Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Housing Affordability Today: What Buyers Should Know

Let’s talk honestly about housing affordability today.

If you’ve been thinking about buying a home, selling your current home, or making a move, you’ve probably seen plenty of headlines about mortgage rates, home prices, inflation, and affordability. Some of those headlines are helpful. Others leave out critical information.

The truth is, affordability is not shaped by one factor alone. Mortgage rates matter, but they’re not the only piece of the puzzle. Wages, home prices, inventory, buyer competition, and your personal financial situation all play a role.

Here’s a clearer look at what’s happening right now: the good, the challenging, and what it could mean for your next move.

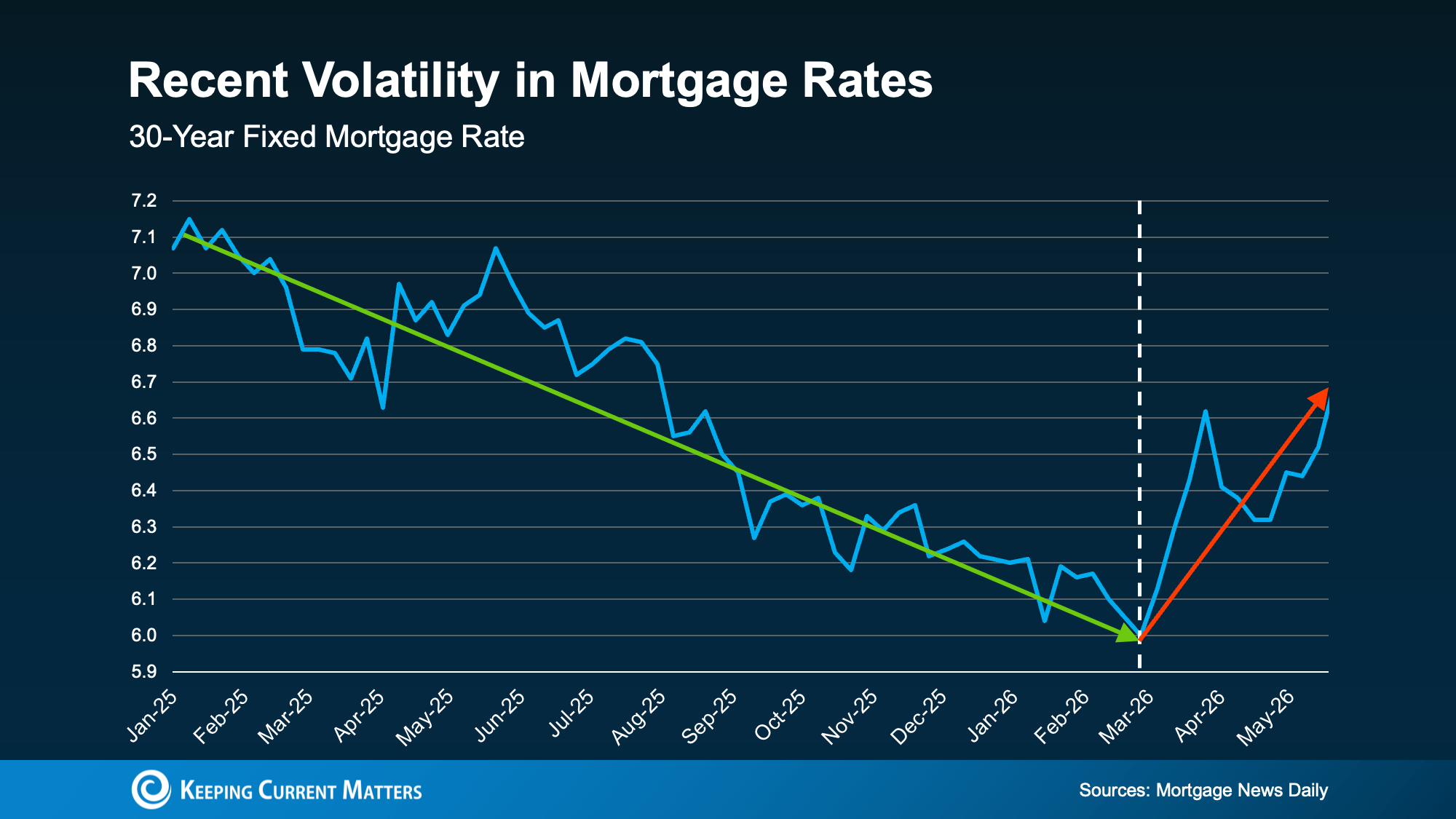

Mortgage Rates Have Been Rising

After a year or more of mortgage rates trending down, they’ve started climbing again. And for buyers, that’s incredibly frustrating.

So, why are rates moving higher?

A big reason is uncertainty. Mortgage rates are heavily influenced by broader economic conditions, and uncertainty often puts upward pressure on rates.

Ongoing global uncertainty, continued tensions in the Middle East, and inflation that has not fully cooled off are all having an impact. Colin Robertson, Founder of The Truth About Mortgage, explained it this way:

“You can’t have $100 a barrel oil and not expect inflation to rise, which translates to higher bond yields and mortgage rates.”

That matters because higher bond yields often lead to higher mortgage rates. And when mortgage rates rise, monthly payments can become more difficult for buyers to manage. Recent data from Mortgage News Daily illustrates the effect this has:

Should Buyers Wait for Mortgage Rates To Fall?

With unpredictable rates, it’s natural to wonder if waiting is the safer move.

If rates are higher now, will they come back down once uncertainty eases? Possibly. But there’s no guaranteed timeline.

Rates aren’t likely to drop until inflation cools further and global uncertainty improves. Even then, many experts believe rates may not drop dramatically. They may return to somewhere in the low- to mid-6% range we were seeing earlier this year.

That means waiting for a major rate drop could keep buyers on the sidelines longer than expected.

For many buyers, the question isn’t, “Will rates fall?”, but:

Can I afford the home and monthly payment based on today’s numbers?

If the answer is yes, and you find a home that fits your needs and budget, buying may still be worth considering. No one can predict exactly when rates will fall, how far they’ll fall, or what home prices and competition will look like when they do.

Wages Are Outpacing Home Prices

On the bright side, there’s also some encouraging news that doesn’t always make the headlines.

While inflation has made many parts of everyday life more expensive, recent data from the Federal Reserve Bank of Atlanta and Redfin show wages have been growing faster than home prices.

According to the data:

- Wages have recently been increasing around 4% year-over-year.

- Home price growth has been closer to 2% year-over-year.

That difference matters for home affordability.

When wages rise faster than home prices, buyers may slowly regain some purchasing power. It doesn’t solve the affordability challenge overnight, but it can help make a home purchase more manageable over time.

For buyers, every little bit of financial breathing room helps.

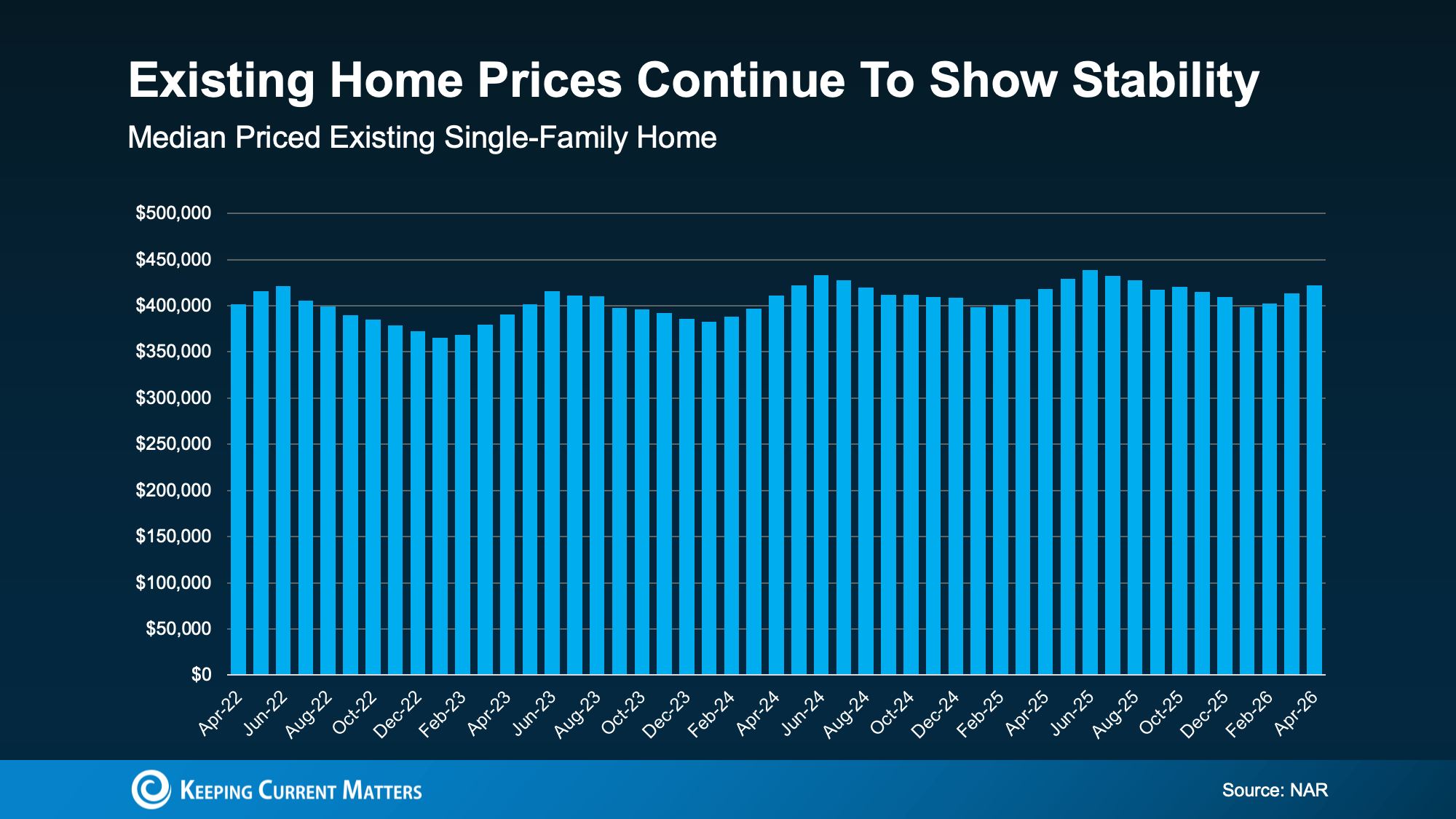

Existing Home Prices Have Held Steady

Another important part of the affordability picture is home prices.

National Association of Realtors data from the past four years show existing home prices have remained relatively steady. There hasn’t been a dramatic runup, but there hasn’t been a crash either. Instead, the market has seen more stability and slower growth.

Price stability like this can give buyers a real helping hand.

Part of what’s keeping prices steadier is that buyers now have more choices than they did in the most competitive parts of the market. More inventory can create:

- Less intense competition

- More time to make decisions

- Better opportunities to compare homes

- More room for negotiation in some situations

Of course, this doesn’t mean every market is a buyer’s paradise. Local conditions always matter. But, having more options can help buyers find a home that better fits their lifestyle and budget.

What Housing Affordability Means for Your Move

Today’s housing market is not simple. Mortgage rates are higher than many buyers hoped they would be, and global uncertainty is keeping rates from settling down quickly.

But the full affordability picture is more balanced than the headlines may suggest.

Rates are still a challenge, but wages are growing faster than home prices, and existing home prices have stayed relatively steady. Buyers today might have more options to make stronger decisions than they did when the market was tighter and more competitive.

As always, the right move depends on your budget, goals, timeline, and local market.

Before deciding whether to buy now or wait, it’s worth running the numbers with today’s information. Not with guesses from last year, last month, or national headlines.

Bottom Line

Housing affordability today is about more than just mortgage rates.

Rates are still a major factor, but wages, home prices, inventory, and local market conditions all matter too. If you can afford the monthly payment and find a home that fit your needs, you may not have to wait for the “perfect” option.

Want to figure out the best move for your situation? Connect with a local real estate professional to review current homes, pricing, and your area’s unique market conditions.

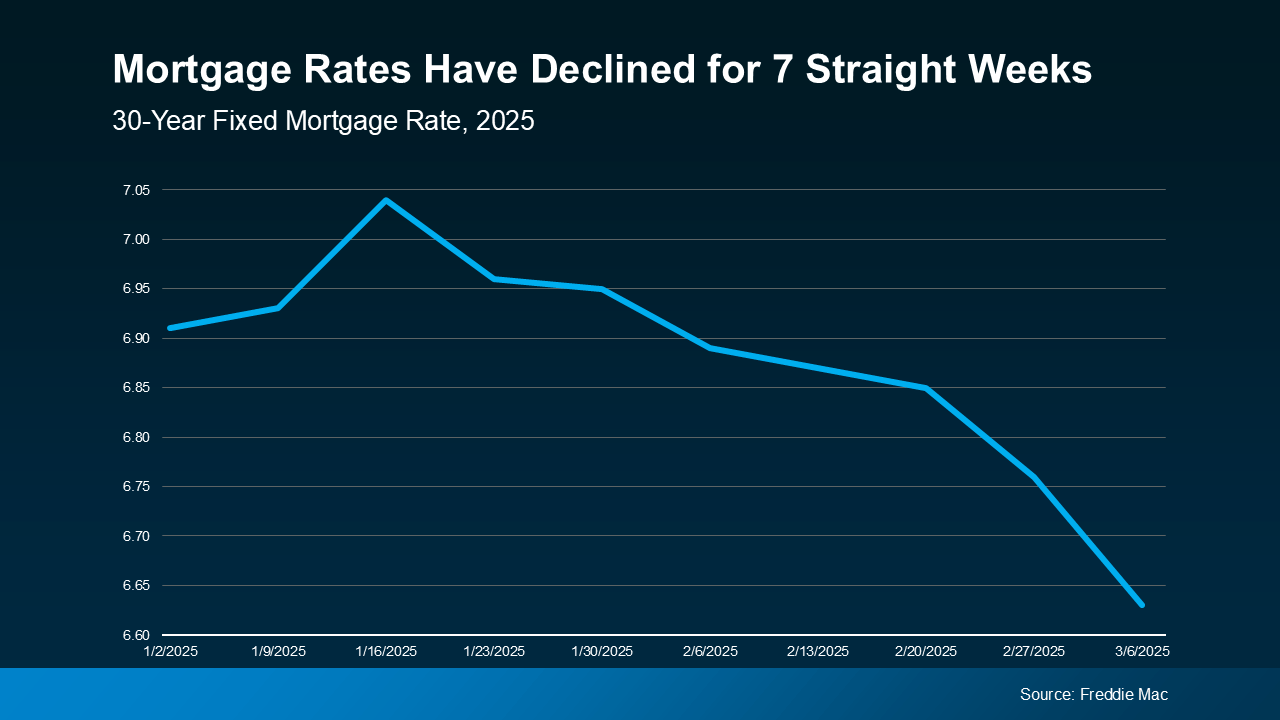

Mortgage Rates Drop to the Lowest Point in 2025 So Far

If you’ve been holding off on buying a home for a lower mortgage rate, take another look at the market. Mortgage rates are trending downward, and they just hit their lowest point of the year so far.

According to a report from Freddie Mac, mortgage rates have been falling for seven straight weeks. The average weekly rate for a 30-year-fixed mortgage is now at the lowest level its been in 2025.

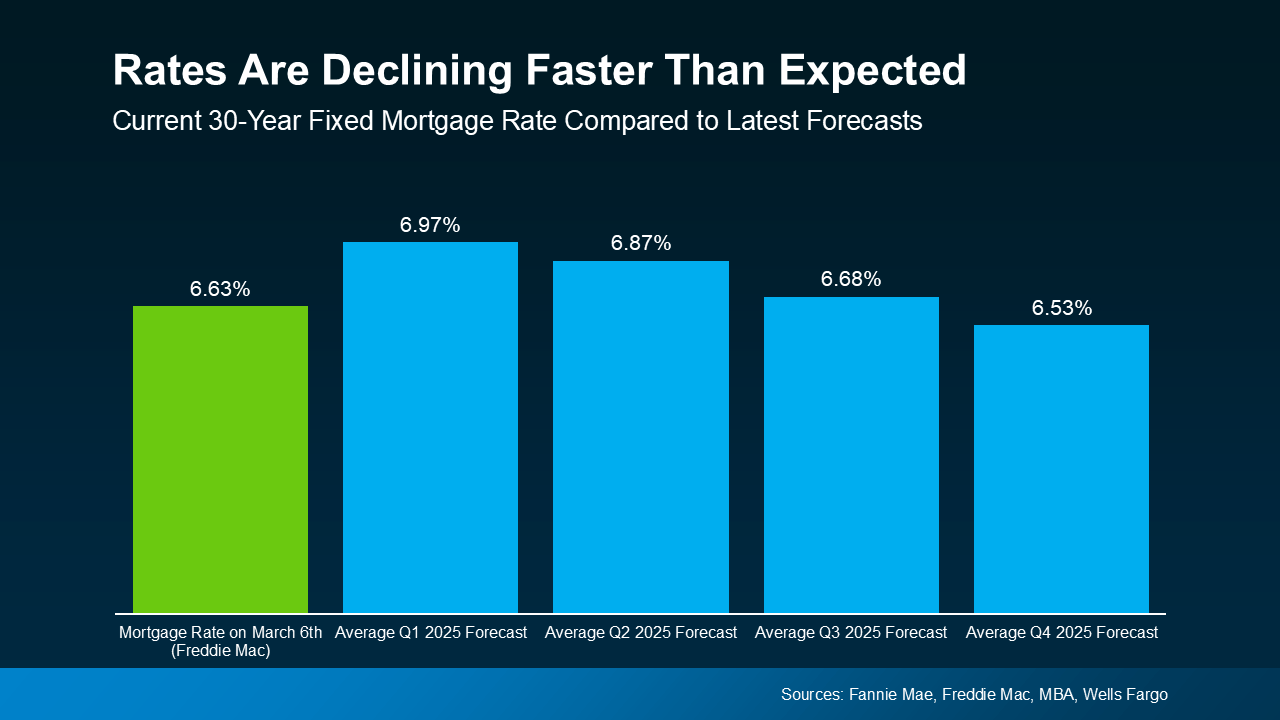

This may not sound significant on its own, but it outlines a remarkable trend. A drop in rates from over 7% to the mid-6’s can make all the difference when buying a home. What’s most significant is that experts previously predicted that rates wouldn’t fall this low until Q3 of this year.

Why Are Mortgage Rates Dropping?

According to Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), ongoing economic uncertainty is a driving force in pushing rates lower:

“Mortgage rates declined last week on souring consumer sentiment regarding the economy and increasing uncertainty over the impact of new tariffs levied on imported goods into the U.S. Those factors resulted in the largest weekly decline in the 30-year fixed rate since November 2024.”

The timing of this rate drop is great for buyers moving into the Spring 2025 market. But remember that mortgage rates can change quickly, and always expect some volatility in markets driven by uncertainty. With that said, this small window of rates dropping into prime buying season might be exactly wait you’ve waited for.

What Falling Mortgage Rates Mean for Your Buying Power

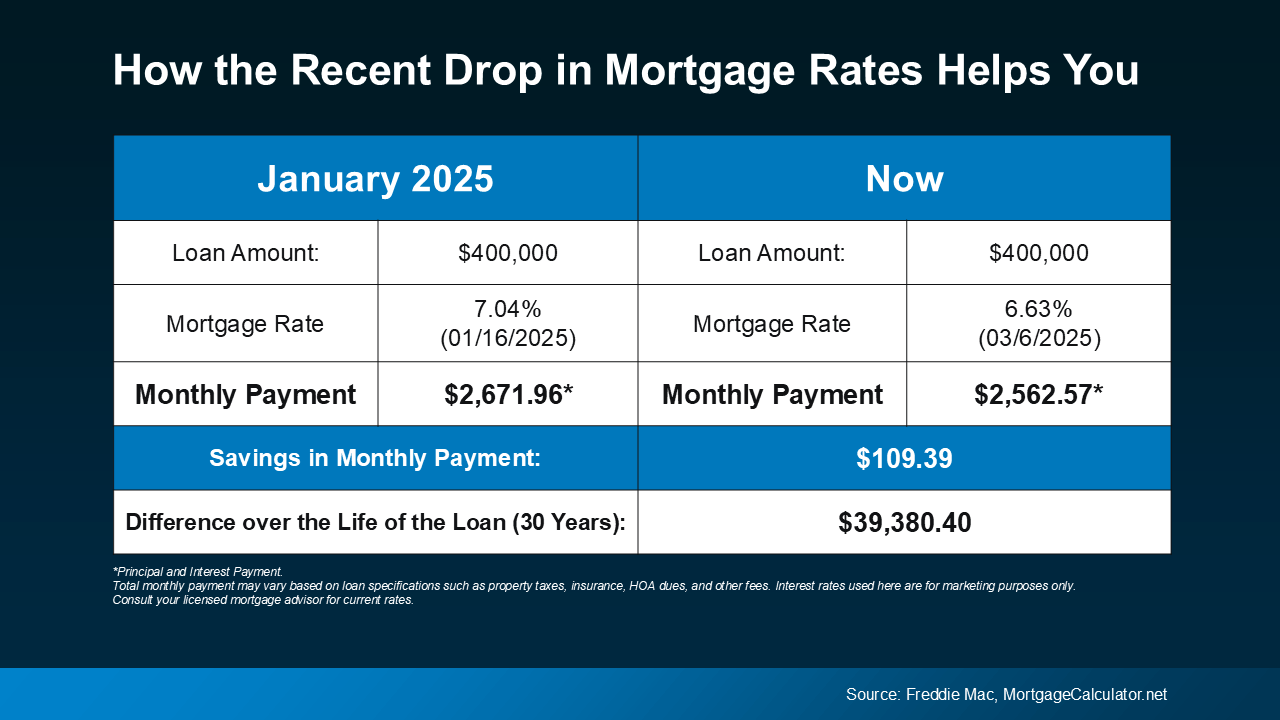

Even a small reduction in your mortgage rate can make a huge difference in your monthly housing payment. The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house when rates were 7.04% back in mid-January (this year’s mortgage rate high). The right side shows what it could look like if you buy a home now at current rates.

In just the past few weeks, the expected payment on a $400K loan has come down by over $100 per month. That’s a significant savings that can make a world of difference when deciding to buy a house.

Recent economic shifts have driven rates down faster than expected, and that’s great news. But remember that this could change at any time in the coming days and months for better or worse. So if you’re waiting for rates to fall further before you buy, think hard about the current window of opportunity before making a decision.

Conclusion

Mortgage rates have dipped to their lowest point in 2025 so far. This grants buyers a great position moving into the spring buying season, especially for those who have been waiting. The unpredictability of the market and larger economy mean volatility, so get expert advice and consider before making a decision.