Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Inflation is moving in the wrong direction again, and that can feel frustrating if you’re thinking about buying or selling a home.

But before the headlines send you into panic mode, it helps to understand what’s actually happening, how it connects to the housing market, and what it may mean for your next move. Simply put: inflation matters, and mortgage rates may stay elevated longer than many people hoped, but that does not mean your plans are off the table.

Inflation Went Up. Here’s What That Means

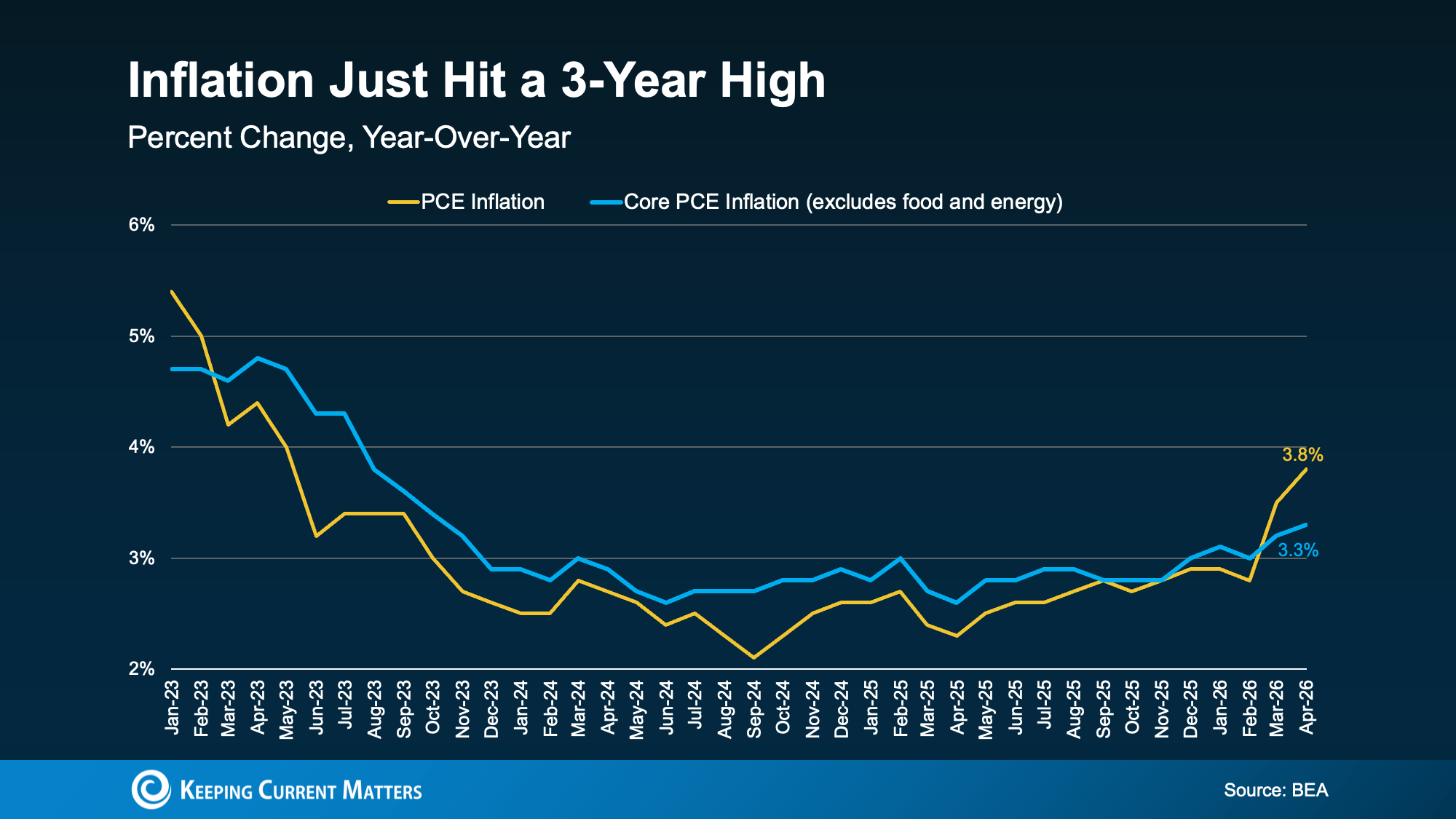

To understand where the economy is headed, we have to look at how the government tracks inflation. One measure that gets a lot of attention is the Personal Consumption Expenditures Price Index, often called PCE.

PCE measures how much more, or less, people are paying for goods and services compared to a year ago. And based on everyday expenses like groceries, gas, utilities, and household costs, you can probably guess why people are paying close attention.

The overall PCE number has moved higher since February. One major reason is the ongoing conflict in the Middle East, which has pushed gas and energy prices significantly higher.

There’s also another version of this measurement called core PCE. Core PCE strips out gas and energy prices because those costs can swing quickly and sometimes make inflation look more volatile than it really is. The Federal Reserve, often called the Fed, watches this number closely.

Here’s the somewhat encouraging part: core PCE is rising, but not as quickly as the overall inflation number. That suggests part of the recent inflation spike may be tied to overseas events and energy prices. If those pressures ease, inflation could settle down somewhat, too.

Why Inflation Matters for Mortgage Rates

Inflation and mortgage rates are connected because inflation influences how the Fed thinks about interest rates.

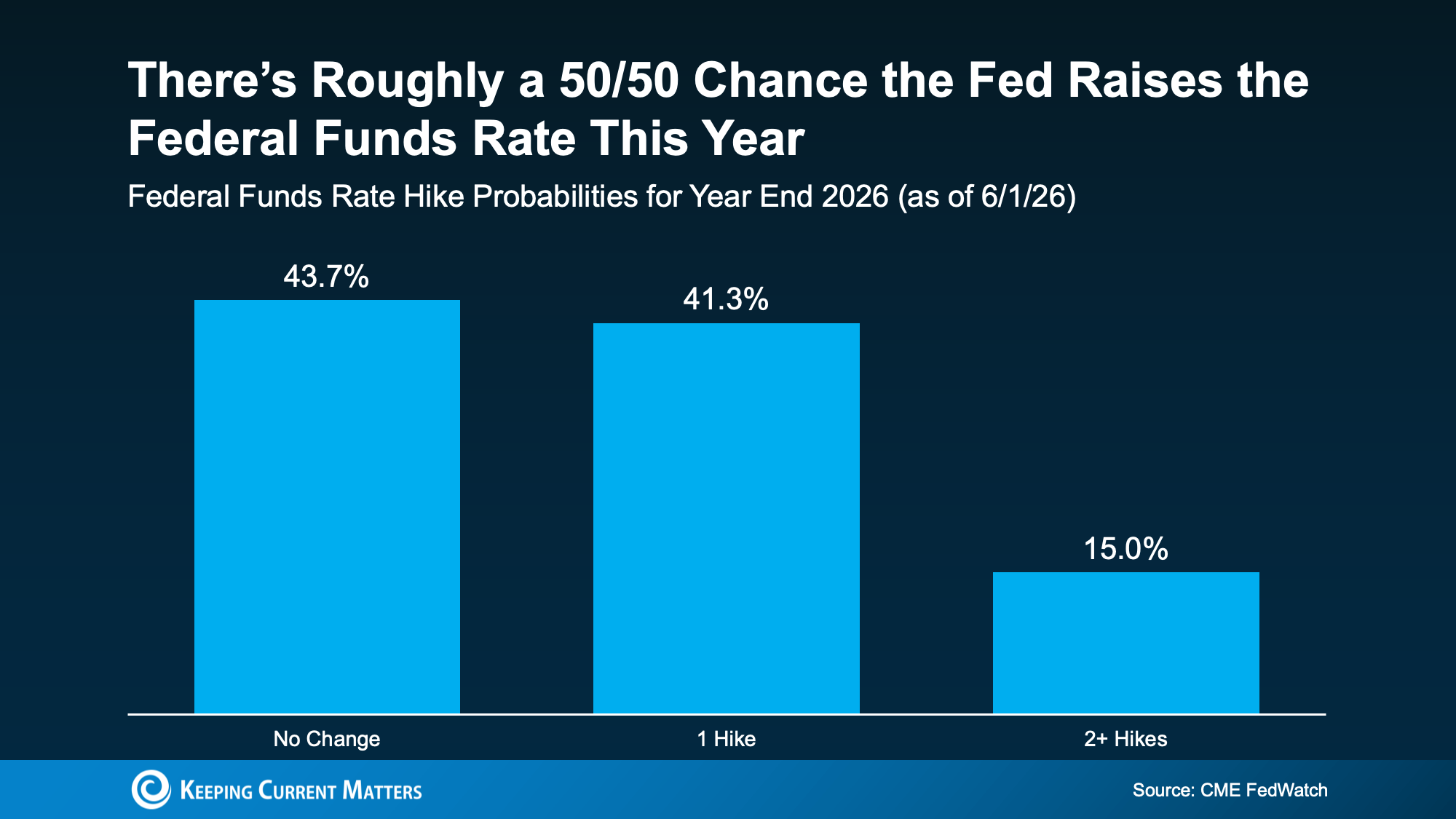

When inflation is high, the Fed may keep the Federal Funds Rate elevated, or even raise it, to help slow spending and bring inflation back down. Mortgage rates do not move in perfect lockstep with the Federal Funds Rate, but the Fed’s decisions can still influence the broader rate environment buyers face.

According to recent data from CME FedWatch, there’s roughly a 50/50 chance that the Fed raises the Federal Funds Rate before the end of 2026.

This “higher for longer” reality means mortgage rates are probably not coming down as soon as most people were hoping.

As Bankrate explains:

“Oil prices and bond yields have dropped a bit . . . but they’re still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

This is a disappointing shift for buyers waiting for lower rates, and it means buying strategy matters more than ever.

Why This is Not 2008

A tougher economy does not automatically mean a housing crash.

Today’s housing market is very different from the conditions that led to the 2008 collapse. Here are a few key reasons why:

-

Inventory is still relatively low. Meaning there’s no major flood of homes hitting the market.

-

Many homeowners have strong equity. That gives sellers more options than homeowners had during the 2008 crisis.

-

Lending standards are stricter. Mortgage qualification rules are much tighter than they were before the last housing crash.

- The main challenge is affordability. Today’s pressure is not being driven by a wave of distressed, underwater sellers.

The market may feel uncomfortable right now, but uncomfortable and unhealthy are not the same thing. A challenging market is very different from a crashing one.

What Buyers Can Do Right Now

Higher mortgage rates don’t mean homeownership is out of reach; it just means the path looks a little different.

Here are a few options worth discussing with a trusted lender:

-

Explore Alternative Loans: Ask your lender about Adjustable-rate mortgages (ARMs) or rate buydowns to help lower your monthly payment in the short term.

-

Seek Financial Assistance: Explore first-time buyer programs, down payment assistance, or seller concessions that could help offset costs.

-

Stay Prepared: Keep in close touch with a trusted agent and lender so you are ready to move fast when rates eventually shift.

A lender can explain which options apply to your situation. Mortgage terms, assistance programs, and qualification requirements vary, so it’s worth getting personalized guidance before making decisions.

The Bottom Line

Inflation is still above where the Fed wants it to be, and that means mortgage rates may stay elevated for a while. But if you need to move, strategy matters more than trying to perfectly time the market.

The right agent and lender can help you understand your options, compare scenarios, and make a move that fits your goals.

Wondering what rising inflation and mortgage rates mean for your next move? Connect with a local real estate professional or lender to talk through your options.