Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If you’ve been shopping for a home lately, you’ve likely felt the pressure of today’s affordability challenges. Higher home prices and mortgage rates have made it harder for many buyers to stay within budget. That’s one reason adjustable-rate mortgages, or ARMs, are getting more attention again.

For some homebuyers, an ARM can offer welcome savings upfront. But before you go that route, it’s important to understand how these loans work, why they appeal to certain buyers, and what the long-term risks might be.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage is a home loan that starts with a fixed interest rate for a set number of years. After that initial period ends, the rate can adjust at scheduled intervals based on market conditions.

As Business Insider explains:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

That’s the biggest difference between a fixed-rate mortgage and an ARM. A fixed-rate loan offers predictability, while an ARM may give you a lower payment at first but less certainty later.

It’s true that costs like property taxes and homeowners insurance can still change with a fixed-rate mortgage. But the principal and interest portion of the payment generally stays steady. With an ARM, your monthly payment can rise or fall once the fixed period ends.

Why More Home Buyers Are Considering ARMs

The main reason buyers look at adjustable-rate mortgages is simple: lower initial costs.

Business Insider puts it this way:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

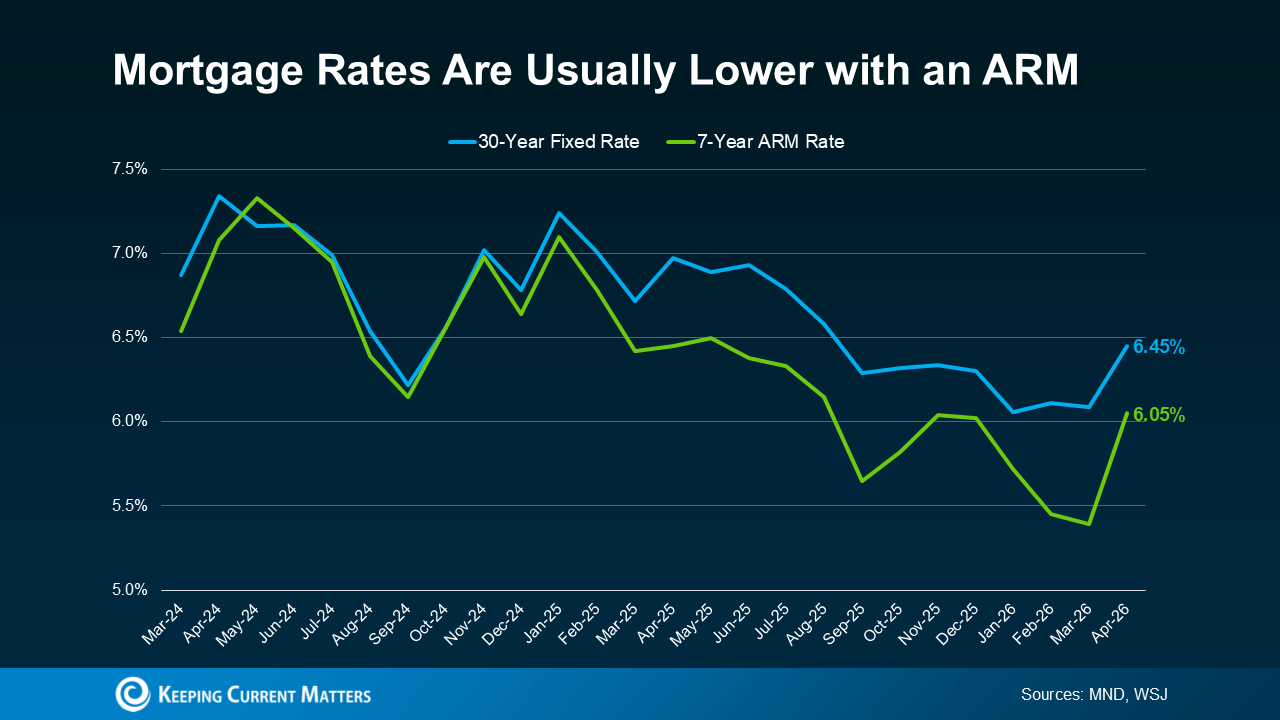

That upfront savings can matter, especially in a market where every dollar counts. Recent reporting from Mortgage News Daily and The Wall Street Journal show that ARM rates have been coming in lower than 30-year fixed mortgage rates.

For many buyers, even modest monthly savings can make a difference. For example, Redfin found that a typical buyer could save about $150 per month by choosing an ARM instead of a 30-year fixed mortgage. Savings like that can help some buyers qualify for a home sooner or make their monthly budget more manageable.

Why Adjustable-Rate Mortgages Are Making a Comeback

More homebuyers are deciding that a lower payment today is worth considering, even if it means taking on more uncertainty later.

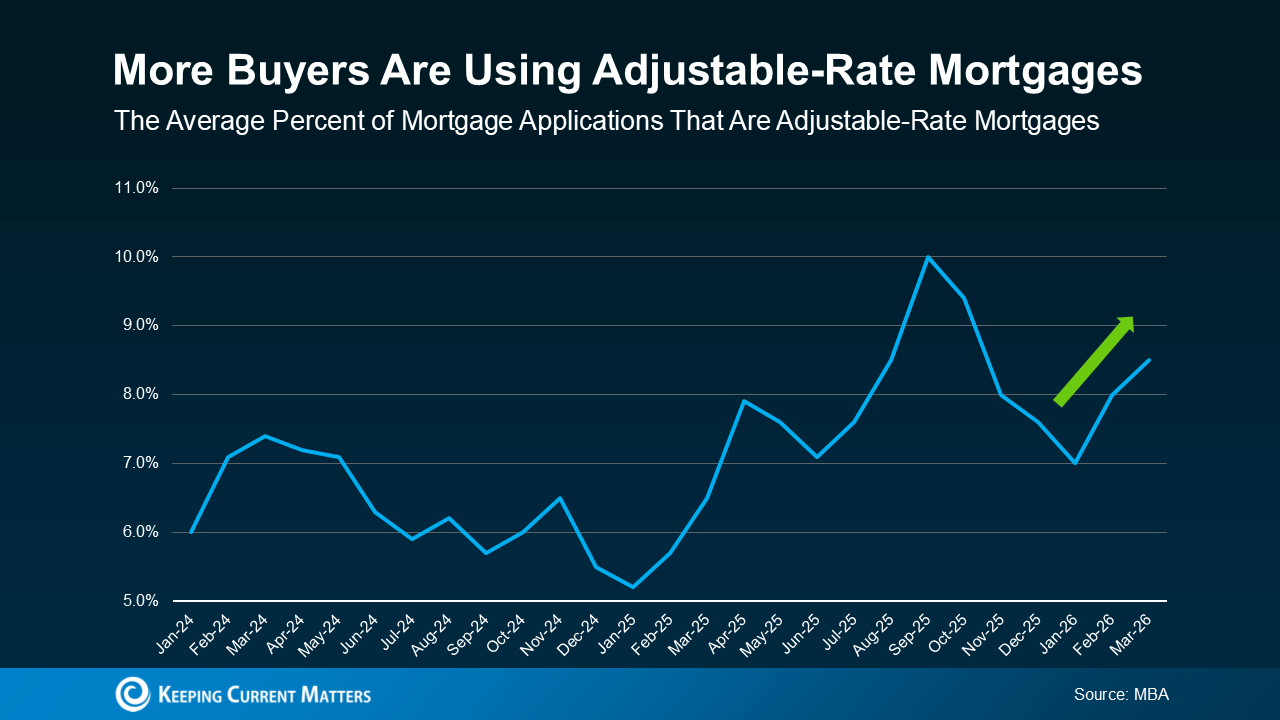

Recent reports from the Mortgage Bankers Association (MBA) show that the share of buyers choosing ARMs has increased in recent years. That doesn’t mean ARMs are becoming the right fit for everyone. But, it shows that some buyers are using them as a strategy to deal with affordability challenges in the current market.

For anyone who remembers the 2008 housing crash, this trend may sound concerning at first. But today’s lending environment is very different.

In the past, some borrowers were approved for loans they couldn’t realistically afford once the interest rate adjusted. Today, lending standards are tighter, and lenders generally evaluate whether borrowers could still manage the payment if rates rise. So while ARMs are becoming more common again, that alone doesn’t point to another housing crisis.

The Pros and Risks of an ARM

An adjustable-rate mortgage can make sense in the right situation, but it depends on your financial plan and your comfort with risk.

An ARM may be worth considering if:

- You expect to move before the rate adjusts.

- You believe your income will increase over time.

- You need a lower initial payment to make homeownership possible now.

Still, there are trade-offs to consider.

Once the fixed-rate period ends, your interest rate can change, and your monthly payment could increase significantly depending on where mortgage rates are at that point. There’s also no guarantee rates will fall in the future, which means refinancing later may not be as easy or as beneficial as some buyers hope.

That’s why it’s important to think beyond the introductory rate. Make sure you understand how long the fixed period lasts, how often the rate can adjust, and how much your payment could increase over time. Most importantly, talk through your options with a trusted lender and financial advisor before making a decision.

Bottom Line: Is an ARM Right for You?

Adjustable-rate mortgages are regaining popularity because they can make buying a home more affordable in the short term. For some buyers, that lower upfront payment can be a helpful tool. But an ARM isn’t necessarily the right move for everyone.

The best decision comes down to understanding how the loan works, weighing the risks, and making sure it fits your long-term goals.

If you’re considering an adjustable-rate mortgage yourself but are still on the fence, reach out to us today. We can connect you with a qualified lender in your area who explore your options with you.