Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Saving for a down payment is often the biggest obstacle to buying a home. With the challenges of affordability today, it’s easy to wonder how anyone manages to save enough cash right now.

But here’s some good news: some buyers are getting into homes with smaller down payments than they may have expected.

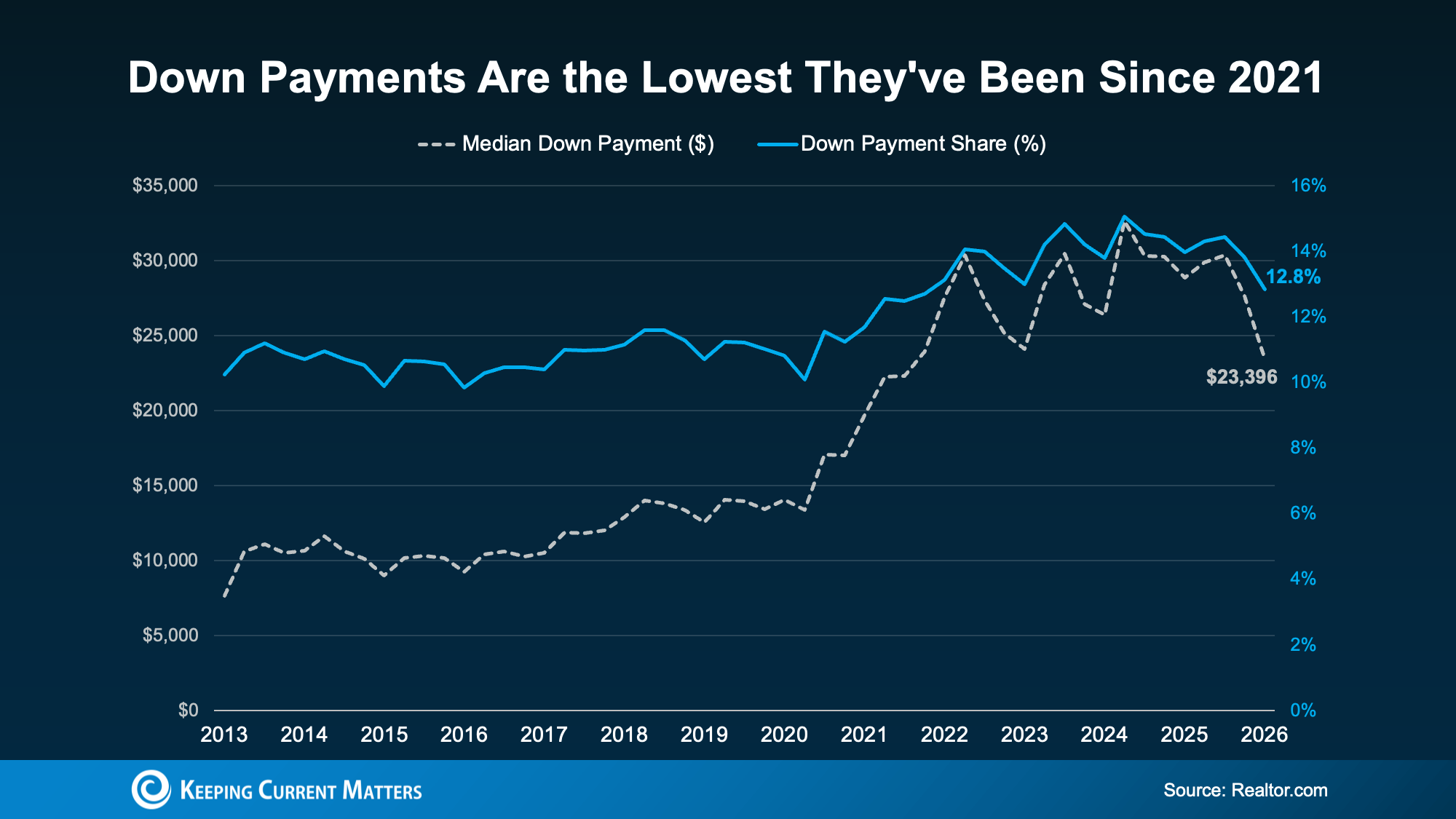

According to Realtor.com, the typical buyer put down about $23,400 in early 2026. That’s about $5,000 less than the year before, a 19% year-over-year drop. It’s also the lowest typical down payment level since 2021.

3 Reasons Why Down Payments Are Shrinking

Why are buyers putting less money down today? Three major shifts in the housing market are driving this trend:

-

Less Competition Between Buyers

In the most competitive markets of the past few years, some buyers felt pressure to put more money down to make their offers stand out.

Today, conditions are more balanced in many areas. With less intense competition, buyers are less pressured to offer a huge down payment to make an offer stand out.

-

Home Price Growth Has Moderated

Your down payment is typically based on a percentage of the purchase price. When home price growth slows or levels off, the dollar amount needed for a down payment can shift too.

In many markets, prices have cooled from the rapid pace seen in recent years. Some areas have even seen slight price dips. That can help reduce the upfront amount some buyers need to save.

-

More Buyers Are Using Lower Down Payment Loan Options

More buyers are also turning to loan programs that often require less money upfront. Government-backed loan options, like FHA loans and VA loans, often allow eligible buyers to purchase with a lower down payment or, in some cases, no down payment. According to Mortgage Professional America, FHA loans have made up more than 24% of purchase mortgages for five straight quarters, while VA loans recently reached their highest share in more than a decade.

Of course, not every buyer will qualify for every program, and any down payment is a huge amount of money to save. To make up the difference, buyers are relying on two things: payment assistance programs and family support.

Financial Help You May Not Know You Qualify For

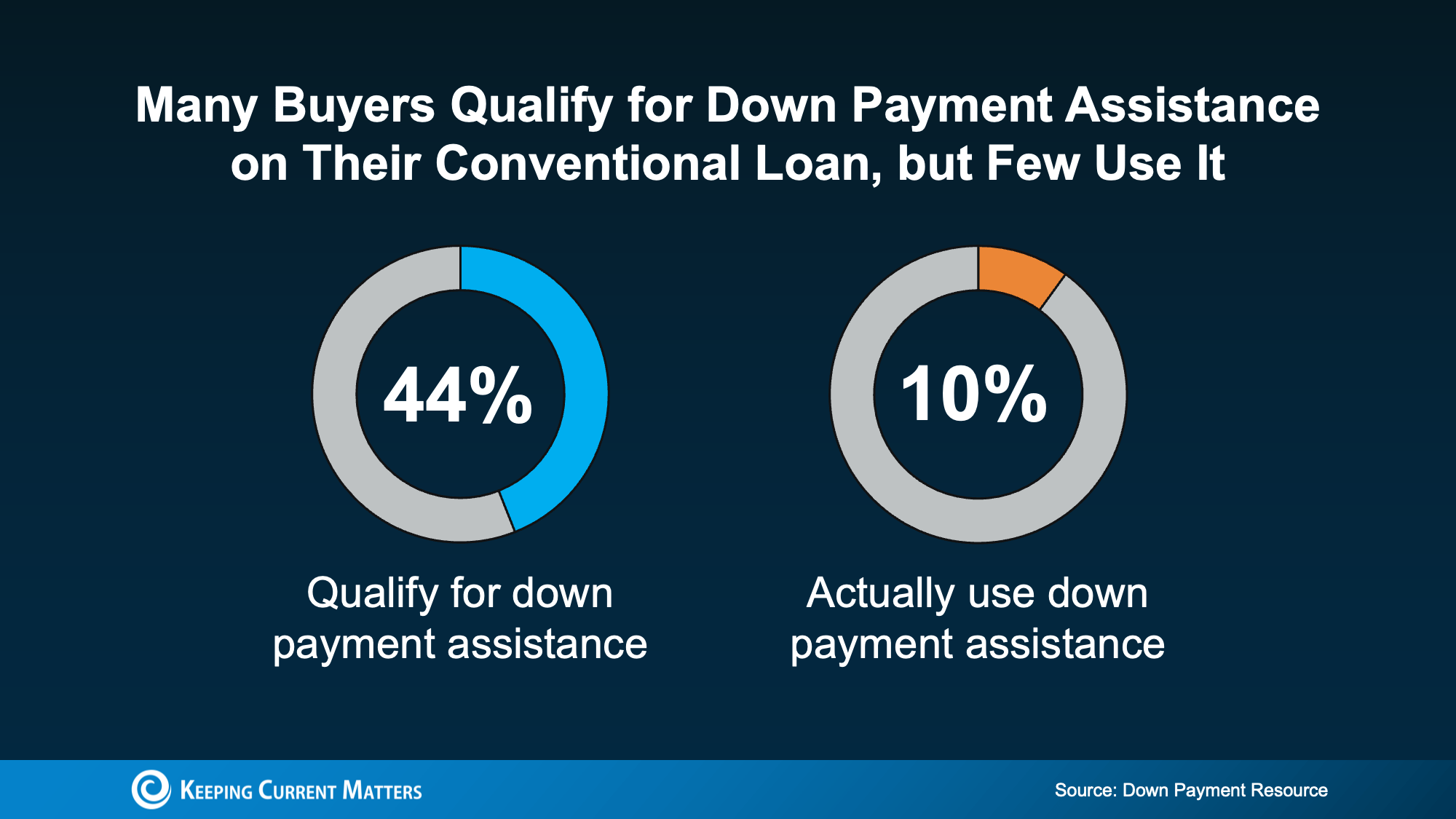

Down payment assistance is one of the most overlooked resources in real estate. A study by the Urban Institute and Down Payment Resource looked at the 10 largest U.S. metros and found that nearly 44% of recent buyers already qualified for a down payment program. Surprisingly, only 10% of those buyers actually used the help when closing on their loan.

There are more options available than many buyers realize. According to Down Payment Resource:

-

There are more than 2,600 down payment assistance programs available.

-

More than half (62%) are designed specifically to help first-time buyers.

-

38% have no first-time buyer requirement, meaning you may qualify even if you’ve owned a home before.

-

62% are open to buyers earning $100,000 or more.

So, don’t assume you’re priced out of a home or ineligible for help. A lender or knowledgeable real estate professional can help you ask the right questions and explore programs that may fit your situation.

A Helping Hand from Loved Ones

A growing number of buyers are also getting help closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support usually goes toward the down payment, followed by helping the buyer qualify for a mortgage and covering closing costs.

Chris Birk, VP of Mortgage Insight at Veterans United, explains it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

Not everyone has family or loved ones who are able to help. But for buyers who do, it can speed up how quickly they’re able to buy a home.

Bottom Line

Down payments are smaller than they’ve been in years, opening the door for more buyers to enter the market. Between down payment assistance programs and support from family, you may have more paths to homeownership than you realize.

Always consult with a trusted mortgage professional to review your financial situation. If you’re ready to start exploring neighborhoods and discussing your goals, contact our brokerage today to connect with an experienced local real estate agent.