Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

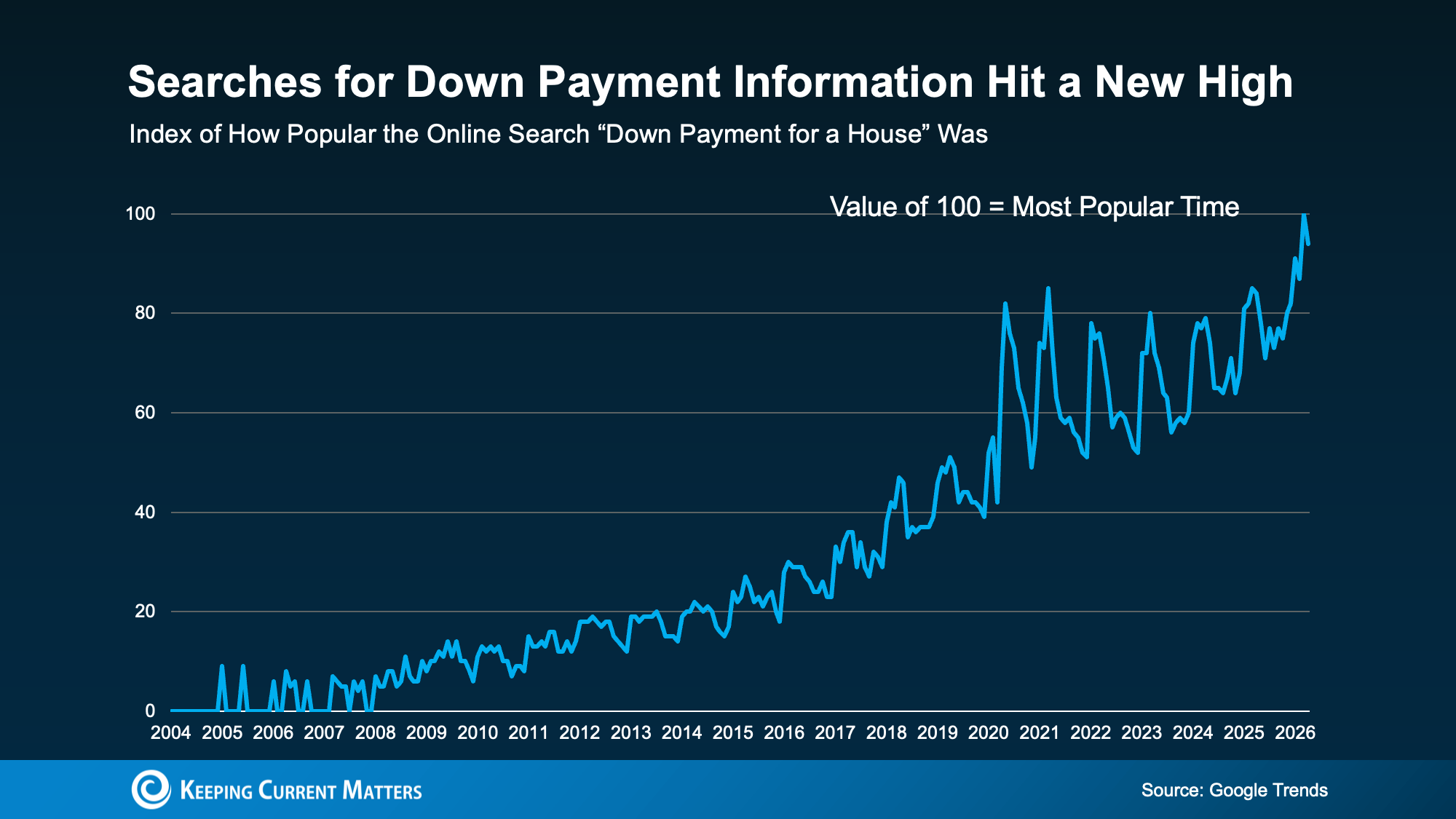

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

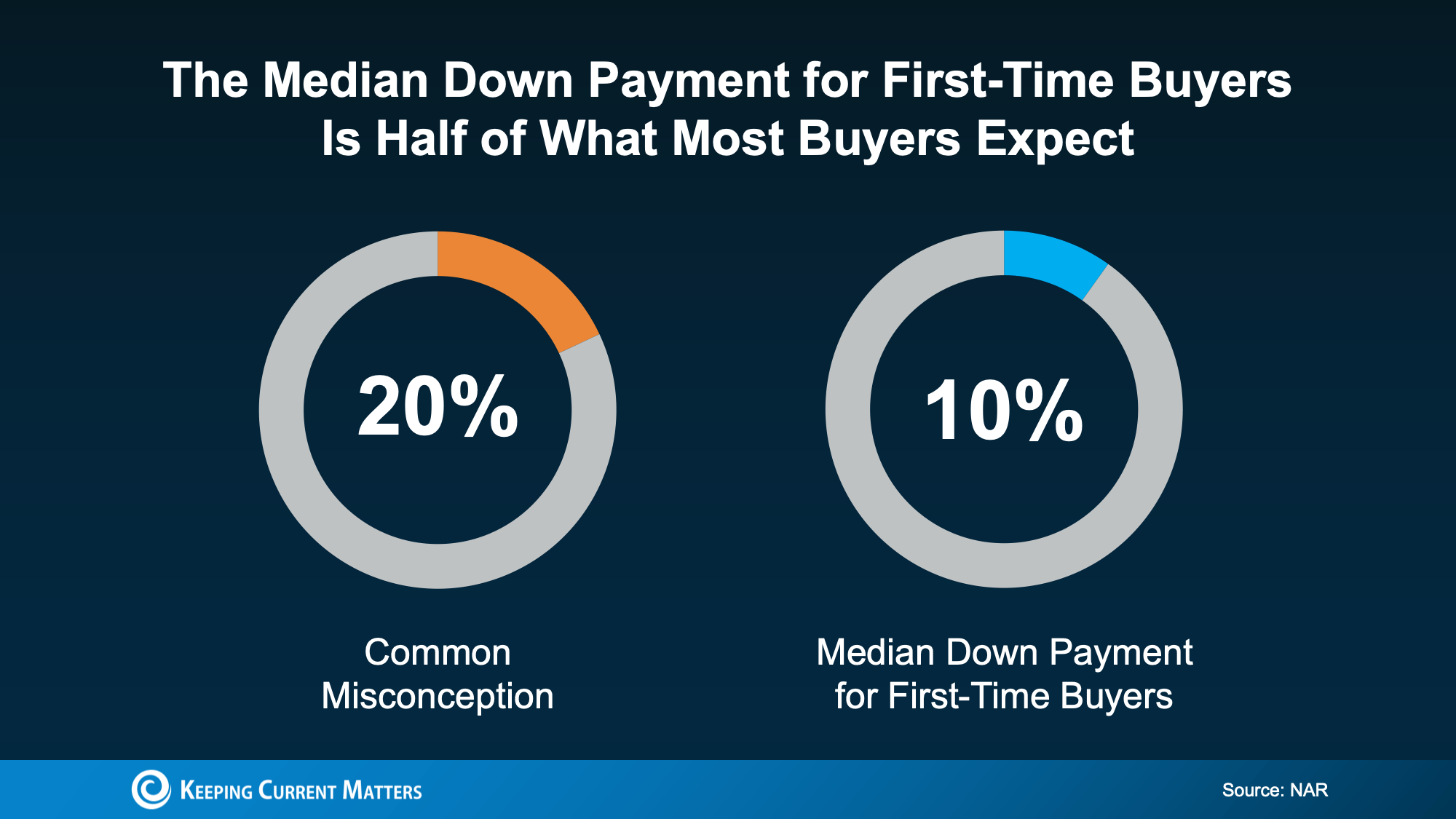

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

Are Home Prices Dropping? What the Latest Data Show

You’ve probably seen headlines or social posts claiming that home prices are falling. It’s an attention-grabbing message, and it naturally leads to two big questions:

- Is this the start of a crash?

- What does it mean for my home’s value?

Here’s the reality: a few markets are seeing small, normal pullbacks, but this is not a nationwide crash. In most areas, prices are still rising or holding steady, just not at the breakneck pace we saw a few years ago.

Home Prices Are Still Rising Nationally

A lot of online chatter focuses on isolated price drops without mentioning the broader data. Nationally, prices have continued to trend upward, but at a slower rate than usual.

According to a new report from the National Association of Realtors (NAR):

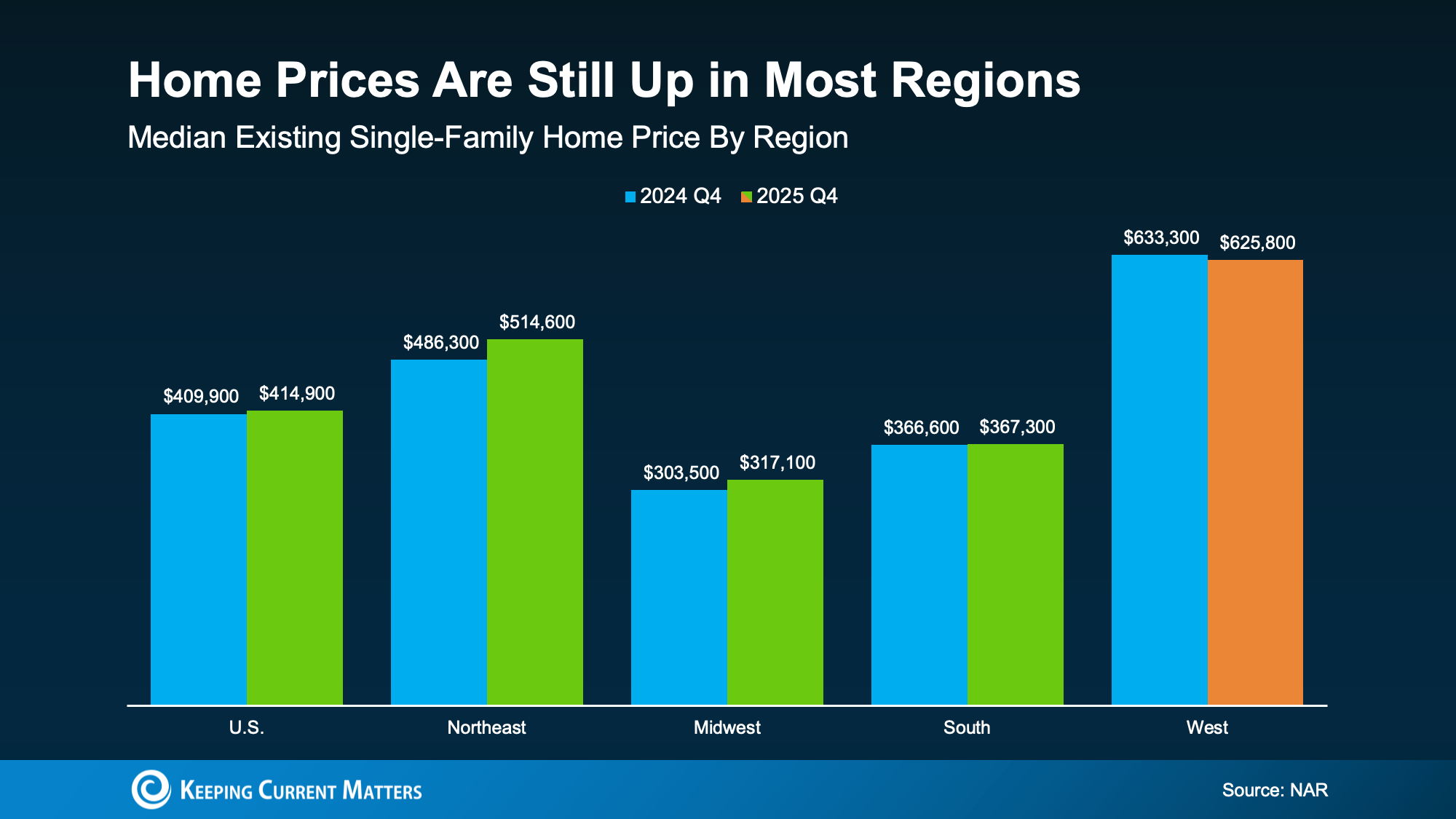

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s modest growth compared to the peak “boom” years, but it’s still growth. And regionally, the story varies.

At a glance, the numbers show:

- Northeast, Midwest, and South: prices generally up or steady.

- West: more mixed, with some markets seeing mild price declines.

In other words, the market is cooling and normalizing, not crashing.

Why You’re Hearing So Much About Price Drops

Price declines make for clickable headlines. But a few factors can make a local shift look like a national trend:

- High-profile metros go viral. A dip in one major market can dominate the conversation.

- Seasonality is real. Some months are softer than others, even in healthy markets.

- Affordability has cooled demand. Higher payments can reduce competition and push prices to level off.

Those are signs of a market adjusting, not collapsing.

Some Markets Have Softened, But Context Matters

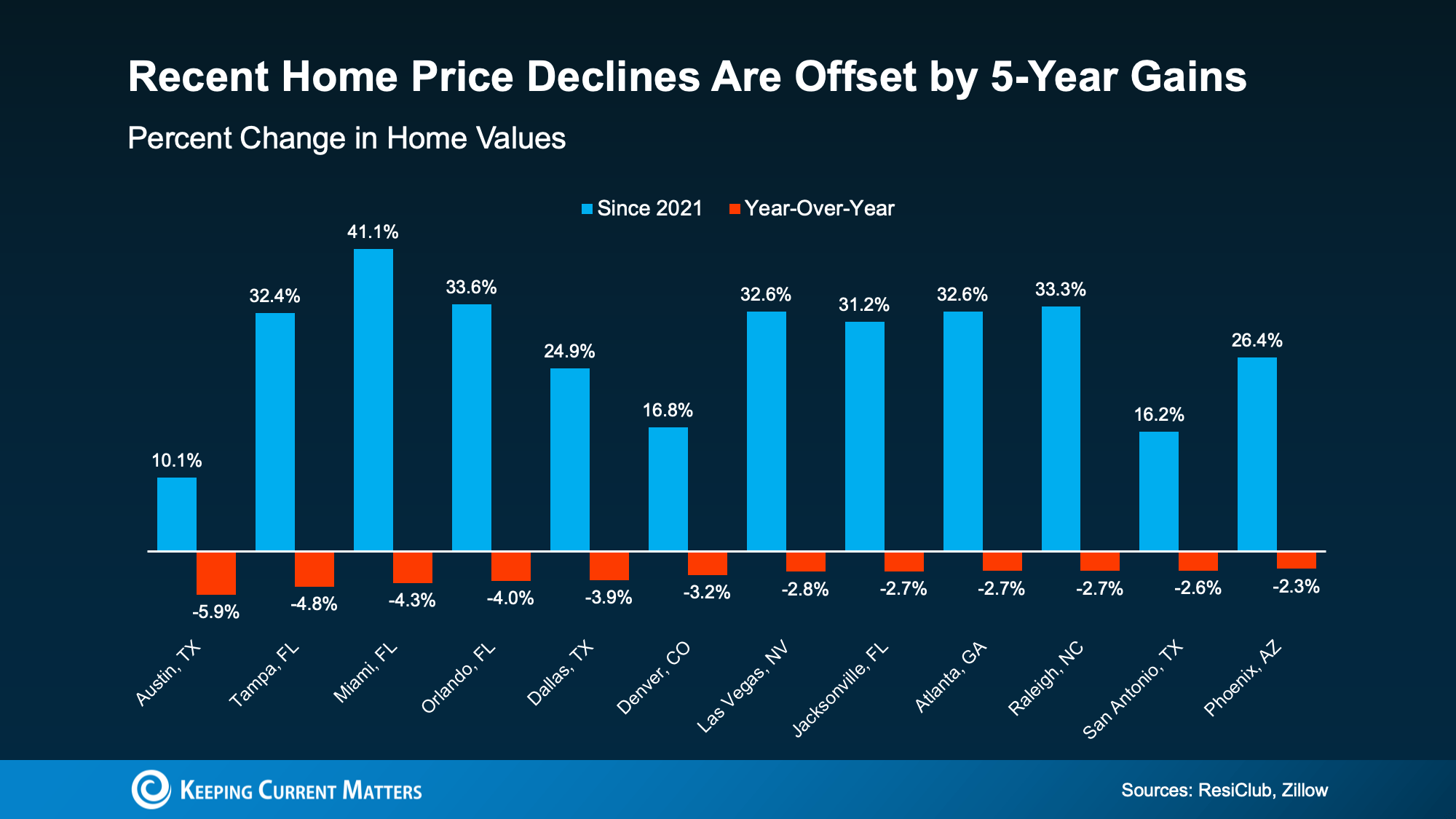

In the places where prices have dipped, it helps to look at the big picture. Many of those markets saw especially strong appreciation over the last several years. When you compare today’s values to where they were five years ago, homeowners in many “down” markets are still up significantly overall.

According to data from ResiClub and Zillow, price dips in the short-term aren’t always the cause for concern they seem to be. The long-term trends tell a clearer story, and they remain strong for many homeowners.

The key point: a pullback after rapid growth is not the same thing as a crash. It’s often a correction toward something more sustainable.

What This Means for Homeowners and Buyers

If you’re a homeowner:

In most markets, you’re not watching value evaporate overnight. Instead:

- You likely still have meaningful equity compared to pre-2020 values.

- Pricing strategy matters more now that buyers aren’t automatically overbidding.

- The best indicator is recent comparable sales in your neighborhood.

If you’re a buyer:

A cooler market can create more breathing room:

- You may see more negotiability in certain areas.

- You may have more time to decide than during the peak frenzy.

- But waiting for a big “crash” could mean missing the right home if your local market is stable.

Real estate is local. The best move depends on your budget, timeline, and the neighborhood you want.

How to Know What’s Happening Where You Live

National headlines can’t tell you what’s happening on your street. To get a clear picture, look at:

- Recent sold prices (comps) for similar homes.

- Days on market and list-to-sale price ratios.

- Inventory levels and new listings.

- Price reductions on comparable listings.

A local real estate agent can help make sense of your market’s unique trends. That way, you know you’re relying on sound information for any decision you make.

Conclusion

Home prices are rising or holding steady in most parts of the country, and a handful of small declines does not equal a nationwide downturn. If you want to know what your home is worth today, review your local numbers with a trusted real estate professional.

Top 12 Home Improvement Projects That Add the Most Value

Home improvement projects can be productive, fulfilling ways to spend your spare time. But, they can also be costly ventures that end up being more trouble than they’re worth. Your invested time, money, and energy matter, and some upgrades don’t offer the return on investment you expect. U.S. News Real Estate explains it this way:

“. . . not every home renovation project will increase the resale value of a home. Before you invest in a swimming pool or new addition, you should consider whether the project will pay itself off by getting prospective buyers in the door when it’s time to sell.“

Like most projects, home improvement is best tackled when you’ve done all the planning beforehand. That’s why it pays to know the cost of your project, and how much it might increase your home value. Whether you have plans to move or not, strategizing to find the best project will pay off in the long run.

How Preparation Pays Off

If you’re planning to move soon, starting early can make a valuable difference. And if you’re not, you’ll still be glad you planned ahead when life’s surprises get in the way. If your moving timeline changes, you won’t want to shell out extra for rushed projects on short notice.

By doing home updates now, you can work at your own pace, saving yourself headaches and money later on. You’ll also have time to enjoy the updates you make to your home before you decide to move. And when you do move, you’ll rest easier knowing there’s no laundry list of work left before you list.

What Buyers Really Want

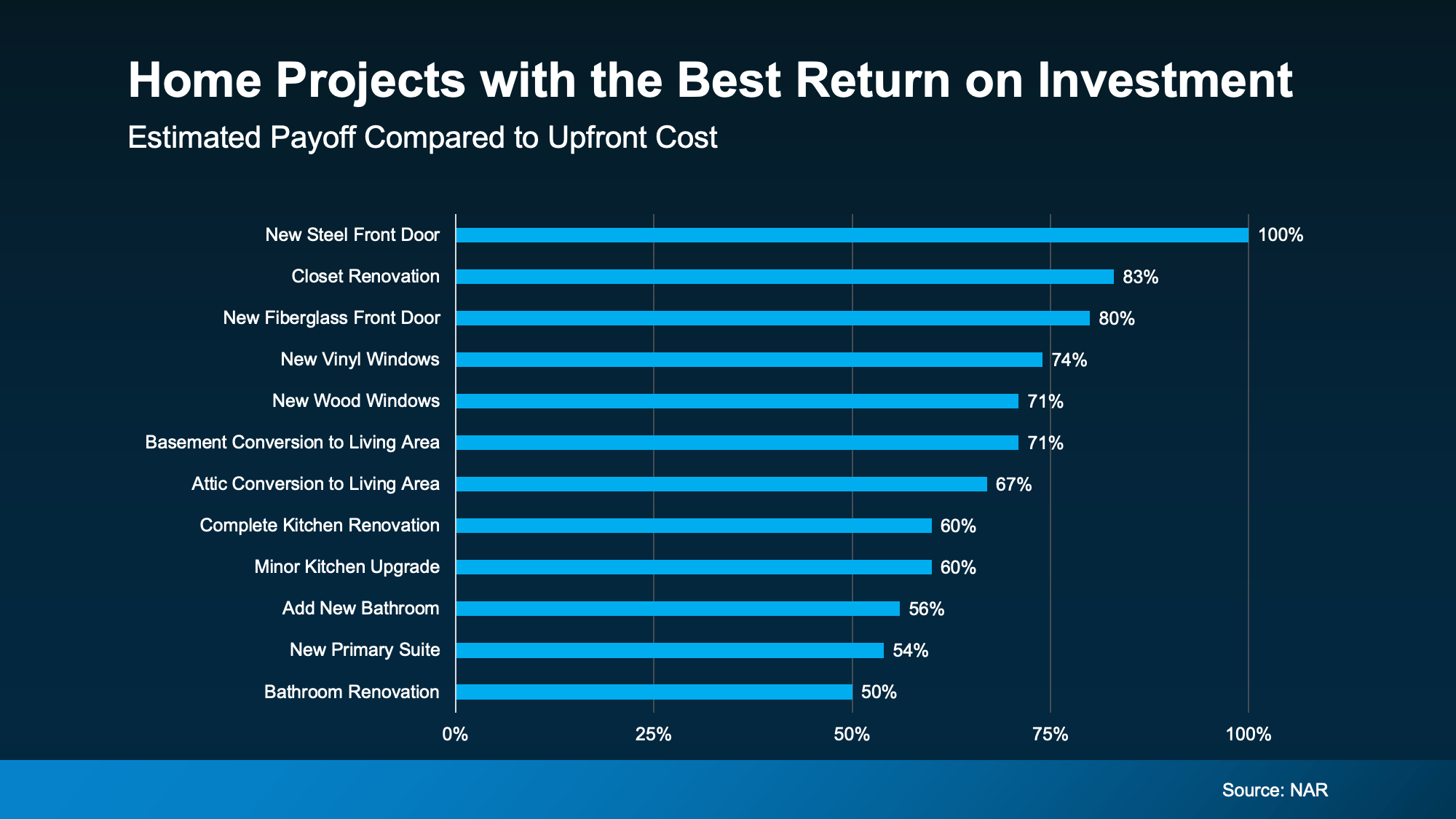

Your first step is choosing a project that will increase your home’s appeal to buyers at selling time. So if you’re not sure what projects are worth your time and money, new industry data can help. A recent study from the National Association of Realtors (NAR) shows the top upgrades offering the best return on investment (ROI).

As the graph above shows, the top home improvement projects that add the highest (estimated) value are as follows:

- New Steel Front Door – 100% return on investment.

- Closet Renovation – 83% return on investment.

- New Fiberglass Front Door – 80% return on investment.

- New Vinyl Windows – 74% return on investment.

- New Wood Windows – 71% return on investment.

- Basement Conversion to Living Area – 71% return on investment.

- Attic Conversion to Living Area – 67% return on investment.

- Complete Kitchen Renovation – 60% return on investment..

- Minor Kitchen Upgrades – 60% return on investment.

- Bathroom Addition – 56% return on investment.

- New Primary Suite – 54% return on investment.

- Bathroom Renovation – 50% return on investment.

If you’ve already been thinking about a high-ROI project on this list, that’s great news. There’s a good chance it’ll improve your living quality now and increase your home’s value in the long term.

But remember that this list is based on national data using averages from listings sold nationwide. The most in-demand improvements that buyers will pay for depends largely on your local real estate market. That’s where talking to a local agent can help, as an article from Ramsey Solutions explains:

“The best way to gauge what you can expect in terms of resale value on home improvements—especially if you’re planning to sell soon—is to talk to a real estate agent who is an expert in your market. They’re sure to know the local trends, and they can show you how other homes with the features you want to add are selling. That way, you can make an educated decision before you start ordering lumber and knocking down walls.”

At the same time, be careful not to overdo it on home improvements. An excess of upgrades can raise your home’s price right out of the local market. And while that may sound ideal, it can make your listing unattractive to the buyers in your area. This is another area where a local agent can help you choose the best projects for your specific market.

Conclusion

Whether you have moving plans on the horizon or not, making thoughtful, deliberate home improvements can be valuable. Even if you have no intention to move, updates give you more reasons to love and enjoy your house. And, of course, the home value increases that high-ROI projects offer are bound to pay off in the future.

Have you been considering a particular home upgrade but aren’t sure if it’s worth it? Contact us today to connect with an agent who can give you the best advice for your unique area.

How Could a Recession in 2025 Affect the Housing Market?

As talk about economic slowdowns runs wild, worries about a potential recession in 2025 are on the rise. Naturally, many homeowners are wondering what a recession could do to the value of their home, and their buying power.

Using historical data from recessions of decades past, let’s see how a recession might affect the housing market in 2025.

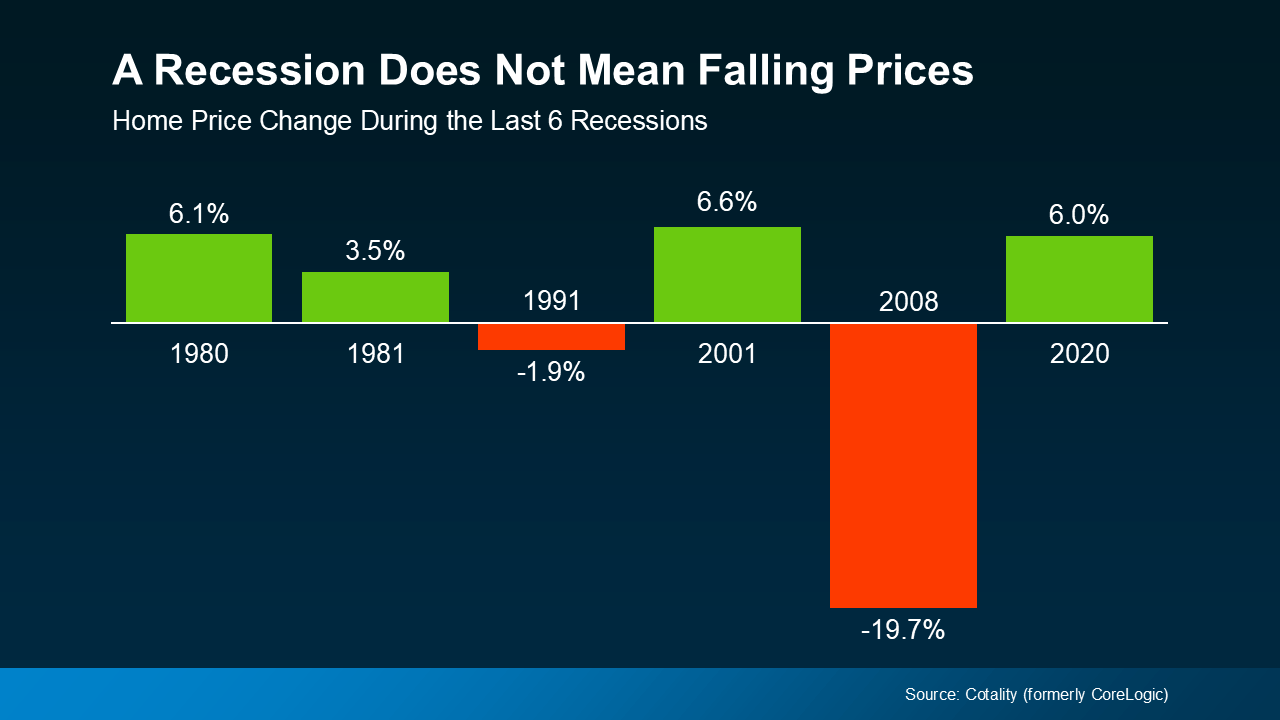

A Recession Won’t Lower Home Prices

It’s a common misconception that a recession will cause home prices to crash, like they did in 2008. In reality, 2008 was the only time the housing market saw such an extreme, dramatic drop in prices. Overflowing home inventory caused that price crash, and conversely, low inventory has prevented a similar crash in the years since.

Even in markets where housing inventory is up, it’s still far below the listing oversupply that caused the 2008 crash. Indeed, according to data from Cotality, home prices actually increased during four of the last six major recessions.

As the graph shows, a recession doesn’t necessarily mean that home prices will crash, or even drop. In reality, historical data shows that home prices usually continue along their current trajectory when a recession hits. And at the moment, home prices are still rising nationally, but at a more normalized rate. So, as the market stands now, a recession in 2025 would most likely drive prices even higher.

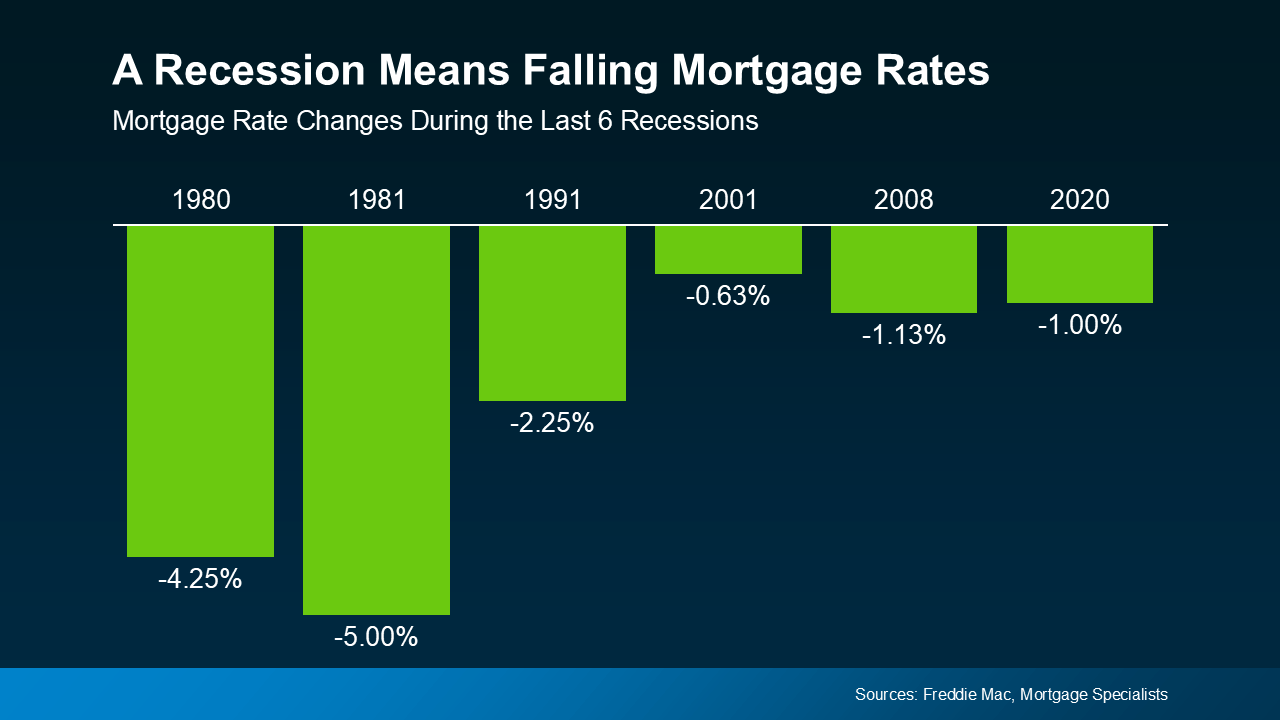

Mortgage Rates Typically Decline During Recessions

Home prices may stay their path during economic slowdowns, but mortgage rates actually tend to drop. Looking again at historical data from the last six recessions, this time from Freddie Mac, mortgage rates fell each time.

Historically speaking, a recession could mean that mortgage rates may even decline this year. However, the last time a recession dramatically lowered mortgage rates was over three decades ago in 1991. So with that said, even if a recession does happen, don’t expect a game-changing drop in mortgage rates.

Conclusion

Nobody ever truly knows what the economy will do, but the odds of a recession in 2025 have increased. Still, a recession doesn’t mean you need to worry about the housing market or the value of your home. The historical data tells us that a recession may even drive home prices higher and mortgage rates lower.

Wondering how an economic slowdown could impact your local market? Connect with us to get the info you need to plan ahead.

Should You Buy a Home This Spring or Wait for Lower Prices?

You’re probably familiar with the saying “The best time to plant a tree was yesterday, but the next best time is today.” It’s a valuable lesson about future planning and investment that, surprisingly, applies to the decision to buy a home too.

Even though buying a home is a major financial expense, it’s also a major investment that grows over time. As the price of your home increases over time, the value of the equity you’ve built grows with it. And while waiting for prices to drop may be an attractive option, trying to time the market rarely works.

But here’s something to consider: the longer you wait to buy a home, the more your patience could cost you. Let’s explain why.

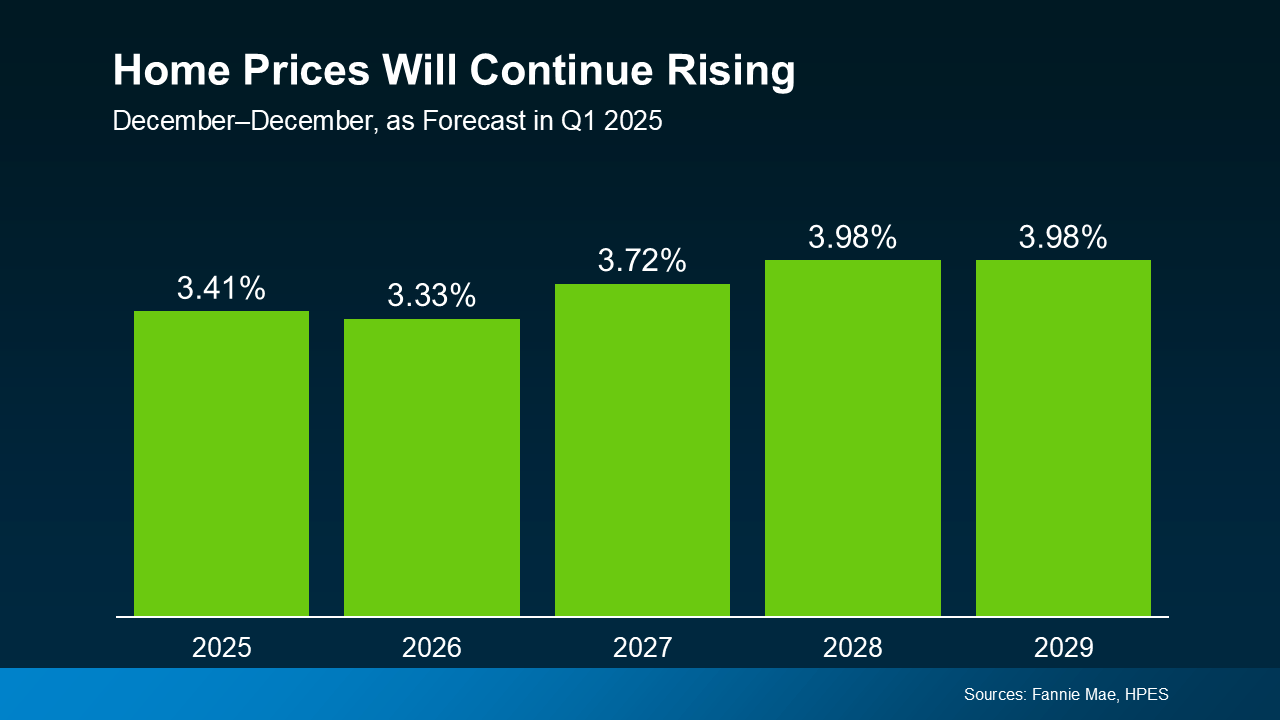

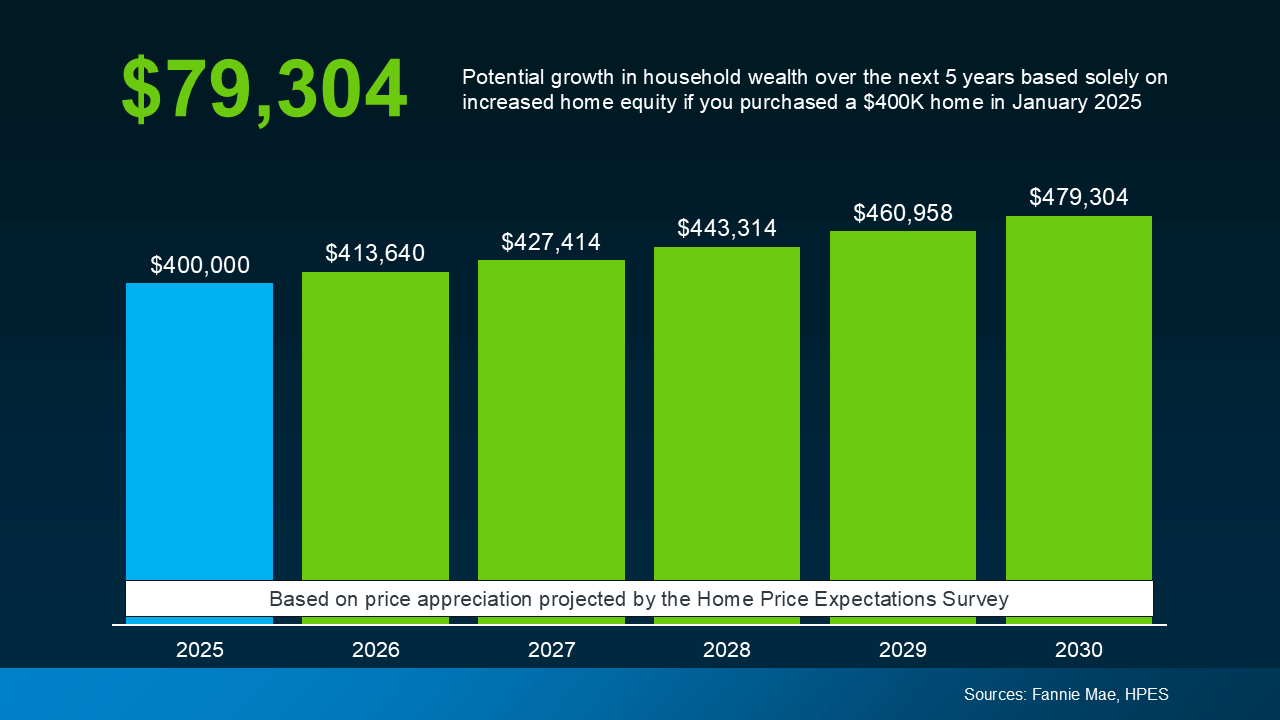

Home Prices Are Expected To Continue Climbing

Each quarter, over 100 housing market experts respond to Fannie Mae‘s Home Price Expectations Survey (HPES). Consistently, the survey results show experts agreeing that home prices will continue to rise through 2029 or even longer.

Sharp price increases may be behind us, but experts predict steadier, healthier increases of 3-4% per year moving forward. This rate of increase will vary by market from year to year, but it’s much closer to normal. Reliable growth is a promising sign for hopeful buyers, and the housing market at large, as the graph below demonstrates.

Even in markets experiencing slower price growth or short-term decreases, the steady gains of homeownership eventually win in time. After all, a growing, long-term financial investment will always beat a one-time discount.

Here are the main points to remember:

- Home prices will be higher next year. Experts don’t expect home prices to fall any time soon, at least at the national level.

- Waiting for a perfect mortgage rate or price drops is a gamble. With only slight dips in mortgage rates expected in the near future, price increase could outpace any potential mortgage savings. Unless home price growth is slow or mortgage rates are low in your area, waiting will likely be more expensive.

- Buying early means building more equity. When you invest in homeownership early, your equity and appreciating home value reward you in the long run.

The Costs of Waiting To Buy

To demonstrate how these theories play out in real-world numbers, here’s a typical example. If you were to buy a $400,000 house in 2025, it could gain almost $80,000 in value by 2030. The graph below demonstrates how this value appreciates year by year based on the expert data we mentioned earlier.

This can be a considerable difference in your future wealth and why buyers who invest early are often glad they did. When it comes to building wealth through long-term investment, time in the market matters.

The question to consider isn’t “Should I wait to buy?” It’s really “Can I afford to buy now?” Just like planting a tree, making short-term sacrifices to buy a home will eventually pay off in the long-term.

Between rising prices and stubborn mortgage rates, today’s housing market is challenging, but achieving homeownership is far from impossible. Exploring different neighborhoods, seeking alternative financing options, or applying for down payment assistance programs can all make a critical difference.

What’s most important is acting decisively when you’re able to, instead of waiting for a perfect opportunity that never comes.

Conclusion

If you’re interested in buying but still undecided, take the time you need to make the right choice. But, remember that realizing an investment takes time, and the sooner you make one, the sooner you’ll be rewarded.

If you’re curious about what’s happening with prices in our local area, then reach out to us. Even if you’re not ready to buy, an expert local agent can fill you in with the info you need.

Many Fear a Housing Market Crash in 2025 – Will It Happen?

Between every economic uncertainty underpinning this year so far, Americans are understandably trepid about the future. Amid market lows and rising prices, many are asking if we’re heading for a housing market crash in 2025.

If talk of tariffs and mercurial markets are giving you pause about your plans, you’re not alone. In fact, new data from Clever Real Estate has found that 70% of Americans are worried about a housing crash in 2025. But how likely is this, and what does the latest data say?

Low Inventory Prevents a Crash in Prices

Before you put your plans to buy or a sell a home on hold, let’s look at the facts. The reality is that the trends in the housing market we’re seeing aren’t signs of crashing, only of shifting. As Chief Economist at First American Mark Fleming explains:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

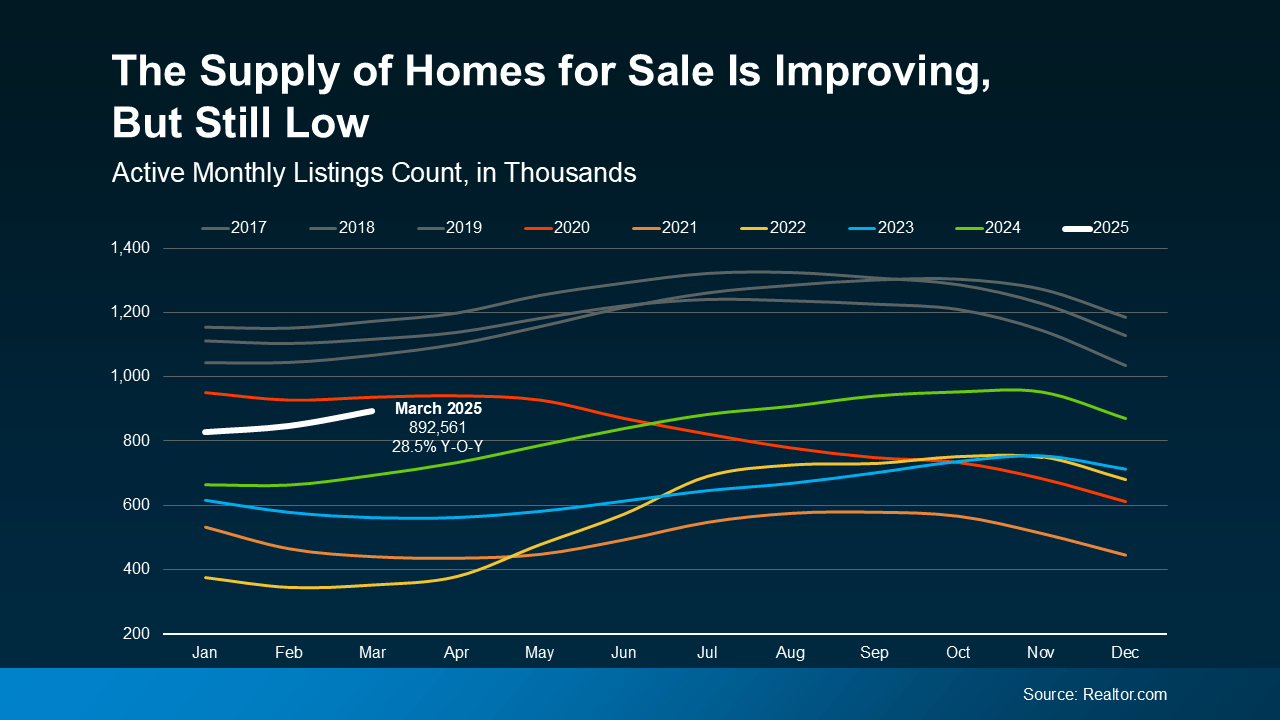

Consider the basic laws of supply and demand. If the supply of something is low, its prices are bound to go up, and homes are no exception. And even though housing inventory is up in 2025, high demand from buyers is still driving home prices higher.

According to recent data from Realtor.com, the number of homes for sale in 2025 is climbing, but still below normal levels. Even still, home supply is at its highest since pre-pandemic levels, showing a positive trend in the right direction.

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

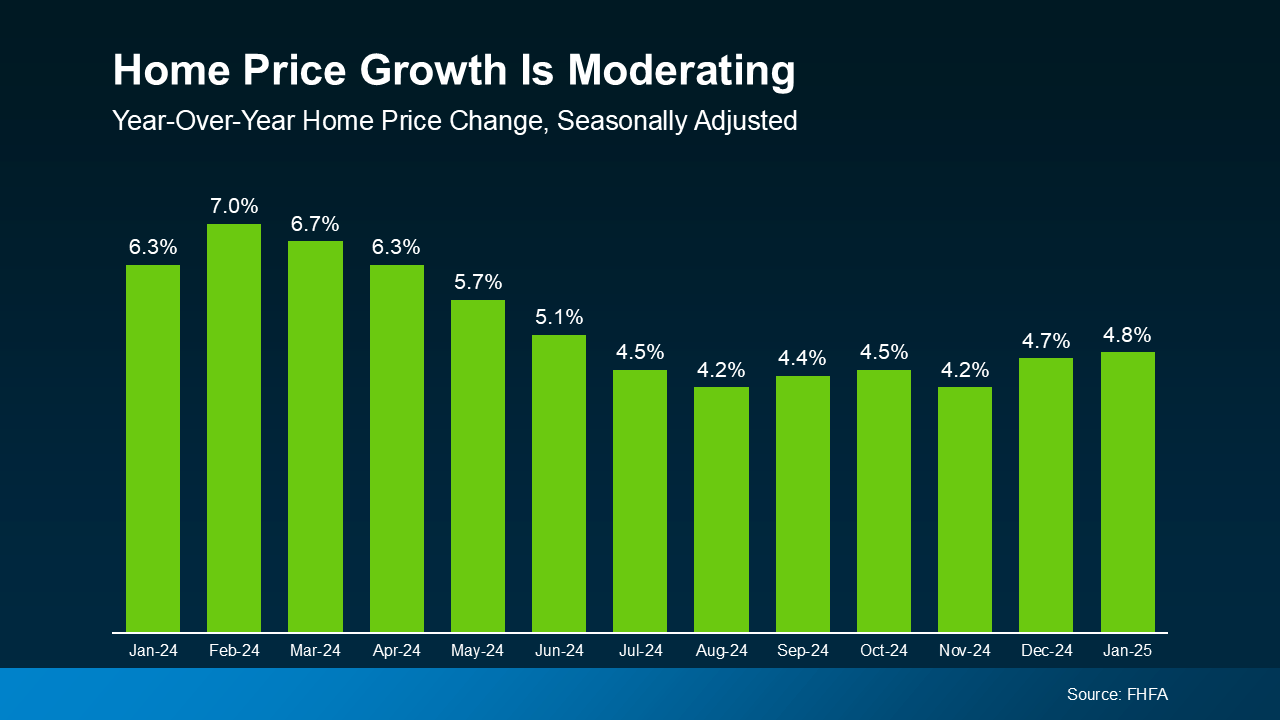

Home Prices Normalize as Inventory Increases

As more homes are listed on the market, upward pressure on home price growth normalizes. Prices may not be falling, but they’re rising at a rate closer to what we’d consider normal for the market.

Even though prices aren’t declining nationally, increased inventory means they’re rising more slowly than they were. The trend we’re currently seeing is what’s considered price moderation.

The good news for buyers is that this price moderation is expected to continue throughout the rest of the year, according to a January report from Freddie Mac:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

This means that home prices will continue rising in most markets, but not as quickly as they did in 2024. This is great news for anyone who’s been priced out of the market thanks to rapid price appreciation these past few years.

These numbers represent national trends, so the true story will vary in individual markets. A local real estate agent can give you the latest details on the market trends in your your own unique area.

Conclusion

Fears of a housing market crash in 2025 abound, but don’t let this worry you. While a little caution is healthy, experts are confident that a housing market crash is unlikely in 2025. As a recent report from Business Insider says:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyond unless the economic outlook changes.”

In reality, this year’s housing market is stabilizing thanks to decreasing price growth and increasing home supply. If you’re curious about the market trends in your local area, contact us today to connect with an agent who can reassure you with the facts.

What’s Your Real Home Value in the 2025 Market?

If you’ve checked home prices in the past few years, you know too well that they’re always rising. But if you’re a current homeowner, have you considered what this might mean for your own home value? It may be that your home is worth far more than you think in 2025.

While rising prices are expected, the home value increases of the post-Pandemic housing market have been dramatic. And if you’re a seller waiting to list, this could mean a huge payoff when you finally close. If you’re eager to know much your own house could sell for, finding out is easier than you think.

The Post-Pandemic Home Value Launch

Home prices typically rise around 2-5% per year, but in 2021-2022 that number rose to double-digit levels. In the spring of 2022, year-over-year percentage growth finally peaked at over 20% nationally. The sheer number of buyers in the market during this time sent home prices soaring as housing supply lagged. And though price growth has settled since then, the home value accrued by homeowners in that time remains.

The lingering effects of that volatile period have caused difficulties for buyers, but they’ve also produced great opportunities for sellers. There’s a good chance your house has gained tremendous value since then, and that means more wealth for you.

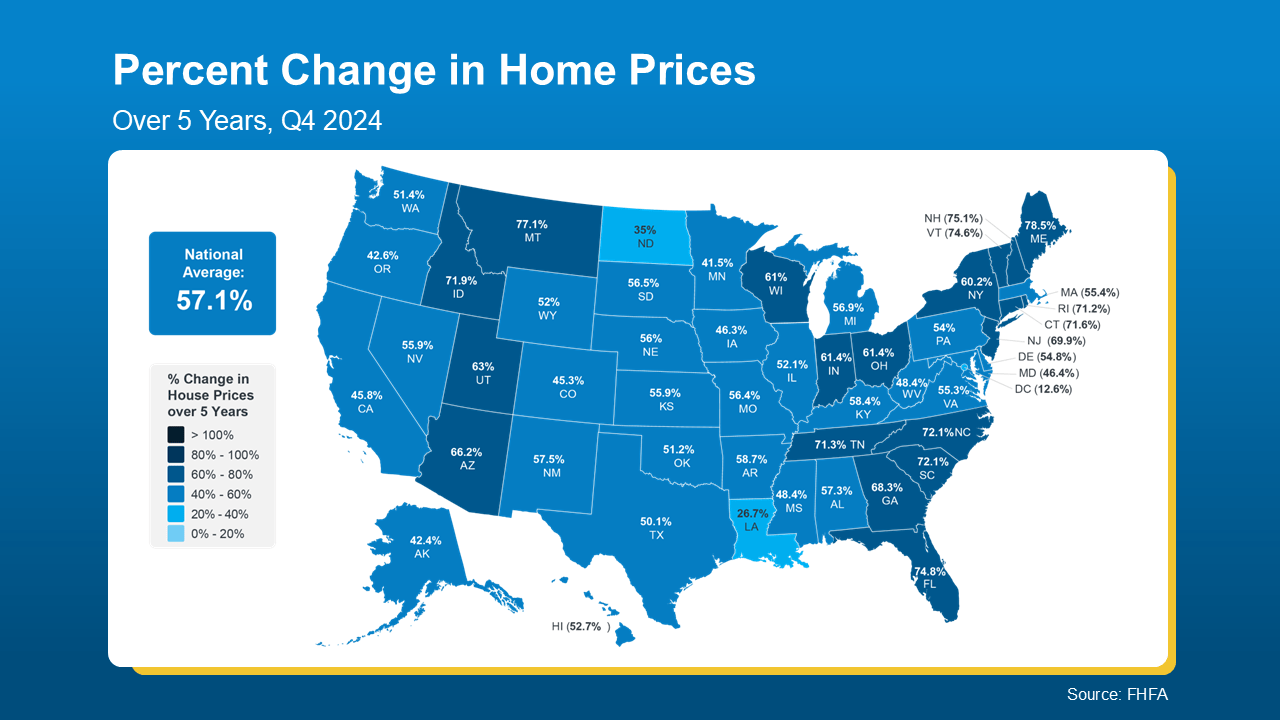

The map below references data from the Federal Housing Finance Agency (FHFA) to illustrate that home prices have risen by nearly 60% in just the past 5 years alone nationally. The most extreme increases have taken place in states marked with a darker blue, like Maine, New Hampshire, and Florida.

If worries about today’s rates and prices have stopped you from selling your home, let these numbers reassure you. Your home’s risen value may be exactly what you need to close the affordability gap and purchase your next house.

Even better, if you’ve owned your home for 10 years or more, your value is likely even higher. You can stack the incredible gains of the past five years on top of five years of healthy appreciation too. And an agent can help you figure out what that really looks like.

How To Find Out What Your House Is Really Worth

Percentages will help you ballpark an estimate, but you need specific numbers to make real, actionable decisions. To help, you can get a free home valuation estimate from us right now using the tool below. You can even sign up for a full valuation report.

Home valuations can be great tools, but only a local real estate agent can give you the best, most accurate look at your house’s real market value. An agent will know the state of your local housing market and the factors driving it. They can provide insights about current housing inventory, pricing of comparable homes, and unique contributors to value like renovations.

By knowing what’s happening where you live, an agent can stack their market knowledge against the unique condition and features of your home and give you an accurate estimate of your home’s current value in your area.

Conclusion

Home values have taken off in just the past few years, and that’s great news for current homeowners. Knowing what your house is worth in today’s real estate market will help you plan your next move. A local agent can give you a great idea of how much your home might realistically sell for.

If you’re a homeowner considering a move, get your free home valuation from us at Century 21 Affiliated now. Ready to sell? Reach out now and we’ll connect you with a local expert real estate agent who can get your house sold.