Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

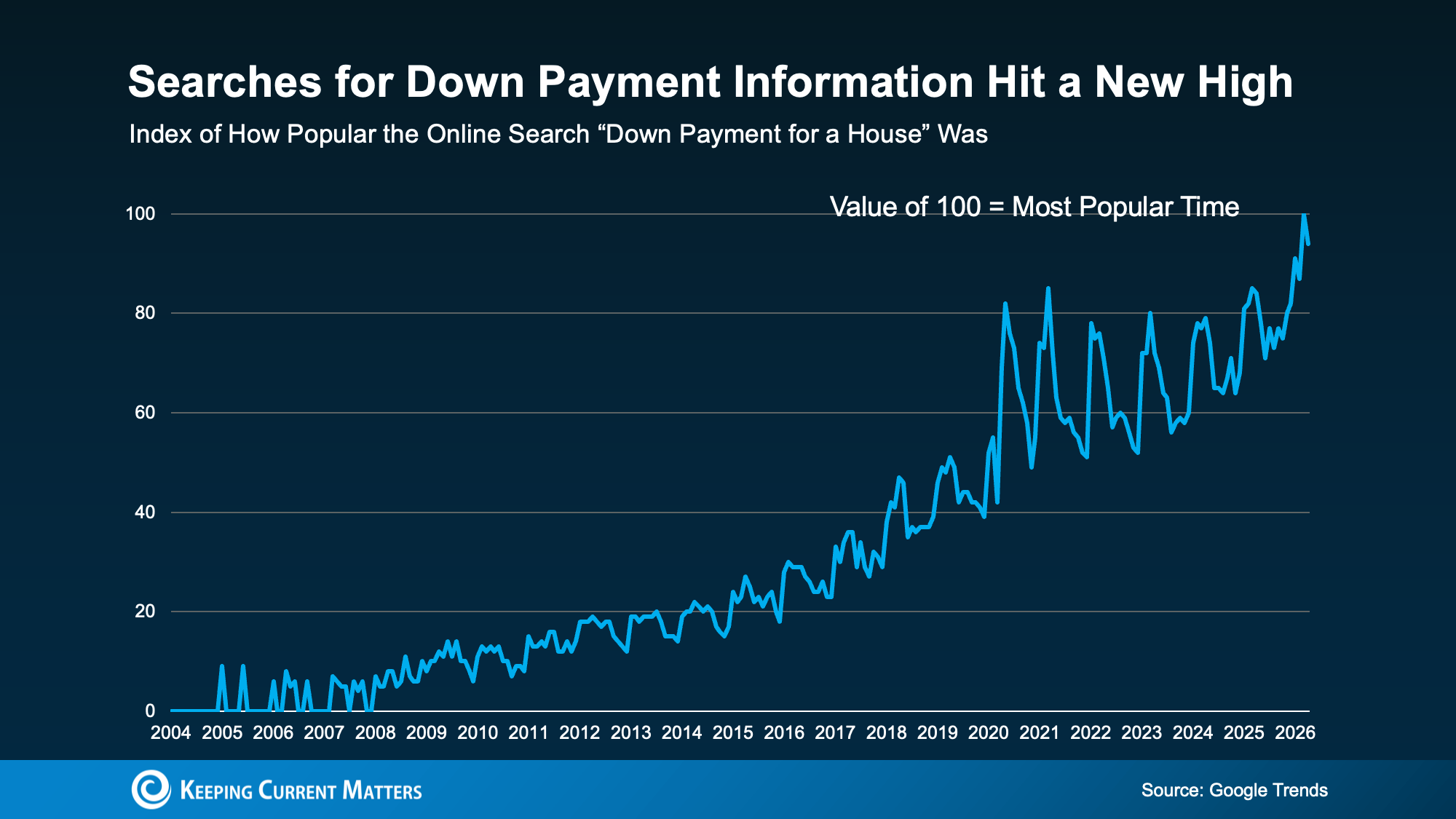

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

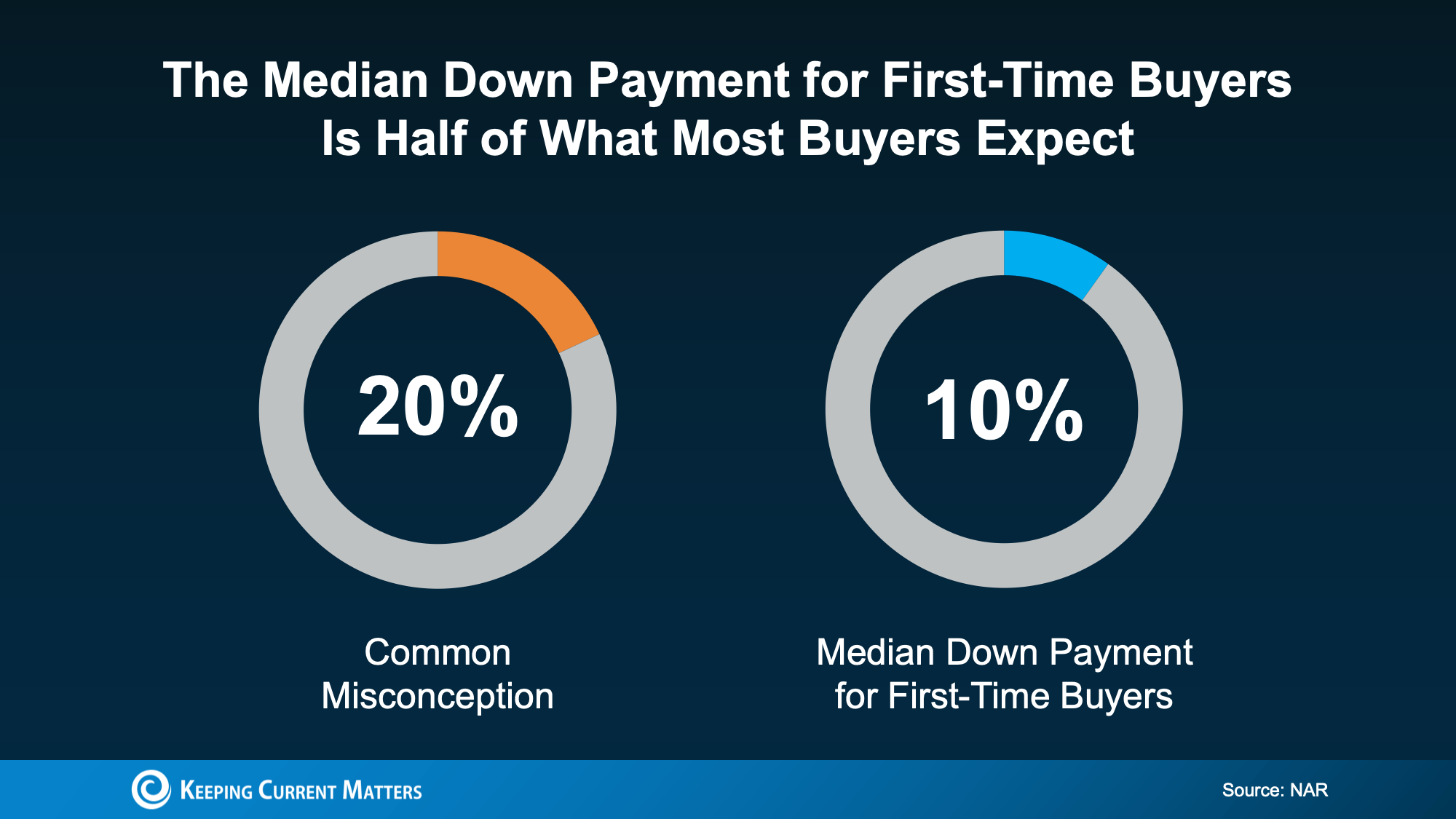

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

Should You Still Buy a Home Right Now? What Buyers Need To Know

Between nonstop economic headlines, global uncertainty, and ongoing concerns about affordability, it’s understandable to wonder whether now is still a smart time to buy a home.

The good news is this: current events may be influencing the housing market, but they have not taken homeownership off the table. For many buyers, the opportunity is still there. It just may require a more thoughtful strategy than it did a few months ago.

Mortgage Rates Have Risen Slightly. Here’s What’s Behind It

After trending downward for much of 2025, mortgage rates have climbed again over the past month. Experts point to a mix of global events and broader economic pressures as key reasons why.

As Mark Fleming, Chief Economist at First American explains:

“Mortgage rates have recently moved higher, driven by geopolitical uncertainty and rising energy costs that are contributing to inflation concerns.”

So what does that mean if you’re thinking about buying a home? Should you wait for conditions to settle before making a move?

Not necessarily.

Your Opportunity To Buy Hasn’t Disappeared

There’s no denying that buying felt a bit more affordable when mortgage rates were closer to 6%. Now that rates are hovering in the mid-6% range, monthly payments are naturally a little higher.

But it helps to take a step back and look at the bigger picture.

For example, if you’re financing a $500,000 home, a rate in the mid-6s could still mean a monthly payment that is roughly $300 lower than what buyers were facing early last year.

That means today’s higher rates have not erased all the progress we’ve seen. In fact, buying a home can still be more affordable than it was just a year ago.

Yes, your payment may have been lower a few weeks ago. But trying to perfectly time the market rarely works in your favor. Conditions can shift quickly, and hindsight always makes past decisions look easier.

Instead of waiting for the “perfect” moment, focus on making the best decision based on your goals, finances, and today’s market conditions.

Expect Mortgage Rate Volatility

One thing buyers should be prepared for is continued movement in mortgage rates.

Rates may keep rising or falling in the weeks and months ahead as new economic reports are released and world events continue to unfold. That kind of uncertainty can feel frustrating, but it’s also part of today’s market.

The truth is, you can’t control what happens with inflation, global events, or mortgage rates next week. What you can control is how prepared you are when the right opportunity comes along.

That preparation can make all the difference.

If You Need To Move, You Still Have Options

For many buyers, the decision to move is not just about market timing. Life keeps moving, even when the market feels unpredictable.

Maybe your family is growing. Maybe you’re relocating for work. Maybe your current home no longer fits your lifestyle or needs. Those reasons still matter, and they may be more important than waiting for rates to change.

Buyers who are moving forward right now are often doing so because their personal situation makes it the right time.

And the good news is there are still strategies that can help make a purchase more manageable.

For example, some buyers are exploring adjustable-rate mortgages (ARMs) to secure a lower initial rate. That approach is not right for everyone, but it’s one example of how flexibility and planning can create opportunities in today’s market.

A Smart Plan Starts With the Right Experts

In a market like this, having a plan matters more than ever.

Working with a trusted real estate agent and lender can help you:

- Understand what you can realistically afford at today’s rates

- Review financing options, including ARMs and buyer assistance programs

- Stay informed as market conditions shift

- Make confident decisions based on your goals, not just the headlines

The right professionals can help you look beyond the noise and focus on what makes sense for your specific situation.

Conclusion

Uncertainty in the market does not mean you’re out of options.

If you need or want to move, buying a home may still be the right decision. The key is to go in with a solid plan, the right support, and a clear understanding of your financing options.

Homeownership is still possible. You just need the right strategy for today’s market.

Mortgage Rate Volatility: What You Can Control as a Buyer

Mortgage rates have been moving up and down lately, and that can make buying a home feel harder to plan for. When rates are unpredictable, many buyers wonder whether they should wait, move forward, or try to time the market.

Here’s the good news: while you can’t control where mortgage rates go next, you can control several factors that may help you secure a better rate. The first step is understanding what’s driving today’s market and knowing where to focus your time and effort.

Mortgage Rate Volatility Is Normal

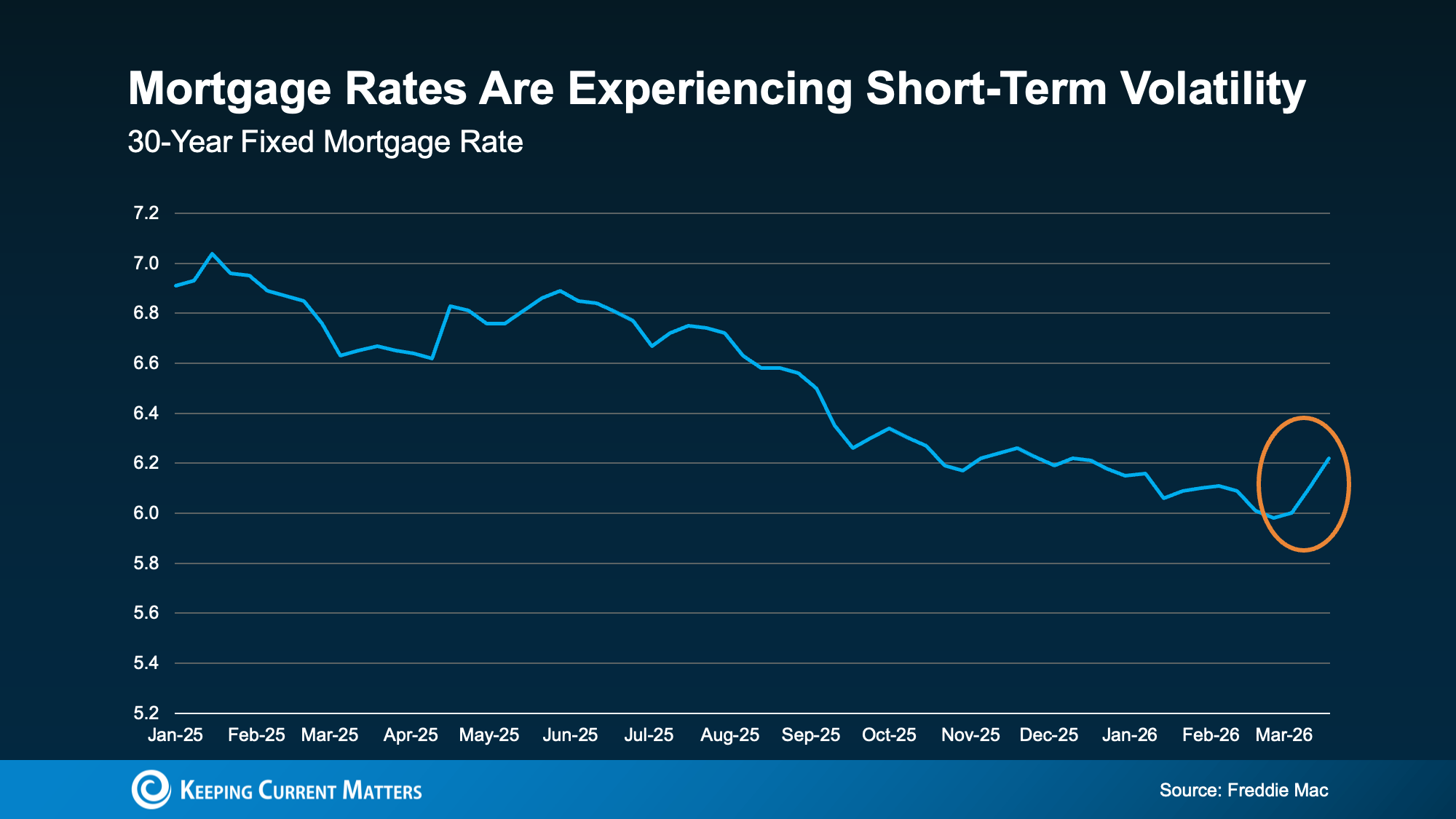

Recent data from Freddie Mac show that mortgage rates have been fluctuating. After trending downward for well over a year, rates ticked up again this month.

That kind of movement can feel frustrating, especially when you’re doing your best to budget for a home purchase. But occasional increases and decreases are a normal part of the mortgage market. Even over the past year, there have been periods when rates jumped before settling back down.

This is another one of those moments, and it helps to keep that in mind.

When there’s economic uncertainty or major global events unfolding, mortgage rates often respond quickly. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

That’s exactly why trying to predict the perfect time to buy usually doesn’t pay off. Rates can change fast, and waiting for the market to cooperate may not give you the outcome you want.

Focus on What You Can Control

You may not be able to influence the market, but you can take steps put yourself in a better position as a buyer. If your goal is to get the best mortgage rate possible, these are the areas that matter most.

Your Credit Score

Your credit score is one of the biggest factors that affects the rate you qualify for. In many cases, even a modest improvement in your score can lead to better loan terms and a lower monthly payment.

As Bankrate explains:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That’s why it’s worth taking steps to strengthen your credit before applying for a mortgage. Paying bills on time, reducing outstanding debt, and avoiding new credit inquiries can all help. If you’re not sure where your score stands or what improvements would make the biggest difference, a trusted loan officer can help you create a plan.

Your Loan Type

The type of mortgage you choose also affects your rate. There are many different types of loans, and each comes with different eligibility requirements, benefits, and pricing.

The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

This is why exploring your mortgage options is so important. A conventional loan may be the right fit for one buyer, while an FHA, USDA, or VA loan may offer better advantages for another. Comparing programs and speaking with more than one lender can help you understand which path makes the most sense for your financial situation.

Your Loan Term

The length of your loan term matters, too. Most lenders offer 15-year, 20-year, and 30-year mortgage options, and the term you choose can affect both your interest rate and your monthly payment.

Freddie Mac explains it this way:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

A shorter loan term may come with a lower interest rate, but the monthly payment is often higher. A longer term may give you more flexibility in your monthly budget, even if you pay more interest over time. The right choice depends on your goals, your budget, and how long you plan to stay in the home.

Conclusion

If you’re in the market for a home right now, the best strategy is not to focus on trying to predict where mortgage rates will go next.

Instead, focus on what you can control. Improve your credit score, explore different loan types, and choose a loan term that fits your needs. Most importantly, work with a trusted lender who can guide you through your options. If you need help connecting with trustworthy lender, reach out to us today.

Mortgage rates may be out of your hands, but the steps you take to prepare are not. And when you focus on what you can change, you give yourself a much better chance to move forward with confidence.