agent can help you interpret what’s happening in your neighborhood, not just what’s happening nationally.

Home prices are expected to continue rising in 2026, though at a more moderate rate.

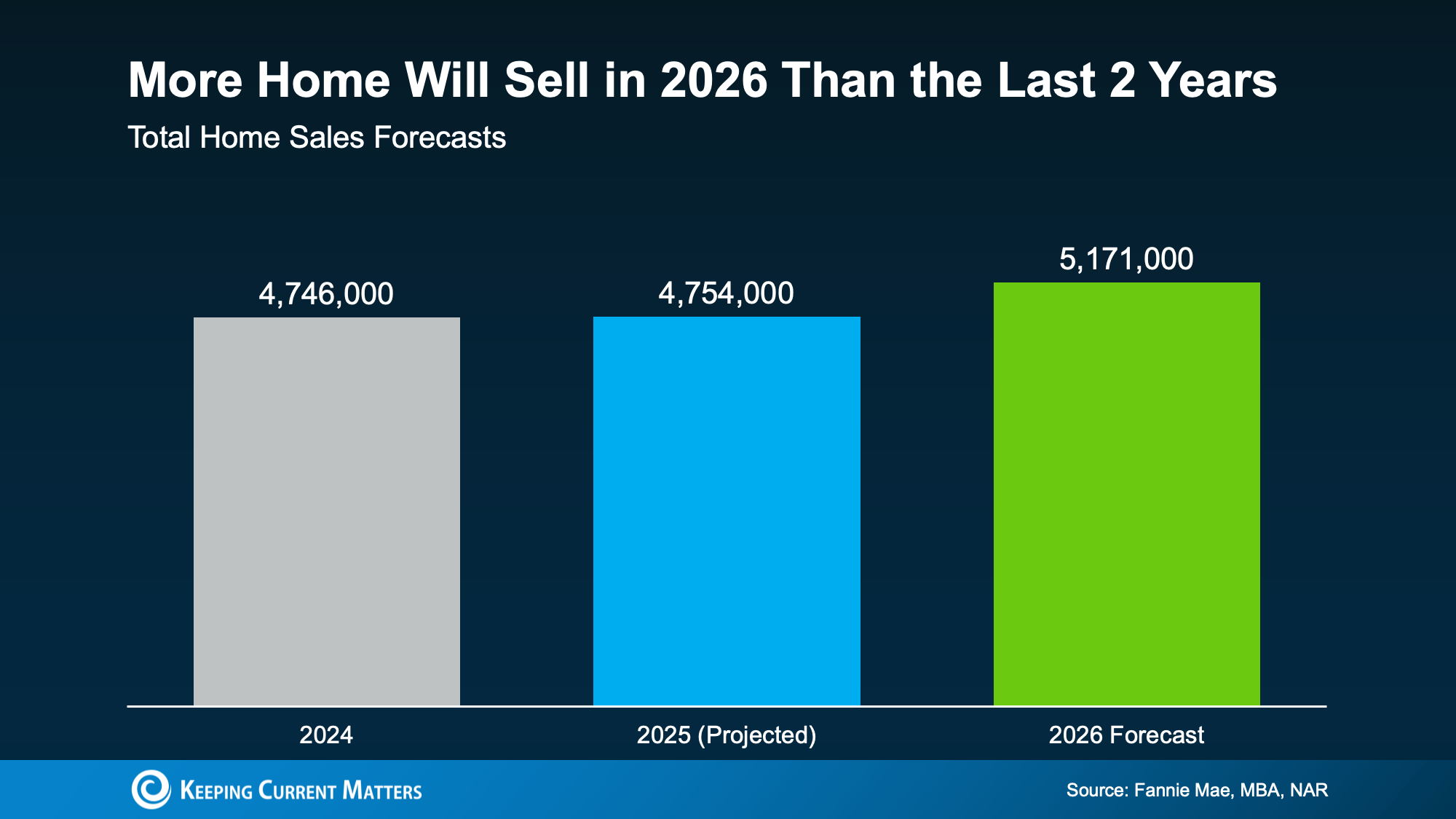

Will More Homes Sell in 2026?

When rates are lower than recent peaks, inventory is improving, and price growth is calmer, you get a healthier affordability equation. That’s why many experts expect more home sales in 2026, as both buyers and sellers find conditions easier to navigate.

As Zillow’s Chief Economist Mischa Fisher notes:

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

Increased affordability in 2026 has experts predicting higher home sales over the past two years.

2026 Could Feel More Balanced Than You’ve Seen in Years

Affordability won’t change overnight. But if current forecasts hold, 2026 is shaping up to be a year with:

- More balance between buyers and sellers

- More predictability in pricing

- More flexibility in negotiations

- More opportunity for people who’ve been waiting on the sidelines

If you’re thinking about buying or selling in 2026, the smartest next step is to get hyper-local: understand neighborhood pricing trends, inventory levels, and what buyers are actually paying (and negotiating) right now.

Ready to start but aren’t sure how? Reach out to us today to connect with an expert agent for all the latest info on your local market.

CENTURY 21 Affiliated Expands Northern Indiana Footprint With New Granger Office

Granger, IN — December 9, 2025 — CENTURY 21 Affiliated, the No. 1 CENTURY 21 franchise in the world, today announced the opening of its newest office, located at 6910 North Main Street, Building 2, Granger, IN 46530. This expansion underscores the company’s commitment to delivering elevated client service, strengthening community partnerships, and supporting continued growth across Northern Indiana.

The new office will be led by Team Leader Kyle Zelmer, a seasoned real estate professional who also manages the Niles, MI office.

“We’re thrilled to be back in Indiana, and even more excited to be in the Granger community,” said Jasen Schrock, President of CENTURY 21 Affiliated. “This office positions our agents to meet rising demand across the region while giving clients an accessible space to collaborate on their real estate goals. Our commitment remains the same: exceptional service, strong relationships, and results that move people forward.”

“Granger is an important and growing market for us,” said Dan Kruse, CEO of CENTURY 21 Affiliated. “We’re confident this office will serve as a catalyst for regional growth and a hub for top-tier real estate talent.”

About CENTURY 21 Affiliated

CENTURY 21 Affiliated is a member of multiple listings services in California, Illinois, Indiana, Michigan, Minnesota, and Wisconsin, with over 1,400+ sales professionals and 60+ offices. CENTURY 21 Affiliated also specializes in worldwide relocation. At CENTURY 21 Affiliated, the customer comes first. The complete commitment to this philosophy has made CENTURY 21 Affiliated such a powerful force in the real estate industry. CENTURY 21 Affiliated has been ranked the No. 1 CENTURY 21® franchise worldwide for eleven years in a row. Visit C2Affiliated.com to learn more.

###

CENTURY 21 Affiliated Announces Strategic Partnership with CMG Financial and Welcomes Greg Harkleroad as Joint Venture Division Sales Manager

Madison, WI – June 26, 2025 – CENTURY 21 Affiliated is proud to announce a new strategic partnership with CMG Financial, a top five privately held mortgage lender in the U.S., and the appointment of Greg Harkleroad (NMLS ID# 427611) as the Joint Venture Division Sales Manager to lead this exciting collaboration.

This partnership represents our continued commitment to delivering a seamless and exceptional home-buying experience for our clients across the Midwest and West Coast. With CMG’s innovative lending platform and long-standing reputation for excellence, combined with CENTURY 21 Affiliated’s position as a leading real estate franchise, we are poised to provide unmatched service and support to our buyers and agents.

“We are thrilled to announce our relationship with CMG Financial,” said Dan Kruse, CEO of CENTURY 21 Affiliated. “After extensively researching mortgage partners, we found CMG to be best-in-class when it comes to technology, customer experience, and agent support. By aligning with a lender of their caliber, we are confident this partnership will significantly elevate the home-buying journey for our clients.”

At the helm of this new joint venture is Greg Harkleroad, who brings nearly 40 years of mortgage experience and a proven track record of leadership, team building, and business growth. His passion for helping individuals achieve homeownership and his commitment to Realtor collaboration make him the ideal leader for this initiative.

“Greg brings decades of mortgage expertise to the venture,” said Sam Bell, President of Brokerage, CENTURY 21 Affiliated. “He has built numerous winning teams and is dedicated to supporting our agents and buyers at every step of the home financing process. We are excited to have him onboard.”

Greg’s approach to leadership centers around strategic hiring, coaching, and fostering strong relationships with real estate professionals to ensure a purchase-focused, service-driven mortgage experience.

“A strong Realtor-lender partnership is the foundation for delivering exceptional service,” said Harkleroad. “I’m excited to collaborate with CENTURY 21 Affiliated to bring that vision to life.”

With this partnership, CENTURY 21 Affiliated continues to prioritize innovation, support, and growth across its markets in Wisconsin, Michigan, and Southern California, offering agents and clients access to an experienced lending team, in-house technology, and personalized mortgage solutions.

For more information, please contact Greg Harkleroad at gregh@cmgfi.com or (513) 617-4407.

About CMG Financial

CMG Financial is a well-capitalized mortgage lender founded in 1993 by Christopher M. George, a former Mortgage Bankers Association Chairman. CMG makes its products and services available to the market through three distinct origination channels: retail lending, wholesale lending, and correspondent lending. CMG also operates eight joint venture companies with builder & realtor partners, holds an impressive MSR/servicing portfolio, and serves the capital markets of fixed income trading & sales through CMG Securities. CMG currently operates in all states, including District of Columbia, and holds approvals with FNMA, FHLMC, and GNMA. The company is consistently recognized as a top-producing lender and top mortgage employer, and it prides itself on helping clients achieve the dream of homeownership through product innovation and streamlined servicing.

About CENTURY 21 Affiliated Real Estate LLC

CENTURY 21 Affiliated is a member of multiple listings services in California, Illinois, Michigan, Minnesota, and Wisconsin with over 1,400 sales professionals and 60+ offices. CENTURY 21 Affiliated also specializes in worldwide relocation. At CENTURY 21 Affiliated, the customer comes first. The complete commitment to this philosophy is what has made CENTURY 21 Affiliated such a powerful force in the real estate industry. CENTURY 21 Affiliated has been ranked the number one CENTURY 21® franchise in the world for eleven years in a row. Visit C21Affiliated.com to learn more.

###

America’s Richest Self-Made Woman, Billionaire Diane Hendricks, and Daughter Konya Hendricks Schuh Take on Hometown Revitalization in New Daytime Docuseries

“BETTING ON BELOIT”

New Home Renovation and Design Series Premieres July 12 at 1 pm ET/PT on A&E, Part of the Network’s Lifestyle Daytime Programming Block

Trailer HERE

NOTE: Konya Hendricks Schuh and Connor Fox are licensed real estate agents with CENTURY 21 Affiliated.

LOS ANGELES – (June 11, 2025) – America’s richest self-made woman, Diane Hendricks (#1 on the Forbes “Richest Self-Made Women” list the last eight consecutive years) is betting big on the town integral to her family’s success. The series chronicles the billionaire entrepreneur and her driven, accomplished daughter Konya Hendricks Schuh’s mission to revitalize Beloit, Wisconsin – once ranked as the state’s “worst city to live in” by USA Today.

Premiering Saturday, July 12, with back-to-back episodes at 1pm and 1:30pm ET/PT on A&E, Betting on Beloit airs as part of the network’s lifestyle daytime programming block. Episodes will also be available the next day on A&E’s website and on-demand.

Rising from humble beginnings to owning the largest wholesale construction supplier in the nation, Diane settled in the area in the 1970s and became a titan of industry – and one of Beloit’s biggest employers – helping build up the region as an industrial epicenter where thousands flocked to achieve the American dream. While Diane’s headquarters remained local, the 1990s saw too many industrial employers move overseas, forcing many residents of Beloit to find opportunity elsewhere. Determined to restore Beloit to its former glory, Diane has spent the last several decades working to improve the city through major economic development efforts. In addition to building a new stadium and school, hotels and multiple restaurants, Diane revitalized the entire industrial riverfront, finding new uses for the once-abandoned factory buildings.

Now, Diane has tasked Konya, a sharp real estate broker with a passion for design and a deep connection to the city, with leading the next phase of the revitalization effort.

Betting on Beloit follows Konya and her dynamic team – which includes her husband Matt (a plumbing contractor and former home builder), good friend and project manager Pete, and her realtor nephew Connor, as well as local artisans and designer friends Kristin and Mitch – as they purchase, restore and reimagine historic homes throughout Beloit’s storied neighborhoods.

With her mother financing this ambitious venture, the stakes are high for Konya and her team as they try to achieve their collective mission: to turn once-neglected properties into vibrant dream homes for individuals and families ready to plant new roots in Beloit. With grit, heart and a whole lot of Midwest spirit, they’re not just flipping houses—they’re rebuilding their community, one home at a time.

Tune in to all 12 episodes to get an inside look at the vision, challenges and triumphs of a bold revitalization journey that proves the American dream is still alive – and rooted in places you might not expect.

Betting on Beloit is produced by Wheelhouse’s Butternut, with Courtney White, Konya Hendricks Schuh, Rachel Sobel, Russ Friedman, Will Nothacker, Frank Carlisi and Tim Grady serving as executive producers.

About A&E

A&E leads the cultural conversation through high-quality, original programming that captivates viewers and brings them to the heart of the stories that matter. Through its distinctive brand of award-winning non-fiction and documentary programming, A&E always makes entertainment an art. For more press information and photography, please visit press.aegm.com. A&E is a division of A+E Global Media (aegm.com), a joint venture of the Disney-ABC Television Group and Hearst Corporation.

About Butternut

Lifestyle production company Butternut is run by lauded producer and executive Courtney White, formerly president of Food Network and general manager of HGTV. A joint venture with Wheelhouse launched in 2022, Butternut creates original food, home and other lifestyle content for all platforms, working with a range of established, emerging and home-grown talent. The company’s current slate includes Next Baking Master: Paris (Food Network); Giada In My Kitchen (Prime Video); Cookie, Cupcake, Cake (Hulu/A&E); Last Bite Hotel (Food Network); Divided by Design (HGTV) and Celebrity Family Food Battle(Roku), executive produced and starring Sofia Vergara, plus other series on deck for launch later this year.

About Konya Hendricks Schuh

With more than two decades of experience in real estate development, sales and construction, Konya Hendricks Schuh brings a deep understanding of the industry and a long-standing commitment to community revitalization. The daughter of Diane Hendricks – co-founder of ABC Supply and one of America’s most influential business leaders – Konya has long been immersed in the business of building, transforming and investing in communities. Sharing in her parents’ devotion to Beloit, Konya has played a key role in numerous projects that have contributed to the city’s ongoing growth and renewal.

As a real estate broker, she specializes in residential and new construction properties, helping clients navigate the market with a designer’s eye and a developer’s mindset. For each project, Konya runs point on all decisions, big and small, and leads the design process with a focus on honoring each home’s history and style while elevating spaces with modern touches.

Konya serves as the secretary and treasurer of the Hendricks Family Foundation, where she helps guide philanthropic initiatives focused on education, workforce development and economic opportunity. She is also the new chairman of the board for Grey Collar Enterprises, which is the parent company of Hendricks Commercial Properties and Geronimo Hospitality Group. In addition to her professional achievements, Konya is a proud mother, wife and devoted advocate for animal welfare.

About CENTURY 21 Affiliated Real Estate LLC

CENTURY 21 Affiliated is a member of multiple listings services in California, Illinois, Michigan, Minnesota, and Wisconsin with over 1,400 sales professionals and 60+ offices. CENTURY 21 Affiliated also specializes in worldwide relocation. At CENTURY 21 Affiliated, the customer comes first. The complete commitment to this philosophy is what has made CENTURY 21 Affiliated such a powerful force in the real estate industry. CENTURY 21 Affiliated has been ranked the number one CENTURY 21® franchise in the world for eleven years in a row. Visit C21Affiliated.com to learn more.

###

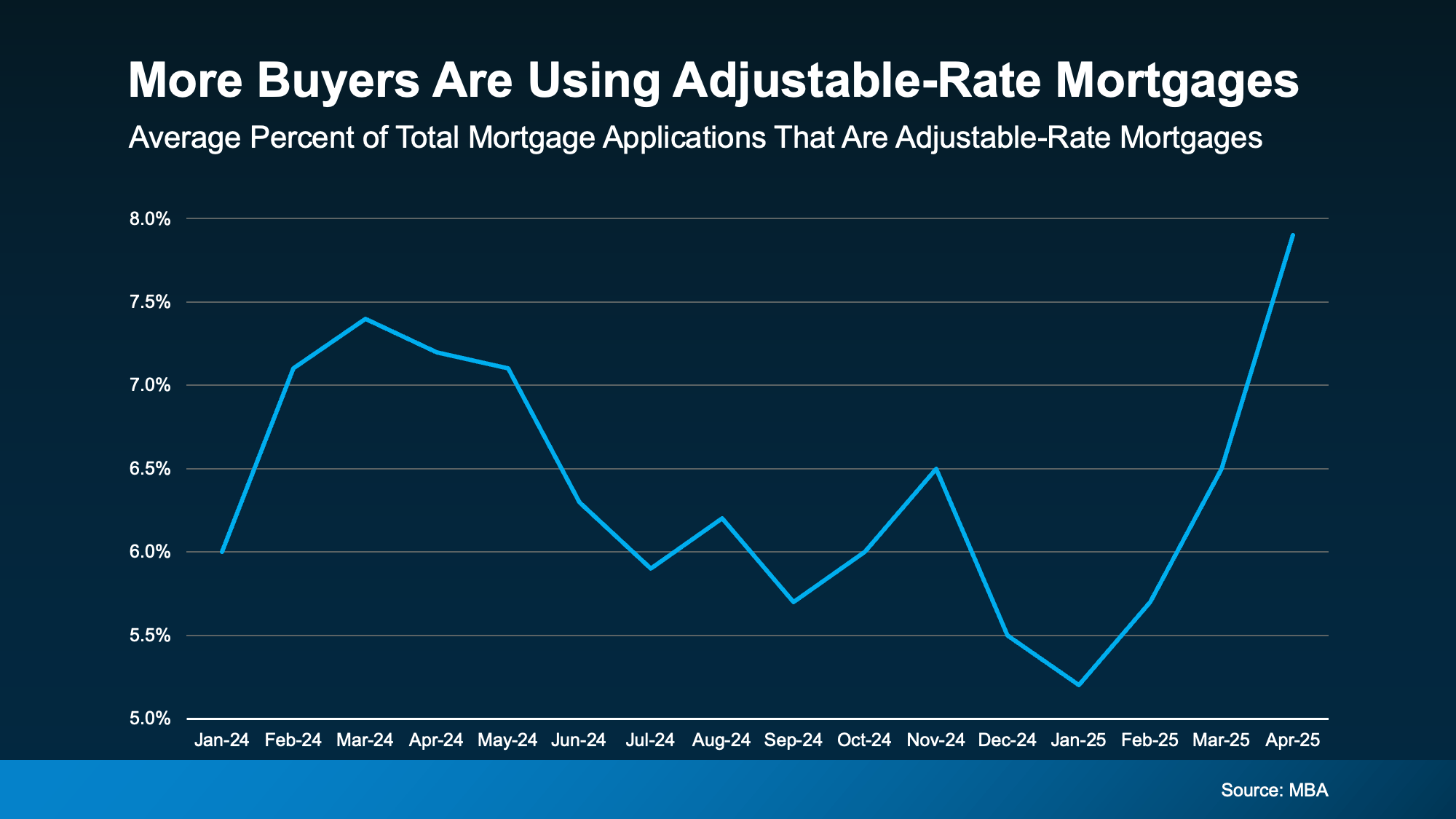

Adjustable-Rate Mortgages on the Rise: Should You Jump In?

If you’re in the market for a house, you’re probably not encouraged by today’s mortgage rates. Elevated rates and rising home prices have many homebuyers starting to explore other financing options that make more sense. One type of loan gaining popularity is adjustable-rate mortgages (ARMs).

If you remember the 2008 market crash, you may be wary of new types of loans. It’s wise to be cautious, but there’s no need to worry. Today’s ARMs much safer and stricter than the ones you may remember from 2008.

During that time, some buyers held loans they couldn’t afford once their rate adjusted. Today, lenders are more careful, and determine whether you can afford an increased rate before the loan is ever offered. This time, ARMs are returning thanks to creative buyers looking for affordable ways to buy a home..

According to recent data from the Mortgage Bankers Association (MBA), more buyers are using ARMs to buy this year.

How Does an Adjustable-Rate Mortgage Work?

If you’ve never heard of ARMs before, you may be wondering what they are, and if they’re right for you. Here’s how Business Insider explains the main difference between a traditional fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Taxes or homeowner’s insurance can still influence a fixed-rate loan, but your baseline mortgage payment typically changes very little. Meanwhile, adjustable-rate mortgages can potentially change drastically in either direction after your initial payment period ends. Depending on your situation and anticipated market trends, this could either work for you, or be far too risky.

Pros and Cons of Adjustable-Rate Mortgages

With ARMs on the rise in 2025, it’s clear that more buyers are finding them appealing. Under the right conditions, they may offer attractive upsides, like a lower initial rate. According to Business Insider again:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

Remember that if you have an ARM, your rate will change over time. As Barron’s explains, they can potentially cost you more in the long run:

“Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up.”

While the upfront savings can be helpful now, consider what could happen if your initial rate ends before you move. Even though rates are projected to ease a bit over the next couple years, nothing is ever guaranteed. Before you choose an ARM, talk with your lender and financial advisor about all your options, and the potential risks.

Conclusion

For certain buyers, adjustable-rate mortgages can offer some big advantages, but this won’t be true for everyone. Understand how they work and whether their pros and cons make sense for you financially. Always talk to a trusted lender and a financial advisor before making entering into a new mortgage.

Need help connecting with a trustworthy lender in your area? Reach out to us for help today.

How Could a Recession in 2025 Affect the Housing Market?

As talk about economic slowdowns runs wild, worries about a potential recession in 2025 are on the rise. Naturally, many homeowners are wondering what a recession could do to the value of their home, and their buying power.

Using historical data from recessions of decades past, let’s see how a recession might affect the housing market in 2025.

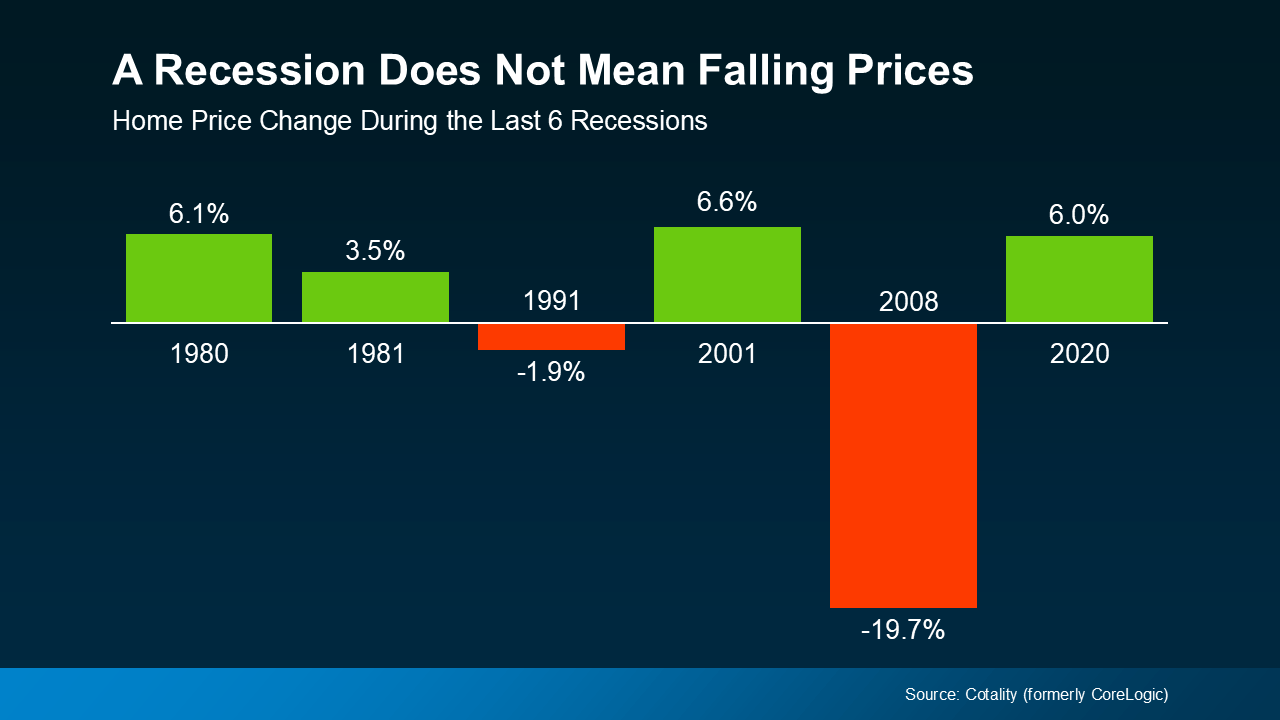

A Recession Won’t Lower Home Prices

It’s a common misconception that a recession will cause home prices to crash, like they did in 2008. In reality, 2008 was the only time the housing market saw such an extreme, dramatic drop in prices. Overflowing home inventory caused that price crash, and conversely, low inventory has prevented a similar crash in the years since.

Even in markets where housing inventory is up, it’s still far below the listing oversupply that caused the 2008 crash. Indeed, according to data from Cotality, home prices actually increased during four of the last six major recessions.

As the graph shows, a recession doesn’t necessarily mean that home prices will crash, or even drop. In reality, historical data shows that home prices usually continue along their current trajectory when a recession hits. And at the moment, home prices are still rising nationally, but at a more normalized rate. So, as the market stands now, a recession in 2025 would most likely drive prices even higher.

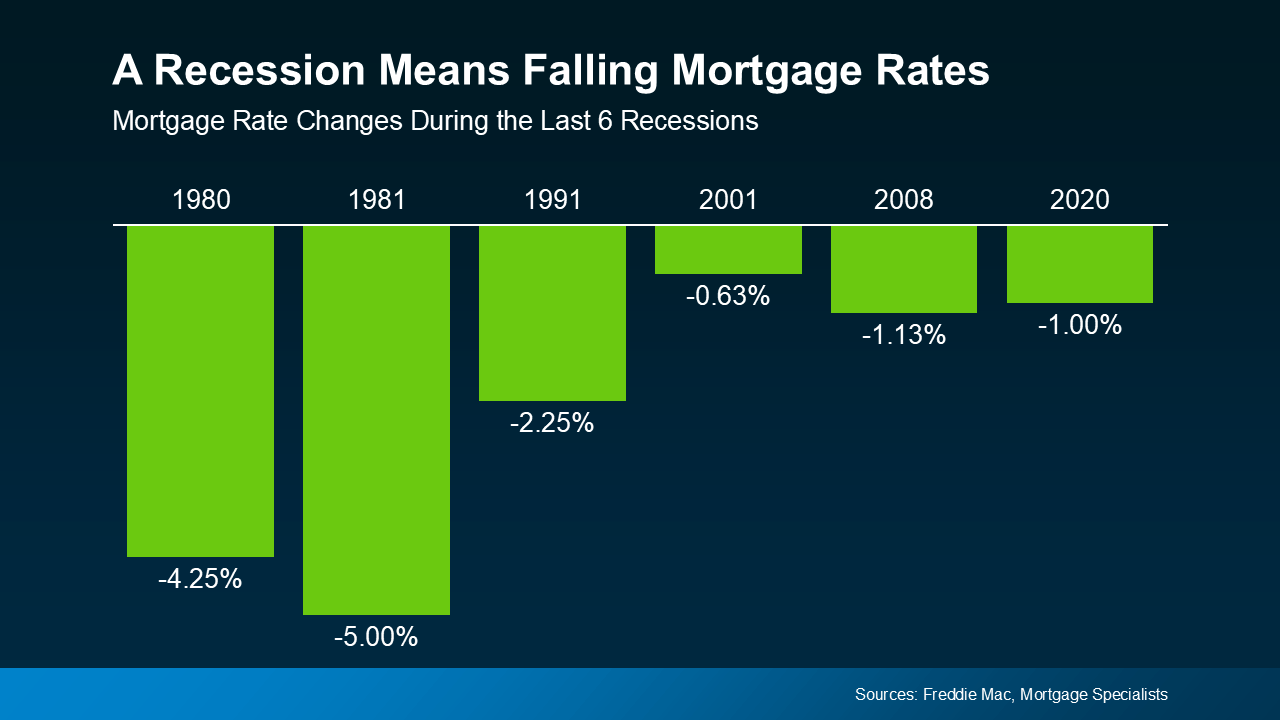

Mortgage Rates Typically Decline During Recessions

Home prices may stay their path during economic slowdowns, but mortgage rates actually tend to drop. Looking again at historical data from the last six recessions, this time from Freddie Mac, mortgage rates fell each time.

Historically speaking, a recession could mean that mortgage rates may even decline this year. However, the last time a recession dramatically lowered mortgage rates was over three decades ago in 1991. So with that said, even if a recession does happen, don’t expect a game-changing drop in mortgage rates.

Conclusion

Nobody ever truly knows what the economy will do, but the odds of a recession in 2025 have increased. Still, a recession doesn’t mean you need to worry about the housing market or the value of your home. The historical data tells us that a recession may even drive home prices higher and mortgage rates lower.

Wondering how an economic slowdown could impact your local market? Connect with us to get the info you need to plan ahead.