Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do You Need 20% Down? Most First-Time Buyers Pay Less

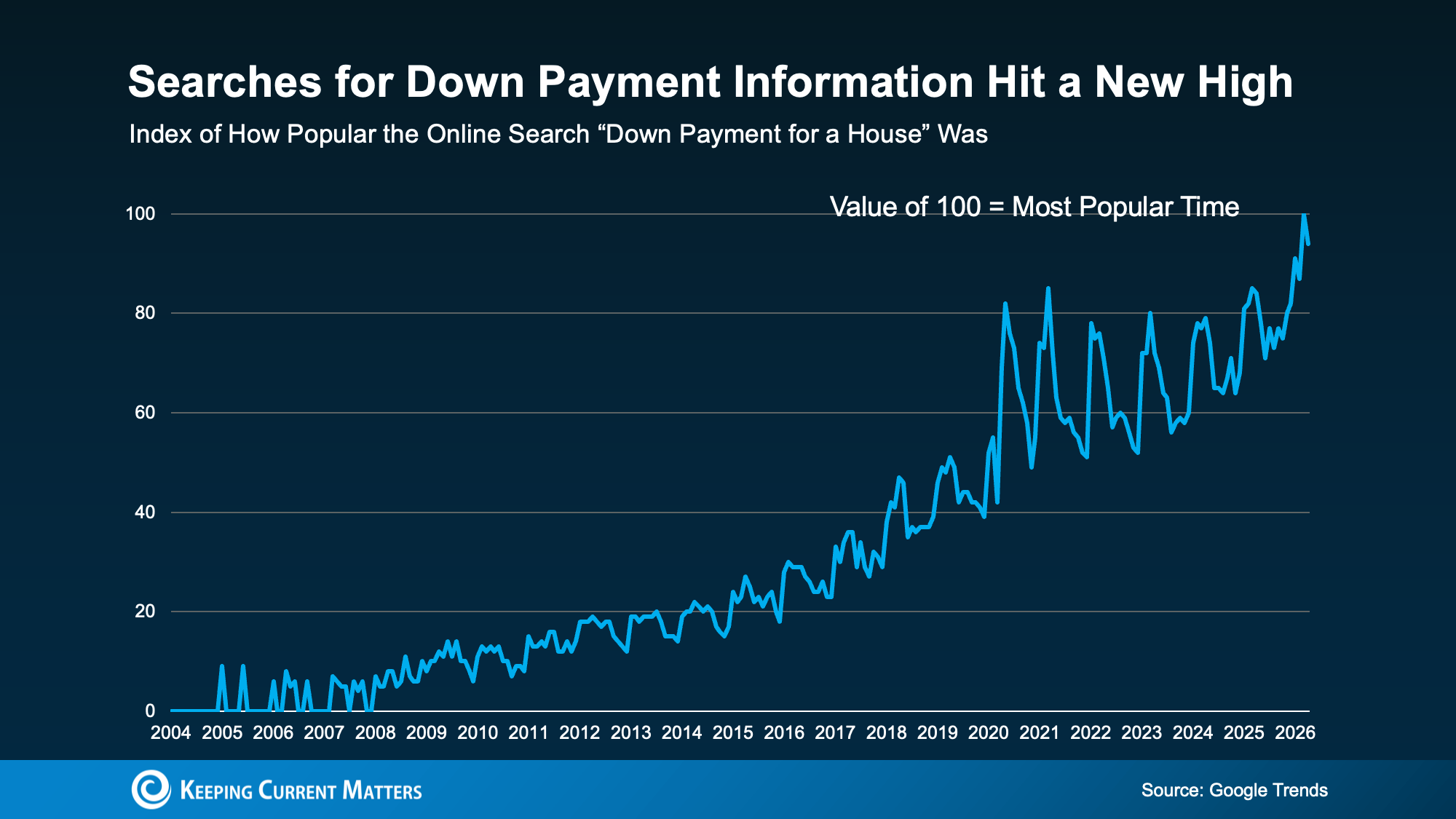

If you’ve been waiting to buy a home because you think you need a 20% down payment, you’re not alone. According to Google Trends, searches for house down payment information recently reached a new high, which shows just how many buyers are trying to understand what it really takes to get started.

The good news is that 20% down can be helpful, but it usually isn’t required. For many first-time homebuyers, the path to homeownership starts with a smaller down payment, the right loan program, and possibly even down payment assistance.

The 20% Down Payment Homebuying Myth

The idea that you must put 20% down to buy a home is one of the most common misconceptions in real estate. It’s easy to see why the myth sticks. A larger down payment can lower your monthly mortgage payment, reduce the amount you finance, and in some cases help you avoid private mortgage insurance.

But that doesn’t mean 20% is the minimum needed to buy a home.

Unless your lender specifically requires it, you may have options that call for far less money upfront. As The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For instance, FHA loans allow down payments as low as 3.5%. VA loans and USDA loans may offer zero down payment options for qualified buyers, including eligible Veterans and buyers purchasing in qualifying areas.

Saving for 20% can take longer than many buyers expect. If you’re delaying your plans only because you believe 20% down is a hard requirement, you may be waiting extra long to buy.

What First-Time Homebuyers Are Actually Putting Down

But if most first-time buyers aren’t putting down 20%, what are they putting down?

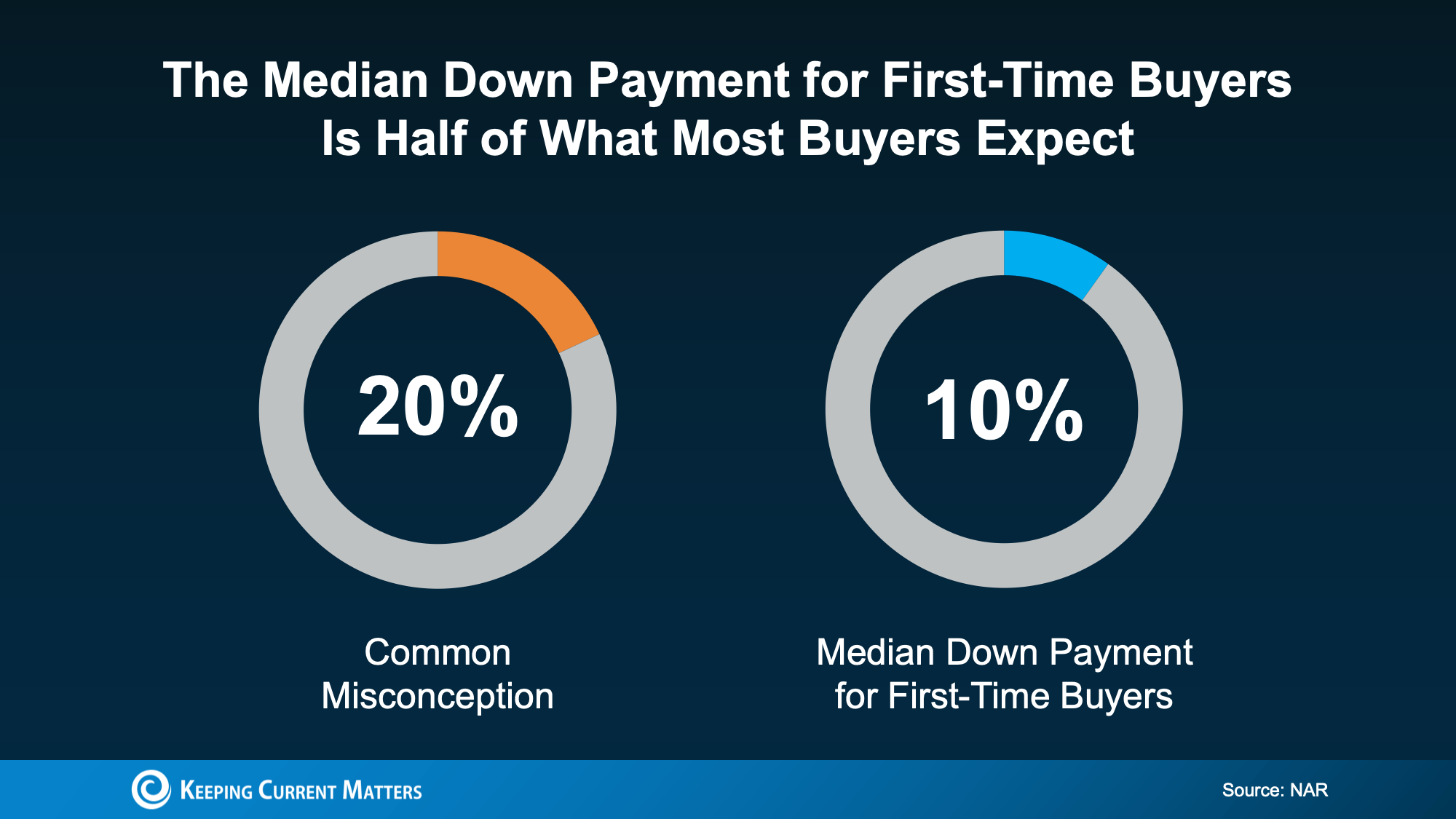

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is 10%. That’s half of the 20% many people assume they need.

This doesn’t mean 10% is the right amount for every buyer. Your ideal down payment depends on your credit, income, loan type, home price, monthly payment goals, and how much cash you want to keep available after closing.

But it does show that first-time buyers are finding ways to purchase without waiting until they have 20% saved. And for some buyers, the number may be even lower depending on the loan program they use.

Down Payment Assistance Could Help You Buy Sooner

There’s another reason the 20% myth can hold buyers back: many people don’t realize how much help may be available.

Down payment assistance programs are designed to help qualified buyers cover part of their upfront costs. These programs may come in the form of grants, forgivable loans, low- or no-interest second loans, tax credits, or other forms of support. Eligibility can vary based on income, location, property type, profession, or whether you complete a homebuyer education course.

Research from Realtor.com found almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% take advantage.

That gap is important. It means many would-be buyers may be leaving valuable assistance on the table simply because they don’t know what programs exist or how to apply.

In the U.S., there are more than 2,600 homeownership programs available, and many provide meaningful financial support. As Down Payment Resource explains:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

For some buyers, that kind of assistance could make a major difference. It may help cover part of the down payment, reduce closing costs, or make it easier to keep emergency savings intact after the purchase. In some cases, buyers may even be able to combine multiple programs for additional support.

The Bottom Line: Explore Your Options

Most first-time homebuyers do not put 20% down, and you may not need to either. While saving is important, the real question is whether you know which loan programs and assistance options fit your situation.

Before you rule out buying, connect with a trusted lender and a knowledgeable real estate professional. They can help you understand what you really need to save, what programs you may qualify for, and whether homeownership could be closer than you think.

It’s Tax Day – Here’s How a Refund Can Help You Save For a Home

If you’ve been planning to buy a house, you know how hard it can be to save for a home. What you might not know is that your tax return can be a helpful boost to your savings and budget. According to a recent post by Freddie Mac:

“ . . . your tax refund from the IRS can be a useful supplement to your homebuying budget.”

So if you’re planning to get a tax refund this year, consider the difference that extra funding can make. A refund can help you pay for the upfront costs of homebuying, like a down payment or closing costs. And, according to the IRS, your tax refund may even help you out this year more than ever.

How a Tax Return Can Help You Buy a Home in 2025

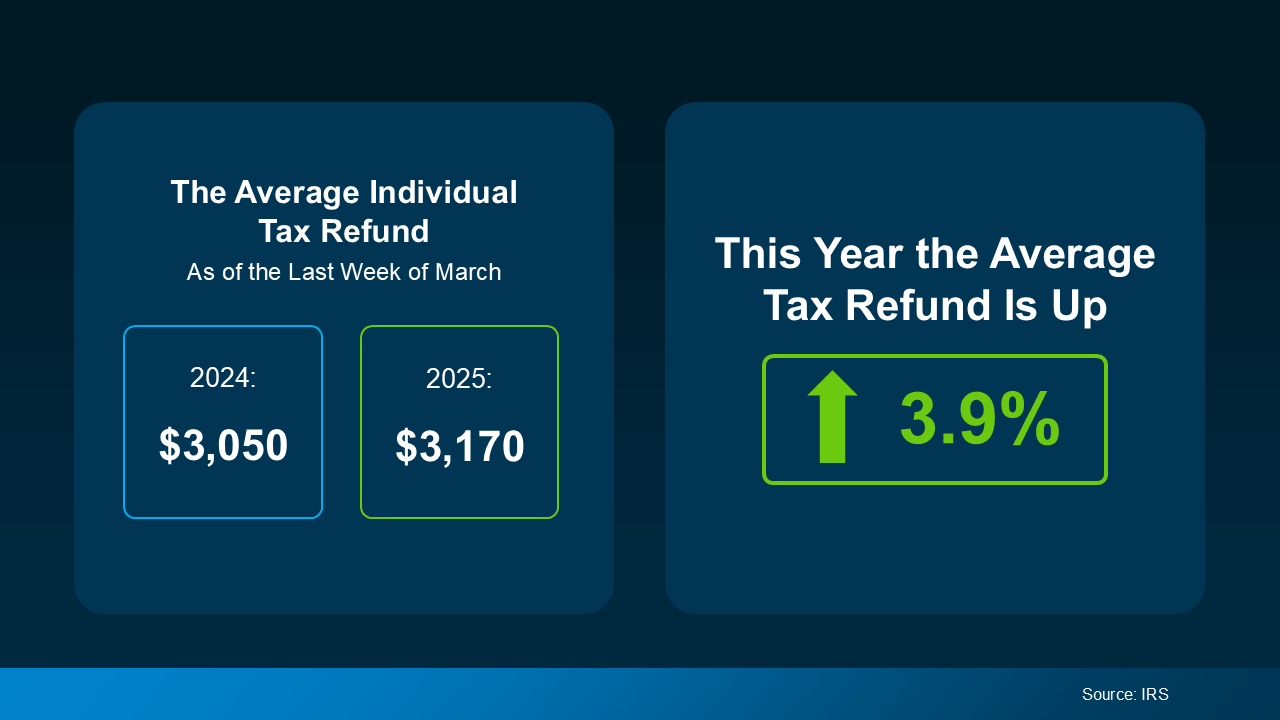

Recent data from the Internal Revenue Service (IRS) has found that the average individual’s refund is 3.9% higher this year. And while that’s not a huge increase, it can make a big difference if you’ve been struggling to save. The graphic below visualizes the new IRS data, comparing the average tax return in March 2024 to March 2025.

Your own personal tax refund will likely vary, but any financial boost helps when you’re saving for a home. According to Freddie Mac, the following are several ways you can put your tax return to good use when homebuying:

- Saving for a down payment – A down payment on a home is often one of the biggest obstacles to homeownership that buyers face. Saving your tax refund for a down payment can be a smart way to make this major step easier. Keep in mind while a 20% down payment may be common, it’s not typically a hard requirement to buy.

- Paying for closing costs – Usually due at closing, closing costs include fees for services like the appraisal, title insurance, and underwriting of your loan. While these vary by state, they’re often between 2% and 6% of your home’s total final purchase price. As a much lower percentage of your home’s price, closing costs can be a great use of your yearly refund..

- Lowering your mortgage rate – Lenders sometimes give buyers the option to buy down their mortgage rate if they qualify. This allows buyers to pay an upfront fee to lower their initial mortgage rate, reducing monthly payments in the short-term. This option can be particularly helpful if interest rates and mortgage payments are a major homebuying hurdle you’re facing..

Financially speaking, this may be more complicated in practice, but there’s no need to do it all on your own. Working with an experienced, trustworthy real estate professional can simplify your financial planning, helping you reach the best decision possible. An agent who understands the homebuying process, your unique financial needs, and your personal goals can make all the difference.

Conclusion

If you’ve been saving for a home, you already know well that every penny counts. Your tax return probably won’t be the final financial boost you need, but there are ways to use it effectively. Planning and identifying how to best spend that money can give you a real, meaningful step toward buying your home.

Are you eager to buy a home but having trouble making things work? Contact us today. We can connect you with local lenders and agents to help make your dream of homeownership a reality.